15 July 2023 | Healthcare

Navigating the Digital Health Funding Landscape: Insights from H1 2023

By workweek

Rock Health’s latest digital health funding report hinted that funding in 2023 is on path to be the lowest funding year since 2019.

Am I shocked? Nope. This latest funding trend has been something folks in the digital health community have been expecting since the 2021 funding boom. Some have even been expecting it since 2019!

In this article, I’ll highlight Rock Health’s latest digital health funding report and my recent virtual event on funding trends with Rock Health’s head of research, Adriana Krasniansky.

The Deets

Digital health startups raised around $6 billion across 240 deals in the first half of the year. Based on 2022’s digital health funding trends, some thought 2023 would/will be the first sub-$10 billion funding year since 2018. While it doesn’t seem like funding in 2023 will fall below $10 billion, it may certainly be the lowest funding year since 2019.

At a more granular level, we saw Q2 funding rake in $2.5 billion—$1 billion less than Q1’s $3.5 billion. Q1 only saw around 15 more deals than Q2.

The total funding, total number of deals, average deal size, and concentration of investments likely indicate the start of a new digital health funding cycle, per Rock Health. Below, I’ve boxed the previous funding cycle.

#Trending

Rock Health noted significant funding trends in H1 2023 regarding the characteristics of deals made and the types of startups receiving funding.

Deal Characteristics

Twelve mega deals were averaging $185 million and accounting for nearly 40% of all funding dollars in H1 2023. As anyone who took statistics would know, these large deals—or outliers—skew the mean deal size. But Adriana brought up an interesting point during our chat: should we view these mega deals as deals that skew the baseline data or treat these mega deals as the data that are part of the funding story? Likely the latter….

Notably, we’re seeing mega deal activity in the background of lower deal volume overall because active digital health investors are making more considerable but more concentrated bets on companies they are confident will succeed in the digital health environment instead of diversifying their investments.

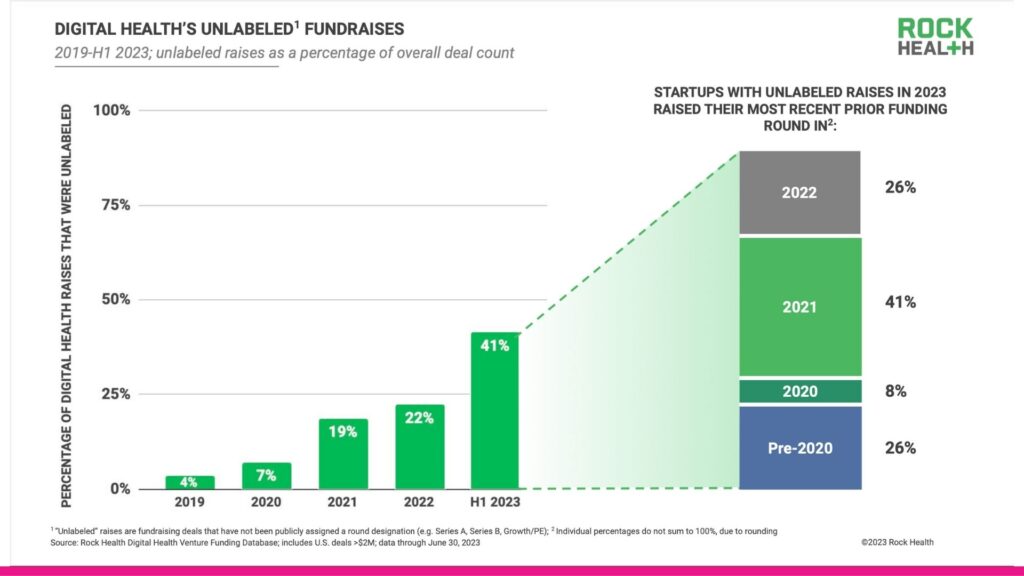

Lastly, two out of five raises in H1 2023 were “unlabeled raises,” meaning these funding rounds were not publicly disclosed (for example, “Healthcare Huddle raised a Series A round”). Interestingly enough, most of the companies that had unlabeled raises over the past six months raised their last rounds in 2020 or onward, and these rounds mainly were early-stage. Mihir Somaiya and Madelyn Knowles, the authors of the Rock Health report, noted these unlabeled raises might protect companies’ prior (high) valuations by avoiding a down round.

[Unlabeled raises are] a battlefield tactic, not a long-term strategy.

Key Funding Areas

There were three key funding areas to note from H1, and these were areas that were earning the above-mentioned mega deals:

- Non-clinical Workflow and practice management

- At-home care

- Value-based care enablement

Dash’s Dissection

Like many in the digital health space, I’m not surprised to see the end of a funding cycle and the beginning of the new one. 2023 is expected to have the lowest funding since 2019, and that’s ok. I like what Mihir and Madelyn said about the funding environment:

Though challenging, tough times can serve as a much-needed market correction, right-sizing innovator and investor expectations for a more steady and sustainable future.

Above all, I’m particularly interested in what types of companies are gaining attention among investors—specifically, the workflow, at-home care, and VBC-enablement companies.

Digital health companies offering at-home care solutions have received increased attention throughout the pandemic, allowing care to be performed in the home instead of in an ambulatory or hospital setting. Incumbent companies like UnitedHealthcare and CVS Health have also moved into this at-home care space through recent acquisitions, meaning there must be something attractive about the space. The reimbursement models are favorable for home health, and costs are theoretically lower, which means at-home providers will need products and services to enable care at home. Hence the investment in at-home solutions.

The non-clinical workflow category has also gained attention lately with the advent of ChatGPT. This past June, I wrote an article about non-clinical workflow startups and hosted a virtual event with Glass Health co-founder and CEO Dr. Dereck Paul (here and here). The potential to streamline notoriously slow processes in healthcare with AI-backed workflow solutions is limitless.

Then, we have value-based care, a term in the healthcare vernacular for decades despite the slow transition to VBC reimbursement models. One of the problems is not having the solutions to enable VBC, which is why it’s not surprising investors pumped money into this area. However, there are two groups of folks in healthcare: those who think VBC will save this healthcare system and those who think VBC sounds better than it actually is. I’m somewhere in the middle.

I’ll end with this note: as we exit the pandemic era, employers and healthcare organizations that jumped on the digital health bandwagon will begin to reevaluate the efficacy of the digital health solutions they bought or subscribed to. Did these solutions bring in a positive return on investment? Were these solutions actually solutions (article here)? Over the next year or so, we’ll see the results.

In summary, digital health funding in the first half of the year followed a downward trend compared to previous years, potentially making 2023 the lowest funding year since 2019. Mega deals accounted for a significant portion of the funding, while deal volume decreased. Key funding areas included non-clinical workflow and practice management, at-home care, and value-based care enablement. These areas attracted substantial investments due to their potential for innovation and market demand. Overall, the funding landscape is experiencing a market correction, setting the stage for a more sustainable future in the digital health industry.

Stay ahead in healthcare with my weekly Healthcare Huddle newsletter, covering digital health, policy, and business trends for 30,000+ professionals. Share with colleagues and subscribe here.