{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Friday, Fintech Takers!

Well, it’s been a busy week.

My thanks to the wonderful folks at the Bank of North Dakota for their hospitality. I had a fantastic time at the Banking Beyond Boundaries event. It’s pretty cool to see some of the smallest rural banks in the country so focused on innovating for their communities.

Also, Fargo is a lovely (albeit cold) city! - Alex |

Was this email forwarded to you? |

|

|

My favorite part of this week’s trip to Fargo was the time I spent with some students from North Dakota State University.

Not only were they very gracious when I wore my Montana State University t-shirt (Go Bobcats!), but they were also a wonderful, very engaged audience for my presentation — Fintech is Never Finished.

I learned a lot from giving the presentation (as always, the best way to learn is to present and defend your ideas), and I hope the students learned something as well.

So, I thought for today’s newsletter, I’d share an annotated version of the presentation. I hope you enjoy it! |

I think the most essential thing for anyone building in financial services to understand is that there aren’t any new ideas.

This industry has, for thousands of years, attracted the smartest, greediest, and most morally flexible people in the world. If you think you’ve come up with a novel idea for how to store, move, lend, or invest money, it’s very likely that you just haven’t studied the history of financial services closely enough. That’s not to say that your idea might not lead to the creation of a successful product or business. It might! Because success in financial services isn’t about having the best idea.

It’s about having the right idea at the right time. |

Take Circle as an example.

After a failed SPAC in 2022, the company successfully went public in June 2025. After pricing its offering at $31 a share, Circle opened at $69 and closed its first day at $83.23. By the end of the month, the stock had climbed to a record $263.45.

Why did that happen? Are stablecoins a novel idea? Not really.

In the U.S., you can trace the roots of stablecoins back to the era of free banking in the early 1800s, followed by the creation of eurodollar accounts after World War II, the development of money market funds in the 1970s, and, of course, Facebook’s ill-fated Libra/Diem initiative in the late 2010s. Circle didn’t succeed because it came up with a brand new idea. It succeeded because it had good timing.

