08 January 2024 | FinTech

Tally Isn’t Adding Up

By Alex Johnson

3 FINTECH NEWS STORIES

#1: Tally Isn’t Adding Up

What happened?

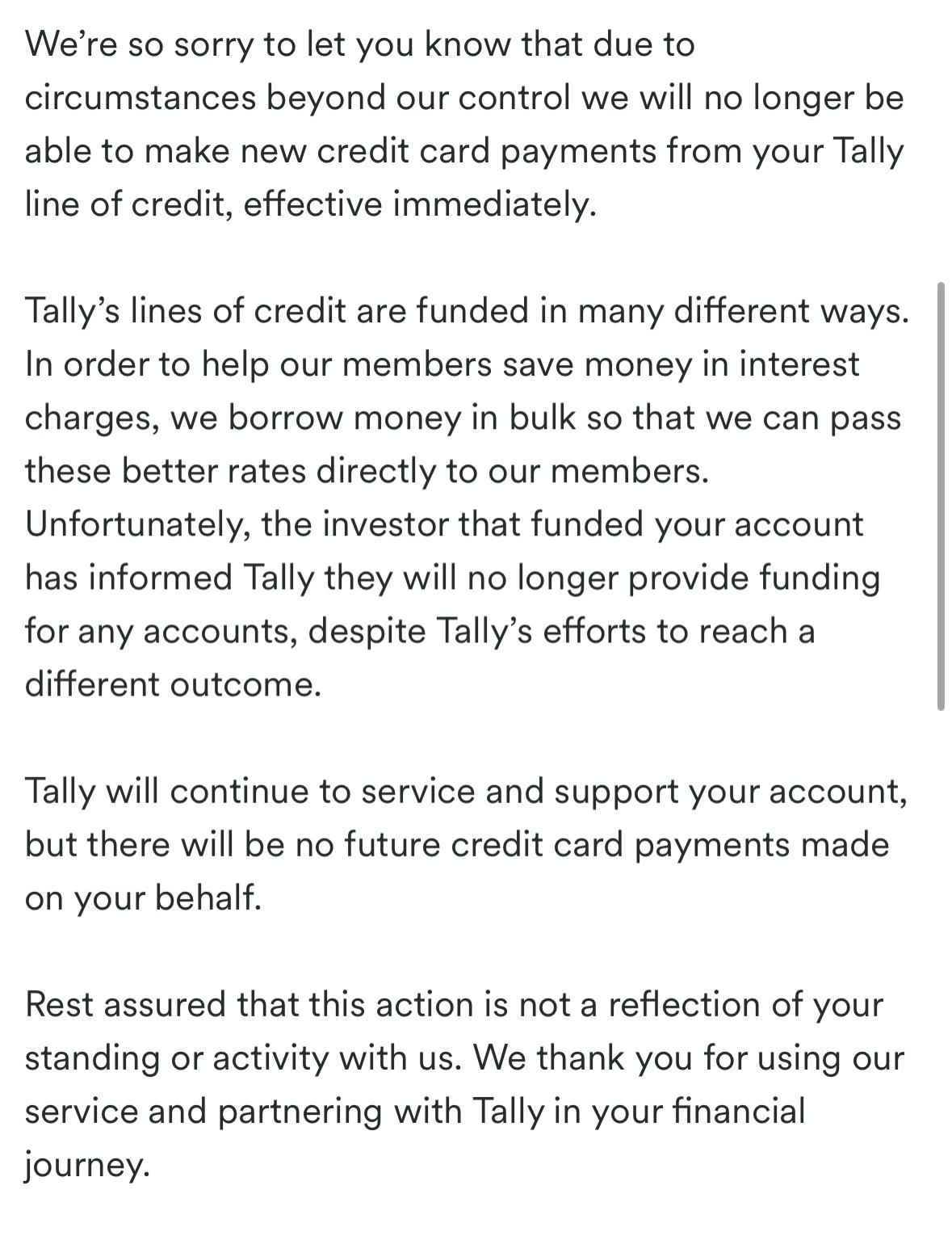

Customers of Tally, a fintech company focused on helping consumers pay off their credit card debt, are reporting some problems:

So what?

The pitch for Tally, which was founded in 2015, is that consumers link together all of their credit cards and apply for a line of credit. If they’re approved, Tally consolidates all of their credit card payments into a single monthly payment at a significantly lower interest rate.

Obviously, debt consolidation and debt refinance aren’t new concepts, but Tally’s focus on automation and digital self-service has helped the company gain traction with customers (Tally claimed to have saved its members $1.2 million in late fees in 2021) and investors (Tally raised a $50 million Series C, led by Andreessen Horowitz, in 2019 and a $80 million Series D, led by Sway Ventures, in 2022).

However, it would seem that the situation has taken a turn for the worse.

It’s not clear who the investor that stopped funding Tally’s loans is. Tally’s bank partner is Cross River Bank, which, in addition to providing BaaS services, also offers asset-based financing. It’s also possible that Tally was working with a different bank or private credit fund to provide debt capital.

What does seem clear from the raft of recent online complaints from Tally customers (Reddit, Better Business Bureau, Trustpilot) is that Tally’s model – customer acquisition fueled by the arbitrage between retail credit card interest rates and corporate debt interest rates – has broken down and customers, like the one who provided the review below, are getting hurt:

I have been a Tally app user for over a year. I continually made payments toward my Tally account, which then also paid my credit card bills. About a month ago, Tally stopped paying my credit card bills. They said their financing for my revolving credit loan fell through and they gave me no other option than to pay $584/month toward my Tally account while now simultaneously paying my credit card bill. The terms of this loan unilaterally changed and now I’m left at the holidays wondering how I’m going to keep the lights on. If this isn’t a breach of contract, I really don’t know what is.

