26 October 2023 | Climate Tech

In defense of the 5% interest rate

By

There are many headwinds facing renewable energy deployment. Even as IEA forecasts that solar will become the #1 source of electricity generation between 2030 and 2040, in 2023, the renewable energy industry (and other cleantech sectors) is having a bit of a reckoning.

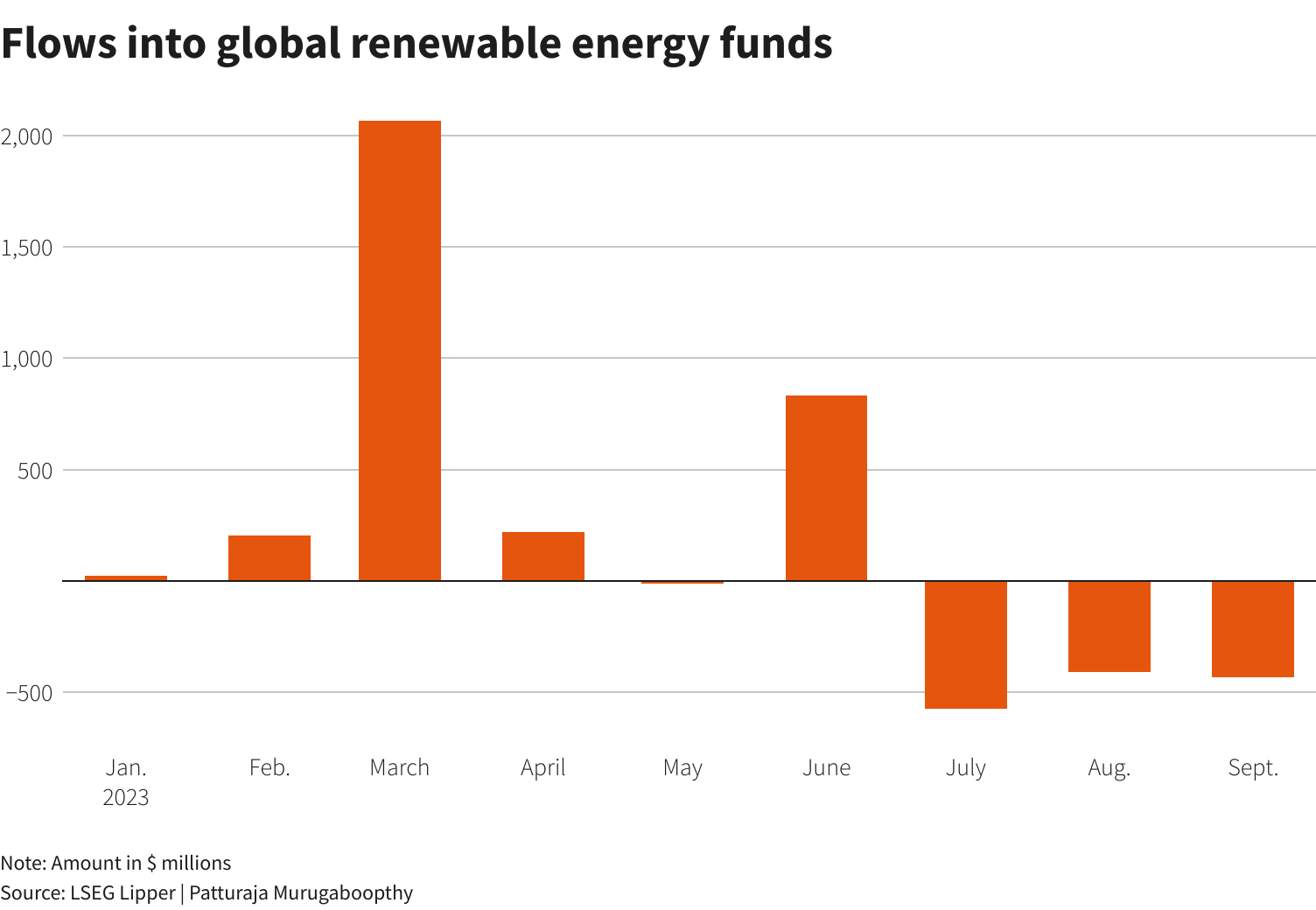

Countless publicly traded cleantech companies, from NextEra to Orsted to Li-Cycle, have shed anywhere from 20-70%+ of their market value in recent months. At the asset level, deploying projects is getting more complex, whether owing to interconnection backlogs, ‘supply chain’ issues, or now, Chinese restrictions on the export of raw battery materials. Amidst these challenges, money has flowed out of investment funds tracking renewable energy companies, reversing a recent trend.

Amidst all of these headwinds, another factor that crops up in discussion is interest rates.

It is tautologically true that when interest rates rise, the cost of financing any project increases. Most renewable energy projects are financed with a mix of debt, equity, and tax equity. As interest rates on the debt portion rise, so too does the holistic ‘cost of capital’ for any project. Even for projects that aren’t financed with debt, a higher rate environment can still raise costs as other players along a supply chain pass along the cost increases of their rising rate payments.

In light of this, there have been some spectacular media headlines of late. A Forbes article this month was titled “Central Banks Are Waging War On Renewables.” A Guardian article, also from this month, was titled “Central banks raising interest rates makes it harder to fight the climate crisis.”

The question I’m here to humbly explore today is whether higher rates are as much of a negative as we’re told. Having acknowledged that they do make things more expensive, let’s dig in further.

