Good morning, Huddler! If you’re a fellow fourth-year med student reading this, just know I share the Match Day anxiety you may be feeling right now. This whole newsletter wasn’t written by me. My anxiety wrote it. In today’s Huddle: - The current state of U.S. healthcare.

- Key findings from McKinsey’s future of healthcare report.

-

Why the future of healthcare is UnitedHealth Group.

|

Was this email forwarded to you? |

|

|

The future of our workforce relies on innovation.

Ally Robotics is taking innovation and streamlined labor to the next level with a no-code robot arm fit to support several industries.

It sounds futuristic. But Ally Robotics is already building strong partnerships. Miso Robotics, the company behind a robotic fry chef, is currently in conversations to adopt Ally’s technology via a non-binding letter of intent.

|

Is the Future of U.S. Healthcare UnitedHealth Group? |

Key healthcare stakeholders like payers, providers, and pharmaceutical services continue to battle harsh economic conditions caused by labor shortages and inflation. As these stakeholders adapt to such conditions, we’re seeing a shift in profit pools. This shift, highlighted by McKinsey’s recent report on the future of U.S. healthcare, speaks to critical profit trends in healthcare.

In this article, I’ll describe the current state of U.S. healthcare, discuss key findings from McKinsey’s future of healthcare report, and try to convince you the future of healthcare is UnitedHealth Group (as first suggested by Dr. Eric Bricker). |

