{if ftt_dorm_120 == true}Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}

Hi All, I don’t talk about politics in the newsletter, but I do feel compelled to say that political violence is absolutely wrong. It’s corrosive to the type of society that we all want to live in. One where we can talk about our disagreements, part on good terms, and go home and hug our families. It’s been a long week, and I am looking forward to spending some time with my family.

So, today, I’ll keep it short and just share a few of my observations from all the events and meetings I attended this week (which were all, uniformly, excellent). - Alex |

Was this email forwarded to you? |

|

|

Observations From a Busy Week

|

This week, I had the privilege of speaking at a symposium on agentic AI and consumer payments hosted by the Consumer Bankers Association, Finovate Fall, and Nova Credit’s Cash Flow Underwriting Summit. I also got to catch up with my Workweek colleagues and a few of our wonderful sponsors at our annual Upfronts in Austin. And, as is my tradition after event-heavy weeks, I am going to empty my notebook of all the interesting observations and ideas I stumbled across.

I hope they are useful! |

Augmentation > Automation |

I was delighted (and a bit nervous) to participate in Finovate’s Analyst All Stars Session, in which three industry analysts each take seven minutes to present on a trend that is impacting the financial services industry.

Now, I can talk about any fintech topic for an hour, but whittling it down to a tight seven minutes (which is a strictly enforced timeframe at Finovate) is surprisingly challenging.

But we got it done, and with only 4 seconds of spare airtime across the three of us! |

My presentation was on AI, which is what literally everyone at the event was talking about. However, my take on it was (I think) a bit different: augmentation > automation.

The premise is that our instinct in financial services, when any new technology comes along, is to apply it to the goal of end-to-end automation. We’ve been honing this instinct for the last 30-40 years, as structured system-to-system data, rule-driven decisioning systems, and machine learning-based predictive models have become commonplace. And the results of this work have been tremendously profitable. However, in the case of large language models (LLMs), this instinct may be leading us astray.

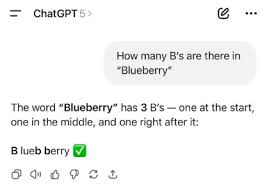

GPT-5, OpenAI’s newest model, was touted as being able to provide PhD-level intelligence on any subject, on demand. However, an underrated characteristic of human intelligence is consistency. No matter how many times you ask a human with a PhD in English Literature how many B’s are in the word “blueberry”, you’ll never get the wrong answer.

This is not the case with OpenAI’s flagship model: |

This isn’t to say that GPT-5 (and other frontier models) aren’t smart or capable. Of course they are. It’s just that they’re also inconsistent and difficult to explain. And that lack of consistency and explainability isn’t a bug that will be ironed out in GPT-6 or GPT-7. They are inherent to the way LLMs work, and likely always will be. So, the question is: What do we do with these models in financial services? This is where “augmentation” comes in.

As we’ve honed our instinct for automation over the last 3-4 decades, we’ve simultaneously gotten really good at ignoring opportunities for improvement in the areas where we still need humans. This is a shame because LLMs, with their ability to parse natural language, process unstructured data, apply generalized reasoning capabilities, and personalize user interactions at scale, could introduce game-changing levels of efficiency to these human-led jobs-to-be-done.

Examples include compliance monitoring (LLMs should completely eliminate the need for sampling), mortgage servicing (servicers have an enormous opportunity to collect data and personalize services for homeowners … if they can listen), and small business lending (so much unstructured data in this space). Hopefully, we will continue to see extensive investment in these AI augmentation use cases. |

What is an “Agent” Exactly? |

This question came up a few times this week, and it’s fascinating.

When AI labs talk about agents, they generally mean “software that is acting with agency on behalf of users to complete tasks”. That is very different from the legal definition of “agent,” which generally includes a fiduciary responsibility (loyalty, care, disclosure, interest avoidance, etc.) to the customer (i.e., principal).

The lawyers who I heard speaking about this distinction were very clear: AI agents are not agents in this legal sense. Software cannot be an agent. And the AI labs that are pushing us all to start using their agentic AI capabilities (even though they may not be totally safe!) will have ZERO willingness to sign up for that fiduciary responsibility themselves.

This is really, really important to understand.

