01 April 2023 | Healthcare

The Great Unwind: How Governments are Preparing for the End of Continuous Enrollment

By workweek

Millions of adults and children in the United States may lose their Medicaid/CHIP insurance coverage. The continuous enrollment provision of the Families First Coronavirus Response Act, which has allowed Medicaid/CHIP enrollees to maintain insurance coverage, has officially begun to wind down as of April 1.

Millions have benefited from continuous enrollment, which means millions may now suffer the consequences of its end.

In this article, I’ll highlight the impetus of the continuous enrollment provision, discuss the impact of its end, and dive into what the federal government and states are doing to ensure the unwinding process runs smoothly.

The Deets

The Families First Coronavirus Response Act (FFCRA) has had a notable impact on enhancing insurance coverage, contributing to a historic low of 8% uninsured rate in the United States last summer (don’t get me wrong, 8% is still egregiously high for insurance coverage).

One of the essential measures in the FFCRA was the provision for continuous enrollment in Medicaid/CHIP, ensuring enrollees remain eligible for these programs until the public health emergency ends. This means that even if enrollees’ income increases beyond the qualifying limit for Medicaid, they can still keep their Medicaid/CHIP coverage.

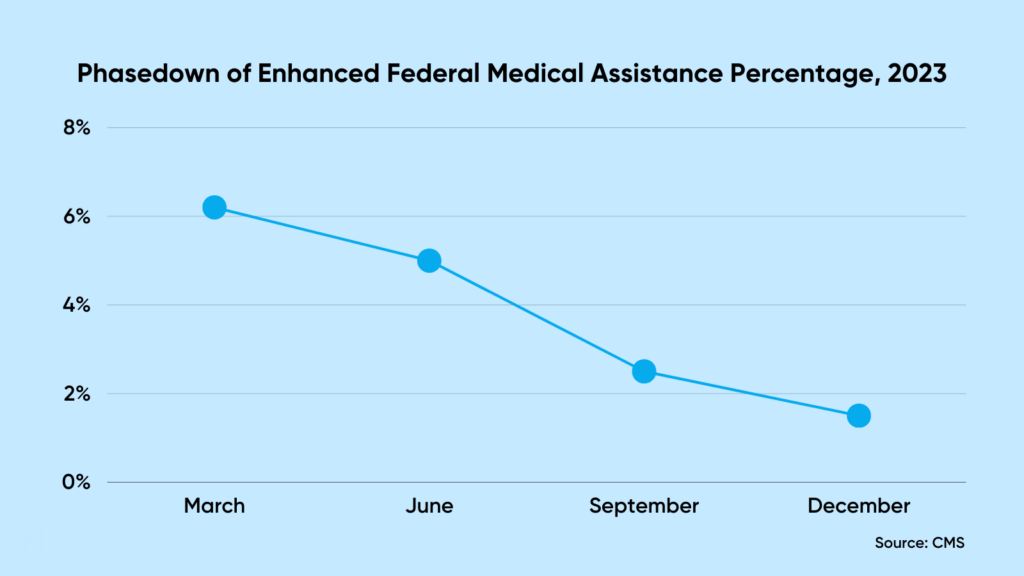

States evidently couldn’t front the money to keep significantly more people on Medicaid/CHIP, so the federal government helped them. By granting states a 6.2% boost in the federal share of Medicaid spending, the government helped them finance these programs on the condition that they adhere to specific regulations, such as keeping premiums at or below the level they were at on January 1, 2020. According to a KFF analysis, the 6.2% increase in the federal match rate for Medicaid/CHIP exceeds states’ cost of the program.

The key benefit of continuous enrollment is that it prevents churn. Churn occurs when individuals temporarily lose Medicaid coverage due to making too much income: they disenroll and then re-enroll when they make just enough income to qualify again for Medicaid. The renewal process, however, is a significant barrier to gaining Medicaid coverage. The process requires time off work, qualification criteria papers, and month-long wait times for approval, forcing Americans to abandon the Medicaid enrollment process.