In defense of the 5% interest rate

I caught up with Barrett Bilotta, CEO of Agilitas Energy, this week to get his pulse on the renewable energy industry in the U.S. Agilitas Energy deploys distributed energy projects and is focused on standalone and solar + storage projects right now. Barrett corroborated the idea that renewable energy project developers are grappling with the rising cost of financing projects, noting:

The cost of money has pushed a lot of projects that were either mediocre or had a long lead time before the shovel would hit the ground to accelerate asset sales. You’ll start to see a lot more churn across companies, assets, projects, pipelines [in coming months].

Barrett and I also drew some distinctions here between projects that are and aren’t impacted significantly by rising rates. The projects that fold or need to shift gears because of a rise in rates are those that were most tenuous to begin with. How ‘good’ is a project if it can’t survive a 5% rate?

To be sure, the move in rates in recent years from 0% to 5% is not at all insignificant. However, interest rates are inherently a useful hurdle that productive projects need to clear. When interest rates were 0% three years ago, a massive amount of capital went to fundamentally unproductive things, whether you prefer to dunk on NFTs or 15-minute grocery delivery companies. Higher rates do raise the cost of capital, but they also concentrate capital towards more vs. less productive uses.

Suffice it to say that ‘strong’ projects that make economic sense and have sound fundamentals are still being deployed. Agilitas Energy is still humming away. In many ways, the first projects to ‘go’ are the ones that perhaps weren’t sound to begin with.

Is that a bad thing? Of course, we would like to see as much renewable energy deployed as possible. But if a project can’t bear what is a historically typical interest rate, it’s worth asking how valuable (assessed from a comprehensive perspective) it was in the first place.

If we follow that train of thought, the next question we bump up against is how much of global decarbonization can be accomplished in the mold of our ‘traditional’ economic system. That’s a familiar question.

If I put on my ‘traditional’ economist hat, perhaps a project that can’t survive a 5% interest rate isn’t a great project, as I stated above.

If I put on my climate tech analyst hat, I venture to guess that part of the reason that many of the projects that can’t survive a 5% rate should still be considered valuable is because of their emissions mitigation potential. Clearly, we’re still a long way away from a world that fully and effectively prices in the negative externalities of greenhouse gas emissions.

Still, renewable energy projects are already armed with significant tax incentives and mechanisms to valorize their emissions reduction potential. They got a boost from the IRA. They can sell renewable energy credits to valorize emissions reductions.

Especially considering that solar is oft touted as the cheapest energy source man has ever known, something in the “rates are killing renewable energy” argument doesn’t quite pencil for me. If the entire ‘fundamentally cheapest energy source’ thing was predicated in part on low-interest rates,’ as some Central Bankers have opined, then that’s an important caveat that wasn’t previously stressed.

Arguments against the 5% interest rate

Central bankers who control interest rates fear one thing most of all: Rampant inflation. Turning to arguments against higher rates, the idea that makes the most sense to me is as follows. If higher rates hurt decarbonization, our failure to decarbonize more quickly will also exacerbate future inflation from climate disasters. The costs of climate disasters are already mounting alarmingly:

- Insured losses from natural disasters in the U.S. now typically approach $100B a year, compared to $4.6B in 2000.

- Four of the five largest wildfires in California’s history have occurred since 2020.

- The average U.S. homeowner has seen their premiums spike 21% since 2015.

- 50,000 people lost insurance coverage for their homes in California this summer alone. Neither Allstate nor State Farm is writing new home insurance policies in California.

- Two out of three American homes are “underinsured.”

Climate risk-borne inflation isn’t something central bankers can inherently manage with interest policy. It’s a challenge that demands dramatic emissions reduction (not to mention adaptation). Against that backdrop, perhaps lowering rates to accelerate renewable deployment does pencil for central bankers, especially as many of them begin to count climate change as part of their mandate.

Further, I am sensitive to the fact that renewable energy projects are fundamentally more exposed to interest rate risk than legacy energy projects and infrastructure. Anytime you have the choice between building something new and operating an existing asset, like a natural gas power plant, it is harder to bear the costs of new construction (which are front-loaded) vs. operating the existing assets in a higher vs. lower interest rate environment. Said differently, higher rates do favor oil and gas infrastructure vs. new clean energy.

Still, tinkering with rates to accelerate decarbonization feels like the wrong lever. Rates impact everything in the global economy. Leaving rates too low could cause significant inflation across the entire economy, which could derail decarbonization just as significantly, if not more so. If rates were still 0%, maybe we’d all be lamenting runaway inflation in the price of the physical goods and raw materials needed to deploy clean energy. Maybe the articles would blame inflation rather than interest rates for ‘killing renewable energy deployment.’

The net-net

Rather than manage economy-wide rates, perhaps we need better direct policies and incentives specifically for clean energy, even if they’re in addition to what’s already out there. Perhaps policies, including potentially from central bankers, need to be specifically tailored to reduce interest rates clean energy project developers can access (e.g., ‘climate concessionary lending’).

It’s also critical that we’re incredibly clear-sighted in what we’re saying when we discuss the cost of different climate solutions. If they’re fundamentally more competitive than legacy oil and gas infrastructure, but only if rates are near 0%, then we should have been noting that all along.

Statements like ‘solar is the cheapest form of energy in the world’ are back to bite us now. Clearly, those statements obfuscate the complexity inherent to analyzing and comparing the cost of different energy generation sources.

Rather than parrot those simple refrains, it’s incumbent on all folks involved in energy and climate tech to iteratively approach decarbonization from a blank slate, asking, for instance, “How do we best deploy clean energy in all interest rate environments?”