{if hosp_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy. |

| |

{/if}{if profile.vars.hew_transition}

A reminder: You’re receiving this because you were previously subscribed to HealthExecWire. Hope you enjoy. | |

|

{/if}

Happy Thursday Hospitalogists!

Today we’re doing a deep dive on Sutter-Allina with the folks over at Health Data Atlas who I know really well. Note this isn’t a sponsored post but they helped provide market intel and context for the strategic decisions that may be happening in the coming days post merger.

Specifically, we’re collaborating on taking a closer look at the operator playbook Warner Thomas at Sutter might deploy at Allina, given his history at Ochsner. Warner, if you or anyone at Sutter is reading this, feel free to reach out and let us know how close - or off base - we are! Let’s dive in.

P.S. Tampa, May 19th. I'll be keynoting the 2026 Transformation Summit.

It’s a small event with senior leaders from large health systems and IDNs spending a full day on workforce strategy, system modernization, and operational transformation. If you're a CHRO, CNO, or leading transformation at a large health system or IDN, your voice should be in the room. If you've already applied, stay tuned! We'll be in touch. |

Was this email forwarded to you? |

|

|

The Warner Thomas Playbook

|

“Just a West Coast system, printing money in a lonely market. Just a Midwest org, born and raised a payer-provider. Strangers, up and down the boulevard of Healthcare M&A, searching for what the other has.”

Sutter Health’s acquisition of Allina Health is Warner Thomas’s first major deal since taking the CEO job in 2022. It’s a major signal of where he’s taking the organization.

Thomas has spent three years doing what he does best: fixing operations. He inherited a system that had been through a bruising antitrust settlement with California, years of operational drift, and a reputation for high prices. He’s built a new leadership team, tighter ambulatory network, and rebuilt credibility. Boxed in by Kaiser and the UC system, competition is fierce in the Nor Cal Healthcare market and the state has made clear it’s watching every move.

Sutter has the money and the operator. What it doesn’t have is room to run.

Allina, meanwhile, has been on a rougher ride. A $164M operating loss in 2023, a “recovery” in 2024 from selling their lab assets to Quest. Selling the furniture to make rent while the neighbors, who happen to be the Mayo Clinic, are building an addition. Still Allina holds attractive assets and the chassis for a turnaround. It has the primary care footprint and market demographics to build something significant in ambulatory and revenue diversification strategies including a VBC forward approach. However, they don’t have the capital, playbook, or leadership alignment to do it alone.

That’s where Warner comes in. He built his reputation on value-based care, but the real engine underneath was always operational: Technology Integration, Physician Alignment, Network Integrity, and serial M&A. VBC was the framework that tied it all together and gave it strategic coherence. Thomas made it work in post-Katrina New Orleans. Our bet is that the playbook travels to the midwest, and Allina is just the starting point as Sutter joins the ranks of Kaiser and Risant Health, and Advocate/Atrium to a lesser extent.

