You might have noticed that there’s been a bit of drama in banking-as-a-service (BaaS) lately.

That’s obviously a significant understatement.

It’s also, from my perspective, a good thing. BaaS – the technical, legal, and operational integration between chartered banks and non-bank companies – is important. While it has existed in its modern form for the past 15 years or so, the explosive growth in fintech and embedded finance over the last 5 years forced BaaS into an accelerated evolutionary state. During that time, everyone – banks, fintech companies, regulators, and humble newsletter writers – has been trying to figure out how to match up supply and demand and safely enable non-bank companies to make banking products available to their customers.

We’ve all learned a lot over the last 5 years!

Recently, regulators have begun to provide more clarity on the way forward for BaaS.

And as they do that, I think it’s worth reflecting on the following question – who is BaaS for?

Competition Confusion

While most bank regulatory agencies in the U.S. don’t have an explicit statutory mandate to promote competition, it has long been a stated goal of financial services policymakers (regulators, legislators, consumer advocates, etc.) to encourage the development of a large, vibrant, highly competitive market for financial products and services.

This is a uniquely American idea.

In a recent speech, Michael Hsu, the Acting Comptroller of the Currency, explained why the U.S. banking market should look different than banking markets in other countries:

The U.S. economy is uniquely diverse, dynamic, and large. These attributes distinguish the economy and banking system of the U.S. from those of other countries. To understand why the U.S. banking system should not, for instance, look like Canada’s or the UK’s, which are dominated by a small handful of large banks, it helps to unpack each of these attributes.

In his remarks, he described why the U.S.’s diversity (economic, demographic, and geographic), dynamism (how quickly our economy evolves relative to other countries), and size (the U.S. economy is the largest in the world, with a GDP of nearly $27 trillion) justifies a thoughtful approach to policy questions on topics like market consolidation.

And he’s not alone. Most policymakers share the belief that it would be bad for the U.S. financial services industry to end up being dominated by a few massive institutions.

Why do they believe this? By promoting a more diverse and competitive financial services ecosystem, what goals are these policymakers trying to advance?

As far as I can tell, there are two primary goals – making banking products better and making banking more accessible.

Let’s unpack each of those.

The concern with a consolidated banking market, on a product level, is that it will cause banks to stop innovating, and consumers will be stuck with clunky, generic products and inconvenient, one-size-fits-all experiences. Federal Reserve Governor Michelle Bowman elaborates on the benefits of competition in encouraging product innovation:

Join Fintech Takes, Your One-Stop-Shop for Navigating the Fintech Universe.

Over 36,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Competition is vital to ensuring that we continue to have a vibrant and innovative banking industry. … [In the last 10 years] we’ve seen how competition has led to the adoption of a suite of digital products and services by banks of all sizes. From remote deposit capture, online account openings, and automated underwriting, to interactive teller machines, banks with more than $1 trillion in assets and those with less than $100 million in assets are both able to quickly onboard new technology to meet consumer demand. This has further led to a proliferation of tailored products and services that meet the unique needs of bank customers.

When it comes to accessibility, the concern with market consolidation is that it leads banks to prioritize certain markets and customer segments over others, leading to a loss of access for those that don’t make the cut. The common metaphor used to describe this problem is banking deserts. Here’s Rohit Chopra, Director of the CFPB:

When the banks shuttered, nothing replaced them. Instead, we see “banking deserts,” communities lacking access to in-person banking facilities. There are large swaths of areas with no bank branches all over the United States because of bank consolidations but 65 percent of existing banking deserts and 81 percent of potential banking deserts are located in rural areas.

Why is local, boots-on-the-ground banking so essential in rural communities? Director Chopra explains:

Rural economies and rural businesses require specialized expertise to meet their credit needs. When taking out a loan to buy large parcels of land, it helps to have a banker who understands local zoning. Rural banking is also different from city banking because the agricultural economy is different. For example, the financial health of farmers depends on unpredictable precipitation and extreme weather events, not to mention highly volatile commodity prices that can upend expectations seemingly overnight. When Main Street banks pack up and leave town, and when issues are instead funneled through national call centers, there is a loss of local, on-the-ground knowledge that is the basis of good customer service, and good banking.

I think this specific concern about banking deserts in rural communities is completely fair (I live in Montana and have seen this problem up close), but what’s interesting is how general regulatory concerns about market consolidation almost always end up morphing into a more specific mandate – to protect community banks at all costs.