But what determines good timing? |

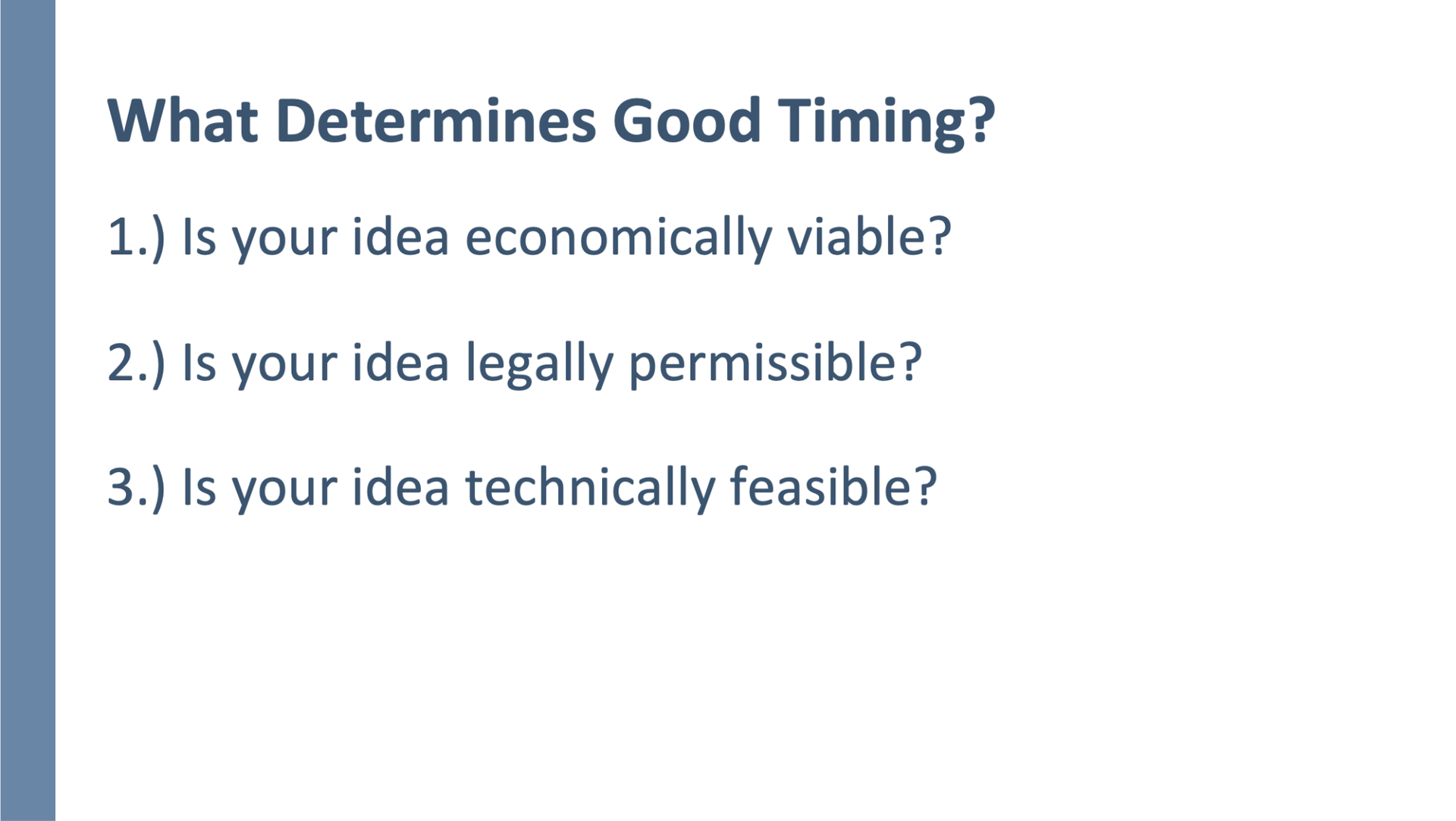

We can distill good timing down to three questions:

1.) Is your idea economically viable?

When the primary component in your product is money, the macroeconomic environment matters quite a bit. A lot of ideas in financial services look really smart when economic conditions are good, and credit performance is strong. When the cycle turns (which it always does!), those same ideas can look really dumb! Long-time fintech VC investors often shy away from investing in lending businesses, for the simple reason that it’s very difficult to predict how macroeconomic factors will impact critical stages in a lending business’s lifecycle. 2.) Is your idea legally permissible?

In financial services, the refs always win. Unlike other industries, you can’t ignore or bully regulators like the Federal Reserve, the OCC, or the SEC and expect to survive for very long.

What they say goes. However, as we are seeing right now, what they say … can change.

When political conditions shift, regulators and regulations can shift too. Sometimes these shifts are temporary, creating regulatory arbitrage opportunities for companies operating on short timeframes to exploit (my guess is that the CFTC’s tolerance of sports betting in prediction markets is going to wind up being an example of this). Other times, these shifts are permanent, creating a more durable opportunity for new products and business models.

3.) Is your idea technically feasible?

A lot of the best ideas for new financial products just aren’t technically feasible when they are first dreamed up.

Max Levchin talked about this on the Fintech Takes podcast last year, in regard to PayPal’s very early experiments with mobile wallets and device-to-device payments. It turned out that not enough people owned Palm Pilots in the late 1990s!

Today, of course, mobile wallets and device-to-device payments are commonplace. |

Circle is a smart, well-run company that has made a lot of good choices over the course of its existence. However, I’d argue that Circle’s success to date is primarily a function of good timing and that good timing was mostly a combination of economic viability (high interest rates = more revenue from holding short-term treasuries) and legal permissibility (the GENIUS Act was signed into law shortly after the company’s IPO).

Now, to be clear, there’s nothing wrong with this path to success. It’s just really difficult to predict! Circle could have made the same choices and executed just as well, and it could have very easily failed if interest rates had stayed low after the pandemic and the political winds hadn’t shifted decisively in the crypto industry’s favor. By contrast, good timing due to technological feasibility is inherently more predictable. Why is that? It’s because technological improvement isn’t cyclical. It’s exponential.

Exponential growth isn’t easy to predict, but it is easier to predict because it only goes in one direction.

