My attempt to sort through a very busy and chaotic week.

{beacon}

{ad_logo_primary}

{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes.

{/if}

Happy Friday, Fintech Nerds!

It’s been a busy week. So busy, in fact, that I’d be hard pressed to recount everything that has happened.

It feels like fintech flew by this week, and today’s newsletter is my attempt to empty my notebook (and my brain) of the observations, questions, and random bits of information I’ve collected recently.

If you’re looking for something more structured, I would recommend my latest sponsored deep dive essay (here) and the first three episodes of my latest sponsored podcast miniseries (here, here, and here).

Fair warning: I’m going to hop across a lot of different topics, though I’m guessing this first one won’t be a surprise.

Only In Vegas

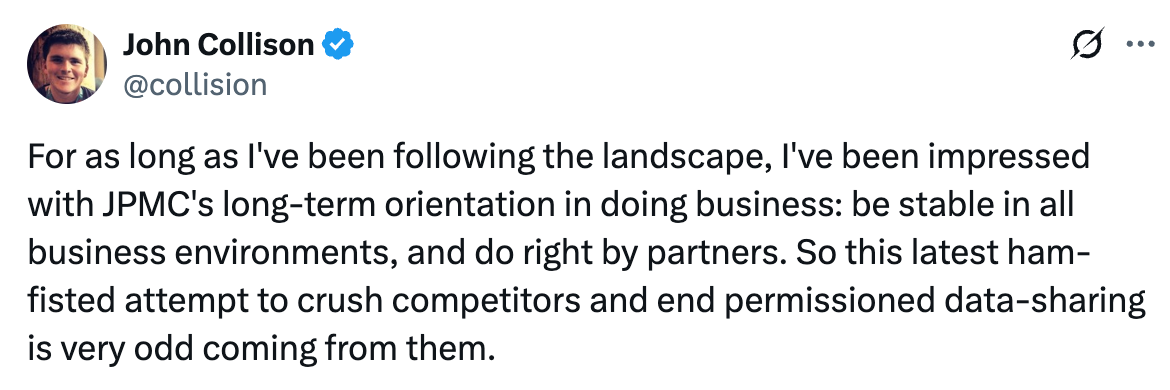

Many folks (including, occasionally, myself) are getting a bit lost in the sauce on the JPMorgan Chase/open banking news. This is understandable. The story is constantly evolving and has a lot of moving parts.

But let’s try to take a step back and look at what’s been happening through a slightly wider lens.

Here’s the rough timeline:

October 2020 — The CFPB (under Kathy Kraninger) formally initiates the rulemaking process for open banking in the U.S. by publishing an Advance Notice of Proposed Rulemaking (ANPR).

October 2022 - October 2023 — The CFPB (under Rohit Chopra) carries the rulemaking process forward (SBREFA Outline of Proposals, Small-Business Review panel, Final Report) and proposes the draft rule (NPRM).

October 2023 - October 2024 — The industry provides extensive commentary to the CFPB on the rule. Big banks start to lean in (sometimes in an anti-competitive way). The main industry standards body for open banking, the Financial Data Exchange (FDX), names a former JPMC executive as its CEO and applies for formal recognition from the CFPB.

October 2024 — The Chopra CFPB publishes the final version of its open banking rule. The Bank Policy Institute sues the CFPB over the rule shortly after, much to the surprise of many FDX members.

January 2025 — President Trump is sworn into office, and the open banking rule takes legal effect (with staggered compliance deadlines for portions of the rule).

May 2025 — The CFPB (under Russell Vought) asks the court to vacate its own rule, siding with the BPI and citing alleged legal defects with the rule.

July 2025 — First, JPMC informs data aggregators that it will charge new fees for customer data API access (a move applauded by PNC Bank’s CEO). Then, only a few weeks later, the CFPB reverses course and asks the court to pause the lawsuit, in response to “recent events in the marketplace,” so it can begin an accelerated rewrite of the rule.

Now, there are a couple of important things to point out here:

The idea that the U.S. should have regulated open banking and that the regulation should encompass consumer-permissioned data sharing via authorized third parties (acting as agents of the consumer) has been relatively uncontroversial and has enjoyed bipartisan support for most of the last five years.

I’m sure it didn’t feel this way to them, but banks actually got a lot of what they wanted in the CFPB’s final rule. Secondary data use (which JPMC is particularly fired up about right now) was heavily restricted, and the scope of the final rule ended up being relatively narrow, focusing only on Reg E and Reg Z accounts, but excluding personal loans, auto loans, mortgages, and wealth management. The big things that didn’t go the banks’ way — such as the ability to charge fees and a defined framework for liability — were areas that the Chopra CFPB studied closely but ultimately determined should not be included in the final rule, often due to specific legal or administrative challenges. (Editor’s Note — This tweet articulates why fees are a tough area to directly address in the rule.)