Here’s Director Chopra again, commenting on the FDIC’s updated policy on bank merger transactions:

Given the unique role federally insured depository institutions play in the economy, Congress and the regulators should consider broader adoption of size and growth caps. There is a strong case to be made that given the critical role that entrepreneurs and small businesses play in our economy and the vast geography of our nation, the U.S. benefits more from having a large number of small and midsized banks, rather than a market structure with just a handful of very large banks, like in Europe and China.

So, it’s not just that we want more competition to help us maintain accessibility (especially in rural communities) and push all banks to continually improve their products and services. We want that competition to come from traditional community banks operating with a branch-based distribution model.

There are a couple of problems with this.

First, in the absence of hard-and-fast rules preventing bank consolidation (which has been the case in the U.S. since the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994), banks have every incentive to get as big as possible. Charles Calomiris and Stephen Haber do an excellent job summarizing why bank consolidation became such a popular strategy in the late 1990s in their book – Fragile By Design:

The incentives to become a megabank were multiple. One obvious benefit was an increase in organizational efficiency. A bank with branches spread across the country could diversify risk across regions. It could also reap economies of scale by spreading its overhead costs for expensive information technology and high-salaried personnel across a larger asset base. Becoming bigger also enabled a bank to capture economies of scope, widening its income stream by providing a broader range of products and services. An additional advantage of becoming a megabank was the potential for obtaining market power. The ability to earn monopoly rents was not an inevitable consequence of increased size, but it was a possibility. A final potential advantage to growing large was the implicit subsidy of too-big-to-fail protection.

Put simply, in a market that permits consolidation, it’s basically impossible to compete if you’re not constantly getting bigger.

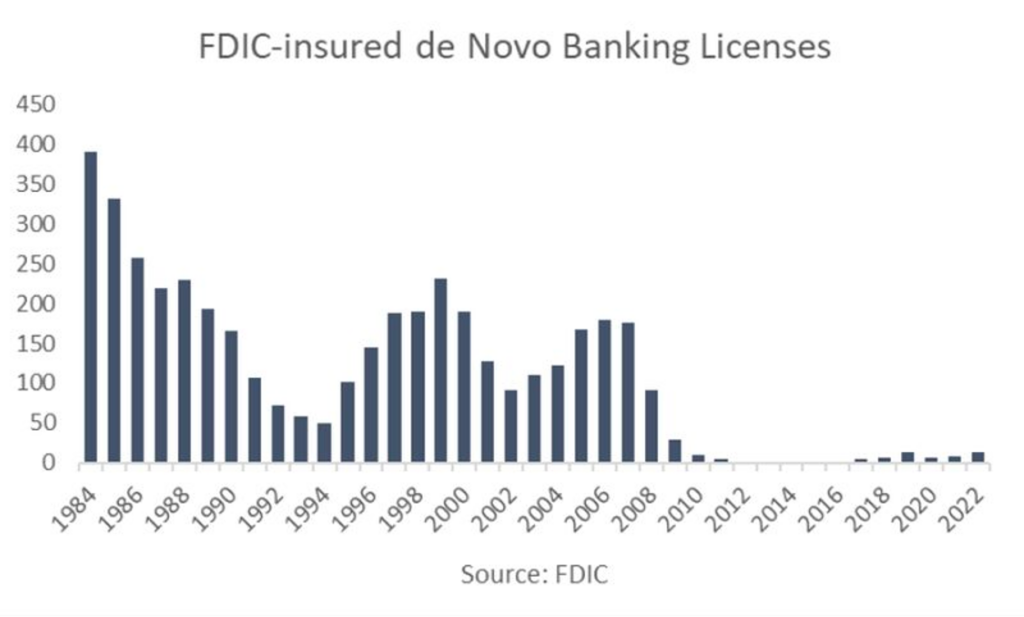

Second, to the extent that you believe smaller and more nimble banks can effectively compete with the megabanks (and there’s not a ton of evidence to support this belief), you would still need a steady supply of new chartered banks to replace the ones that are getting gobbled up. The problem is that since the great financial crisis, that supply has dried up. This chart shows the number of FDIC-insured de novo banking licenses granted annually in the U.S. between 1984 and 2022:

The reasons for this decline are myriad and complex – increased costs to acquire a license and comply with regulations, falling premiums on M&A transactions, etc. (read this article by my Bank Nerd Corner podcast co-host Kiah Haslett for more details) – but the end result is that the U.S. is no longer producing nearly enough new banks to replace the ones we lose (even with regulators’ increasingly negative positions on bank M&A).