|

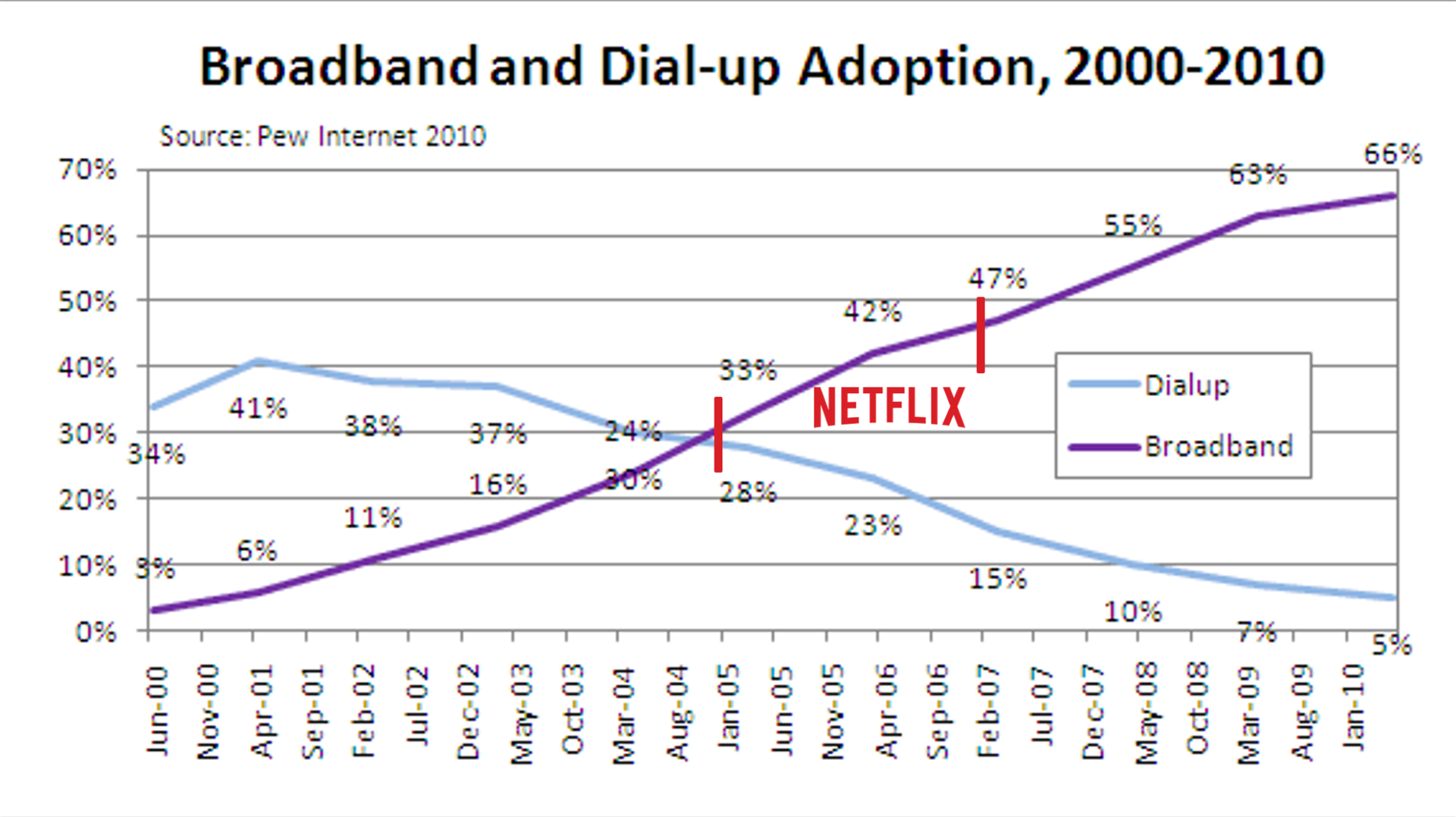

Netflix is a good example.

To their immense credit, the NDSU students were aware that Netflix used to be a mail-order DVD business, rather than a media streaming business. What most folks don’t know is that Netflix’s transition from DVDs to streaming wasn’t random or based on the intuition of its founders. It was a highly analytical decision, based on the growing adoption of broadband internet in the U.S. and the displacement of dial-up internet, which any 90s kid can tell you was utterly insufficient for any form of video streaming. Look at the chart above! Netflix engineers started working on the company’s streaming service in 2005, right around the time that broadband overtook dial-up. And it launched streaming in 2007, when broadband had reached roughly half of U.S. households. Netflix saw where the puck was going, and it skated, very precisely, to that spot. |

So, the question I put to the NDSU students was this: What are some unsolved (or badly solved) problems in financial services that technology might now enable us to address? |

It felt unfair to ask the students to answer that question on the spot.

So, instead, I flipped the script, and I spent the remainder of the presentation pitching them some ideas for new fintech products and services, and having them pepper me with questions about the ideas, as if they were VC investors evaluating my startup pitches.

Below, you’ll find six of the ideas from my presentation. I offer them to you for free, recognizing that ideas, in this industry, are plentiful. I’ll leave it to you to determine if the timing for them is right. |

