{if profile.vars.board_room_user_fitness == true && (time("now") > profile.vars.user_fitness_reviewed_time + 7200) && (time("now") < profile.vars.user_fitness_reviewed_time + 1209600) && (!profile.vars.onboarding_complete_time)} {/if}{if hosp_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy. |

|

|

{/if}Happy Friday Hospitalogists!

You should find today’s newsletter pretty useful as Elevance’s earnings call is our first peek behind the curtain as to how a health insurer perceives all of the various changes happening within their segments (outside of Medicare Advantage). Also, if you could take a moment to forward this newsletter to your entire firm and force subscribe them team or colleague I would greatly appreciate it. Hospitalogy is my livelihood and these take a while to put together! They can hit that little orange button below.

Oh, and if you or they are interested in joining my community where we discuss trends like these on a monthly basis and give you access to useful intelligence to bring back to your org, you can apply here and join plus membership to support me further while getting incredible bang for your buck. Let's dive in! |

Was this email forwarded to you? |

|

|

BLAKE'S BREAKDOWN: ELV Earnings

|

Going deeper on an interesting topic, theme, or trend |

Elevance Q2 Earnings Overview: BBB, Medicaid, ACA, IDR, and more Implications |

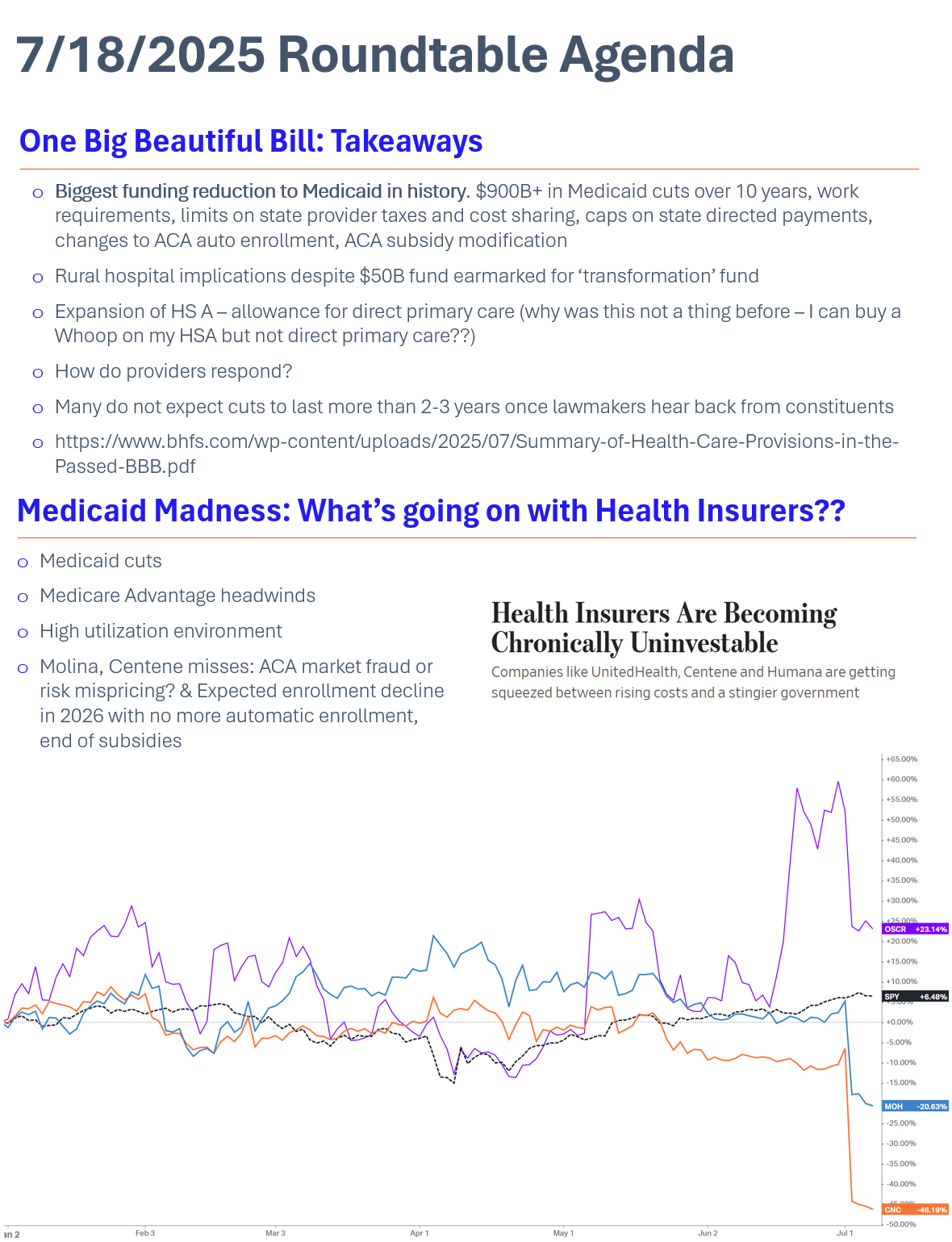

This week, the Wall Street Journal published an article with the headline Health Insurers are becoming Chronically Univestable - and with everything going on (public perception, elevated utilization, Medicaid cuts, ACA subsidy and enrollment crackdown), it's pretty clear to see why. So let's peek under the hood at Elevance's earnings to see exactly how they're navigating these murky, volatile waters.