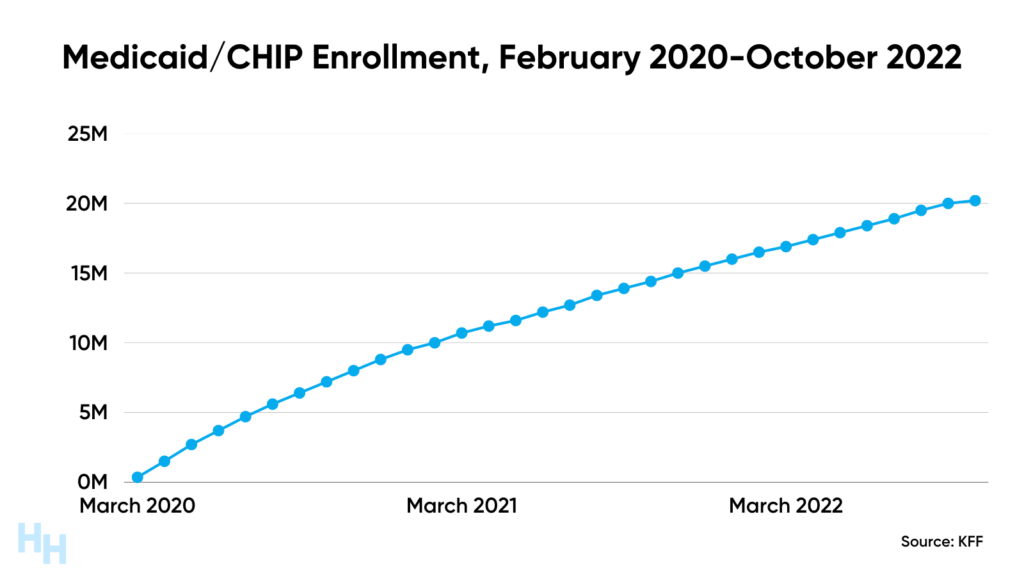

The FFCRA’s continuous enrollment provision led to a 28.5% increase in Medicaid/CHIP enrollment (Oct ’22 vs. Feb’ 20), covering 91.3 million adults and children. So what happens now that the continuous enrollment provision is winding down?

The End of Continuous Enrollment

The Consolidated Appropriations Act of 2023 put an end date (3/31/23) on the continuous enrollment provision. But, instead of millions of Americans losing Medicaid/CHIP coverage at once—like falling off a cliff—continuous enrollment will be phased out—like skiing down a long green trail.

The federal government will slowly decrease the federal match rate, which increased to 6.2%, throughout 2023. However, states must comply with specific rules that were also part of the FFCRA to continue to receive federal funding.

This “unwinding” will provide states sufficient time to work through their Medicaid/CHIP renewals and minimize the likelihood someone is booted off the program even though they qualify.

The impact of the end of continuous enrollment is significant. KFF surveyed state Medicaid officials and estimated that Medicaid/CHIP might lose between 5% and 13% of its enrollees—5.3 million to 14.2 million people. Even scarier is the Robert Wood Johnson Foundation statistic showing that 64% of adults in Medicaid-enrolled families surveyed didn’t know they may lose coverage once continuous enrollment ends. So, if you’re a physician or provider caring for Medicaid patients, bring this up the next time you see them!