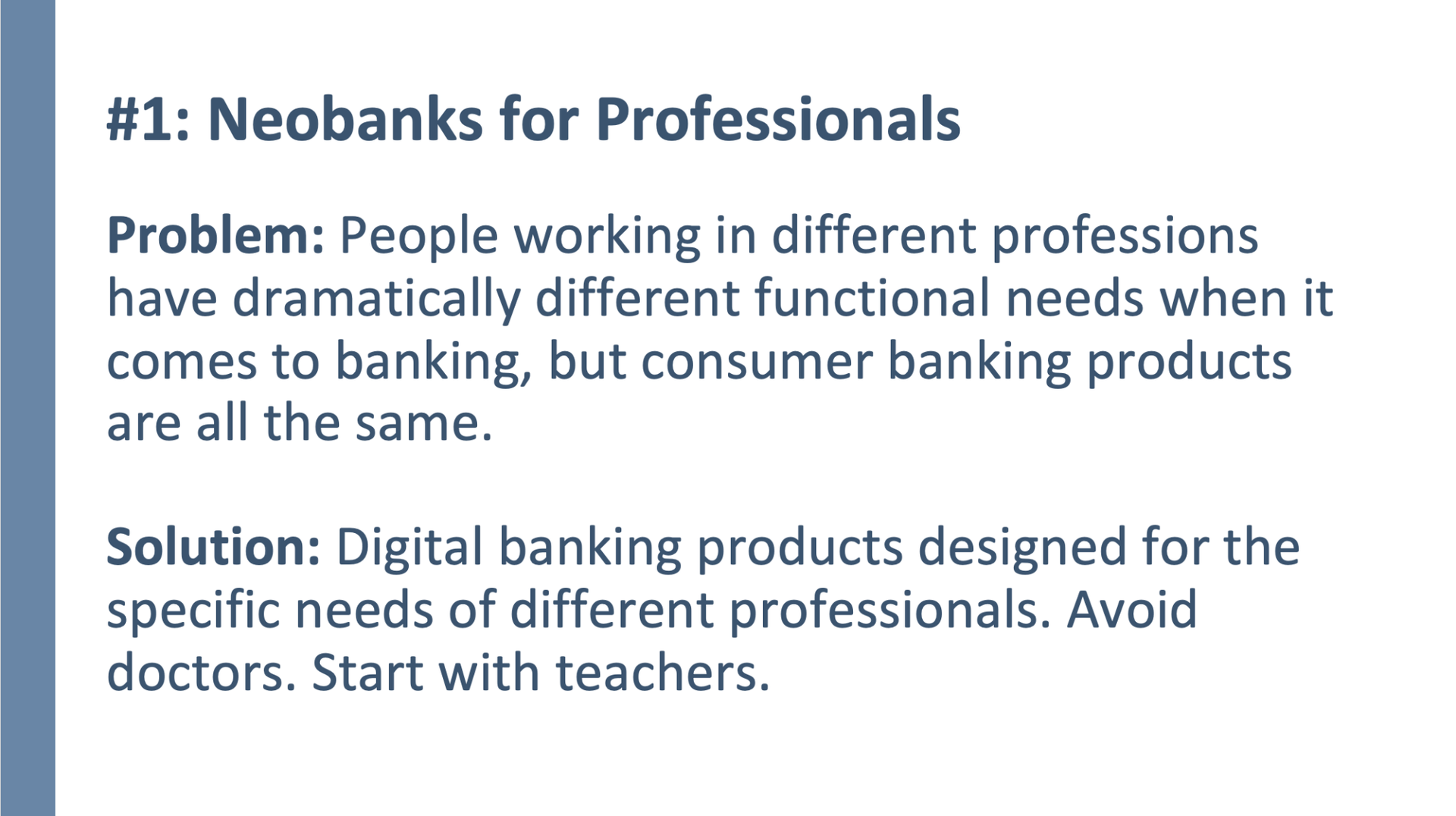

I find it odd that we build SaaS operating systems for companies in different verticals, but we don’t build specialized operating accounts for the professionals working in those verticals.

Workers in different professions have different functional needs when it comes to financial services. While credit unions have long specialized in serving specific professions (and even professionals working for specific companies), that specialization rarely translates into differentiated products.

Teachers are my favorite example. Teachers need a bank account that has built-in budgeting and income smoothing (because they get paid in a lump sum upfront for the summer months), retirement planning and investing (because pensions are increasingly underfunded), corporate cards and expense management (because they often pay out of their own pockets for district expenses), access to private student loans (because teachers require post-graduate degrees to move up the salary schedule), and discounts and rewards tied to purchases from local businesses (because those businesses often want to give back to teachers in their communities), among many other things.