As I wrote about earlier this week, if JPMC’s plan to charge the data aggregators, at the pricing it has proposed (which is, by all reports, quite high), goes into effect (and especially if other big banks follow its lead), the results could be much worse for the bank than it might imagine. Screen scraping could surge back, but in a much more decentralized and chaotic manner than we have previously experienced. Fraud and scams, built on access to screen-scraped data, could become even more common. And the number of negative JPMC customer service interactions could increase … significantly.

In response to JPMC’s aggressive fee gambit, the CFPB … the Russell Vought everything-the-government-does-is-bad-long-may-the-free-market-reign CFPB … requested and has been granted a stay by the court, so that it can amend the rule. The best case for JPMC at this point is that the CFPB fast-tracks a revision to the rule that pushes out the compliance deadlines and then, separately, works on other changes to the rule to address industry concerns. The problem, even in this optimistic scenario, is that those other changes could impact areas (such as secondary data use, scope of covered data, etc.) that the banks don’t want to see altered. It’s also possible that the Vought CFPB will discover, like the Chopra CFPB did, that implementing things like cost-recovery fees and defined liability frameworks in the rule itself is more difficult than it might have expected, even if it is more naturally sympathetic to banks on those issues.

I share all of this context in order to illustrate why I was so surprised by JPMC’s fee gambit and why some of the commentary from other industry participants has this bewildered, almost concerned tone to it:

He sounds like he’s talking to someone at an intervention. We're worried. This isn't like you. You're hurting the people around you.

And he has a point. JPMC overplayed its hand, and it’s worth trying to understand the psychology behind this mistake because the folks at JPMC are really smart. They’re great poker players. They don’t make many mistakes.

My best explanation is that JPMC sued the CFPB (through the BPI) back in October of last year simply as a reflex. That was always going to happen because that’s what big banks do when a regulator (especially the CFPB) crafts a rule they don’t like (Rohit Chopra expressed a similar opinion in a recent Reddit AMA.). The bank probably thought there was a decent chance that the lawsuit would lead to some changes in the rule (especially if Trump won the election), and if not, no harm in trying.

The bank likely didn’t expect the Vought CFPB to throw its full-throated support behind the lawsuit and ask the court to vacate the rule entirely.

When that happened, I think certain JPMC executives saw this narrow and completely unexpected window of opportunity to take out all of their frustrations on the Chopra CFPB and data aggregators and to reshape the ecosystem by doing something that they never would have done under any other circumstances. Even if it meant jeopardizing all of the progress it had made in its relationships with fintech companies and the soft power it had established in the open banking ecosystem through FDX. And even if it meant risking a backlash from the ascendant tech VC/crypto community, the Vought CFPB, and the White House.

Please excuse this analogy, but it’s a bit like if your friend were engaged to be married, after a long and, at times, strained courtship. And right before the wedding, he was unexpectedly whisked off to Las Vegas for a surprise bachelor party. And after an impromptu visit to the club (organized by that one friend in the group who is always encouraging the others to take dumb risks) and a lot of drinks, he decided to throw caution to the wind and propose to one of the strippers.

It’s an obviously bad idea that only kinda makes sense if you’re drunk in Vegas at 3:00 AM and getting cold feet about committing to a future that is very different from your life up to that point.

The Vought CFPB’s abrupt about-face and decision to initiate an accelerated rulemaking process in response to JPMC’s fee gambit is the equivalent of the hungover early-morning flight back from Vegas the next day.