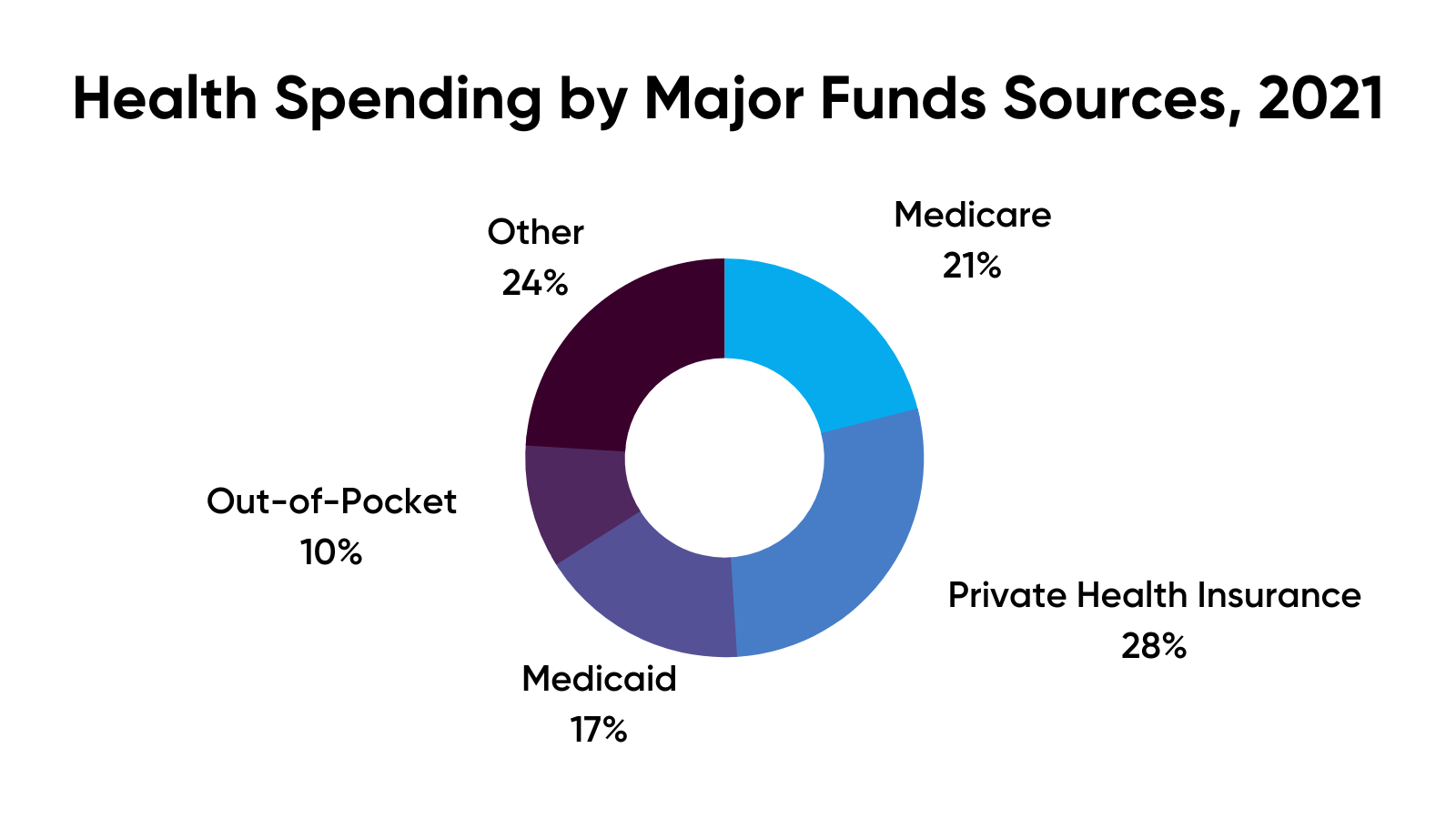

The Current State of U.S. Healthcare U.S. healthcare is still much the same as a decade ago, characterized by its high spending, egregious uninsured rate, and razor-thin hospital operating margins. National Healthcare Expenditures (NHE) in 2021 grew 2.7%, reaching $4.30 trillion. I can’t even explain that number because it’s unfathomable. While NHE in 2021 slowed compared to 2020 (which saw a 10.3% increase), it still made up 18.3% of gross domestic product. Below demonstrates where the money is coming from. |

Medicare NHE grew 8.4% in 2021, representing 21% of NHE by major funding source, with Medicare Advantage spending driving the growth (14.1% in 2021). MA is expected to make up 50% of all Medicare beneficiaries. Recall the MA market has been quite lucrative, making it an attractive area for providers, payers, and payviders (we’ll get to this soon).

While Medicare enrollment is growing with the aging population, Medicaid enrollment is about to decrease significantly, with the formidable Medicaid redeterminations starting in April. I covered the Medicaid cliff here, describing how the end of continuous enrollment may lead to millions uninsured. Currently, 8% of all Americans are uninsured.

