| ||||||||||

| ||||||||||

Happy Monday, Fintech Takers! And May the 4th be with you (and especially with Cordelia!) Lots to get to today, so let’s jump right in. - Alex P.S. — Every week, 95 million consumers in 6,500+ stores across the country walk past a largely untapped marketing channel. For some reason (probably because folks are already in “wallets out” mode), fintech companies are seeing 49% more reach when they add in-store ads to their marketing strategy. I'm joining Daniel Murray of The Marketing Millennials next week in a virtual event to explore why this channel is landing for fintech companies, and how to build a repeatable acquisition playbook around it. If your marketing teams are looking for new channels, please send them our way! Was this email forwarded to you? Sponsored by Fundbox B2B platforms that want to offer SMBs capital have two options. The second: find infrastructure that keeps up. Fundbox's embedded capital infrastructure gives B2B platforms full-stack, white-label, embedded credit products, with underwriting, compliance, and capital all handled. For platforms debating their two options, Fundbox has made the math pretty simple.  Toll Gate by Henri Rousseau. 3 FINTECH NEWS STORIES #1: Please Let This Be The EndWhat happened?The U.S. Senate may finally be in a position to pass the Clarity Act, based on some newly proposed language on the issue of yield-bearing payment stablecoins:

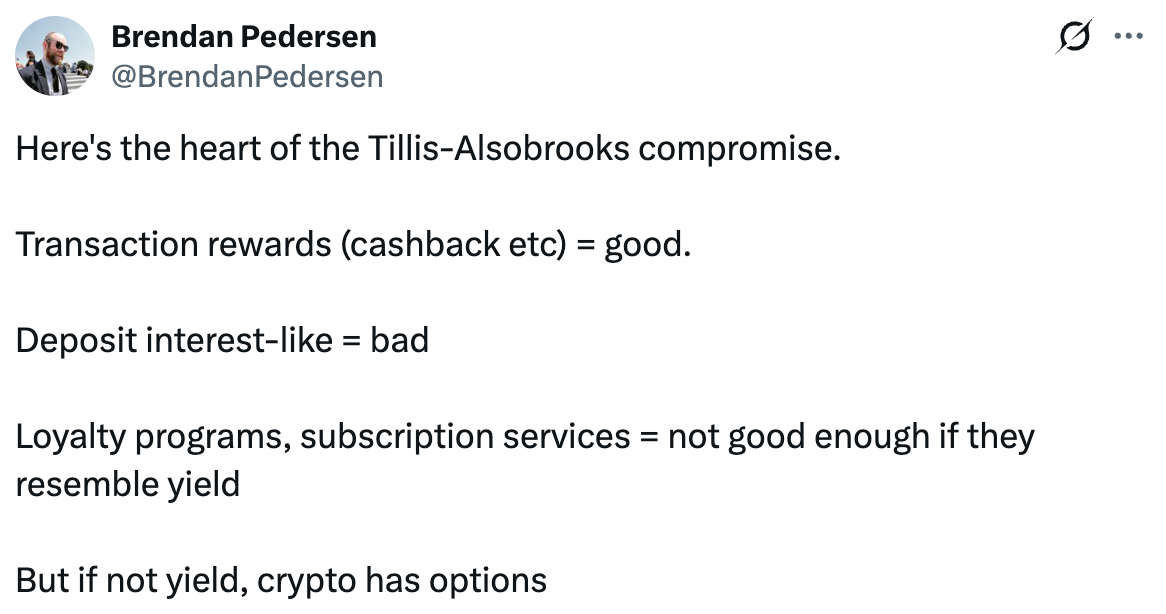

So what?I’m so tired and I just want this to be over. The endless wrangling over an issue that probably doesn’t matter that much in the grand scheme of things has become unbearable. I mean, just look at that legal language! No interest or yield in connection with holding a stablecoin … but if it’s based on activities or transactions, then it’s OK … except if those activities are tied to loyalty programs or subscriptions that function like yield on deposits. Brendan Pedersen, the reporter who broke the news of this new compromise, does his best to summarize it here:  This is confusing! What does “resemble yield” mean? What options does crypto have, exactly? Would, for example, a subscription service that rebates fees only to users with an average daily balance greater than $X be considered a loyalty program or a "yield-equivalent" on a deposit account? I don’t know. No one knows. If the Clarity Act is passed with this compromise included, this question (and many many others) would need to be answered by federal regulators, who would be responsible for writing the implementing regulations. However, such regulations would be immediately challenged in court, given the vagueness of the bill's language and the diminished deference courts now show to regulators.. But will it pass? Coinbase is apparently onboard:

This full-throated support, coming on the heels of Coinbase’s persistent intransigence on this issue, is likely to give the banking lobby pause. However, at this point, it may be too difficult for them to stop. This seems like a compromise that is specifically designed to drive a wedge between community banks (which are freaked out by the specific threat of deposit displacement) and the big national banks (which seem more concerned about allowing any new forms of competition into the market). And that brings me to a question that I hadn’t thought to ask until just now: Where is the Electronic Payments Coalition on this issue? The EPC is a trade association representing Visa, Mastercard, and the big credit card issuers. It exists, primarily, to oppose any legislative or regulatory threat to the credit card market, such as the Credit Card Competition Act. If yield-bearing payment stablecoins were the all-encompassing threat that the banks have claimed that they are, why hasn’t this latest compromise — restricting stablecoin yield on the holding of funds but allowing stablecoin rewards on payments activity — triggered an angry response from the EPC? I mean, the compromise explicitly allows for cashback on stablecoin transactions! Isn’t that a massive threat to credit card issuers?!? Apparently not. My guess as to why the EPC isn’t interested in this issue is that credit card issuers are confident in the value their product provides. They know that consumers LOVE credit card rewards and they know that the revenue that pays for those rewards (annual fees, late fees, interest from revolvers, and interchange fees reluctantly paid by merchants) is stable and sufficiently diversified. They rightly believe that stablecoins are not a threat to their business (and may actually be a boost). Objections to yield-bearing payment stablecoins tell you a lot about the confidence that the companies lodging the objections have in the value of their own products. #2: OpenAI is Ushered Inside the Banking PerimeterWhat happened?Customers Bank revealed, in dramatic fashion, a new partnership with OpenAI:

So what?I’m not shocked that Customers was the one to take this step. It has always been willing to take innovation-flavored risks. Customers was one of the earliest and most aggressive banks to move into crypto. It operates a deposits and tokenized-payments franchise for 100+ digital-asset firms (Coinbase, Circle, Paxos, etc.), which has been a significant source of growth and profitability for the bank (as well as a source of compliance trouble … the bank got hit with an enforcement action from the Fed in 2024 over AML and sanctions deficiencies tied to its digital-asset business). This most recent earnings call, on which the AI clone was used, was actually the very first earnings call that Sam Sidhu had done since taking over the Customers Bancorp CEO role from his father Jay at the beginning of this year. That is one hell of a way to introduce yourself to investors, and it leaves me with a few questions:

#3:How Much Risk Will Erebor End Up Taking?What happened?Erebor Bank filed its first call report, seven weeks after opening its unadorned virtual doors, reporting nearly $1.1 billion in deposits:  So what?This news has been celebrated on fintech VC twitter as unprecedented growth for a de novo bank or fintech neobank. I won’t comment on the veracity of that claim, although it does seem entirely possible. A billion dollars in seven weeks is FAST. What I will say is that, in banking, the rapid accumulation of deposits is universally seen as a risky thing by regulators because it is highly correlated with bank failures. This phenomenon has been studied extensively by the FDIC. Acquiring lots of deposits quickly usually comes with a cost, either monetary (i.e., paying higher rates) or risk (i.e., taking on higher-risk customers who other banks don’t want) or both. And if banks are willing to absorb those costs, it’s usually because they have a plan to deploy that liquidity to generate above-market returns, which also often entails a lot of risk. The combination of risky loans + expensive, non-sticky deposits frequently results in bank failures. Now, if you wanted to defend Erebor, you could point out that unlike the most prominent bank failure in recent history (Silicon Valley Bank), most of Erebor’s deposits are insured. While roughly 90% of SVB’s deposits were uninsured before the bank failed, Erebor reports that only 23% of its deposits are uninsured. This difference matters. Insured depositors are much less likely to run, assuming that they know they are insured. However, if we’re going to use SVB as our counter-example for Erebor (and I think it makes sense to do so given that they are going after roughly the same customer base), then we should also talk about the composition of Erebor’s deposits versus SVB’s deposits. Prior to its failure, SVB's deposit base was 46% non-interest-bearing demand deposit accounts. These were operating accounts for startups and startup founders that cost the bank nothing. Erebor's deposit mix is 12% non-interest-bearing and 88% interest-bearing, which means Erebor's cost of funds is significantly higher than SVB’s was. And what is Erebor doing with all of these expensive interest-bearing deposits? Nothing, yet. The call report shows zero loans on the bank's balance sheet, zero loan commitments outstanding, and 83% of total assets sitting at the Federal Reserve earning IOER. As currently structured, Erebor is functionally a money market fund with FDIC insurance. It earns a thin spread between Fed reserves and what it pays its depositors, and right now that spread is essentially zero. The bank reported a $6 million net loss in its first 52 days, and salaries alone ($5.6M) exceeded total revenue ($4.6M). The bigger issue, though, is what the lending side will look like once it spins up. Palmer Luckey has said publicly that Erebor will run "the most conservative loan-to-deposit ratios of any bank in history," with early indications targeting around 50%, meaning the bank intends to lend out only half of every deposit dollar it takes in. At the same time, Erebor's stated mission is to serve early-stage startups, defense companies, and crypto-adjacent operators that other banks won't touch (i.e., higher-risk borrowers, often with non-standard collateral). This is, ironically, very similar to SVB, which had an even lower loan-to-deposit ratio when it failed in 2023 than what Erebor is aiming for in 2026. That didn't mean SVB wasn't taking risks with the money it wasn't loaning out. As we know, it was, and that's what ended up sinking it. Erebor seems to be betting that it can avoid the same fate by keeping its ratio of insured-to-uninsured deposits high, keeping its loan-to-deposit ratio low, and not doing anything stupid with the money that it has left over. It’s a sound idea, conceptually. However, in practice, there’s a reason why regulators worry about banks with this profile. The temptation to eventually do something stupid with the money is very very strong. Sponsored by MX In this Data Takes spotlight, MX digs into the distance between what consumers report and what their spending shows. 62% identify as living paycheck to paycheck. 2 READING RECOMMENDATIONS #1: Partner Banking is: a) Back b) Broken c) Obsolete d) All of the above (by Jason Henrichs, Fintech Business Weekly) 📚 I really enjoyed Mr. Henrichs’ guest essay in Mr. Mikula’s newsletter yesterday. BaaS is in a fascinating state of flux right now. #2: The Coming FinTech Liquidity Supercycle (FT Partners & Blue Dot Investors) 📚 Some interesting stats in this report from FT Partners and Blue Dot Investors. *Bonus: Fast Rails, Frozen Books: What Banks Are Missing in the Era of Faster Everything (with Rouzbeh Rotabi at Qolo and Kiah Haslett of Fintech Takes Banking) 💻 Instant payments. Real-time subaccount posting. Stablecoin settlement. Your commercial clients can get all of that somewhere ... the question is whether it's from you. Rouzbeh and Kiah dig into why banks are losing ground on treasury management and what fixing it requires. May 20th @ 12 pm ET (virtual); register here. *This rec is brought to you by one of our fantastic brand partners. 1 QUESTION FROM THE FINTECH TAKES NETWORK There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network. I’m interested in digging into the history of auto-pay. Do you know of any good resources (articles, books, people to interview, etc.) on this topic? If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network! Thanks for the read! Let me know what you thought by replying back to this email. — Alex | ||||||||||

|