15 December 2022 | Climate Tech

Carbon removal hub(bub)

By

If you wanted to develop a technology and start a business, and your goal was collecting small pebbles off a beach, which beach would you choose between the two options below?

- Beach A has ~400 pebbles for every 4,000 grains of sand

- Beach B has ~400 pebbles for every 1,000,000 grains of sand

You might pick Beach A. Given an equal amount of work, you’d expect to gather more pebbles; On Beach B, you’d spend more time sifting sand.

This year has proven that choices aren’t always that simple. The carbon removal industry, in which companies develop approaches to remove CO2 from the ambient air, has gotten red hot, with headlines, upsized funding rounds, new venture firms, and hype galore.

Carbon capture, which seeks to remove CO2 from point-source emissions, and has been a concept since the 1970s, has fallen out of favor, at least relative to removal. Even as carbon capture deals with inputs where the percentage of CO2 may be as high as 12-14% (coal flue stacks) or at least 8-10% (natural gas flue stack). In comparison, the amount of CO2 in the atmosphere is roughly 400 parts per million (0.04%).

While CO2 in the air is ~2,500x more diffuse than in flue stacks (example above), carbon removal isn’t 2,500x harder than carbon capture. In fact, for direct air capture, the minimum work calculation nets out with carbon removal around 3x the difficulty of carbon capture (Carbon Capture, Herzog, 2018).

Still, I offer this set-up as food for thought as we wrap up the year in carbon removal and summarize more recent developments.

The ‘momo’ trade

Invariably, there are tech sectors that are ‘hot,’ attracting a lot of attention, investment, employee applications, and headlines. Two years ago, it was crypto. Now it’s AI.

Climate is ‘hot,’ too, overall, and within climate, carbon removal is one of the hottest areas of all. To underscore the momentum the industry’s built this year, here are some highlights:

- Frontier raised close to $1B to make advanced market commitments to carbon removal companies for their future carbon removal credits

- Climeworks, one of the oldest carbon removal companies (commercializing direct-air-capture), raised a ~$650M equity round

- Lowercarbon Capital raised a $350M dedicated fund to invest in carbon removal companies’ equity

By some estimates, climate and climate tech funding has ‘captured’ a quarter of all venture funding this year. And with significant contributions from large rounds like Climeworks’, carbon removal and broader ‘carbon market’ companies took home no small piece of the overall climate pie. In the first half of the year, ~$1.

Carbon removal and ‘carbon tech’ are some of several ‘momo’ (i.e., momentum) trades in climate tech currently. Whether that endures is TBD.

Taking a step back

If you’re new here, you may have some questions. Are we giving up on emissions reductions? Is there a moral hazard to carbon removal, as it might offer cover to ignore emissions reductions entirely? What’s up in carbon capture, as we asked earlier?

For one, despite all the funding numbers and announcements, the scale of the carbon removal industry is minuscule. There are only a handful of direct-air-capture facilities operating globally. Any one plant’s capacity might be ~5,000 tonnes of CO2 removed annually. Other carbon removal companies we’ve covered, like Charm Industrial (listen to the pod here), likely managed similar volumes this year.

For context, global annual emissions in CO2 equivalent are roughly 50B, as in billion tonnes. 5,000 tonnes of carbon removal represents about ~3 seconds of annual, global emissions. Even nature-based carbon removal solutions that are more scalable and developed, such as reforestation, represent millions of tonnes of annual removal capacity, which brings us into the range of an hour of annual, global emissions.