#2: Venture Debt, Post-SVB

What happened?

Arc, a neobank for startups, launched a new product:

Arc … today announced Capital Markets, a private debt marketplace that connects premium technology companies with the world’s leading tech-focused lenders to facilitate custom debt transactions. Through Capital Markets, eligible technology companies receive term sheets for up to $250M in debt capital from an exclusive network of pre-qualified lenders, representing $100 billion AUM. Onboarding takes less than 10 minutes, funding terms are provided in 1-5 business days, and customers receive dedicated support from the Arc Capital team throughout the process. There is no cost for startups to receive funding terms from Arc’s private network of Capital Partners.

Capital Markets leverages financial API integrations, artificial intelligence, and other data enrichment layers to ingest, transform, and structure raw financial data. The standardized financial data and credit metrics, including the startup’s “Arc Score,” are surfaced in a secure data room accessible through the Capital Markets platform to streamline the credit underwriting process. Arc then programmatically qualifies the startup for debt capital across its contractual network of lenders and displays a curated selection of funding options based on the startup’s unique financial profile and needs.

So what?

Arc Capital Markets sits at the intersection of a few different trends:

- The failure of SVB and the waning of relationship lending. The old model for startups to raise debt financing was to go and ask Silicon Valley Bank or one of its few bank competitors for a loan. Usually, this required the startup to already have a banking relationship with the bank, and you just accepted whatever terms they offered. There was no shopping around. With the failure of SVB and the broader pullback on debt capital financing across regional banks, this model was thrown into disarray. The market became much more fragmented and mercenary.

- The growth of private credit. This pullback by regional banks happened at roughly the same time that private credit, an asset class that includes debt financing for startups, exploded as investors increasingly saw a high-yield, low-risk market available for the taking. I wrote more about the rise of private credit here if you’re interested.

- The emergence of embedded lending. As many platform providers have discovered, lending (particularly commercial lending) is much easier when you have programmatic access to relevant financial information. This has been the secret sauce for the small business lending done by platforms like Square and PayPal, and it seems that it is now making its way (in a slightly different form) into the world of corporate debt financing.

So, overall, I’m bullish on what Arc is building here. There is absolutely a need for a data-driven platform for matching up startups and lenders and facilitating streamlined (though still somewhat bespoke) venture debt transactions.

Two questions:

- How will Arc balance the needs of both sides of its network over time? Startups (in a post-SVB world) want the best possible terms and the most streamlined experience possible. Lenders want to generate the best possible yield at the lowest risk possible. You can see how these two objectives might come into conflict. I’ll be curious to see how Arc navigates that conflict as it builds out its network.

- How deep will Arc get into loan servicing and covenant management? Venture debt usually comes with a lot of strings attached. Lenders like to build a lot of covenants into their loan agreements in order to protect their downside. Managing these loans is usually a very complex and manual process for lenders (and borrowers). I wonder if Arc will build more software to help out in this area over time.

#3: What is Robinhood Trying to Be?

What happened?

Robinhood made an acquisition:

Retail trading giant Robinhood has announced a deal to acquire U.K.-based Chartr Limited, a media company that specializes in data visualization and newsletters, to add to its in-house, independent media brand Sherwood Media.

The acquisition is intended to help Sherwood expand its editorial offerings as it gears up to launch a news hub early next year.

Chartr’s products focus on simplifying complicated topics with data visualizations that Sherwood plans to integrate into its content, including its daily financial newsletter, Snacks, its web products and its social media content.

Sherwood launched with a focus on newsletters but has since begun expanding into other platforms.

In June, the company said it planned to expand to events, podcasts and build out a print magazine. It hired a head of sales to begin its commercial expansion.

So what?

I’m filing this under the category of “a little bit is good, but a lot is bad.”

Robinhood acquiring MarketSnacks in 2019, after MarketSnacks had seven years to find product-market fit and build its audience, made sense. Snacks (as Robinhood rebranded it) has, from what I can tell, been a valuable tool for keeping Robinhood’s users engaged and, to a lesser extent, pulling in new users.

Spending a ton of money to hire Joshua Topolsky (former editor-in-chief of Engadget and The Verge) to spin up an entirely separate media subsidiary (Sherwood Media) and then doubling and tripling down on that subsidiary’s product roadmap (including through an acquisition), before that subsidiary has even launched its core product makes … less sense.

This is another small bit of evidence for a larger theory that I have been workshopping – Robinhood has no idea what it wants to be when it grows up, and its pandemic-fueled growth surge and IPO (which was, for Robinhood, what the Zoltar machine was for Josh Baskin) significantly hampered the company’s ability to figure that out.

2 FINTECH CONTENT RECOMMENDATIONS

#1: Fintech in 2024 (by Tanvi Lal) 📚

As I always do at this time of year, I will be passing along any good 2024 fintech predictions that I come across.

Tanvi’s predictions are excellent. Nothing truly shocking, but I loved the level of depth she went into on vertical SaaS in this piece.

#2: BNPL is Good; I will die on this hill (by Simon Taylor, Fintech Brainfood) 📚

A great rant from Simon this week on BNPL, which hits on something really important – a lot of the criticism heaped on BNPL isn’t about BNPL per se, but rather about lending (and consumers’ irresponsible use of it) more broadly.

1 QUESTION TO PONDER

Is there any value in requiring banks (and other financial services providers) to share their full terms and conditions through open banking APIs at their customers’ request?

This is an area of disagreement between banks and the CFPB on 1033 rulemaking, and I’m curious to understand if I’m missing something. I get sharing key terms and conditions (pricing, rewards, fees, etc.), but what is the value in sharing the full terms and conditions document?