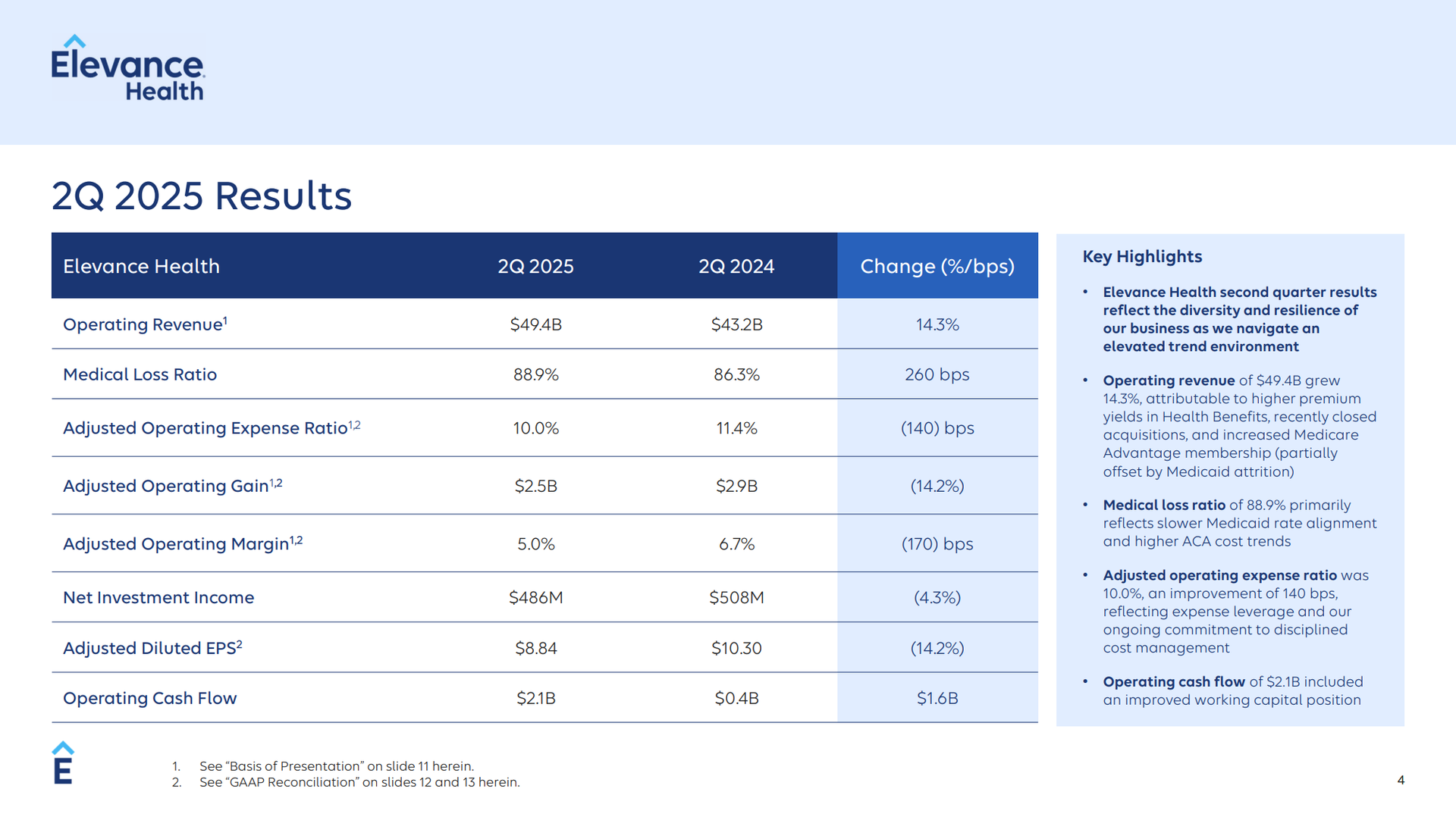

Yesterday (July 17), Elevance cut its guidance after posting dismal Q2 earnings stemming from elevated utilization trends in marketplace plans and rate pressures in Medicaid. Here’s the full Q2 presentation covering Q2 2025 trends for the managed care behemoth. Highlights from the quarter:

|

Medicaid utilization: 1/3 of trend relates to higher acuity while 2/3 is attributable to utilization & coding (last year this was 60/40). July rate cohort aligned with historic assumptions, but still trails real‑time trend, so margin recovery pushed out several rate cycles.

ACA marketplace dynamics: Medicaid disenrollees and lower effectuation rates pushed healthier lives out; ~70% of pressure is risk‑pool shift, ~30% utilization/coding. Utilization hotspots include ED visits (2x higher than commercial!!), behavioral health, specialty pharmacy, and some outpatient providers which Elevance management blamed on AI-enabled upcoding and aggressive IDR filings (hello Nutex) and you’re 1000000% about to see this become the next battleground for the No Surprises Act nonsense. Case in point - Elevance’s recent lawsuit in Georgia.

-

“This quarter, we took very aggressive action and filed a legal suit against what we think is the misuse of the IDR process under the No Surprises Act. And just to put that in perspective, we've seen out-of-network providers and their billing partners submit thousands of disputes sometimes hundreds in a single day, and our payment request can be significantly inflated, which is costing the entire health care system sometimes those are from as much as 21x bill charges, just to give some perspective on this.” - ELV Q2 earnings call

Commercial book: Mostly in line with expectations: -

Large‑group fully insured: Margins on plan, benefiting from more disciplined market pricing; July renewal season showed good retention. Still elevated utilization trends, but ELV priced this in. They’re seeing similar cost hot‑spots as ACA, but less severe.

-

Shift to ASO continues, but Elevance capturing that business; overall commercial contribution viewed as stable earnings ballast in 2025.

