03 October 2022 | FinTech

What’s Gonna Happen With BNPL?

By

My wife Stevie and I moved to a new house this week, and after Costco and Best Buy, we hit up Sephora.

I’m a nerd at heart and I’m very curious—I always ask cashiers and retail workers about their experiences with new fintech products. Back when I lived in Brooklyn, I helped a local coffee shop move to Square because they couldn’t process card payments. I also once helped the West Hollywood A.P.C. figure out some random Shopify issue they had with their POS terminal.

So naturally I asked the young lady behind the counter at Sephora whether Afterpay and Klarna—two Buy Now Pay Later brands that were heavily advertised throughout the mall and the store as well—were popular payment methods at the store.

Much to Stevie and my surprise, she said they were actually super popular—a lot of folks apparently both, but Klarna was popular because you get rewards when you pay off your debt (which is actually really smart.)

Which reminded me—what happens to BNPL in the new economy? To me, things are clearly trending towards a recession; that usually has some long term implications on consumer lending.

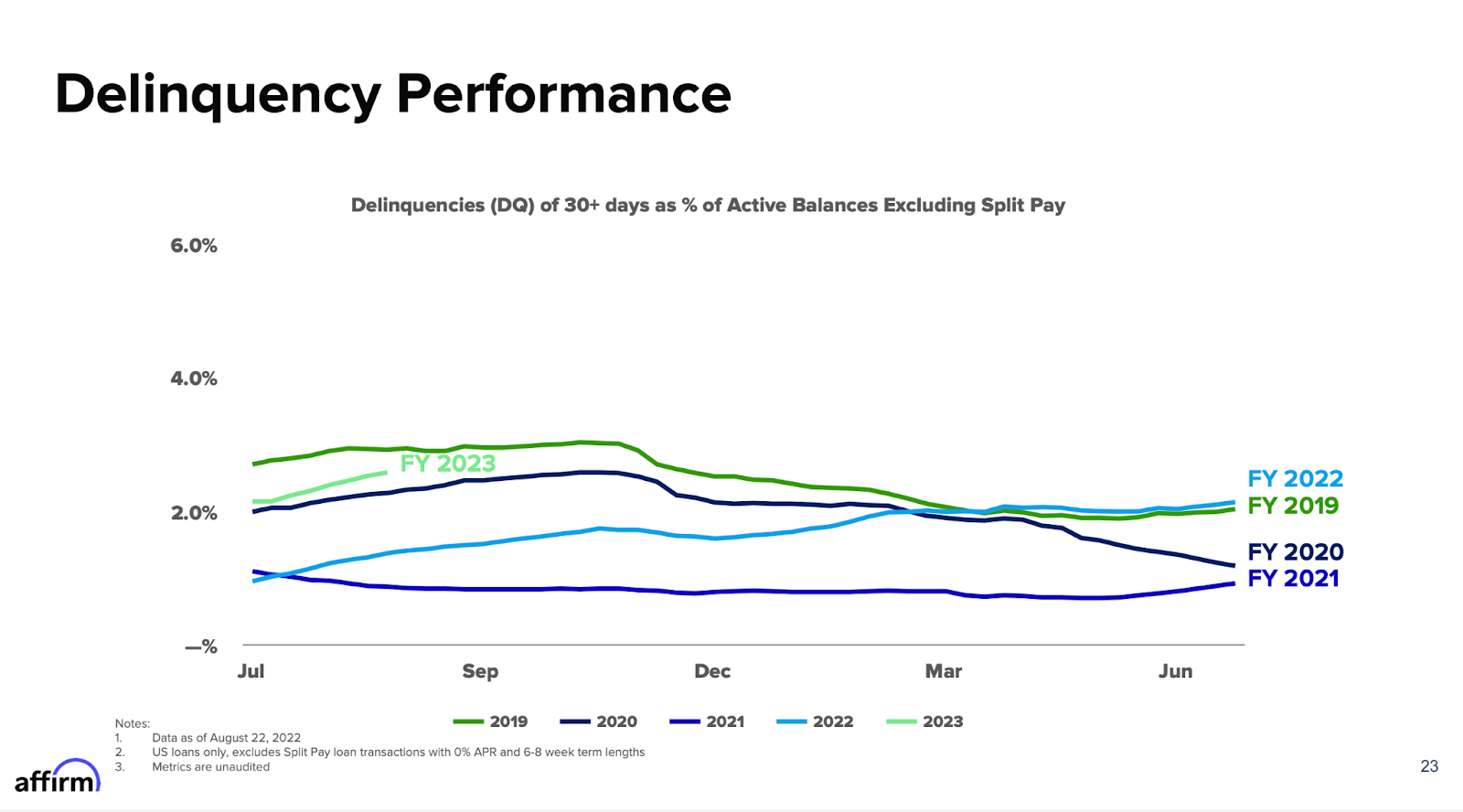

For BNPL, the story over the past few months has been rising delinquencies; Affirm is down significantly since January, mainly due to concerns that inflation is putting more stress on consumers, and that’ll trickle down to installment loan payments. Based on a Q4 investor presentation, delinquencies will be at a 4 year high in 2022.

A recent CFPB report on BNPL illuminated some other potential landmines—late fees and charge offs were increasing for the ecosystem as well. According to the report, which you can read here, the percentage of customers that paid at least 1 late fees went up almost 3% in 2021 (from 7.9% to 10.5% in 2021.) Charge offs increased by almost a full percent too—from 2.9% to 3.8%.

Lastly, another interesting trend over the past few years may play a factor too: more and more BNPL GMV is coming from everyday purchases like gas and groceries. In 2019, everyday purchases accounted for $3.3 million—in 2021, it’s up to $229.2 million. That’s a massive jump, and more indicative of consumer behavior trends than BNPL. If more and more people are struggling to pay for necessary purchases and need to turn to BNPL or credit cards, and the economy keeps heading south, consumers could be overextended in the long run.

There are a lot of different solutions BNPL companies can implement to offset delinquencies and ensure that users aren’t overextending their credit or BNPL limits. But, frankly, BNPL debt is hard to track—the CFPB launched an inquiry around the fact that a lot of BNPL companies haven’t historically sent data back to credit agencies. If its hard to keep track of how many BNPL loans a consumer takes out, getting overextended could happen pretty quickly.

Obviously this is a trend that will play out over the next few years—we won’t see things shift quickly unless things with the economy get way worse. But, as an observer, it’s something to keep an eye on. And for builders and folks inside of these BNPL companies, the economy presents a number of opportunities to refine and remodel BNPL to make it more sustainable and even more consumer-friendly than ever before.