|

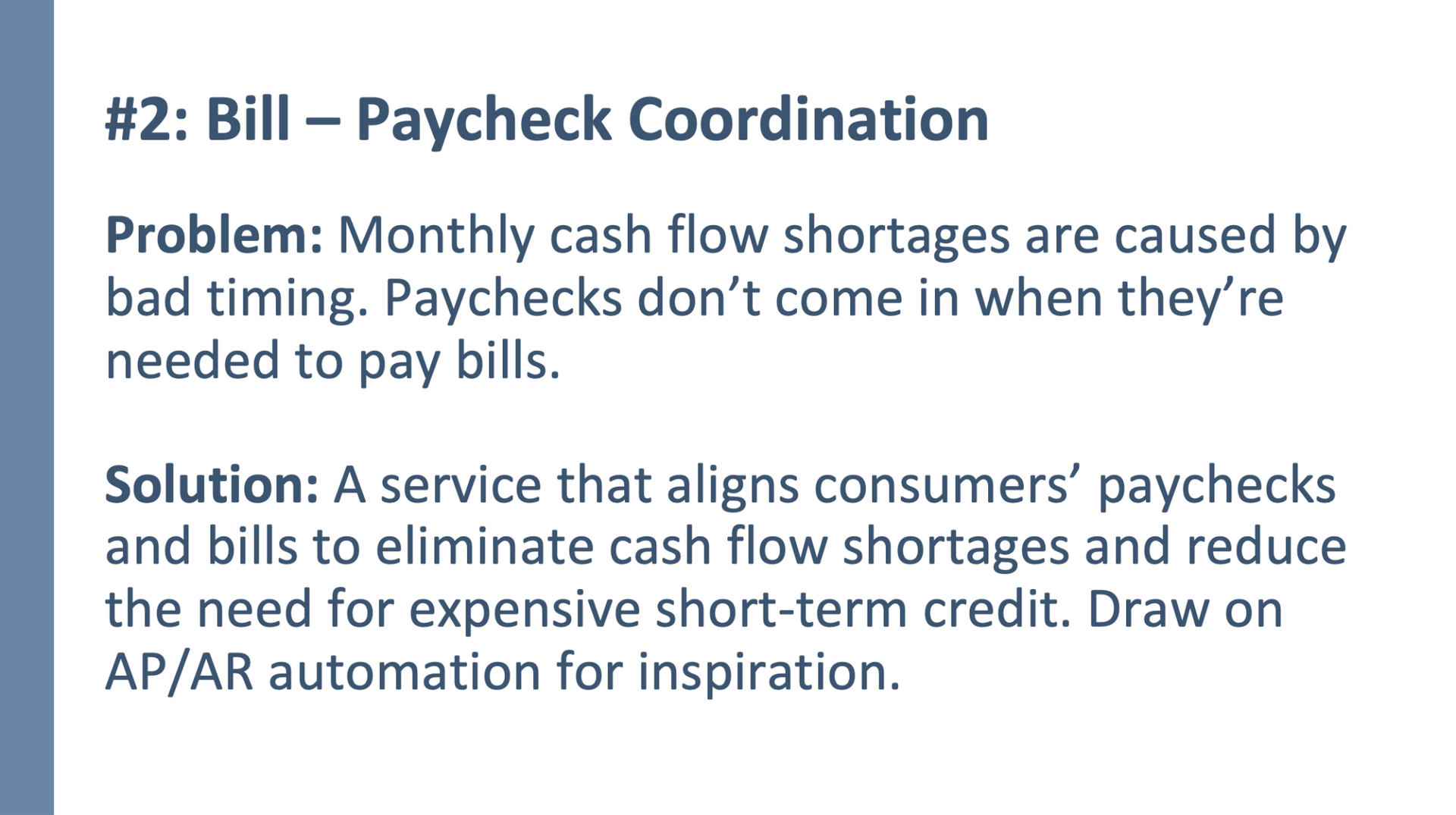

The dates on which people get paid by their employers and the dates on which they are required to pay their billers are somewhat arbitrary. Employers and billers would likely be willing to be somewhat flexible on those dates, on an as-needed basis, if it decreased stress for their employees/customers. This is especially true for billers, which view the termination of their services (e.g., disconnecting an electrical service) as a worst-case scenario to be avoided at all costs.

The problem is that there is no mechanism for proactively identifying income/bill mismatches and coordinating adjusted payment terms to solve for them. But imagine if there was!

Imagine if a bank could proactively advance a consumer their income (we are already pretty good at this in fintech through mechanisms like EWA) and/or negotiate with their billers to adjust their payment due dates to eliminate the temporary cash flow shortages that cause them to pay late or sign up for expensive short-term credit options.

|

With AI, shipping code will become easier and less expensive. Community banks will get better at building table-stakes back-end infrastructure rather than waiting on their core providers for it. However, AI won’t make community banks any better at shipping a point of view, which is what it takes to build differentiated products for specific customer segments. This is where B2C and B2B fintech startups will continue to excel.

The challenge for those startups will be customer acquisition, which has been and will continue to be one of the most intractable problems in B2C and B2B fintech. It costs a lot of money to acquire customers in the same digital marketing channels that every other fintech company is competing in. And unless your macroeconomic timing is perfect and you can convince VCs to subsidize the necessary level of marketing spend to reach scale, it’s unlikely that you will be able to get your differentiated product in front of all of the customers that could use it.

There is an opportunity here for collaboration.