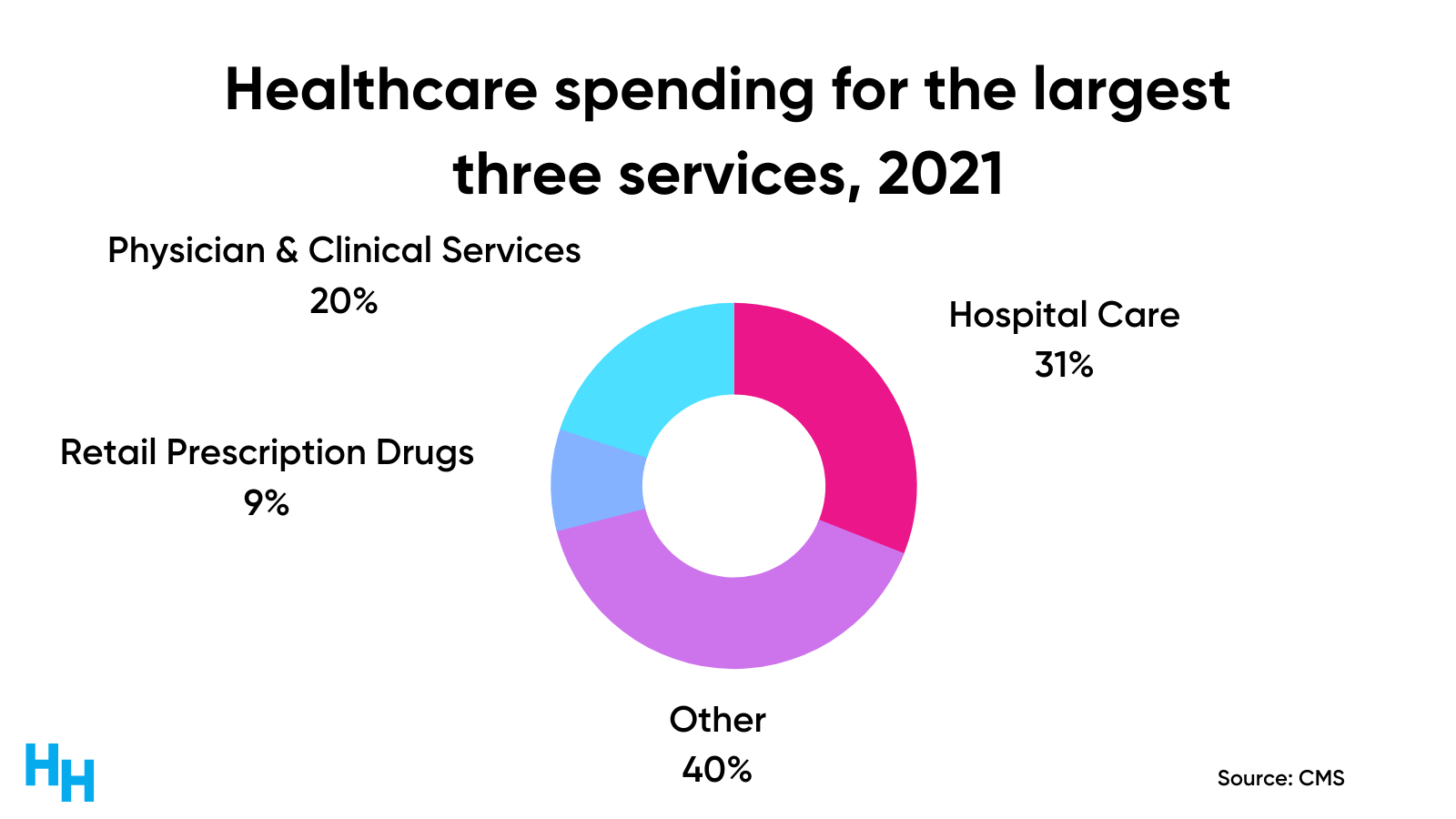

Lastly, hospitals experienced their most challenging year financially in 2022 due to high inflation rates and increased labor expenses. Nearly half of all U.S. hospitals ended 2022 with negative margins. However, revenue-driving areas in the outpatient setting increased, like surgical centers. So, given the current state of U.S. healthcare, what can we expect over the next couple of years? |