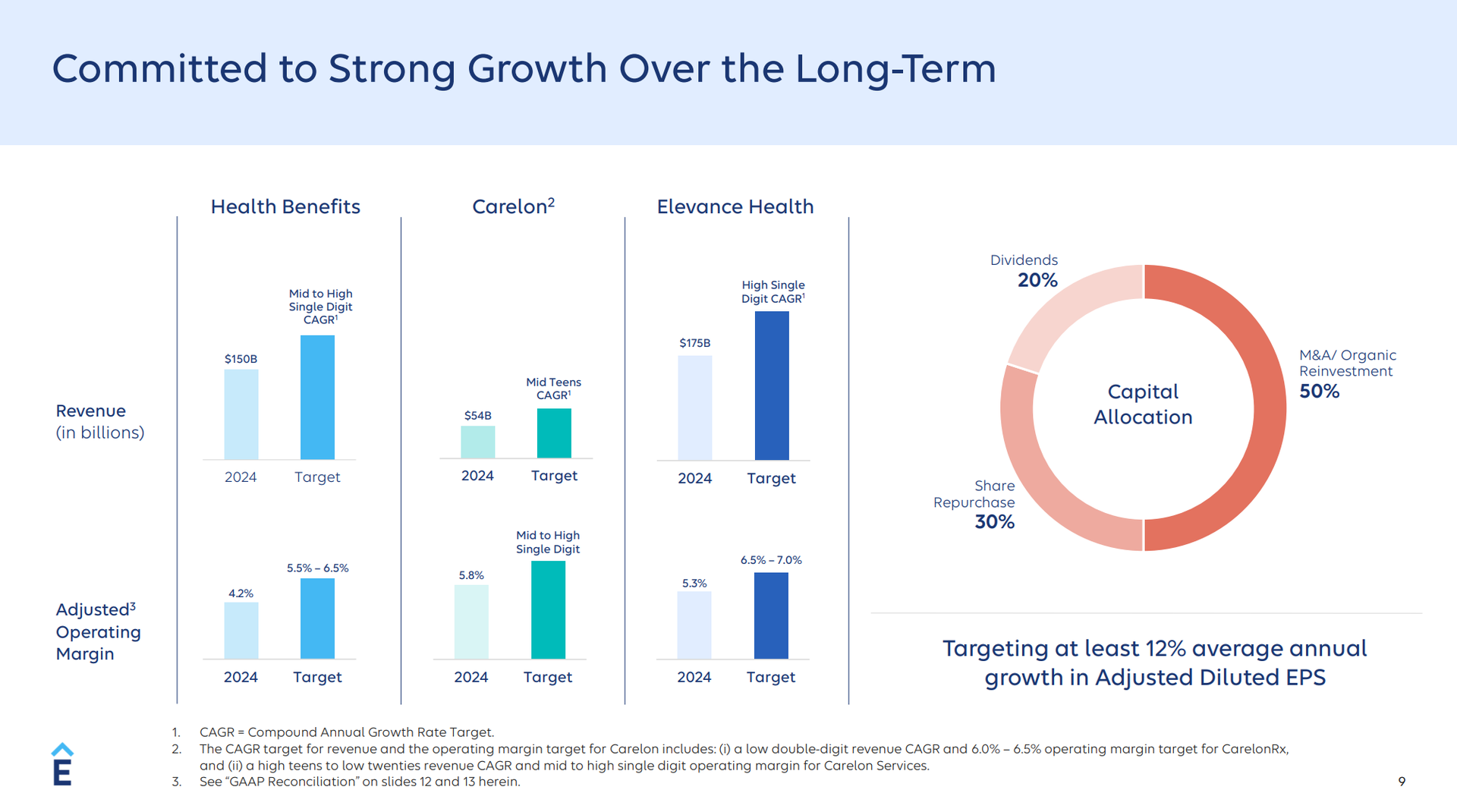

Carelon: Is working on cross-selling services and expanding risk-based arrangements in Optum fashion. CarelonRx saw solid growth while its services segment is growing 50%+ year over year. It was interesting to hear about Elevance’s progress with acquiring CareBridge in 2024 for a reported $2.7B - short term, this acquisition diluted earnings given its services are high revenue, low margin. Management mentioned plans to continue scaling the service across dual eligible and high acuity Medicaid populations.