Think of it as the fintech version of franchising. You help sub-scale B2C and B2B startups that have built differentiated products for specific customer segments (perhaps our neobank for teachers?) package up their products so that they can be distributed by community banks and credit unions that would be unable or unwilling to build those products themselves. |

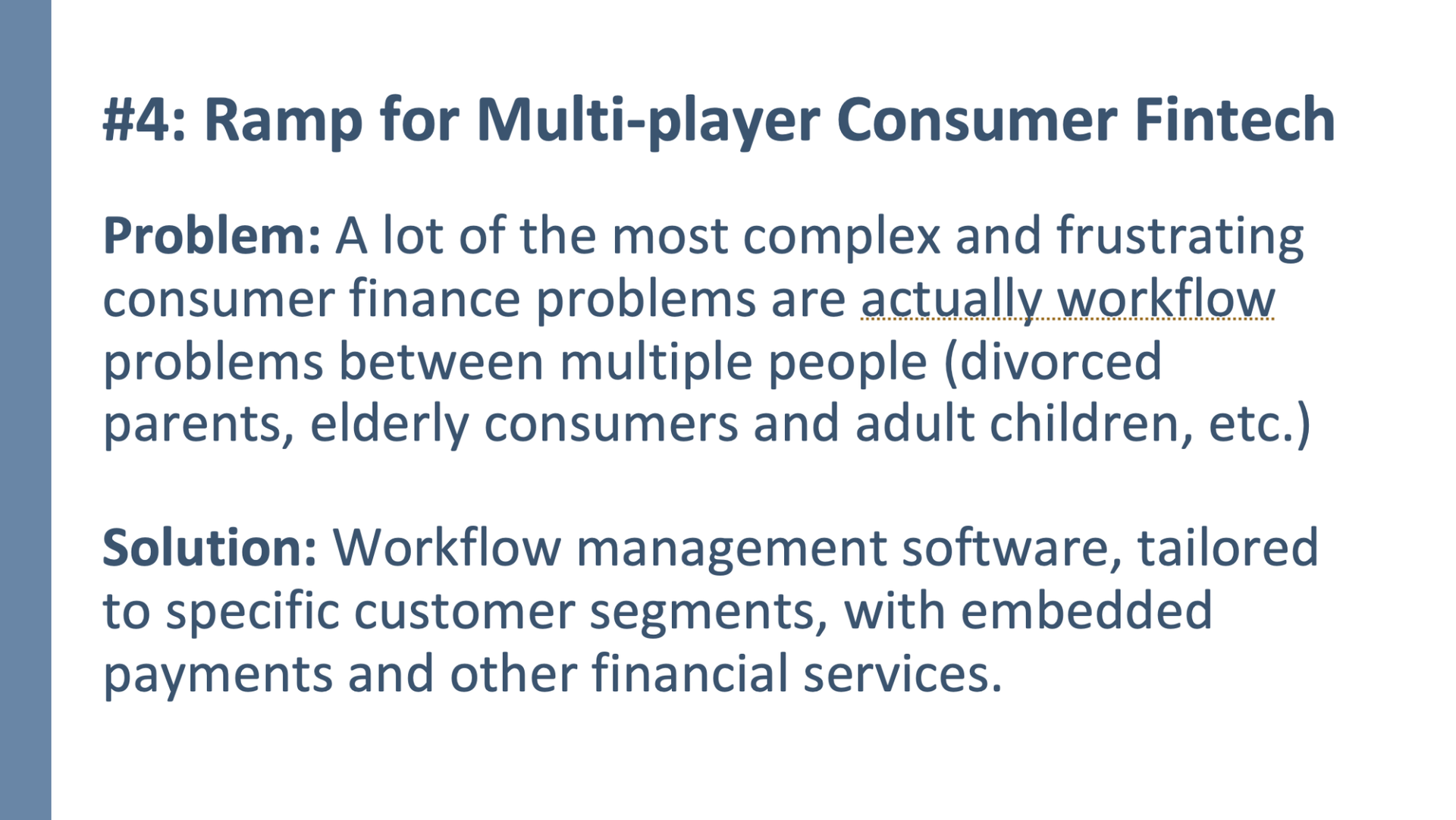

Ramp uses AI and intelligent automation to solve coordination problems within companies relating to expense management and procurement, in order to save those companies time and money.

On the B2C side, those same types of finance-adjacent coordination problems exist within specific groups of people (families, most often), but very little software has been built to help those groups solve those problems.

Where is Ramp for adult siblings who are jointly taking care of their aging parents? Where is Ramp for divorced couples co-parenting their kids? |