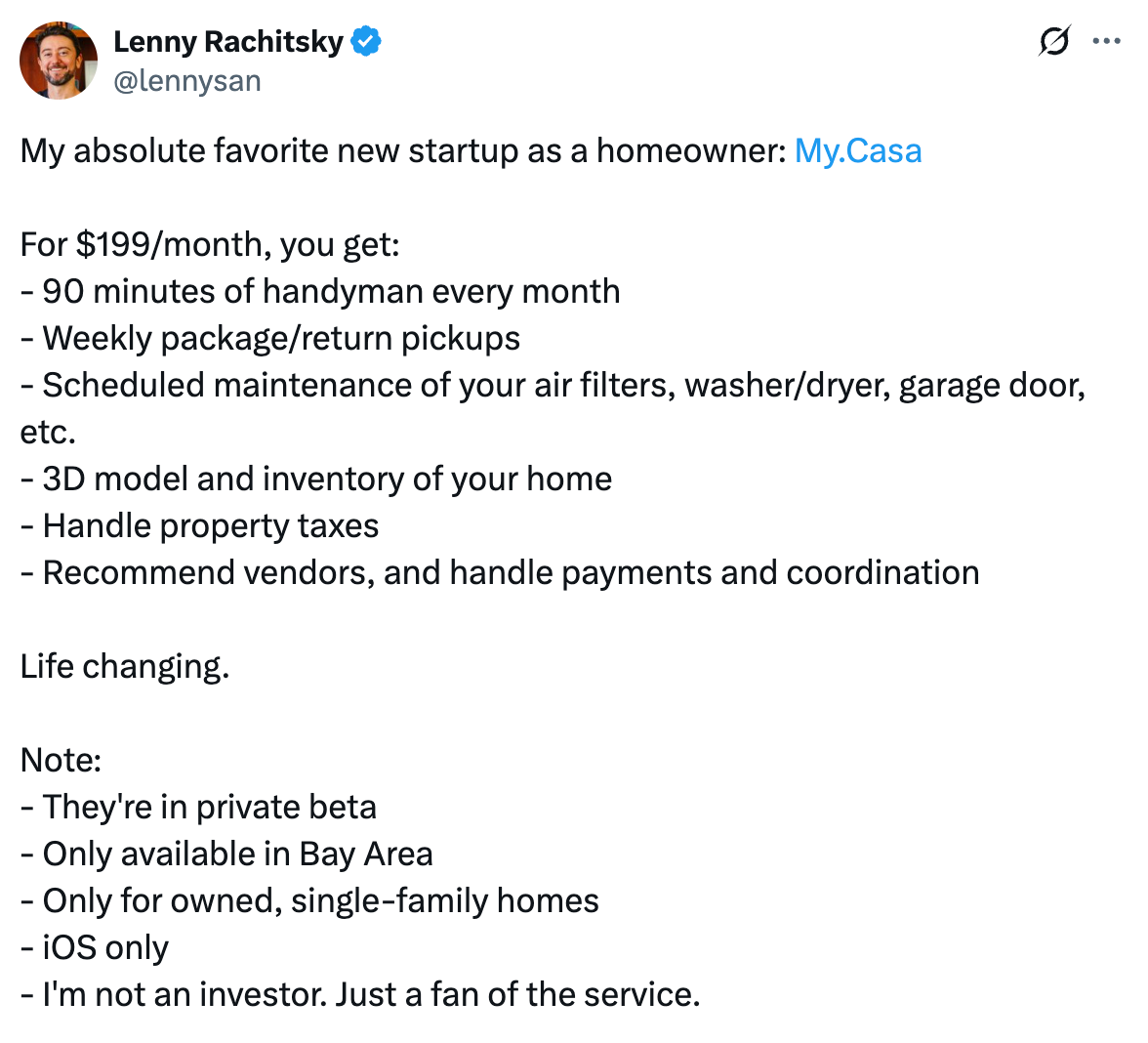

Rocket’s Next Acquisition Target

The company’s budget for acquisitions is probably depleted after dropping more than $10 billion to snag Mr. Cooper and Redfin, but if it can find some spare change under one of the sofa cushions, it should really consider scooping up Casa.

This is *exactly* the type of service that needs to be overlaid on top of the crappy experience that is mortgage servicing today:

JPMC + Coinbase

JPMorgan Chase and Coinbase recently announced that they are working together, which is interesting for two reasons.

First, the companies are building a direct integration between their products, rather than relying on data aggregators:

JPMorgan Chase & Co. and Coinbase Global Inc. signed an agreement to directly link customers’ bank accounts to their cryptocurrency wallets

The connections between Chase bank accounts and Coinbase crypto wallets are expected to go live next year, according to a statement Wednesday.

By establishing this type of direct relationship with a bank, financial-technology companies could cut out data aggregators such as Plaid Inc., MX Technologies Inc. or Akoya, which have traditionally served as behind-the-scenes connectors between the companies and banks.

Coinbase plans to maintain all its existing relationships with data aggregators, with direct connections to Chase accounts in addition to those, a Coinbase spokesperson said.

I would LOVE to know what, if anything, Coinbase is paying for this integration.

Second, JPMC will allow its customers to use their Chase credit cards to purchase crypto through Coinbase:

Customers will be able to fund Coinbase accounts with their Chase credit cards for the first time — an option expected to be active this fall, the firms said in the statement. They will also be able to redeem Chase rewards points to fund their crypto wallets.

Given the bank’s historical aversion to crypto (Jamie Dimon has called it a “fraud” and a “scam” multiple times) and its decision to restrict customers’ use of credit cards for other activities (like paying off BNPL loans), this strikes me as a significant change.

Under No Circumstances Should the CFTC Be Put in Charge of Regulating the Crypto Industry

My understanding is that the CLARITY Act (which just passed in the House of Representatives) would classify most crypto assets (except for stablecoins) as commodities rather than securities, which would put them under the regulatory purview of the Commodity Futures Trading Commission (CFTC).

Who knows how far this legislation will ultimately go (it sounds like the Senate will be a challenge), but I just need to say this for my own sanity — the CFTC should not, under any circumstances, be the primary regulator of the crypto industry.

