18 March 2024 | FinTech

NFTs are Officially Over

By Alex Johnson

3 Fintech News Stories

#1: WOW! This seems unsustainable!

What happened?

MoneyLion introduced a new premium subscription:

Priced at $9.99 a month, MoneyLion WOW offers members exclusive benefits like cash back on first- and third-party products and offers. Together, these can add up to hundreds of dollars in benefits each year, according to a presentation released Thursday in conjunction with the earnings call.

For MoneyLion, the premium subscription offering is expected to increase the company’s total addressable market, increase recurring revenue, boost product adoption and deepen customer engagement, the presentation said.

“Any WOW member will be very clearly incentivized to consolidate their financial lives with MoneyLion,” [Dee] Choubey [CEO of MoneyLion] said during the call.

“We want to become the most trusted go-to marketplace for financial decisions, and our WOW membership is a step in that direction, providing unique value at a great price,” he added.

So what?

I’ve been critical of MoneyLion in the past, but at least back then, I understood exactly what I was criticizing – a neobank that was making some dicey choices in search of profitability and increasing customer LTV.

Today, I don’t even know what MoneyLion is.

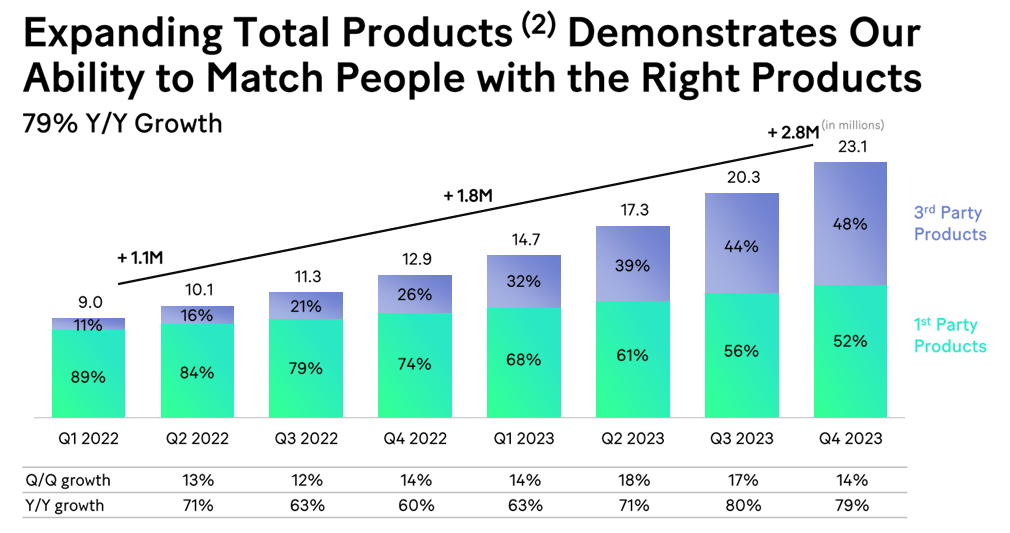

In addition to its first-party products (banking, cash advances, investing, etc.), it has built a marketplace and set of PFM capabilities (kinda like Credit Karma), from which it generates referral fees. From what I can tell, the marketplace business has been the primary driver of most of the company’s “growth” (a term that I put in quotes because MoneyLion uses some pretty funky accounting when it comes to defining customers, products, and EBITDA) for the last couple of years:

Look at those green bars! That doesn’t seem like a great trend, and it makes the idea of a premium membership tier a little weird.

What does a MoneyLion user get for paying $9.99 a month? From what I can tell, it’s mostly a combination of reduced fees on MoneyLion’s first-party products (not worth $10/month on its own) and cashback offers from the third-party providers in the marketplace (there’s no information on MoneyLion’s website about how much these cashback offers will be or when users should expect to see them).

On the company’s most recent earnings call, the CEO said, “As we continue getting more partners, the value proposition becomes irrational for anyone not to have the MoneyLion WOW membership.”

I guess that’s possible, but personally, I don’t see it. MoneyLion strikes me as a company that’s so focused on monetizing its customer relationships, that it has stopped caring about earning those relationships.