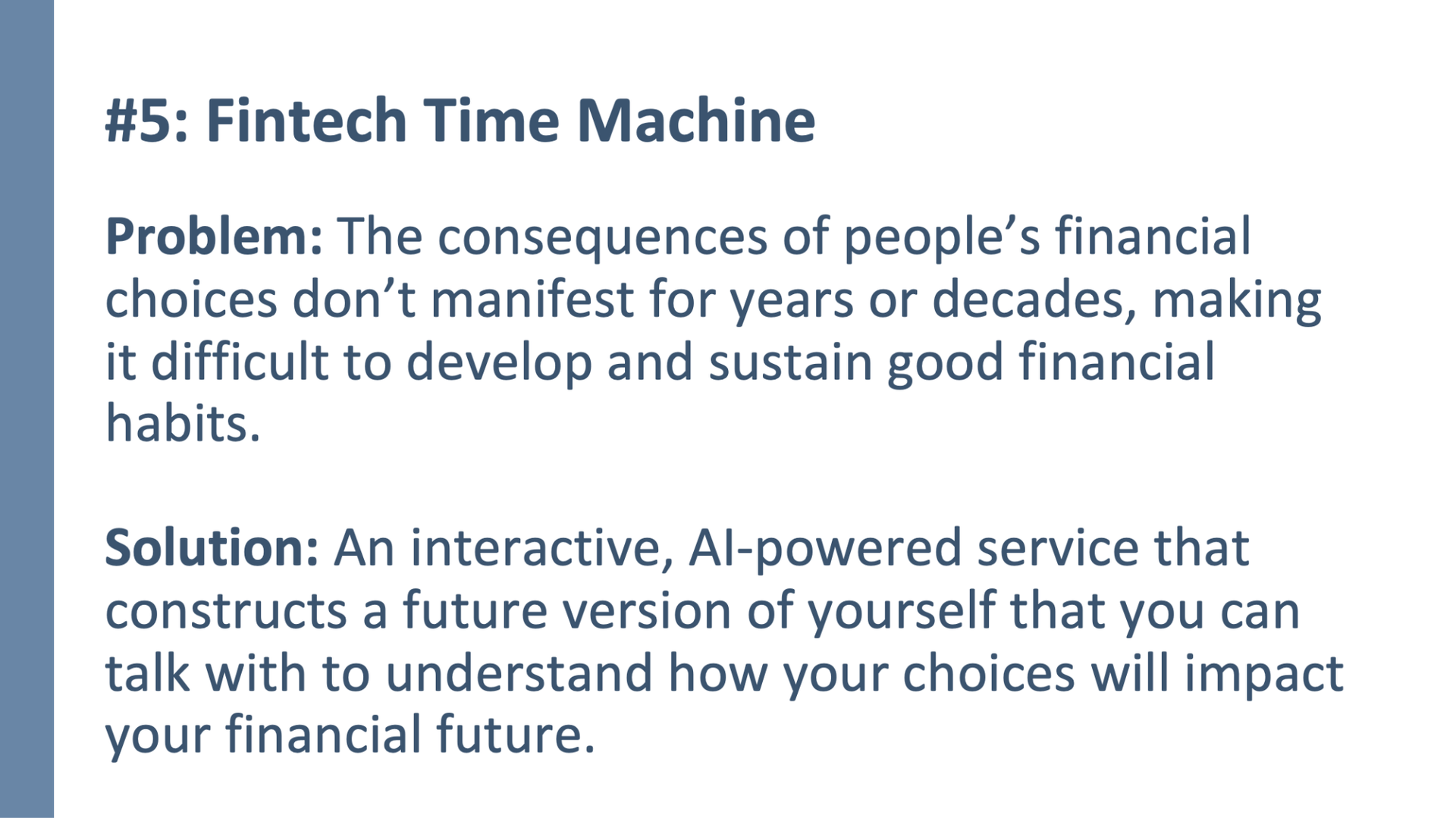

AI may finally unblock one of the biggest challenges in personal financial management: Helping people feel the future impact of their financial decisions in the present. One of the most difficult parts of establishing and maintaining good financial habits is that the benefits of those habits are only obvious years or decades down the road, while the pain from the sacrifices those habits demand is felt immediately.

Could we use AI to analyze consumers’ current financial situations and trajectories and enable them to “time travel” into the future and talk with their future selves, asking them questions about what their life is like, the past financial choices that they’re most proud of, and the ones they most regret?

(I know this one sounds a bit science fiction-y, but financial nihilism is a real problem and folks like Frank Rotman are working to solve it. It seems obvious to me that AI will be a part of the solution.)

