26 January 2023 | FinTech

CBInsights’ Q4 Fintech Investing Summary

By

2022 was a very weird for the whole tech industry, but it was particularly challenging for VC’s. In the public markets, valuations for tech companies were getting slashed left and right—VC’s needed to figure out how that affected the private markets. And fintech was one of the hardest hit sectors—valuations fell dramatically and VC dollars to the sector dried up.

Having a summary on Q4 2022 is beneficial for us—we’ve been tracking and commentating on venture trends all year and I’m curious to see where we ended up:

Global fintech venture investments fell 62% YOY

A huge drop in venture capital investments across the board in 2022 vs 2021. Globally, $75.2 billion was deployed into the venture capital ecosystem. While that’s significant lower than 2021, its 52% more than the amount raised in 2020.

US fintech venture investments fell 50% YOY

US fintech VC investments fell a little less than the rest of the world, but still contracted 50%. With deals only dropping 9%, that implies that deal sizes are getting smaller. This makes sense considering mid-stage and late stage deals have shrunk significantly in the US between ‘21 and ‘22: mid-stage fell 5% and late stage fell 3%. More concerning was quarterly data—at $3.9 billion, its the lowest mark since Q1 2018.

LatAm VC funding drops 71%, but hits all time high on early stage market share

LatAm fintech venture funding dropped a ton—the most out of any geography. But that could be because 2021 was such an anomaly for the region, which is closely tied to crypto and is an up-and-coming sector in fintech. While VC dollars have tightened up, the market share for early stage deals reached an all time high of 72%. What does that imply? It could mean that VC’s are still bullish on the potential of financial innovation in the LatAm, and are taking more, but not as big, bets in the sector.

All fintech subsectors are down bad:

Payments, -49%

Banking, -63%

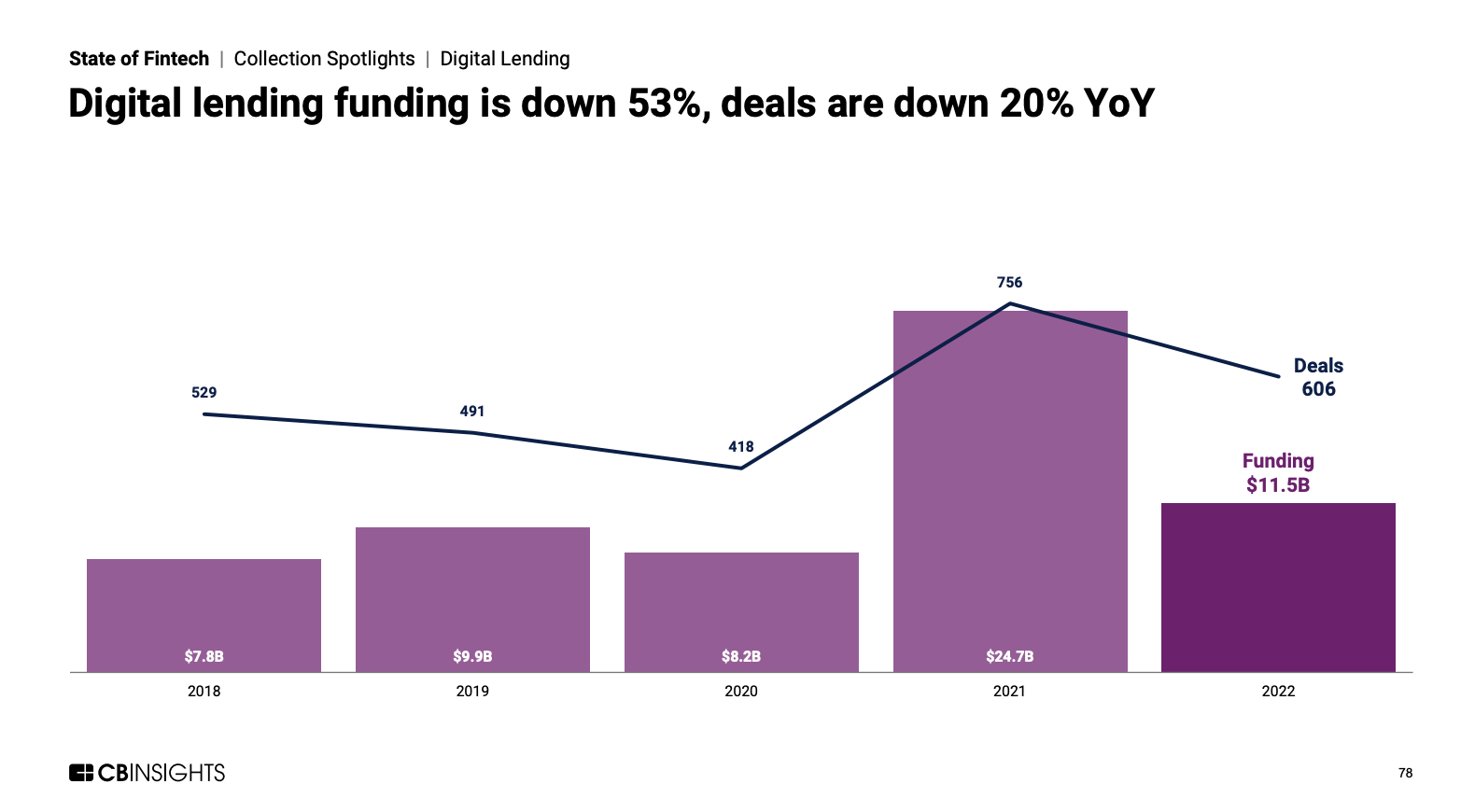

Digital Lending, -50%

WealthTech, -41%

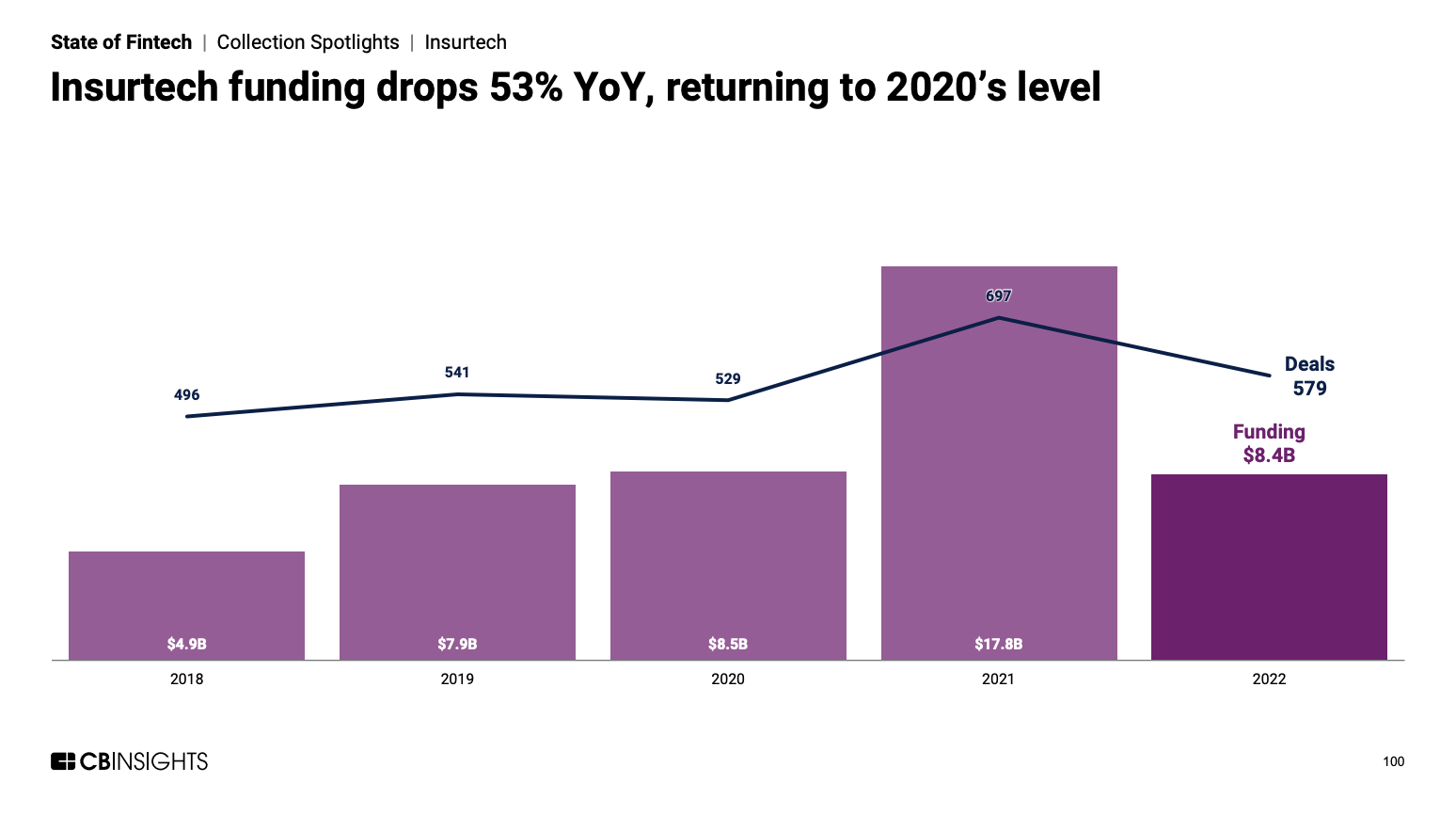

Insurtech, -53%

The most alarming drop is banking—not only does it lead other subsectors by double digits, but quarterly deals reached its lowest levels since Q2 2018. The rationale might be the fact that VC’s are realizing what a tough business neobanks are—you either need to become fully regulated or need to figure out multiple revenue streams in order to be profitable per user. As customer acquisitions rise, expect more VC’s to stay away from neobanks, at least for awhile.

In conclusion, it is clear fintech had a challenging Q4 2022, as venture investments to the sector fell significantly. While the frequency of deals haven’t been too impacted, particularly in early stage investments and geographies like LatAm, its the other subsectors that really drag down the whole portfolio—particularly neobanking and payments. A prolonged market contraction is likely, so we’ll have to wait and see how VC’s adjust.