Why?

Because of how utterly it has failed to regulate the crypto industry’s cousin in speculation: prediction markets (this article gives a very in-depth explanation of how the CFTC has dropped the ball with Kalshi, if you’re curious to learn more).

Thankfully, it seems that Brian Quintenz’s nomination to CFTC chair may not be moving forward, based on concerns regarding his seat on Kalshi’s board.

FICO’s Q3 Earnings

After watching Bill Pulte throw the mortgage market into a state of utter confusion with nothing but the power of vague tweets, I made sure to tune into FICO’s Q3 earnings call, which took place this week.

It did not disappoint.

Quick recap.

Under Pulte, the FHFA has decided to adopt a “lender choice” model, allowing mortgage lenders to select either Classic FICO or VantageScore 4.0 for each loan sold to the GSEs, without mandating the use of both. For the first time ever, this pits FICO’s 20-year-old FICO Classic score (which it has been aggressively raising the price of) against a competitive score (VantageScore 4.0) that’s both cheaper and more predictive.

Stock market analysts were understandably concerned about this development, and on the earnings call, FICO attempted to reassure them:

The FICO Score is the in standard measure of consumer credit risk in the U.S. The FICO Score is the backbone of safety and soundness in the mortgage industry. Over the last 30 years, the FICO Score has fundamentally transformed the mortgage industry, enhancing stability and liquidity in secondary markets, standardizing credit evaluation for investors, expanding fair and objective access to credit and empowering cost-effective and sustainable homeownership for Americans.

It also forcefully pushed back on the FHFA’s decision to allow lenders to choose between two scores, rather than one (or mandating that they pull both):

The FHFA has long rejected the practice because it undermines the safety and soundness of the enterprises and their counterparties, damaging liquidity in the $12 trillion mortgage industry. Lender choice encourages mortgage participants to shop for the most [ lax ] score, which drives unavoidable gaming and adverse selection for all risk holders. It creates a race to the bottom by incentivizing score providers to weaken their credit decision criteria to score more consumers and one more business with their score, which will lead to increased costs for consumers. Lender choice will result in higher capital requirements from regulators that the holders of mortgage risk will have to bear, and American taxpayers will bear significant additional risk.

And made the case that if the lender choice model does continue, FICO 10T (the company’s newest score) must be allowed to compete:

Any initiative to promote competition and ultimately lower cost should include the best Score, which is FICO Score 10 T. FICO Score 10 T's superior predictiveness will drive significant loss avoidance savings for market participants and billions of dollars of savings for consumers.

However, when an analyst at JPMorgan asked this question:

We're about a year removed from VantageScore providing the loan level data set to the banks. And my understanding was that was a prerequisite for them getting their score approved. Are you guys, for some reason, hesitant to provide that data to the banks? Or is the FHFA -- is there some sort of negotiating with the FHFA on what that looks like? I'm just not quite clear as to why FICO 10 T doesn't have a data set like that in the market.

FICO’s CEO simply said:

We are working with them to get the data out.

That’s not a tremendously satisfying answer. One wonders if there was a certain amount of complacency behind FICO’s delayed move to provide loan-level data for FICO 10T, because it didn’t expect that the FHFA would ever implement a lender choice model.

If that’s the case, it was a significant miscalculation.

Interestingly, FICO’s Q3 results were quite good. It beat expectations, with revenues of $536 million (up 20% year-over-year) and a record-breaking free cash flow of $276 million. It also completed the largest stock buyback in any quarter in FICO’s history and raised its adjusted earnings per share guidance for the year from $28.58 to $29.15.

And yet, FICO’s stock dropped after it reported these earnings, hitting a 52-week low as of Thursday.

No wonder the company is ramping up its budget for lobbying.

MORE QUESTIONS TO PONDER TOGETHER

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis.

What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

We ditched the like button. Added smarter reactions. And made it easier to converse and DM. It’s still the fintech nerd haven you know — now just with a better feed. See it here.

I’m working with Dilly Labs and the wise and powerful Tom Johnson on a little research project and I am looking for folks who work at a consumer lending company (bank, credit union, non-bank lenders, etc.) and who have experience buying/implementing/working with credit decision engines to fill out a quick survey.

I promise it won’t take long! And it will be extremely helpful! So …

(Editor’s Note — If you work at a technology company that sells a credit decision engine, feel free to pass the link to the survey on to your clients. That’s perfectly fine. However, if you attempt to fill out the survey yourself, a terrible curse will befall you and your company. This isn’t a joke. The curse is real.)

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex

{if profile.vars.rh_reflink_11}

Share with Fintech Takes, get cool stuff!

Have friends who'd love Fintech Takes too? Click the link below to share with your friends and get awesome rewards when they subscribe!

PS: You have referred {{profile.vars.rh_totref_11}} people so far