Third, and most importantly, this focus on preserving community banks as the only acceptable vector of competition for megabanks ignores a much more effective vector of competition – a group of companies that Jamie Dimon says that the megabanks should be scared shitless of – fintech companies.

Fintech Improves Banking

Fintech is well-suited to deliver on policymakers’ competition-related goals.

You want to make banking products better?

Allow me to introduce you to B2C and B2B fintech companies – neobanks, online lenders, digital brokerages, PFM providers – who specialize in manufacturing differentiated financial products; products that force traditional banks to up their game, to the benefit of their customers.

Pay-in-4 BNPL is a good example. As I wrote about recently, after pay-in-4 BNPL exploded in popularity in 2020 and 2021, large credit card issuers responded by introducing similar installment lending functionality within their existing card products. According to research from the CFPB, this feature has become surprisingly popular with cardholders:

Why is this feature so popular?

I think the answer is, again, fairly simple – retroactive BNPL functionality makes it easier for consumers to use their credit cards rationally, as a payment instrument (primarily), and as a source of additional liquidity (where necessary).

Cardholders are acting rationally! When they need to make a big purchase on their card, which they won’t be able to easily pay off by the end of the month, they are utilizing this BNPL feature rather than revolving a balance.

For all credit card users, from deep subprime to superprime, credit cards with built-in BNPL are a better product design than traditional credit cards.

This is the benefit of fintech companies competing with banks. They are pushing banks to build better, more rational versions of their products.

You want to make banking more accessible?

Allow me to introduce you to embedded finance, a tried and tested distribution model for financial products that has been supercharged in recent years by the rapid adoption of software across every industry and the growing awareness of and interest in financial services as a monetization and customer engagement mechanism among companies in those industries.

Small business lending – the product category that policymakers most frequently cite when pining over the disappearance of community banks – is a good example. According to my back-of-the-envelope calculations, Square and Shopify have extended roughly $14 billion in loans to small businesses since launching their business lending divisions in 2014 and 2016, respectively.

Is that still not good enough for you? Do you believe, like Director Chopra, that there are certain local, boots-on-the-ground banking activities that community banks are especially (perhaps uniquely) qualified to provide?

Well then, allow me to refresh your memory on an important point – fintech partnerships are one of the only viable, non-M&A ways for community banks to grow and thrive in today’s rapidly consolidating market.