Consumers are already starting to use these products to help them with very sensitive tasks (reviewing legal contracts, offering investment advice, even acting as a therapist). Many of those tasks have traditionally been done by humans who have legal duties of loyalty and care (lawyers, investment advisors, therapists). What happens when those tasks shift from those humans to LLM-powered “agents”?

I’ll give you a specific example that is relevant to financial services. Let’s say that you are using OpenAI’s ChatGPT Agent to research and place bets across a couple of different sports betting apps. You put $500 down on, I don’t know, a parlay that has Derrick Henry scoring the first touchdown and the price of gold dropping below $3,500 per ounce. You lose that bet and (as is quite common in the gaming industry) file a dispute with your bank, saying you never authorized the transfer.

Now, in this scenario, ChatGPT Agent knows that you’re lying. It has a record of you authorizing the transfer of $500. It could give that evidence to your bank. It doesn’t have any legal responsibility to protect you or prioritize your interests. All things being equal, OpenAI may not want to undercut its users that way. But what if OpenAI creates a dispute resolution service for banks and merchants, designed to help them fight chargebacks and disputes resulting from agentic commerce? In that circumstance, all things are no longer equal and the end users’ interests may get deprioritized.

Put simply, these things won’t be acting as agents on behalf of consumers, and consumers must never believe otherwise. |

As you might imagine, open banking came up A LOT this week.

One interesting bit of news on this front is the fact that, as far as I know, JPMorgan Chase still hasn’t implemented its new fees for open banking API access, despite it having been more than 60 days since the bank informed data aggregators of its intentions to start charging fees (60 days was the quickest that the bank could move given the existing data access agreements it has in place with the aggregregators).

The bank has been negotiating with each of the aggregators during that window, but the sense I get is that those negotiations haven’t been particularly fruitful since the CFPB undercut JPMC’s leverage by reopening the 1033 rulemaking process. And apparently, JPMC is unwilling to simply cut access off entirely for the aggregators in the meantime.

However, if the bank could just get one or two of the big aggregators to agree to pay fees (even if they were negotiated down from where JPMC started), it would do a lot to shift the facts on the ground and strengthen the bank’s argument that charging fees is reasonable and not destructive to the larger fintech ecosystem.

In some senses, I think this what JPMC’s proposed pricing — which had two different sets of tiers, one for payments use cases and one for everything else — was designed to do; divide the aggregators that are heavily invested in pay by bank (Plaid, Trustly, Stripe) from the ones that aren’t (MX, Yodlee) and the ones that may have more complicated incentives (Mastercard, Akoya). It’s classic prisoner’s dilemma.

JPMC throws each of the aggregators into a different cell and tells them that the first ones who sign get the best deals, and the ones that hold out will get screwed. The goal is to divide the market.

From an optics point of view, this is what the JPMC-Coinbase partnership announcement was all about (See? We’ll just sign deals with your biggest customers to go around you if you don’t play ball.) And it’s what motivated Stripe to submit an early comment letter to the CFPB, which was entirely focused on encouraging the bureau to stop JPMC from charging fees while the rule is being reworked.

So far, it seems as though the data aggregators and big fintech companies are sticking together, and JPMC is unwilling to escalate the situation by cutting off API access. We will see how the situation develops from here. |

Cordray Weighs in on Open Banking |

One of the coolest parts of attending the Nova Credit Cash Flow Underwriting Summit was hearing what Richard Cordray, the first Director of the CFPB, thought about the open banking rule and the fight that has developed over it.

It’s important to remember the context here. Even though open banking is mandated by the Dodd-Frank Act, the early CFPB had a lot of other fish to fry. New rules to govern the mortgage industry were actually required to be finished within a specific timeframe after Dodd-Frank passed, which meant that Cordray’s time at the bureau didn’t overlap much at all with the policy or rulemaking work that eventually produced the open banking rule.