The Future State of U.S. Healthcare Profits

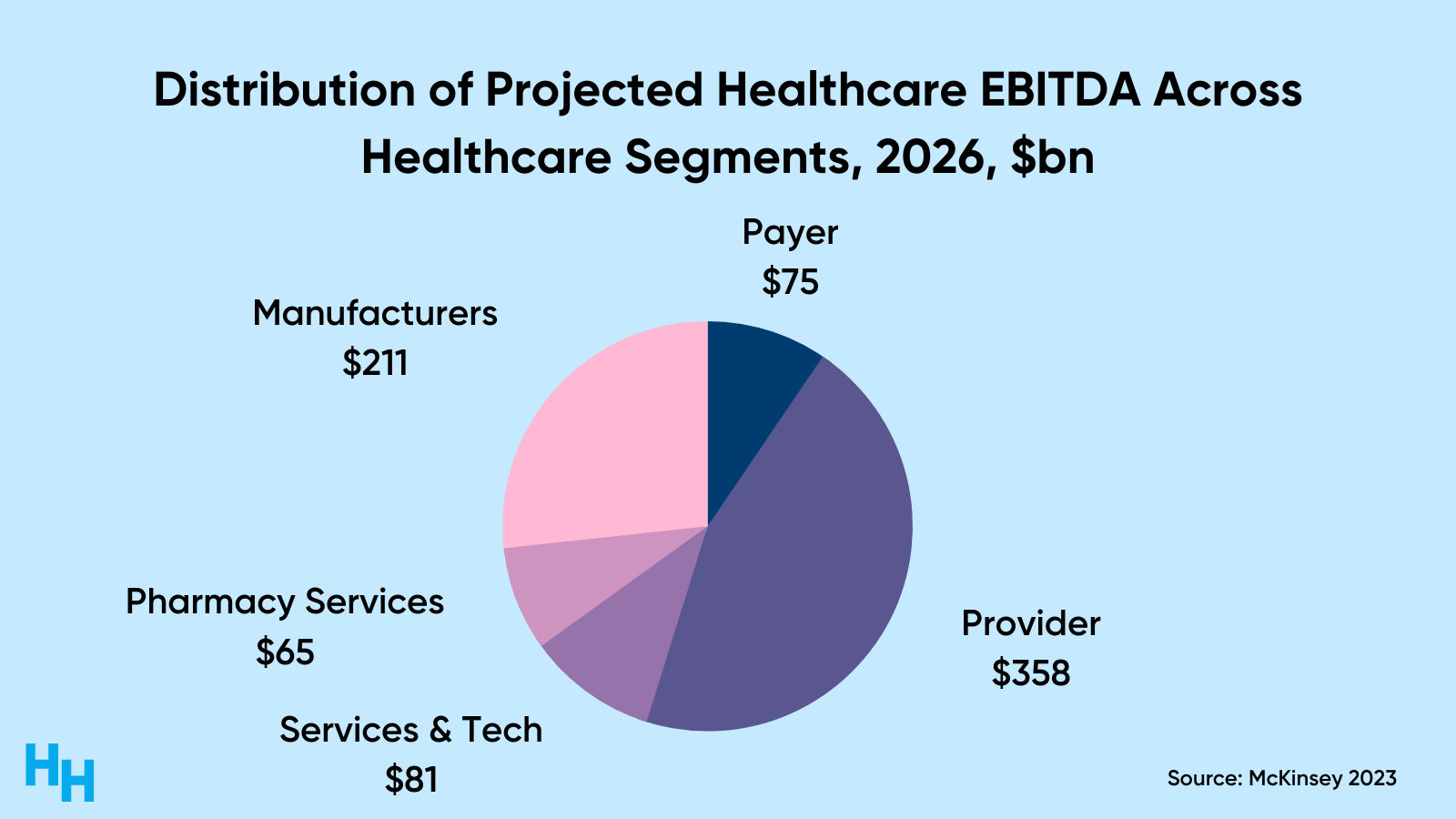

McKinsey researchers predict healthcare profit pools will grow at a 4% CAGR from $654 billion in 2021 to $790 billion in 2026. They break down profit pools into five different areas: |

Many profit pools are experiencing growth within each category, but I’ll highlight the fastest-growing ones, especially as they relate to trends I’ve discussed in previous newsletters. Payers

The payer profit pool is predicted to grow at an 11% CAGR, from $40 billion in 2021 to $75 billion in 2026. MA growth is driving these profit pools. Again, MA is a lucrative market since it allows payviders (UnitedHealth Group), for example, to take on high-risk (and highly reimbursed) patients while controlling costs to maximize profit. The government segment of the payer profit pool, which includes MA and Medicaid, is expected to be 50% greater than the commercial segment by 2026. Yes, the moneymaker will be government-funded (taxpayers, really) insurance—not private insurance.