|

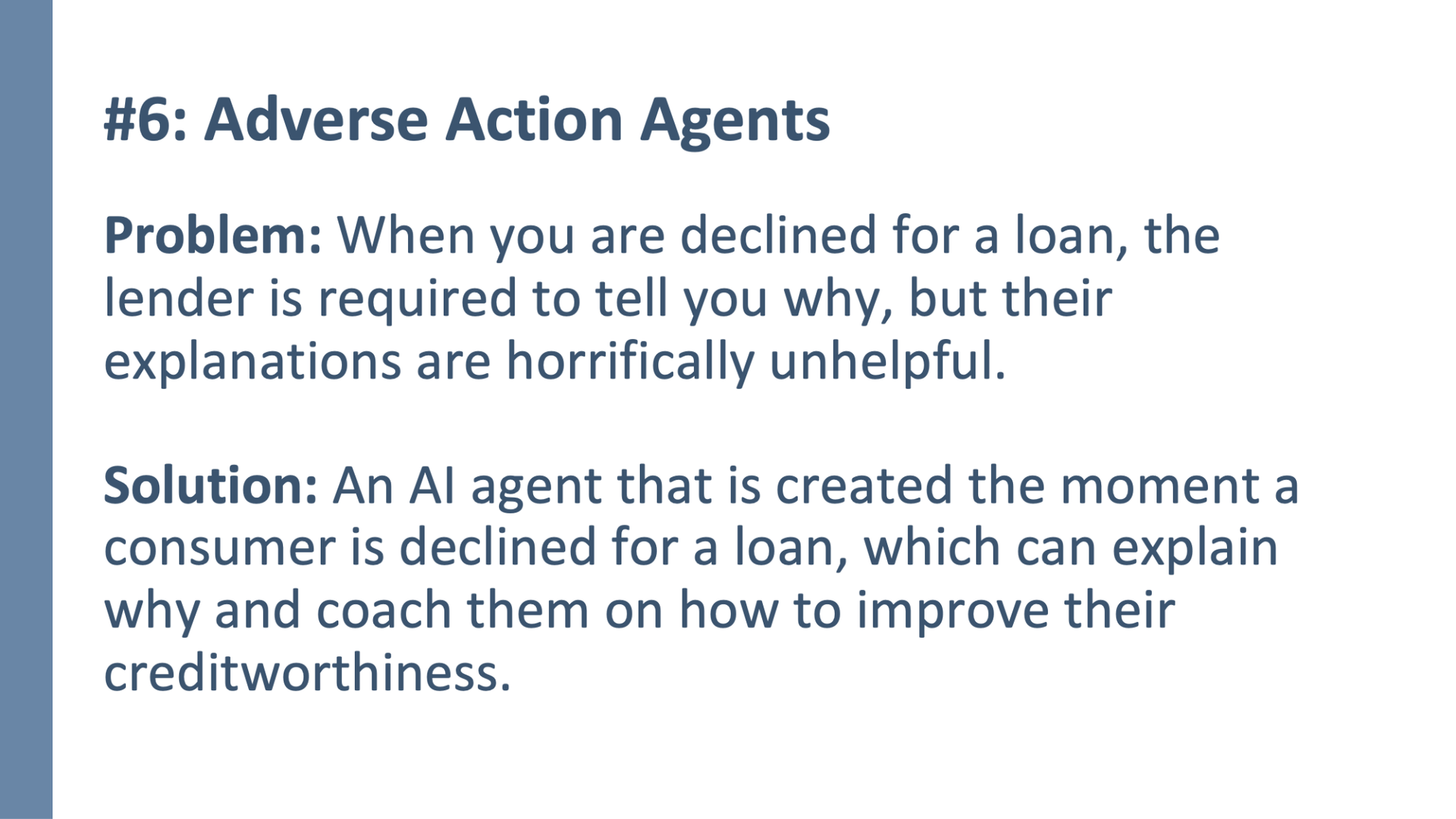

The way that we do adverse action notices — the explanations that lenders are legally required to give to applicants who are declined for loans about why they were declined — are lame and unhelpful. It’s literally just a check-the-box exercise for the lenders, and it tells consumers nothing useful about why they were declined or what they need to do moving forward to improve their chances of getting a loan. It need not be this way.

Instead, imagine if, when a consumer is declined for a loan, an AI agent is spun up instantly for that consumer to interact with. The agent could provide a comprehensive, personalized explanation to the consumer for why they were declined, and, critically, that explanation could empower the consumer to be interrogative. They could ask questions, pose hypotheticals, and request advice on how to improve their creditworthiness. |

|

|

MORE QUESTIONS TO PONDER TOGETHER |

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis.

What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

Drop your question here, whenever inspiration strikes! |

|

|

There are many fun events — virtual and in-person — coming up in the next few months. Here’s where I’ll be! |

I'm hosting a virtual event with TruStage where we'll look at how lenders are rethinking risk, and how borrowers are responding on the other side of the table. And most importantly: what frameworks actually help when you have to act without certainty. Save your spot! |

Kiah Haslett and I are going to be hosting an event with the marvelous folks at Team8 during New York Fintech Week. It’s about AI and how it is changing banks’ build, buy, and partner decisions. Great topic. Great venue. Space is limited, but let me know if you’re interested! |

There’s also going to be basketball at New York Fintech Week! Come hoop with us! |

Talk about a great topic and a great venue. We’ll be talking about bank - fintech partnerships at a ranch in the mountains in northern Montana. In June. Fuck yes. Space is very limited, but let me know if you apply, and I’ll put in a good word! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network

|

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 62,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|