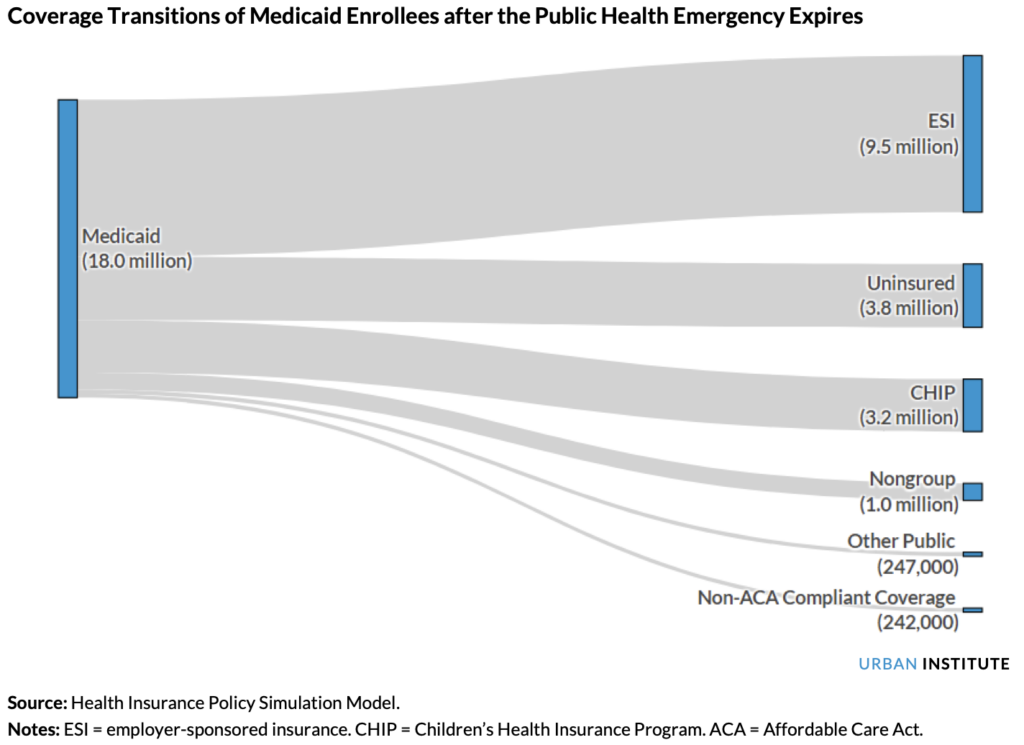

I’ll emphasize, however, that 5.3 million to 14.2 million adults and children may lose Medicaid/CHIP coverage but may not necessarily end up uninsured. The Urban Institute performed an insurance policy simulation model using recent household survey data on health coverage. The simulation model estimates 18 million Americans will lose Medicaid/CHIP coverage, around 4 million will become uninsured, and the rest will transition to other government insurance programs, employer-sponsored insurance, or ACA marketplace insurance.

Dash’s Dissection

Here’s my burning question:

- With the millions of Americans expected to lose Medicaid/CHIP coverage and a general lack of awareness among Medicaid/CHIP enrollees that they may lose coverage, what are governments doing to prepare for the efflux of enrollees?

Federal and state governments—and even Google—have implemented plans to prepare for the unwinding of continuous enrollment.

Federal Government

Knowing the unwinding process will burden states, CMS launched temporary waivers to ease the procedures and operations of states’ unwinding process. Specifically, this temporary waiver will help facilitate the renewal process for certain enrollees by allowing states to determine Medicaid/CHIP eligibility based on SNAP and TANF eligibility.

Since millions will inevitably be booted off of Medicaid/CHIP, CMS has created a Marketplace Special Enrollment Period for qualified individuals and their families. This special enrollment period will allow folks to enroll in Marketplace health insurance outside the typical annual open enrollment period. Note, the recent Inflation Reduction Act added $64 billion for a three-year extension of enhanced premium assistance for ACA insurance plans. So, those enrolled in Marketplace plans will have these tax credits through 2025.

State Governments

CMS has required states to develop and publish operational plans for their unwinding process. These plans include:

- How states will prioritize renewals.

- How long states plan to take to complete renewals.

- How states plan to reduce inappropriate coverage loss.