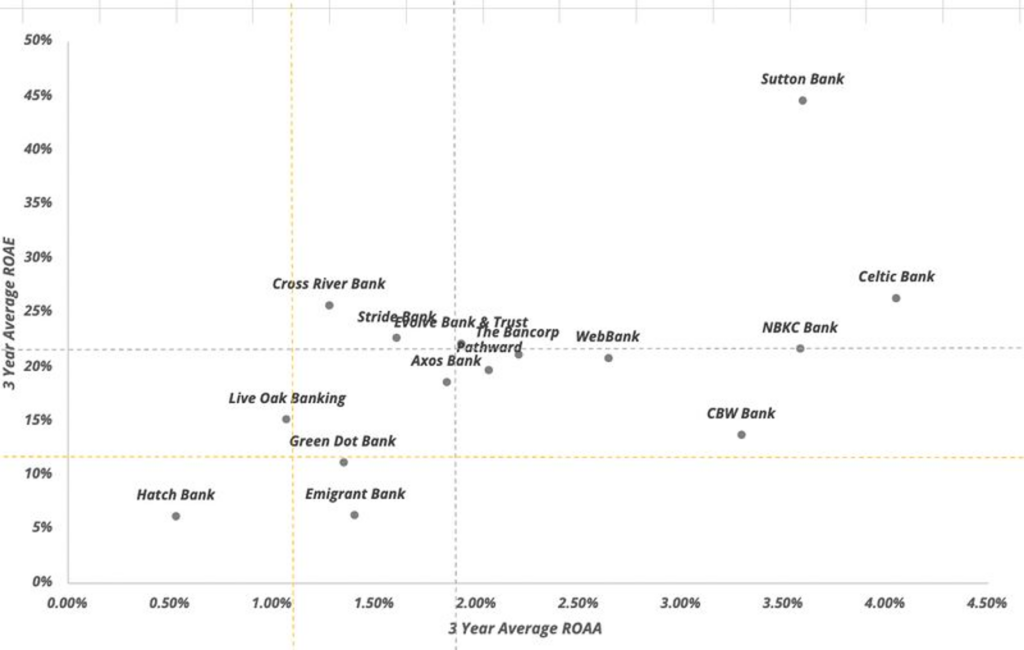

According to an analysis shared by Jonah Crane, Partner at Klaros Group:

The median partner bank return on average assets for the period 2021-2023 was 1.92%, compared to the community bank median of 1.1%, and median partner bank return on equity was 20.8% compared to the community bank median of 11.4%. These numbers actually outpace the performance of the same cohort of partner banks for the period 2018-2020.

This persistently great performance explains why, despite all the regulatory drama in BaaS right now, the percentage of mid-size banks that report that they are in the process of developing a BaaS strategy in 2024 (7%) was nearly double the percentage in 2023 (3.7%), according to Cornerstone Advisors’ What’s Going On in Banking study.

Fintech forces banks to innovate. It improves the accessibility of banking products for underserved customer segments. And it acts as a critical source of stability and profitability for community banks.

So why is it that when most policymakers talk about the importance of maintaining the competitiveness of the U.S. banking market, they either fail to mention fintech as a potential solution or paint it as part of the problem, as Senator Sherrod Brown, Chair of the U.S. Senate Banking, Housing, and Urban Affairs Committee, did in his opening statement in a hearing with the heads of the prudential regulatory agencies last year (emphasis mine):

We have created a financial system where just a handful of the largest banks now hold $14.75 trillion in assets—more than half the nation’s GDP.

Fewer and larger banks mean consumers have less choice in the marketplace for banking services.

Less competition means banks pay depositors less and charge higher fees.

Mergers and acquisitions also serve as justification for branch closures, particularly in rural areas and working-class communities. We’ve seen that far too often in Ohio.

And we know that drives more consumers out of the banking system toward high-fee, predatory non-bank financial companies—like check cashers and payday lenders and fintech apps.

There are plenty of problematic fintech apps out there (I’ve written about many of them in this newsletter), and fintech, when enabled irresponsibly, can absolutely pose risks to the banking sector. But lumping fintech – as a category – in with check cashing and payday lending?

Come on, man!

We Have to Find a Way Forward for BaaS

This is the context in which we need to think about everything that’s happening right now with BaaS.

We are in a market that is structurally set up to encourage consolidation. That market is overseen by policymakers who, for the most part, bemoan that consolidation while, at the same time, remaining steadfastly critical of the creative ways in which smaller market participants attempt to compete with their larger peers. This is bizarre, as Travis Hill, Vice Chairman at the FDIC, observed in a speech last year (emphasis mine):

Another way banks compete is through innovation and efficiency, which over the long term can involve things like transitioning away from higher-cost branches and toward lower-cost websites, and engaging in third-party partnerships or banking-as-a-service. Yet these are all types of activities that bank regulators currently view skeptically. Of course, capitalism is built on competition, and competition has many benefits, but it appears that regulators want a merger policy that encourages more competition, yet dislike many of the things banks do when faced with stiffer competition.

The status quo is unacceptable. If we truly want a vibrant, diverse, and highly competitive financial services ecosystem, and if we assume that we won’t be able to stuff the internet and interstate banking back into the boxes they came in, then we need to find a way to turn BaaS into a viable long-term business for banks and an accessible on-ramp for non-bank companies looking to offer banking products.

That’s obviously a tall order, and solving for it is beyond my capabilities and certainly beyond the scope of this essay.

However, I do have one thought to add to the debate – we need to think carefully about the cost of compliance.

The Cost of Compliance

Remember Jonah Crane’s numbers on BaaS banks’ ROA and ROE over the last three years? Well, there’s a nuance in those numbers that I neglected to share. Despite the overall improvement during that three-year period, partner bank returns for both 2022 and 2023 were actually down from 2021 levels. Additionally, the average efficiency ratio of partner banks (non-interest expense divided by net revenue) increased from 61% to 67% between 2022 and 2023.

