17 February 2022 |

Inside The Cannabis Industry’s Battle With 280e

By Jay

Cannabis Tax Codes

How much money are U.S cannabis businesses losing from 280e…

We’re keeping the tax talk going and discussing the “American Cannabis Revolution” between the federal government and state-licensed businesses.

There’s (almost) nothing new under the sun, however, and similar to Great Britain’s attempt to tax American colonists without proper representation; in 2022 U.S. cannabis businesses are being forced to pay taxes to a federal government that won’t even recognize them as legitimate.

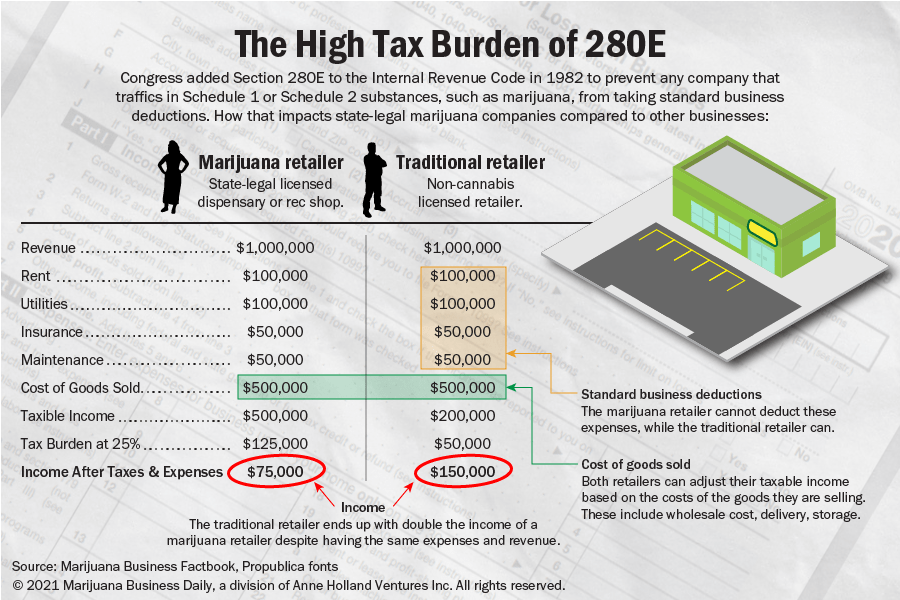

The Origins Of 280e

If you’ve been subscribed to The Green Paper for a few months, you might remember a recent edition talking about tax code 280e and the story behind it.

Long story short, an illicit drug dealer sued the tax court in an effort to claim business expenses on his taxes. He won and was able to write-off several thousand dollars in expenses, like traveling to San Francisco

Tax code 280e was formed the next year, which says businesses who are handling controlled substances can’t claim business expenses on their taxes.

Where a traditional, non-cannabis retailer might take home $150,000 in income after taxes and expenses, a cannabis operator might take home just $75,000; despite equal revenue, rent, utilities, insurance, etc.

{kind=link}

There have been efforts in place to repeal Section 280e for years.

The IRS case involving California-based cannabis company, Harborside, is one of the most publicized battles of all. It was eventually ruled that the cannabis company owed millions of dollars in back taxes, for improperly claiming expenses for a business handling a federally illegal substance.

Harborside is one of California’s largest and most successful cannabis companies. It has been involved with a 280e battle for years, first beginning in 2010 when the IRS audited an Oakland dispensary for the years 2008 and 2009.

The federal government, and the IRS, have repeatedly blocked efforts to repeal 280e or at the very least, allow companies like Harborside some leeway.

At one point, federal prosecutors were attempting to seize Harborside Health Center, the largest medical-cannabis dispensary in Oakland circa 2016, but that threat was eventually removed and the focus remained on Harborside’s taxes.

The court ordered Harborside to pay $2.4 million in back taxes, reflecting tax years ending July 31st, 2007 through July 31st, 2012.

(CHAMP) vs. Commissioner

CHAMP is one of, if not the only, business to successfully challenge the IRS [https://casetext.com/case/californians-helping-to-alleviate-med-problems-inc-v-commr-of-internal-revenue] over a 280e tax case. It’s a 2007 case, and the 2015 case we mention below (spoiler alert): unsuccessfully tries to follow the same playbook.

CHAMP’s primary line of business was providing counseling and other caregiving services to California adults with debilitating diseases. Additionally, clients were provided with medical cannabis, in accordance with California law. The IRS claimed CHAMPS improperly claimed deductions, and treated them as a plant-touching company.

It was eventually ruled that 280e does not affect expenses associated with caregiving services, and therefore CHAMPS can deduct business expenses from that line of business. The organization, like other plant-touching businesses, can’t claim expenses associated with medical cannabis.

Olive vs. Commissioner

A 2015 case, Olive v. Commissioner, involves medical cannabis dispensary operator Martin Olive and the local tax commissioner.

Olive owned The Vapor Room, a place to purchase medical cannabis and consume it on-site with Vapor Room-issued vaporizers.

Olive claimed business expenses for two tax years. The IRS blocked this and Olive petitioned the tax court. The court found 280e prohibited The Vapor Room, and businesses like it, from claiming ordinary business expenses on their taxes.

The Vapor Room argued it provided additional services, not just medical cannabis, and should therefore be able to claim business expenses on those services.

The food, beverages, art supplies, and additional services were free, but patrons paid for the medical cannabis. This immediately dwindled Olive’s scope of business to just medical cannabis and precluded him from claiming traditional expenses.

Looking Forward

The high tax burden associated with operating a cannabis business is crushing even successful operations, who can’t afford to go to market under such strict tax regulations. California’s legal cannabis industry is being swallowed by the illicit market, as licensed operators beg Gov. Gavin Newsome to take action.

Something has to change, unless regulators are seeking to create a cannabis industry whereby only the largest companies can weather the storm that is outrageously high taxes, forced to be paid by even small cannabis companies.

Our Take

Since 2014, U.S. states have generated over $8 billion USD in taxes from the adult use cannabis market alone, such that it’s inexcusable that cannabis companies are forced to pay taxes while simultaneously being treated as criminals in the U.S.

In ideal world, cannabis businesses would continue to challenge tax code 280e in court. The more media attention that can be drawn to these cases, the more pressure will be put on lawmakers and other decision makers to act and change the circumstances for legal cannabis businesses.

That said, for many cannabis companies, simply staying afloat until these policies change is the #1 priority, so allocating resources to challenge the federal government in court is an expense they cannot justify.