{beacon}

| |||||||||||

| |||||||||||

| | |||||||||||

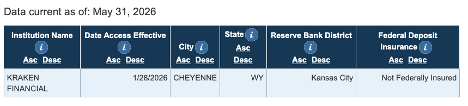

Hello! Kiah here. Welcome to Fintech Takes Banking, my weekly newsletter where I highlight things I think are interesting or important for bankers and the surrounding environs. This is the second newsletter in a series I’m doing about master accounts; the first is available here. This newsletter extensively discusses the Federal Reserve Board and the Federal Reserve Banks. When I am discussing those institutions, I will capitalize those terms respectively, even if it pains my AP Style-trained journalist soul. Was this email forwarded to you? Sponsored by Linker Finance An account opened is not actually a deposit. And it’s definitely not a relationship to count on. The Master of the Master AccountLast week, we looked at the brief and recent history of the Federal Reserve master account. Today we’re going to talk about who controls these accounts and why that matters. The answer, via 12 U.S. Code § 342, is that Federal Reserve Banks have the authority to open, or not, a master account to the Federal Reserve Banks (with the exception of a master account to a foreign person — we will not be getting into that; this is already complicated enough). “The Federal Reserve Board cannot direct the Federal Reserve Banks to do anything,” said Roman Goldstein, senior director at Klaros and the former lead innovation policy analyst at the Federal Reserve Board. “If the Banks wanted to get together and say ‘We're keeping out non-banks from the payment system,’ they could do that. That's why the Board didn't write master account rules; it wrote master account guidelines.” Wow, that was easy! That’s all for today. Just kidding! Roman is right. The Federal Reserve Banks have the authority to approve master account applications. But there have been a number of parties that seem to be exerting influence and weighing in on this access, which begs the question: Who really controls who decides who gets these accounts? “In theory, the applications go to the individual Reserve Banks, and the individual Reserve Banks decide whether you get an account or not,” Julie Hill, the dean and Wyoming Excellence Chair at the University of Wyoming’s College of Law, told me. “But it just cannot be that the Board has nothing to say about it... because the payment systems are unified systems.” The Skinny Master AccountIn October 2025, Federal Reserve Governor Christopher Waller gave a speech where he welcomed “a new era for the Federal Reserve in payments” and proposed a “payment account” that would be tailored for firms that don't need the full master account toolkit. This “skinny” master account wouldn’t pay interest on balances, wouldn’t include daylight overdraft privileges or discount window access and would feature balance caps to limit risk. “There are many eligible firms engaged in substantial payments activities that may not want or need all the bells and whistles of a master account, or access to the full suite of Federal Reserve financial services, to successfully innovate and provide services to their customers," he said. At the end of 2025, the Federal Reserve Board of Governors issued a request for information on a payment account that would be for “the express purpose of clearing and settling the institution's payment activity.” It would be open to institutions that are already eligible for Federal Reserve accounts, which would need to request them from the Reserve Banks. The comment period closed at the beginning of February. Crypto Cracks the Master Account Access WallA month later, there seemed to be an exciting and unprecedented development in the fintech quest to obtain direct access to the payment rails. In March, the Federal Reserve Bank of Kansas City announced it had approved Kraken Financial, a Wyoming-chartered special purpose depository institution, for a limited purpose account for a term of one year. Kraken Financial is a subsidiary of cryptocurrency exchange Kraken. Kraken is a Tier 3 entity in the Fed’s framework, and its account “includes restrictions and limitations tailored [to its] business model and risk profile that are appropriate to mitigate risks.” The Fed did not disclose Kraken’s access to the range of Fed financial services. In its release, Kraken said it would integrate “Federal Reserve connectivity directly into the platform’s settlement and payments layer” and that it could connect to core payment rails like Fedwire. The Wall Street Journal reported that Kraken’s account would not receive the “payment of interest on reserves held at the central bank.” The timing of this announcement was a surprise for many, given it had only been a month since the Fed’s comment period on payments accounts closed. For now, it seems that Kraken slipped its application right as the window opened and right before it closed. Lucky for them! In the database, Kraken appears on the “existing access” page with an account access date that is more than a month before this information was known publicly. This database lists “financial institutions that have access to Reserve Bank financial services:” they either have their own Reserve Bank master account or access Reserve Bank financial services by settling transactions in the master account of another depository institution, according to the Fed.  