#2: Is it worth building a standardized business credit score?

What happened?

Worth AI, a new fintech infrastructure company, raised some money and emerged from stealth:

The company’s team, which already numbers more than 40 employees, has one mission: to standardize business credit scores. That way, lenders can have a more holistic view into the health of businesses, and entrepreneurs can have better access to capital — without as much interference from human bias.

One of the biggest struggles for financial institutions that are underwriting small businesses, [Suneera] Madhani [Co-founder and Co-CEO of Worth AI] says, is having to rely on the personal credit scores of founders and owners. “There isn’t a standardization on the business credit score,” she says. “One of the reasons why it’s been missing in the marketplace for so long is because no one’s had that real-time access to that financial data.”

The recent advances in generative AI, the co-founders say, can change that dynamic, allowing their platform to aggregate more than a thousand data points from sources like tax returns, bank accounts, QuickBooks, Stripe, secretaries of state, enterprise systems planning software, and even social media. Worth AI tabulates all of that information and updates it continuously, so that lenders can expand or restrict credit access on the basis of recent business performance.

So what?

The Co-founders and Co-CEOs of Worth AI – Suneera Madhani and Sal Rehmetullah – have an impressive track record (they previously co-founded Stax, a payment processing company), and I’m not surprised that they were able to get funding for this new venture.

I will be a bit surprised if their vision – a standardized business credit score – ends up getting significant traction in the market.

As I’ve written about previously, the problem with business lending is that, unlike consumers, businesses aren’t homogenous from a credit risk perspective. A 12-person bakery in Naples, Florida, is very different from a 25-person VC-backed healthtech startup in San Rafael, California. That’s not a problem that can be solved by acquiring more data or building smarter algorithms. It can only be solved by specialization.

Small business lending doesn’t need one standardized credit score. It needs hundreds or thousands of niche credit scores.

#3: NFTs are Officially Over

What happened?

Starbucks is shutting down its NFT-based loyalty program:

In late 2022, Starbucks dipped its toes into the world of Web3 with a beta launch of its new NFT rewards program, Starbucks Odyssey. It has remained as a closed, invite-only beta ever since.

However, according to a recently updated FAQ on the official Starbucks Odyssey website, it seems that the NFT reward program will never leave beta. That’s because Starbucks is killing it.

According to the website, the Starbucks Odyssey program will officially end on March 31. Users in the closed beta have until March 25 to complete any remaining Journeys, which were “themed activities” like online games and quizzes that enabled members to earn NFTs and reward points. The project’s Discord channel, a major element for any Web3 community, will be shut down on March 19.

So what?

NFTs always struck me as a social psychology experiment dressed up as a business concept – what’s the most transparently, aggressively dumb crypto-related thing we can convince consumers and businesses to take seriously?

However, my pessimism was tempered by the enthusiastic participation of people and companies that I take very seriously. Starbucks was at the top of this list. Surely, I thought, if Starbucks (designer and operator of one of the most successful rewards programs in the history of capitalism) sees value in NFTs as a mechanism for capturing consumer engagement and building brand affinity, I must be missing something.

Nope!

Turns out that Starbucks was just as fooled by the baffling rise of NFTs as the rest of us. ZIRP is one hell of a drug!

With this news, I think I’m now officially ready to close the book on NFTs.

2 Fintech Content Recommendations

#1: How To Be(come) A Great Partner Bank In The BaaS Space (by Ron Shevlin, Forbes) 📚

A great overview from Mr. Shevlin on what banks that are still serious about BaaS (and yes, there are still some) should be doing to position themselves well for the future. Take some time to read this one (and download the report that it’s based on).

#2: All Eyes on Silicon Valley Bank (by Eric Newcomer & Madeline Renbarger) 📚

I was sad to miss this summit, but this is a useful summary of the key takeaways. The one on relationship banking was particularly interesting to me.

1 Question to Ponder

Who is the world’s most knowledgeable person when it comes to the design and production of physical debit and credit cards?

I want to nerd out on this topic, and I’m looking to chat with the expert.