Providers

The provider profit pools are estimated to grow at a 3% CAGR from 2021 to 2026, much lower than that of payers. But, the provider profit pool, which includes hospitals, office-based physicians, and post-acute care, will reach $358 billion by 2026—the largest of all profit pool segments.

The fastest growth within the provider profit pools comes from the office-based physicians, virtual healthcare, and pre-acute/non-acute segments. - Office-based physicians: Value-based care models’ profit pools are projected to grow at a CAGR greater than 10% between 2021 to 2026.

-

Virtual Care: Home health profit pools are expected to grow at a CAGR greater than 10% until 2026. I recently discussed the power of the home health movement here.

-

Pre-actue/non-acute: ambulatory surgical centers and retail clinics’ profit pools are expected to grow at a CAGR between 5 and 10% until 2026. Care in these non-acute settings has significantly higher margins (two to three times higher) than the acute setting. Hospitals and PE firms will continue to shift focus to these non-acute settings.

Services and Technology

Health services and technology profit pools are expected to have a 10% CAGR between 2021 and 2026, to $81 billion by 2026. Software (13% CAGR) and data & analytics (19%) drive this growth. These profit segments focus on patient engagement, clinical decision support, and workflow capabilities. I’ve discussed in previous newsletters that I’m bullish on digital health technology that focuses on improving clinical and non-clinical workflows. Bureaucracy is killing healthcare and the delivery of medicine. Health services and technology is an important sector that can improve efficiency in healthcare.

Pharmacy

Pharmacy services profit pools are expected to grow at a 3% CAGR from 2021 to 2026, reaching $65 billion. Leading the growth are the specialty pharmacy and infusion services profit pools. Physician office and ambulatory site infusion profit pools are predicted to grow 11% CAGR until 2026. Home infusion is also expected to increase between 5 and 10% CAGR. As medicine shifts to more patient-centered care (convenience), care will shift into the home and more convenient outpatient settings compared to the inpatient setting.

The McKinsey report provides a deeper analysis, but the trends I reported above will be the trends I’m following over the next couple of years and will continue to write about. |

Dash's Dissection

The future of U.S. healthcare is UnitedHealth Group (UHG). Or, at least, every large health insurer’s business models will mirror UHG’s.

UHG has already tapped into all of the critical profit pools I discussed. As Dr. Eric Bricker said in his video about the report: it’s as if McKinsey made the report for UHG.