What drove these decreased returns and higher (i.e., worse) efficiency ratios?

Compliance costs.

Regulatory scrutiny on BaaS has raised the cost for BaaS banks to run fintech programs. This has resulted in these banks raising the floor on the size of the programs they are willing to work with (anecdotally, I’m being told that some banks are requiring at least $5 million in equity capital for any prospective fintech partners).

This is a logical shift for the banks, but it’s a bad outcome for the ecosystem overall. By raising the floor, we are shrinking the field of competition and making it more likely that diverse fintech founders from non-traditional backgrounds (who, in the best of times, struggle to raise money from VCs) will be unable to get their ideas off the ground.

Why, specifically, is the cost of compliance going up?

People.

All the BaaS banks that I have spoken with have told me that regulators’ answer to the question of how they can improve their risk management controls and compliance processes is simple: add more bodies.

Historically, this has been the way that regulators have resolved the compliance issues (particularly BSA/AML issues) that they have uncovered inside the banks that they supervise.

When we hear the words “consent order” these days, our minds immediately jump to BaaS and community banks. However, 10 years ago, it was megabanks like JPMorgan Chase and U.S. Bank that were routinely getting slapped by regulators for BSA/AML failures.

And the language used by regulators and prosecutors in describing these failures makes it clear that they pinned the blame, primarily, on a lack of staffing. Here’s the United States Attorney for the Southern District of New York describing the reasons for the $528 million fine that U.S. Bank was forced to pay in 2018 for BSA/AML failures dating back to 2009 (emphasis mine):

U.S. Bank’s AML program was highly inadequate. The Bank operated the program ‘on the cheap’ by restricting headcount and other compliance resources, and then imposed hard caps on the number of transactions subject to AML review in order to create the appearance that the program was operating properly.

And in addressing these regulatory concerns, the big banks did exactly what regulators asked them to do – they threw more bodies at the problem.

In order to deal with a series of compliance issues in the early 2010s, JPMorgan Chase hired 3,000 additional staff to work in risk, compliance, legal, and finance, including 500 who were dedicated specifically to AML compliance.

I’m sure this was annoying to JPMC (it ate into its profit margin), but it was absolutely feasible.

This approach is not feasible for community banks providing BaaS today. These banks can’t scale their human compliance resources linearly as they add new fintech programs. There has to be economies of scale, at a certain point, or BaaS, as a business, stops making sense.

So, how do we do that?