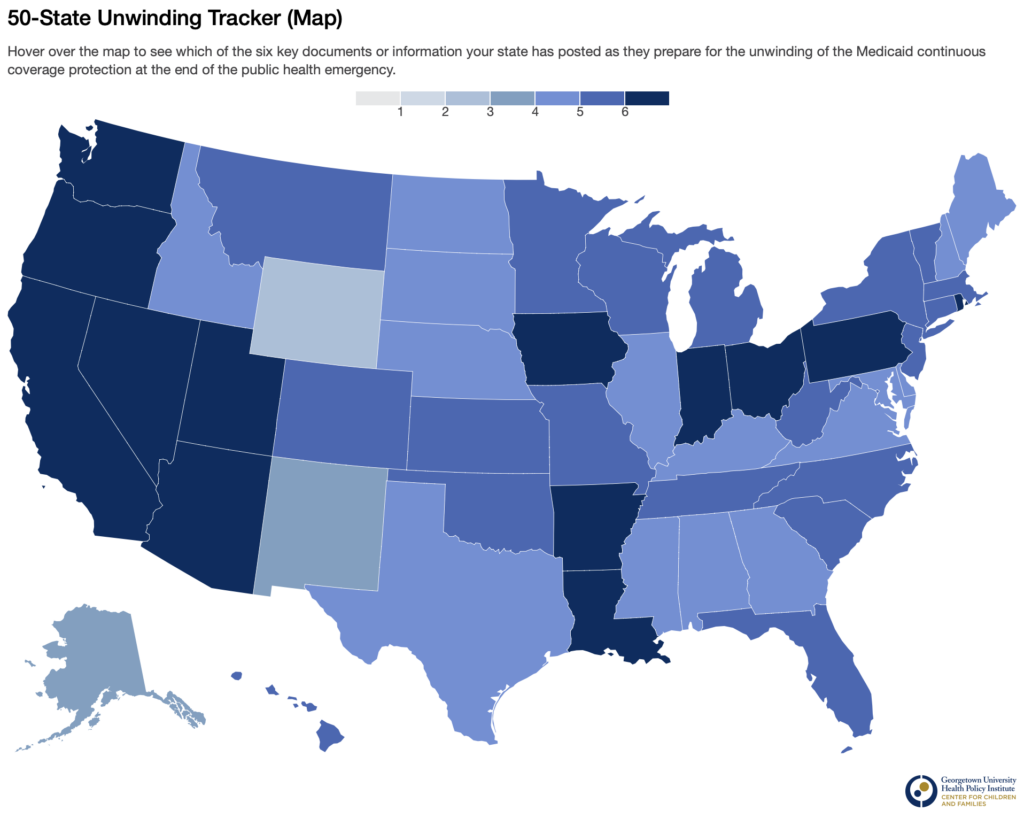

To track states’ progress in developing and publishing these operational plans, the Georgetown University Health Policy Institute launched its 50-State Unwinding Tracker. This tracker counts six key documents or information states have posted publicly regarding their unwinding procedures. These key documents include the state’s unwinding plan or a summary, an alert to update contact information, and an unwinding FAQ. Only 13 states have published all six key documents.

Additionally, several states have adopted and/or implemented Medicaid expansion during the pandemic, with North Carolina being the most recent state to adopt it. As of this newsletter, 41 states (including DC) have adopted the Medicaid expansion. Recall the ACA allows states to expand their Medicaid programs for individuals with incomes up to 138% of the Federal Poverty Level. In return, the federal government will increase its federal matching rate.

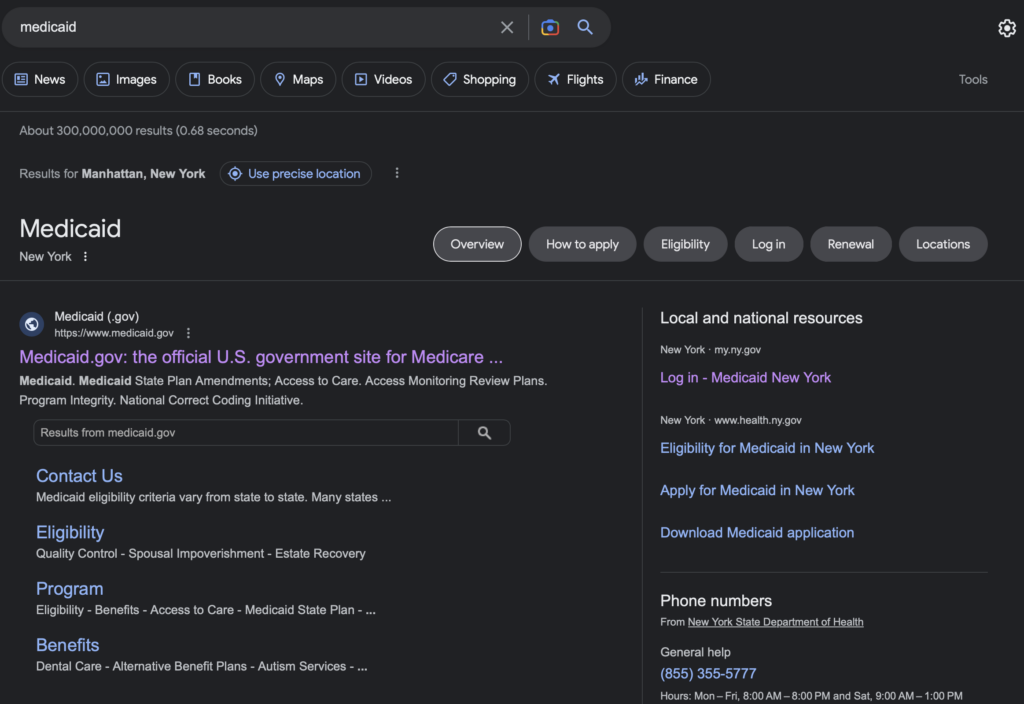

Lastly, Google has been boosting Medicaid info for several months to make individuals more aware of the unwinding of continuous enrollment and provide them with resources for Medicaid/CHIP renewals. For example, when you do a Google search for Medicaid, or a Medicaid-related term, information on your state’s Medicaid program is the first result, displaying tabs such as “How to apply” and “Renewal.”

Governments, as well as big tech like Google, have a critical role in helping individuals and families who lose their Medicaid/CHIP coverage find other options for health insurance. The consequences of losing coverage can be severe, as those without insurance often face poorer health outcomes and limited access to healthcare services. This can lead to delayed diagnosis of serious illnesses like cancer, which can significantly impact health and economic productivity. Additionally, when uninsured individuals receive healthcare services, providers are often not initially compensated, resulting in the government spending approximately $33.6 billion annually on uncompensated care.