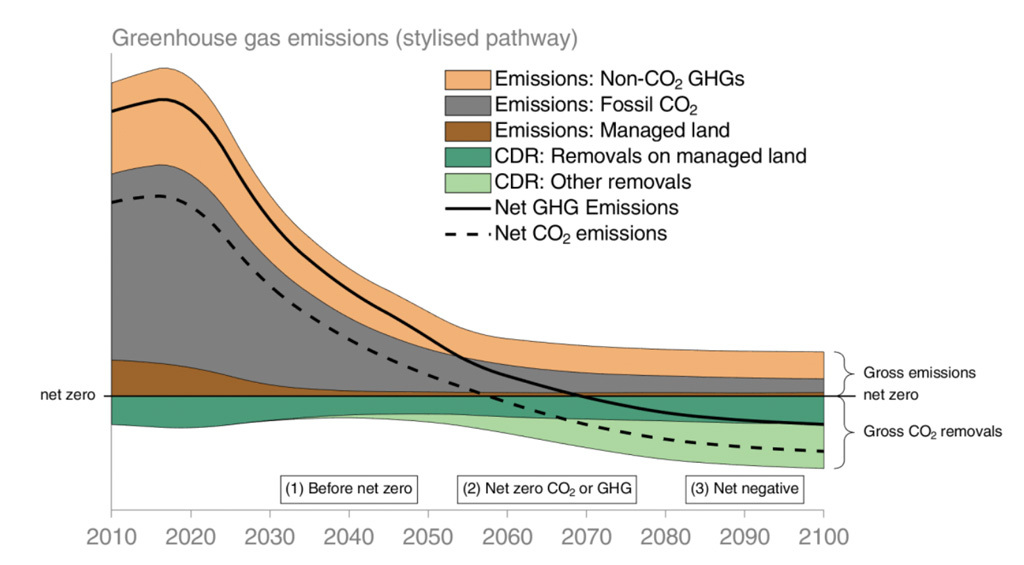

Further, since the Industrial Revolution, emissions have already increased the CO2 concentration in the atmosphere by approximately 40%. As a result, most models for climate change mitigation include scaling carbon removal not just to offset hard-to-reduce emissions but as a way to sweep up legacy emissions in the atmosphere. More carbon removal capacity is necessary, and soon.

For instance, IPCC modeling and research on pathways to limit global warming to 1.5* C almost all include carbon removal capacity picking up significantly in coming decades:

All analysed pathways limiting warming to 1.5°C with no or limited overshoot use CDR to some extent to neutralize emissions from sources for which no mitigation measures have been identified and… to achieve net negative emissions to return global warming to 1.5°C…

None of that offers a clean distillation of what ideal investment percentages would look like between emissions reduction and carbon removal. Nor have we spent much time talking about carbon capture and its forecast role in mitigating climate change either. We will in a future newsletter, but for now, suffice to say the answer is… no one knows for sure!

Looking ahead

Controversy and questions aside for a minute, things are still full steam ahead for the carbon removal industry, especially in the U.S.

This week, the Department of Energy announced an additional $3.

While approaches to carbon removal differ significantly, all companies have some things in common, like requiring access to storage and sequestration solutions for the carbon they remove from the air, access to renewable energy so the CO2 they capture isn’t ‘undone’ by emissions from electricity use, etc…

In speaking with a representative of one carbon removal company yesterday, they noted that their team is ‘scrambling’ to understand the hub proposal’s implications and get their application in order. Happy holidays!

They also noted that companies that have gone through other ‘hub processes’ with the DOE found the application orderly and organized, which is encouraging news. Finally, it’s also worth noting that as hubs spin up, the DOE wants to ensure environmental justice considerations are at the forefront of the companies’ applications. Which is refreshing – in a podcast earlier this fall, Peter Olivier and I discussed why it’s critical that this nascent industry partners with local communities and brings them into the fold.

Meanwhile, Frontier, the advanced market commitment fund we discussed earlier, announced it facilitated a fresh $11M in carbon removal purchases for Stripe and Shopify from seven firms: Arbor, Captura, Carbin Minerals, Carbon To Stone, Cella, CREW, and Inplanet. Here’s a Twitter thread on these start-ups.

Frontier’s stamp of approval is a decisive vote of confidence for these firms. In their write-up, Frontier also noted they’re seeing “increasing diversity in approach” from companies applying for their funds across removal and storage. Which is good; a mosaic / portfolio approach to carbon removal solutions (and climate solutions in general) is needed. We don’t know what tech will be most effective. Some will 1,000x their removal capacity. Others will founder. Funding many offers a higher chance of a few big winners.

The net-net

Sometimes people seek out the glory of doing hard things. Carbon removal is more expensive and technically challenging than most opportunities for emission reductions. Perhaps we feel like we deserve the hard route as we lag on climate change mitigation.

And while necessary, I’m also conscious of and almost wary of presenting carbon removal as the success story for 2022 in climate tech. If you spend your time swimming in tech and venture capital circles, carbon removal is top of mind. Most people don’t however. There are countless other sectors that are relatively underfunded, under covered, and will impact more people more quickly.

All that said, significant future carbon removal capacity is, in my opinion, as inevitable as it may seem improbable right now. Tracking the story of the industry’s growth over the next decades will be fascinating and should make for a great book in 2030 or 40. I’ll stay on top of it for you.