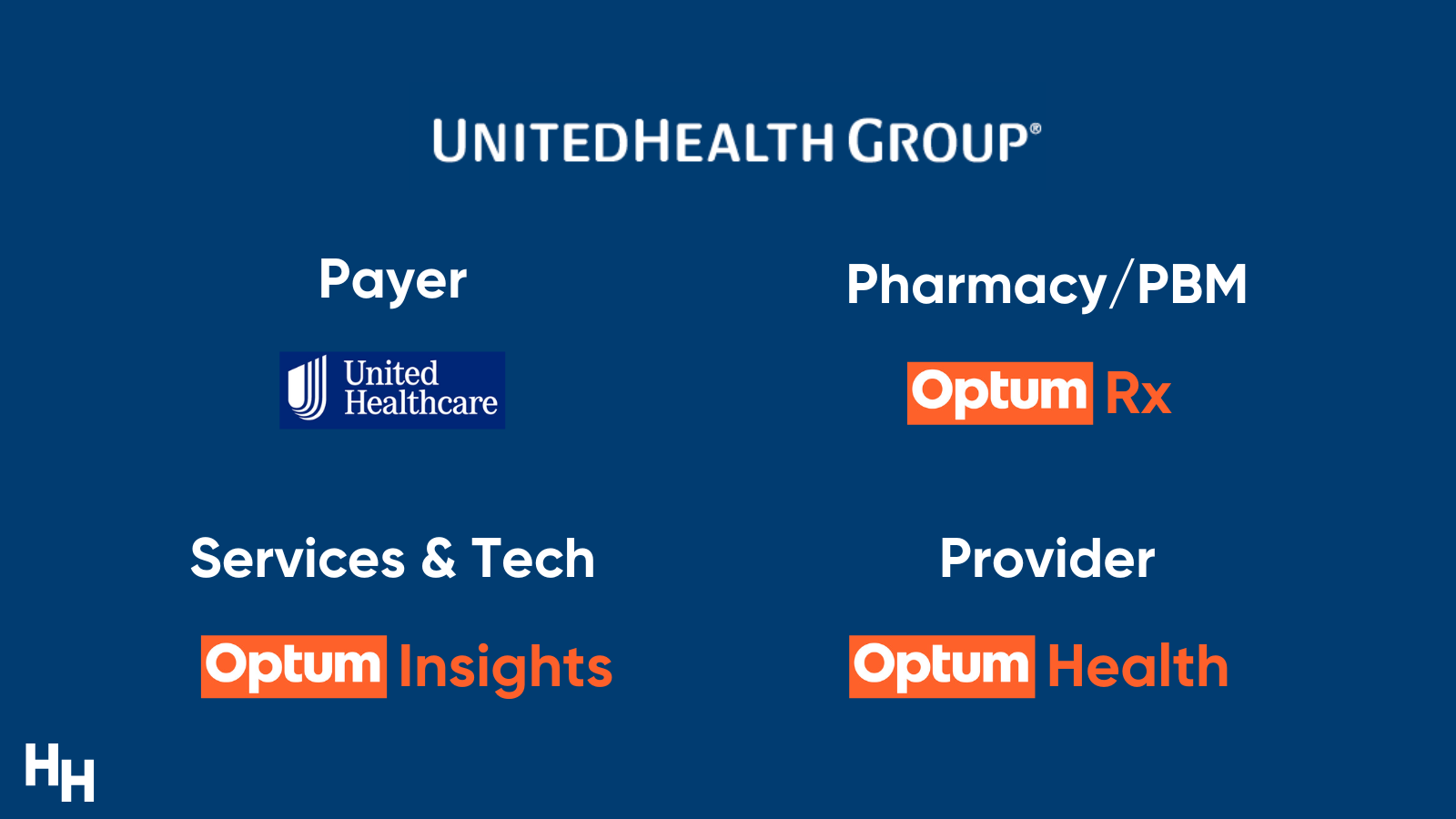

UHG has consistently squashed its competitors regarding profits, raking in $20.6 billion in profit last year. Its biggest competitor, Cigna, posted $6.7 billion. UHG isn’t just a “payer.” Far from it. UHG is a payer and provider and offers health services & technology and pharmacy services.

The graphic below shows how UHG’s different verticals align with nearly each profit pool category the McKinsey report focused on. Note UHG owns the largest share of PBM and Medicare markets (Medicare Advantage!) among its competitors. |

So, if McKinsey is saying government insurance segments, specialty pharmacies, virtual healthcare, and software & data profit pools will grow the quickest over the next few years, and UHG is already heavily invested in these areas, you’d think others should follow suit. And that they are.

CVS is following UHGs playbook; CVS has Aetna (payer), Caremark (PBM), CVSspecialty (specialty pharmacy), CVS pharmacy (regular pharmacy), Oak Street Health (health provider, recently acquired), Signify Health (home health). All CVS needs data solutions like Optum Insight, and then CVS will have completed the UHG Playbook.

Humana is another company following the playbook, as discussed by Blake here. What’s interesting about Humana is that the company is exiting the commercial insurance market. That’s just not where the money is at. But, as McKinsey reported, the government segment of the payer profit pool, which includes MA and Medicaid, is expected to be 50% greater than the commercial segment (e.g., private insurance) by 2026.

Follow the money.

