| ||||||||

| ||||||||

Happy Tuesday, Hospitalogists! Today I’m sharing news and trends over the month of April (okay with some stuff from the end of March and beginning of May…sue me). Of course my personal favorite was letting you guys know last week about the Hospitalogy AI Retreat taking place in November out in Phoenix. 3 days, application-based. Flights, hotel, and ticket costs covered. I’m blown away by the applicant list so far. Senior leaders from Endeavor, Saint Francis, UF Health, Ascension, Baylor Scott + White, UT Health, and more are in the mix. Man, you guys are the best and I can’t wait to 100 seats. If you're on the fence about applying, go read more here. Hope to see you there! Let’s dive in. Was this email forwarded to you? Hospitalogy stuff last month:Apply to the Hospitalogy AI Retreat here! Podcasts last month: Watch these on Youtube here! Like and subscribe to my new channel! (can’t believe I’m saying that…smh)

re: Podcasts - I would love y’all’s support! Drop a review on Apple or Spotify if you have the time to do so. Any support or share really helps me out. Also, if you guys have any feedback or suggestions for me, please feel free to reply to me. Newsletters this month:

Virtual and Community Events

April 2026 — Consolidated Themes & TrendsWhoop is coming for traditional healthcare…along with the rest of ACCESSCMS accepted 150+ organizations to ACCESS and extended the application window to May 15, but plenty of folks walked away after seeing the reimbursement rates for participants. Sword Health and Omada, two scaled tech-enabled players, passed. CMS also quietly noted most accepted participants have never served Medicare before…like Whoop, which now seems to have a professional services entity in healthcare. I can see the wearables play pretty easily - if the bet works economically, awesome. But if not, you’re still getting your devices and services in front of a new customer segment, and having the government foot some if not all of that bill. Overall if ACCESS works, CMS’ deflationary bet is validated and the VC-backed digital health cohort got outflanked by companies they didn't see coming, all the while health systems will need to deal with the Cadence’s of the world. If it fails, CMMI just lit up a very public test with the wrong participants. Relevant articles:

Bundled payments are ramping, mandatory, and nationwideIn the IPPS proposed rule, along with a 2.4% pay bump, CMS has proposed to expand its Comprehensive Care for Joint Replacement (CJR) into CJR-X, which is the first-ever mandatory, nationwide, episode-based payment model in US history and include HOPDs. October 1, 2027 start. 3,000+ IPPS hospitals in scope. 90-day episodes. 29 risk adjusters versus the original CJR's 3. As mentioned HOPD triggers are now included, closing the site-of-service differential.

Combined with LEAD coming and TEAM already in flight along with the Ambulatory Specialty Model finalized last October, CMS has assembled the most aggressive value-based payment stack since the ACO era began. Health systems that built CJR and BPCI infrastructure are about to have a moat; the rest need to catch up ASAP. Relevant articles:

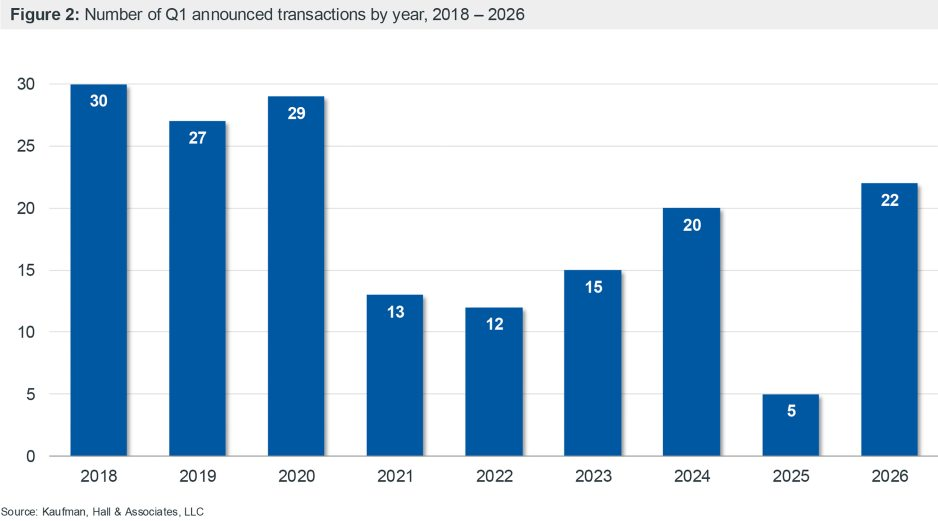

Hospital M&A bounceback, but with a caveat: divestitures and portfolio realignment remain dominant themes Kaufman Hall's Q1 count of 22 deals and $14.5B transacted revenue was both a 6-year Q1 high and 68% divestiture-driven. Only 18% involved a distressed seller, versus 43.5% across all of 2025. For-profit systems are sellers 11x more often than buyers. Large nonprofits (Sutter/Allina as the marquee at $26B and 39 hospitals) are doing cross-market mega-mergers where scale alone isn't the thesis — capability and geography are. Ascension's non-acute AmSurg play, Corewell's Quest lab JV, UHS-Talkspace → health systems are looking for opportunistic partnerships and acquisitions on the outpatient side, or to enhance their existing portfolio. As of this writing the only M&A play to buck this trend involves Atrium’s play for WakeMed in what has already created quite the stir in that market. Relevant articles:

Private Equity is back, babyHealthcare displaced tech as the #1 direct lending sector in Q1 (22% of YTD issuance, up from 18% in 2025; tech slipped to 14%). Several healthcare PE funds closed while certain firms upped their take-private game. For instance, Blue Owl took a healthcare REIT (Sila Realty) private for $2.4B. American Industrial Partners took Avanos private at a 72% premium. Earlier in Q1, WCAS took Select Medical private at a 25% premium, or $3.9B. This month, McKesson also sold 13% of MMS to Apollo for $1.25B at a $13B implied valuation, ahead of a planned IPO. KKR-backed GMR Solutions (Global Medical Response - emergency med provider) filed to go public seeking a valuation up to $5B as the firm looks to exit to the public markets. Finally, Carlyle's roll-up of Knack RCM and EqualizeRCM into an "AI-native, global, multi-specialty" is a signal where PE wants to play on the tech forward side of things, and we’ll see more activity here - building category leaders designed around AI-native operating models. Dabbling in VBC given opportunities in LEAD. Healthcare PE is back, baby. Relevant articles:

DC is moving on every front at once, in unusual directionsA few different, discombobulated things of note from Capitol Hill:

Whatever you think of the substantive direction, the pace of regulatory activity coming out of Washington right now is somewhat insane (sorry for all you policy wonks tracking all this), and the investment side holds significant alpha for those who can keep up and take advantage (except for you, Medvi) - peptide consumer health, psychedelic biotech, hospice enrollment moratoriums, MA compliance intensity, MFN drug-pricing precedent, etc etc. Relevant articles:

Insurers and PSHPs Flee the ACAInsurers saw a rebound in Q1 public earnings announcements, broadly speaking, on the back of a muted flu season and an industry wide reset. The biggest secular shift was probably in the ACA between expired subsidies, expected shakeout, and market exits. UnitedHealth Group’s ACA membership set to decline by a third in 2026, Medicaid attrition running as expected, intentional contract exits.  Cigna also announced an ACA exit across 11 states (announced April 30 alongside a Q1 beat at $68.5B revenue). Centene dropped 2 million ACA lives in a single quarter while still raising guidance. Total enrollment dropped by about a million, but the final number is still unknown. Baylor Scott & White Health Plan quitting both Medicaid and ACA (225K members, 321 jobs) and Oregon placing ATRIO under receivership in the same week round out the picture for subscale regional plans that can't make the math work in the post-OBBBA environment. Relevant articles:

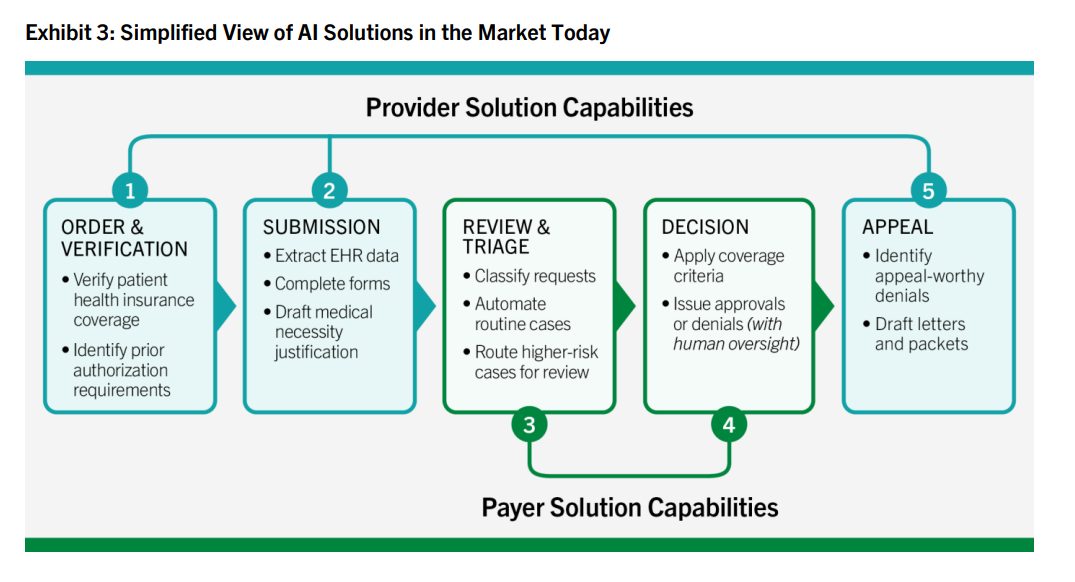

The Ambient Convergence Thesis ContinuesAny evidence of OpenEvidence’s apparent moat is shrinking as ambient players converge on the same use cases to present to physicians and enterprise customers - ambient, CDS, prior authorization, chart automation, inbox management, etc. Most everyone uses OpenEvidence for CDS…but does that edge maintain over time? Players like Abridge already have UpToDate embedded in its CDS system. Layering NEJM and JAMA's peer-reviewed content on top, then routing it context-aware into the ambient documentation workflow, directly encroaches on OpenEvidence's positioning as the trusted evidence engine. OpenAI for Clinicians is here. So is Claude, which just so also happens to be potentially raising…$50B.  Couple Doximity's positioning as another physician distribution channel operating in the same arena and noise increases in the space. Also worth noting: NEJM Group and JAMA inked content deals with OpenEvidence too, which, as I read them at the time, I thought were exclusive so…I suppose that ship has sailed. The copilot arms race continues Relevant articles: AI escalated from pilot to enterprise infrastructure, and the regulatory architecture is finally trying to catch upAidoc's $150M Series E led by Goldman Sachs Alternatives (with General Catalyst, SoftBank Vision Fund 2, and Nvidia’s NVentures piling on, $500M+ in total funding ahead of a stated 3–5 year IPO path) signals a material shift in health tech. This company, and the health IT space combined with private equity activity above, is now an institutional capital story. When Goldman's growth-equity arm leads a clinical AI round at that scale, capital is underwriting durable revenue with a specific thesis in mind for what the future healthcare system holds.  One friction-inducing data point worth mentioning is PHTI's report on AI-powered prior authorization. The report found that AI actually drives up healthcare costs when deployed by payors, because providers respond with their own AI to appeal denials, which I fondly have referred to as the AI Bot Wars. It’s an escalating arms race with no system-level cost benefit for now, until a unified objective platform comes along. Whether AI nets out to deflation or inflation at the system level remains to be seen, but I choose to be optimistic. Relevant articles:

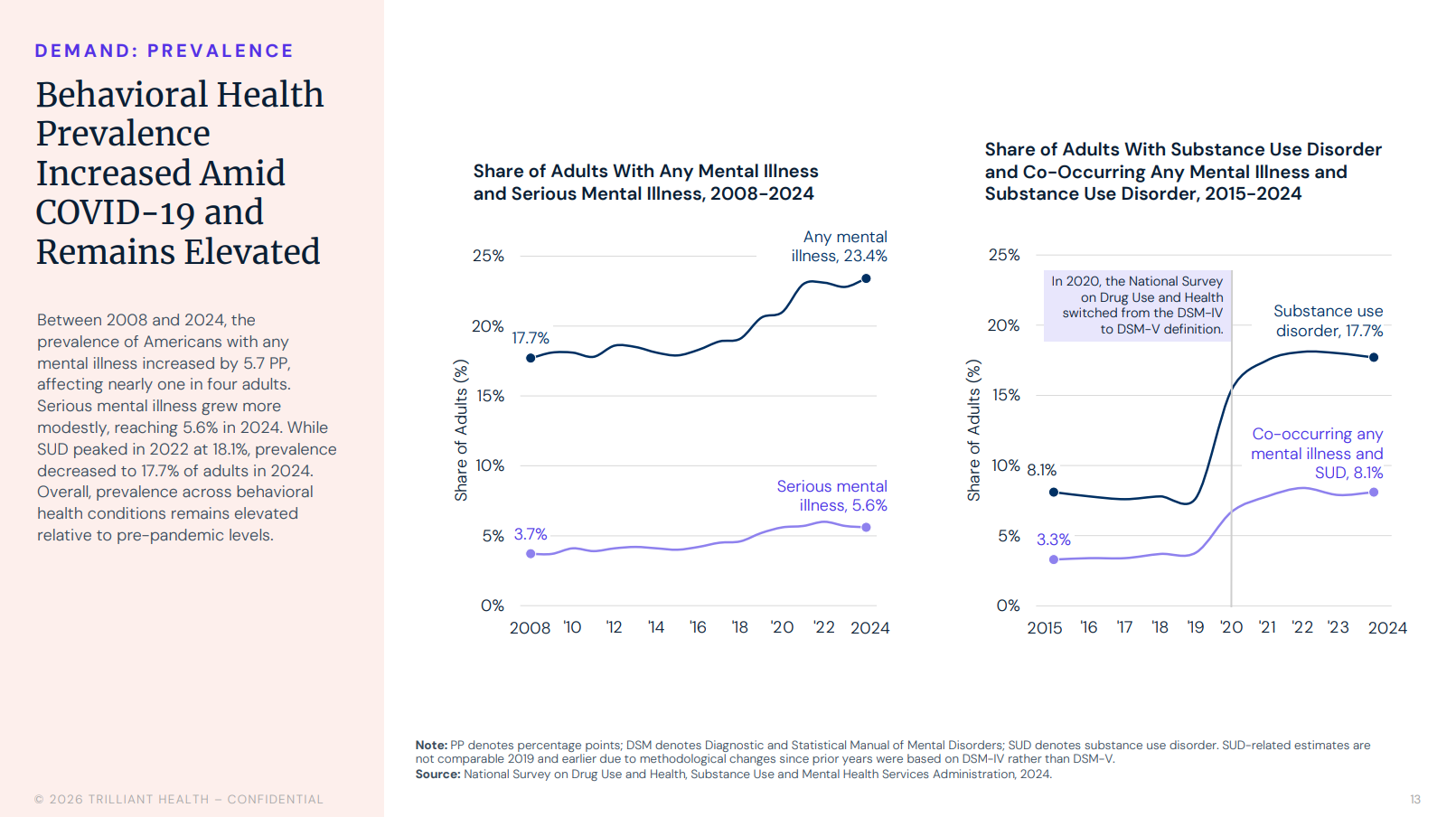

Behavioral health demand continues to skyrocket as capital and partnerships fly into the space Trilliant's 62.6% utilization growth since 2018, anxiety up 89.3%, telehealth carrying 65.6% of behavioral health visits in 2024 (vs 18.4% in 2018) — combined with Recover Now-Widespread Wellness, ARC Health-NC Mental Health, and Talkiatry-AMGA all hitting in the same 10-day window. Talkiatry now sits as the largest private employer of psychiatrists in the country (800+ FTEs), and AMGA's network gives it a distribution layer that gets reimbursed in-network across 100+ plans. BH M&A was up 17% YoY in 2025 and the table's set for another record year. Let’s also not forget about UHS-Talkspace, Baylor-Geode, and others I’m surely forgetting. Relevant articles: Cuban-Humana pharmacy partnership turns heads as PBM model dismantlesMark Cuban's Cost Plus and Humana's CenterWell Pharmacy went live April 27 with an end-to-end employer prescription play. Cost Plus's SwiftyRx (digital pharmacy SaaS platform) will become CenterWell's order-intake software, and CenterWell becomes one of Cost Plus's pharmacy partners. CenterWell brought in $22.5B of revenue in 2025, so the deal is significant, but also playing ball with healthcare royalty and incumbency. I have to wonder whether Cuban's been told off-mic that he can't actually break up Big Medicine without picking sides, and Humana's the side worth picking. Mark, if you’re reading this, would love the rationale. Either way, the PBM model as I’ve noted before is under significant threat. Relevant articles: Antitrust and political tightening - cost narrative shifts to hospitals in AprilAtrium’s bid for WakeMed ($2B Atrium capital commitment, 3,300 jobs, NC's largest virtual care network), is being reviewed by both the AG and FTC, with NC Treasurer Brad Briner publicly opposing it on cost-of-care grounds the same day and demanding either rejection or a $1.5B endowment, with the approval vote being delayed in the process. The FTC's new Healthcare Task Force, the DOJ West Coast Strike Force, and the House Ways and Means hearing this past week where HCA, CommonSpirit, NYP, and ECU were collectively compared to Disney for profitability… signal a coordinated tightening of the political and antitrust environment around health system consolidation, simultaneous with the largest nonprofit deal of the year. Relevant articles:

ON YOUR RADAR

*This resource is brought to you by one of my brand partners who help make this newsletter possible! MISCELLANEOUS MADDENINGS I managed to sneak in a round at Stevens Park in the heart of Dallas on Sunday afternoon and left feeling incredibly frustrated at the short game, shooting an 80 (10 over, par 70). Bottom line here is I just need to practice more. Every round this year, something is off, which leads to dumb inconsistencies. Sunday was the short game. Pecan Hollow a couple weeks ago was my inability to get off the tee box. Someday I’ll put together the complete game! Thanks for the read! Let me know what you thought by replying back to this email. — Blake | ||||||||

|