Fed's master account database Kraken and the Kansas City Fed did not respond to multiple requests for comment on this account. Kraken also appears to still use Dart Bank for domestic FedWires. But Wait! Politicians have Some Thoughts TooAfter the Board began gathering comments on the payments account, lawmakers and politicians also chimed in. Congress has already once dictated who could have a master account in the Monetary Control Act in 1980. Could they do it again? In April, Representatives Young Kim, R-Calif., and Sam Liccardo, D-Calif., sponsored the PACE Act that would create a bespoke federal payments charter. The specialized charter means payments companies could work with a federal regulator without having to receive a national bank charter or obtain money transmitter licenses in 50 states. But Capitol Account reported that at a recent hearing, lawmakers seemed lukewarm to the idea, and the bill has yet to pick up additional sponsors. The next month, the White House entered the fray with Executive Order 14405, “Integrating Financial Technology Innovation into Regulatory Frameworks.” The order declared the policy of the United States to “streamline regulatory processes, reduce unnecessary barriers to entry, and encourage collaboration between fintech firms, federally regulated financial institutions, and Federal financial regulators.” The executive order had directives for the federal financial regulators but included some requests for the Federal Reserve Board as well. It requested the Board submit a report within 120 days that assessed the legal authority of the Federal Reserve to extend direct access to payment accounts and services to uninsured depository institutions and non-bank financial companies, options for expanding such access and the legal impediments to access and legislative or regulatory options to remove them. The report also seeks an articulation of whether individual Federal Reserve Banks have legal authority to act independently of the Federal Reserve Board in granting or denying access and what Board-level policies exist to ensure consistent evaluation across all 12 districts. “The devolution of power between the Board and the Reserve Banks is genuinely not well understood,” said Jasper Sneff Nanni, managing principal at FS Vector. “The question here is: How are these decisions actually made? Do the Reserve Banks decide on their own? Are they coordinating closely with the Board? Does it vary by case?” The Fed’s FingerprintsOne example that illustrates the Fed’s influence in Reserve Bank decisions is TNB, the narrow bank. TNB applied for a master account at the Federal Reserve Bank of New York in 2017. Recall that TNB’s “novel business model” boiled down to “take large institutional deposits, put them at the Fed, take a cut of the interest the Fed paid and pass the rest along.” It’s not the most interesting use of money I’ve ever heard of, but attorneys at the New York Fed were concerned that the bank would take only uninsured deposits and have no federal regulator, Julie wrote in her 2023 paper. So they asked the Board for its insight. Of course, applications that are submitted to the Reserve Banks can and do go to the Board. The Fed has delegated authority to approve bank merger applications “that do not raise any significant anticompetitive concerns” to the Reserve Banks, according to a 2014 letter from the Federal Reserve Bank of Chicago. But Roman said nothing like that exists for master account applications. When TNB’s application was brought to the Board, the Board became concerned that TNB’s business model “could complicate the implementation of monetary policy, disrupt financial intermediation, and negatively impact our nation’s financial stability,” according to Julie’s paper. Not TNB's operational soundness, not risk to the payment system and not a concentration of uninsured deposits. It’s possible the Fed was right to be worried; maybe a TNB master account means the central bank would have trouble controlling monetary policy (imagine having a business model so powerful you interrupt monetary policy). The Fed proposed lowering the rate of interest paid on excess balances maintained at Federal Reserve Banks by eligible