The Difference Between Manufacturing Innovation and Distribution Innovation

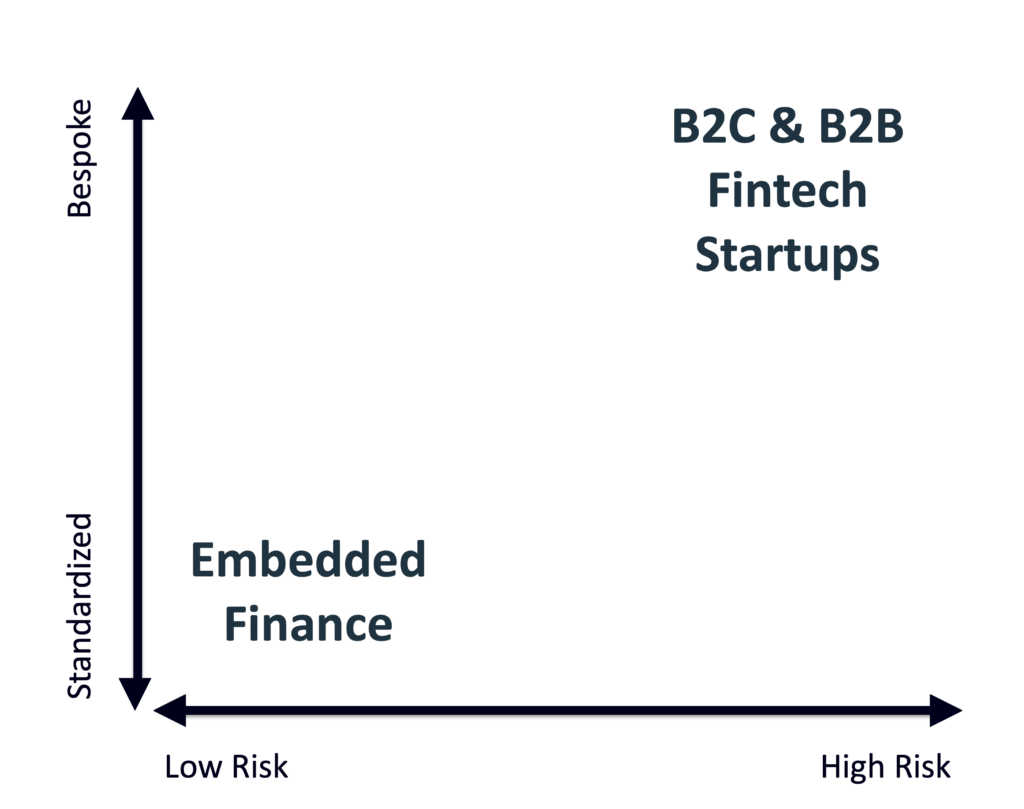

It’s obviously a tricky problem to solve, but one idea is to start drawing a distinction, when it comes to the required level of compliance oversight, between fintech programs built around manufacturing innovation and programs built around distribution innovation.

Manufacturing innovation, which serves the policy goal of making banking products better, is the province of B2C and B2B fintech startups.

These providers compete by building highly differentiated, bespoke wedge products that they can use to attack market incumbents. They constantly put pressure on the assumptions undergirding traditional bank products (why can’t a deposit account be both a checking account and a savings account?), and they live in the edge cases. They create a lot of value, but they also come with a lot of risk; risk that justifies more intensive, human-directed compliance controls and oversight.

Distribution innovation, which serves the policy goal of making banking more accessible, is the province of embedded finance.

A non-bank brand offering an embedded finance product doesn’t typically compete on the basis of the financial product itself (its design, function, price, etc.), but rather on the unique distribution advantage that it has built through its primary business, which gives it a captive customer base to sell into and a wealth of data to target and personalize that sales effort. The product isn’t the source of the brand’s competitive differentiation, which means that it (and the technology and processes that support it) can be standardized, and, ideally, that standardization can allow for a more efficient, automated, and scalable approach to compliance. This is how, over time, compliance and risk management in more mature embedded finance categories (co-brand credit cards, indirect auto lending, etc.) have evolved, and I don’t see why newer embedded finance categories (banking, B2B charge cards, etc.) can’t follow a similar path.

Who is BaaS For?

It’s easy for a conversation about competition as a policy matter to quickly become abstract and disconnected from reality. Trying to answer questions like, “What’s the right number of banks to have in the U.S.?” is an interesting academic exercise, but it risks obfuscating the essential truth of the matter.

The point of competition in financial services is to make money work better for everyone: the gig worker who needs to get paid as quickly as possible to make ends meet, the small business owner who needs a one-stop shop for all their banking and payments needs, the startup founder who needs an automated CFO in their pocket to make smart treasury management decisions. Everyone.

Which brings us back to the question I posed at the beginning of this essay.

Who is BaaS for?

BaaS is for everyone who benefits from a more competitive financial services ecosystem.

Unless your name is Jamie Dimon, that means BaaS is for you.

About Sponsored deep Dives

Sponsored Deep Dives are essays sponsored by a very-carefully-curated list of companies (selected by me), in which I write about topics of mutual interest to me, the sponsoring company, and (most importantly) you, the audience. If you have any questions or feedback on these sponsored deep dives, please DM me on Twitter or LinkedIn.

Today’s Sponsored Deep Dive was brought to you by Unit.

Unit is a leading financial infrastructure platform for banks and technology companies. Unit provides digital banking technology and embedded finance solutions to enable banks and technology companies to reach customers via digital channels. Headquartered in New York City, Unit is backed by top investors, including Insight Partners, Accel, Better Tomorrow Ventures, and Flourish Ventures.

For more information, visit www.unit.co.

Created By

Alex Johnson

Join Fintech Takes, Your One-Stop-Shop for Navigating the Fintech Universe.

Over 36,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Events

Staying up-to-date with the fast-paced, dynamic changes in the fintech industry can be challenging! Join Alex as he demystifies our industry’s most pressing news and answers your burning questions.

Fintech moves fast. But here at Fintech Takes, Alex Johnson and his rotating panel of guests move faster so that you can stay on top of the latest and greatest news in the industry without breaking a sweat.