In summary, as healthcare stakeholders adapt to harsh economic conditions, we’re seeing a shift in profit pools. McKinsey researchers predict healthcare profit pools will grow at a 4% CAGR from $654 billion in 2021 to $790 billion in 2026. Health services and technology and payer profit pools are predicted to grow the fastest at over a 10% CAGR until 2026. Interestingly enough, all of the fast-growth profit pools reported by McKinsey are the profit pools UnitedHealth Group has already tapped into. It’s as if the McKinsey report is a report on UnitedHealth Group. Given these trends, other large payers will follow UHG’s playbook.

|

|

|

PAST -

Are Digital Health Solutions Actually Solutions? (link)

- Prescription Predicament: How Three New Models are Tackling Drug Prices (link)

-

Do weight-management companies have a future? (link)

|

|

FUTURE - Match Day and the official launch of a new project I’ve been working on (see bottom of email).

- Why physician-owned hospitals don’t exist, for better or for worse.

-

What the end of continuous enrollment means for millions of patients, physicians, and health systems.

|

|

|

1) The Public Health Emergency is Ending: What Does it Mean for Digital Health?

Health and wellness investor Jess Schram wrote a comprehensive article about the impending impact of the public health emergency’s end on digital health companies. She covered the recently-proposed DEA rules that involve rolling back pandemic-related telemedicine flexibilities for controlled substances. Hundreds, if not thousands, of digital health companies have built business models around these pandemic-related telehealth regulation flexibilities. Consequently, populations who previously lacked access to substance use disorder treatment, for example, could access care via these digital health services. So what happens now once these flexibilities revert to stricter regulations? Check out Jess’s article here.

2) How the University of Kansas Health System Will Use Generative AI

The University of Kansas Health System formed a partnership with AI health tech company Abridge to integrate its generative AI technology across 140 provider locations. Abridge’s technology analyzes provider-patient conversations to write provider notes (H&P, progress notes) in the provider’s desired format. So, the provider doesn’t need to write their note after seeing a patient since the AI tech already did it for them in the format they use. This partnership is a prime example of bridging (ha!) AI tech and medicine to streamline clinical workflows. I wrote about the impact of generative aI and healthcare here.

3) Weight Watchers and Noom Enter the GLP-1 Market

Weight Watchers and Noom moved into the GLP-1 medication space to remain competitive with the hundreds of other weight-management companies’ solutions offering GLP-1 medications. Weight Watchers will acquire chronic weight management telehealth startup, Sequence, for $132 million, valuing each Sequence member at around $4,500. Wow. Noom, on the other hand, silently announced it would offer GLP-1 meds to select members. You'll be toast quite soon if you’re in the weight management space and not offering GLP-1 meds. But, when every company is advertising GLP-1 meds for “weight loss,” how will they differentiate themselves to survive? I explain more here.

|

|

|

Here are some jobs that I’m curating for the healthcare industry. Use this link to submit your role to be featured if you’re looking to hire.

Teleradiologist, Mayo Clinic

Our favorite health system, Mayo Clinic, is seeking a remote radiologist. Do I even have to give reasons to work for such a robust health system like Mayo Clinic? |

|

|

I’ve been working on a project that I think will be super helpful for all of us incoming and current residents. It’s a personal finance guide covering everything from budgeting to investing. I’ve put much effort into making this guide as comprehensive and easy to understand as possible, so I’m excited to share it with you all. If you’re like me, you might feel a little overwhelmed by all the financial responsibilities of being a resident. But trust me; this guide has everything you need to get on track and start building a solid financial foundation. Plus, it’s written specifically for graduating medical students and residents, so you know it’s tailored to our unique situation. I plan to launch the guide officially next Sunday after Match Day, but I wanted to give you a sneak peek. I hope you find it as helpful as I have!

If you’re interested in checking it out, click here 😉. |

|

|

Next week’s newsletter will be a bit different. I’ll dive into a new guide I put together for graduating medical students and residents (see section above). Plus, I’ll announce where I’ll be going for my internal medicine residency! Keeping it simple, Jared |

|

|

Get your brand in front of 20,750 doctors, nurses and healthcare decision-makers |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|