Big Beautiful Bill Implications: When discussing the new legislation (top of mind for probably every person working in healthcare across the U.S.) ELV called out expectations for additional risk pool churn in both Medicaid and exchange populations, decline in enrollment, and the potential for even HIGHER utilization in Q4 (typically the strongest anyway due to seasonality dynamic with deductibles) as members use their benefits before they lose coverage. So on the provider side we might see even stronger short-term volumes in Q4 stemming from these dynamics for those with higher exposure to these payors.

|

Tech & Innovation: While Elevance is wary of AI-enabled documentation and upcoding tools on the provider side, the firm is focused on prior auth automation and AI payment integrity (duh)

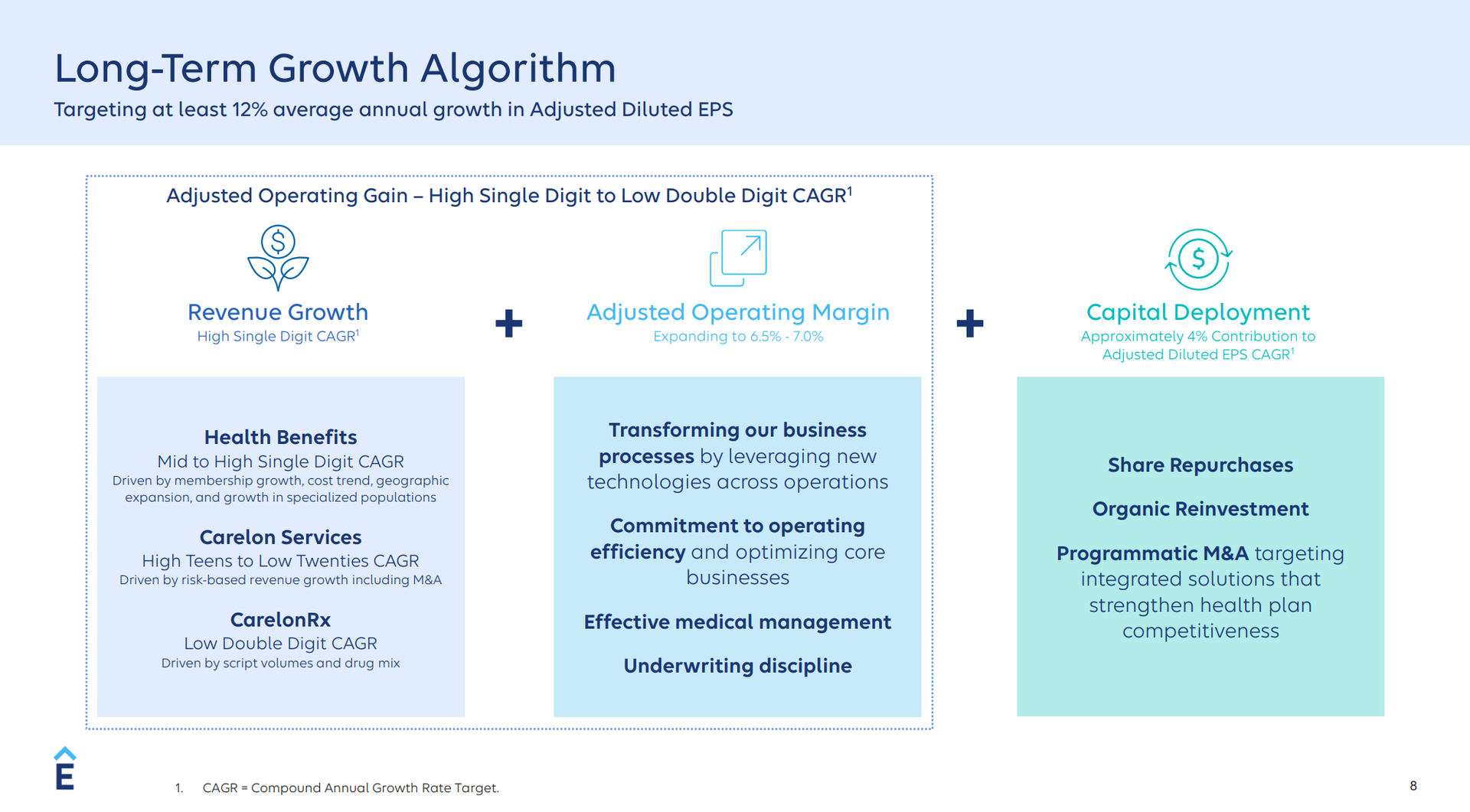

Overall, Elevance is playing defense in public programs (Medicaid/ACA) by resetting earnings and leaning on data‑driven cost controls, while playing offense with Carelon and a disciplined commercial book with a partnership-focused model moving forward. Expect choppy margins until Medicaid rates re‑price and trend lag resets and ACA subsidies are clarified, but structural cost actions, pricing discipline and Carelon growth give line of sight to stabilization in 2026.

|

Case in point: the WSJ reported today that ACA players are seeking double digit premium hikes next year amid volatility around government subsidy support for the marketplace plans. So I'll leave you guys with this question: are health insurers uninvestable at this point, and if so, what opportunities or challenges do these dynamics present? Would love your thoughts on the space. |

A Health System Merger Announcement Spotted in the Wild! |

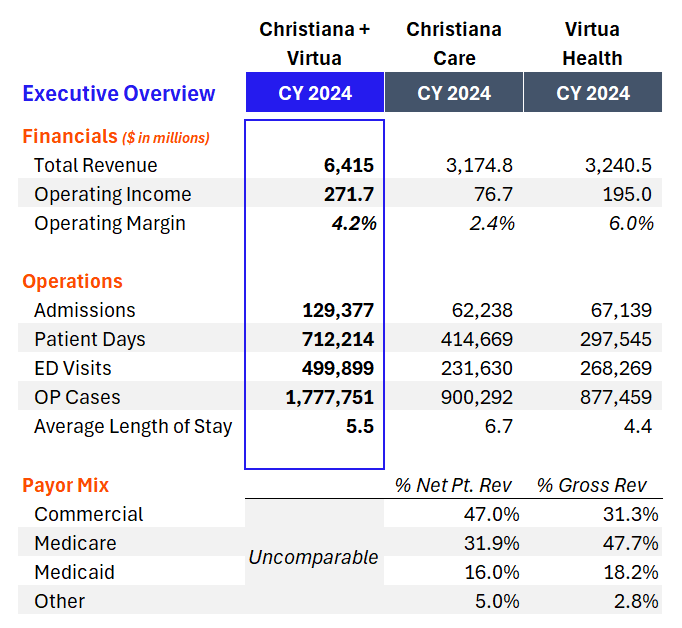