institutions that hold a very large proportion of their assets in the form of balances at Reserve Banks in 2019, undermining TNB’s business model. But this example made me wonder how much credence any individual Reserve Bank should assign to the Board’s concern versus the application’s merits. Does the Board’s opinion serve as a de facto vote on these applications? Does it serve as a veto?! For TNB, apparently it did. “[T]he New York Fed’s general counsel wrote that the New York Fed was not prepared to issue the account because ‘senior policy officials at the Board . . . have expressed the strong view that the New York Fed should not approve TNB’s request,’” Julie wrote. The (In)visible Hand of InfluenceIn what could be entirely coincidental timing, the Federal Reserve Board had an announcement of its own the day after the White House’s executive order: the next step in the payments account proposal. The Board also made a request of its own: It asked that the Reserve Banks to “temporarily pause decisions on access requests from institutions that fall within Tier 3 of the Board's Account Access Guidelines until the Board has completed its policy development process on the payment account proposal.” The temporary pause request makes the invisible hand visible. The Reserve Banks are the only institutions that get to decide who gets a master account and the master account guidance and framework have been out for four years now. Why is this pause needed, even if the Fed is thinking about creating a new account structure? Can’t it be a “both/and” and not an “either/or”?  It’s giving “I...worked on this story for a year...and...he just...he tweeted it out.”  It’s giving “I...worked on this story for a year...and...he just...he tweeted it out.” More broadly, I won’t lie: I am dying for the information the White House has requested. So too, I’m sure, are the companies (some of which do not exist anymore) that have sued various Reserve Banks, and at times, the Board, to get it. But this feels like a big ask from an organization that has denied its influence when it comes to master account access — while exercising it — for almost a decade. You can see this practice in the lawsuits over these accounts that Julie documented in her paper. When Fourth Corner Credit Union sued the Kansas City Fed in 2017 and TNB sued the New York Fed in 2018, the Board filed amici briefs. When Custodia sued the Board in 2022, the Board’s argument to the court was that it doesn’t decide to open these accounts. “[T]he Board downplays its large and sometimes pivotal role in account requests. Instead, it shifts responsibility for decisions to the Reserve Banks, who it claims are not bound by laws that might constrain the Board,” Julie wrote in 2023. How much has changed since then? The Board’s influence in master accounts has been a wily thing. It exists when it’s convenient: the graveyard of failed access requests, the lawsuits deemed not ripe. And yet, the Board seems almost miffed when a Reserve Bank goes against it: why make the temporary pause request four years after putting out the framework that was intended to help the Reserve Banks with these decisions? But mostly, so far, it’s been hard to pin down for accountability purposes. FROM THE VAULT What’s on my mind and filling my time: ⚽️ Catch me if you can: Reuters looked at the fitness expectations and demands of the referees in the men’s World Cup, tracking total distance and sharing the outlines of the fitness test. I ran a modified version of the intervals test this weekend as part of heat training and can confirm it’s tough. 📫 You've got mail!: One of my resolutions is to write more cards, letters and postcards. One happy consequence of this is occasionally getting to buy more stamps, and the Postal Service has some bangers out: Barbie stamps, dragons (D&D but who is looking closely), Jeopardy and Betty White. Buy some and send some cards! 🎙️ On Bank Nerd Corner: I break down the two recent Supreme Court decisions that promise to reshape the administrative state and financial regulation with Mike Silver, a partner at Spencer Fane. 🎧 *Bonus Podcast Rec: Agent of Record, with Parlay Finance and me. I’m an AI novice (and a little skeptical); Parlay Finance CEO Alex McLeod is an AI expert. Together, we’re creating a podcast series that breaks down what’s real when it comes to artificial intelligence in banking, in conversation with actual practitioners and bankers. If you’re a financial institution exploring AI (and be honest, who isn’t), you won’t want to miss out on Agent of Record. First episode is live! *This rec is brought to you by one of our fantastic brand partners. Thanks for reading and going deep into master accounts with me! Hope you're not sick of it yet. 😏 - Kiah | |||||||||||

|