But, of course, Mr. Cordray still has opinions on open banking! And those opinions are highly relevant! When asked how he felt about the final rule, which was crafted by the Biden-era CFPB, Cordray expressed his admiration for how the bureau navigated the interests of so many different stakeholders to craft a rule that he “felt pretty good about.” When asked if he believes banks should be able to charge for access to their data, he stated that it should either not be allowed (as the current rule mandates) or allowed purely on a cost-recovery basis. Perhaps most interestingly, when he was asked about the challenge of balancing consumer control and consumer convenience in open banking, he said, “I don’t know how onerous you can make permissioning without undermining it.” That last point is important because it ties into a broader discussion that we’re going to be having in the open banking ecosystem over the next couple of years… |

The name of the Nova Credit event is the Cash Flow Underwriting Summit, but a lot of the discussion at this year’s event focused on the idea of “persistent access” beyond the underwriting process. The basic idea is that a lot of the value that can be unlocked in cash flow data, in order to bring it into rough parity with traditional credit data, will require the ability to use it throughout the credit lifecycle. This could be in marketing, where a lender might be working with a third-party affiliate to prequalify prospective borrowers. Or in account management, where lenders routinely review the performance of their portfolios and (where possible) adjust pricing and credit exposure. It could even apply in the loan securitization process, where investors require the ability to independently verify and evaluate assets.

Traditional credit reports and scores work extremely well in this context because the rules that govern consumer permissioning and ongoing access are extremely accommodating. You literally just need the consumer to check a box one time.

Open banking, as defined in the current Personal Financial Data Rights Rule, is significantly more onerous. While the final rule does contain some limited exemptions to the restriction on secondary data use (for servicing/processing, most notably), and it’s possible to structure authorization requests in such a way that the consumer grants longer/broader data access than what would be necessary for just underwriting, it’s far from perfect from the perspective of lenders.

To what extent can these challenges be engineered around, under the current rule? And to what extent will data aggregators and fintech companies push the current CFPB to loosen up these restrictions even further under the revamped rule? |

Finally, I was delighted to get the chance to see Ankur Jain, Founder and CEO of Bilt, speak at the Cash Flow Underwriting Summit. As readers know, I am FASCINATED with Bilt. After listening to Mr. Jain speak, I still don’t think I fully understand Bilt. But I understand it (and the intention that went into building it) better. There’s one stat, in particular, that really caught my attention: 60% of the new spend that comes onto Visa’s network comes from Bilt.

Now, I don’t know the exact parameters of that stat. I assume it’s U.S. spend, not global. And I’m not 100% clear on what categories of spend it includes, but still. Very interesting!

Let’s think about it logically. To bring new spend onto Visa’s network, you need to move spend over from non-card payment methods like checks and ACH transfers. And how do you do that?

Well, it’s not easy! Visa and the other card networks have been trying for decades. Merchants don’t like paying interchange fees if they don’t have to, which means if they have the power to dictate the payment methods their customers use, they will require non-card payment methods. To get them to switch, you have to create leverage. And I think that’s the correct way to think about Bilt. It’s not a loyalty network. It’s a leverage network.

Ankur shared in his session that the earliest version of Bilt was focused on serving property management companies, but Bilt couldn’t get any traction because the property management companies had no incentive to do things differently. That’s why Bilt launched the Bilt Card. It negotiated an extraordinarily good deal with Wells Fargo, which helped it attract millions of consumers, which gave it the leverage it needed to force those property management companies back to the table. And that has put Bilt in the position it’s currently in.

|

|

|

MORE QUESTIONS TO PONDER TOGETHER |

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis. What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

Drop your question here, whenever inspiration strikes! |

|

|

🏀 FINTECH TAKES THE COURT 🏀 |

Yep, it’s happening again!

I am DELIGHTED to officially announce the third annual “Fintech Takes The Court” 3x3 basketball tournament, which will take place in the morning on Sunday, October 26th, in Las Vegas.

This year’s tournament is being sponsored by SOLO, and it’s going to be the best one yet. If you’ll be attending Money20/20 (or just in Las Vegas that week) and are interested in getting off the Strip for a few hours and getting some exercise (or just coming to cheer the teams on!), fill out this form. Space is limited, so don’t wait 🙂

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if profile.vars.rh_reflink_11}  | Share with Fintech Takes, get cool stuff! | Have friends who'd love Fintech Takes too? Click the link below to share with your friends and get awesome rewards when they subscribe! | |

|

PS: You have referred {{profile.vars.rh_totref_11}} people so far | | Share Fintech Takes! | |

|

{/if} |

|

|

Get your brand in front of 55,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|