ChristianaCare and Virtua Health announced plans to explore merging into what would create a $6.4B+, 600-site health system across 4 states in the Northeast with a combined operating margin of 4.0%+ (as of calendar year 2024).

Based on financial performance, both health systems seem to be relatively healthy, so I would chalk this announcement up to opportunistic rather than survival-mode which is most of what we’ve seen in recent years. Though we’ve seen quite a bit of activity over the years in Pennsylvania and New Jersey (Nuvance, UPMC, Geisinger, etc.). Here are some numbers on what the combined entity would look like (sourced from EMMA bond disclosures). If you have additional context on this deal or their local market environments (from any perspective) please feel free to add color for me by replying!

|

|

|

Today at noon CT we're chatting about the BBB implications in context of ELV earnings above, health insurer woes, implications for providers, and whatever else is on members' minds. For plus members only - apply below! |

|

|

Royal Portrush has kicked off and with someone who has a 22 month old, it is absolutely wonderful to wake up with major championship golf ALREADY ON. Brian Harman with the -6 round 2!! Man seems to come alive one weekend a year and it just so happens to be links golf courses. As a fellow lefty, I love to see it. Then you have some of the usual names lurking around. Should be a great weekend. Enjoy the weekend Hospitalogists! See you Tuesday. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

Get your brand in front of 45,000+ executives and healthcare decision-makers. |

I'm building a community of leaders in corp dev and enterprise strategy

at hospitals and health systems to help us connect, learn, and grow together. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721 Want to ruin my day? Unsubscribe. |

|

|

|