In summary, the continuous enrollment provision in the Families First Coronavirus Response Act allowed Medicaid/CHIP enrollees to maintain coverage throughout the public health emergency, despite changes in income that would otherwise disqualify them from these programs. Consequently, millions more U.S. adults and children maintained insurance coverage throughout the pandemic. However, with the public health emergency ending in May, Congress has told states to officially begin unwinding their continuous enrollment, meaning they must redetermine who qualifies or does not qualify for Medicaid/CHIP. Millions are expected to lose Medicaid/CHIP insurance, but this doesn’t mean they’ll be uninsured. The federal government and states have enacted procedures to help streamline the renewal process or help those who no longer qualify for Medicaid/CHIP find insurance.

OUTSIDE THE HUDDLE

1) What’s Behind Hospitals’ Financial “Losses”

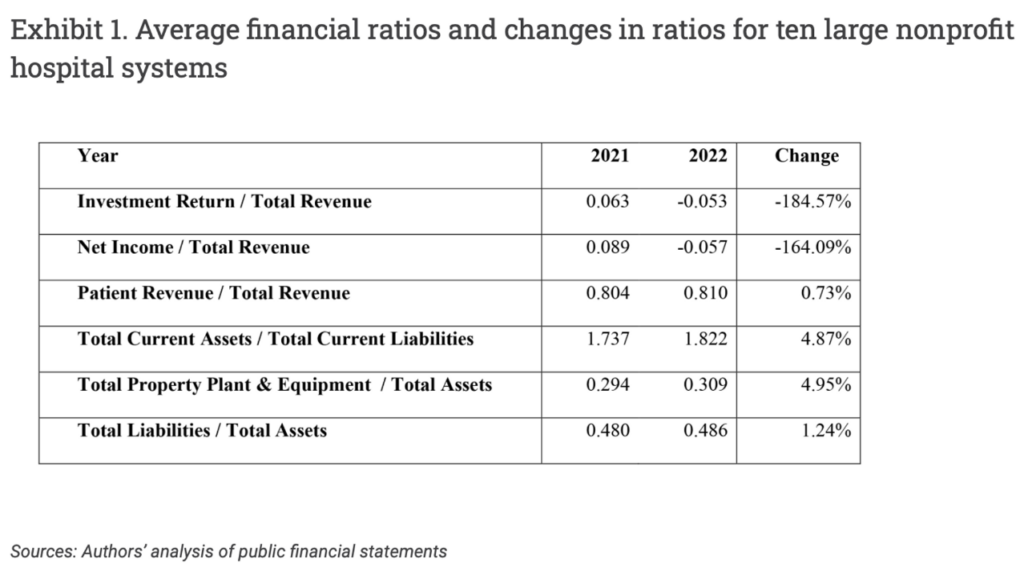

Researchers looked at recent quarterly financial statements from ten large non-profit health systems, finding that “labor shortages” weren’t the main driver of poor margins—it was investment losses. So if these hospitals’ risky financial investments are driving down margins, should the community (taxpayers) be fronting hospitals’ expenses, considering these NFP hospitals are tax-exempt? This is yet another paper shedding light on the community value of NFP hospitals. The value NFP hospitals bring to their communities isn’t black and white—it’s quite gray. Paul Keckley touched on the grayness in his recent newsletter here.

2) Ohio Attorney General Sues Healthcare’s ‘Modern Gangsters’

Ohio Attorney General David Yost filed a lawsuit against Cigna Group, Humana, and Prime Therapeutics for engaging in price fixing that harmed Ohio pharmacies and patients. He calls out PBMs as “modern gangsters … [that] have absolutely destroyed transparency, scheming in the shadows to control drug prices on all sides of the market.” I covered PBMs and the whole complexity of the drug supply chain here.

3) Trends in Primary Care with Guests Jared Dashevsky (me!) and Blake Madden

Blake and I had the privilege to join Affirm Health’s Katila Farley on the first episode of the company’s new podcast The Business of Primary Care. In the podcast, Katila, Blake, and I discuss how money drives change in healthcare and the importance of aligning incentives, the corporatization of primary care, and the shortage of primary care physicians. Give the episode a listen and let me know what you think!

If you enjoyed this deep dive, share it with colleagues. Sign up for the Healthcare Huddle newsletter here.