|

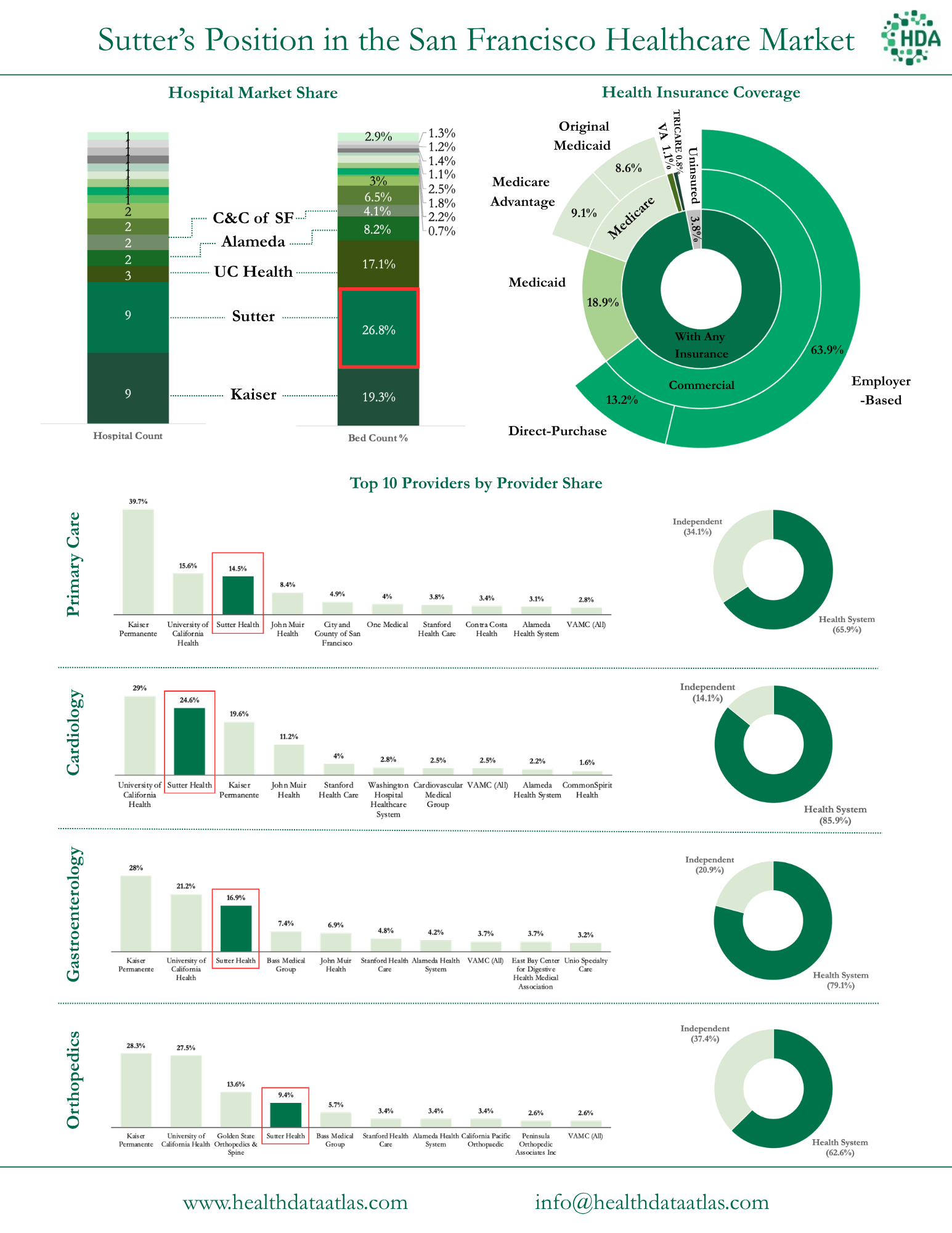

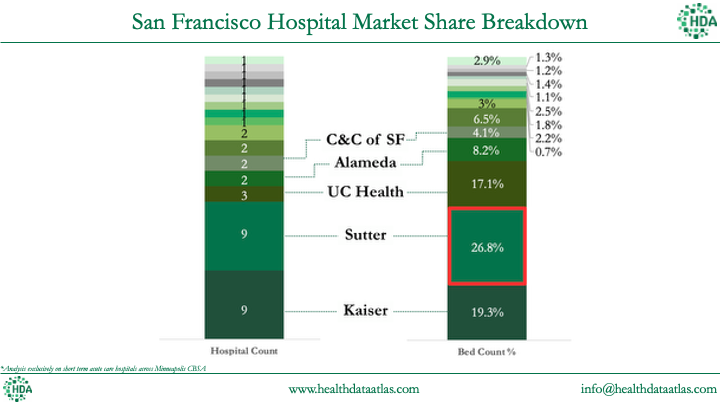

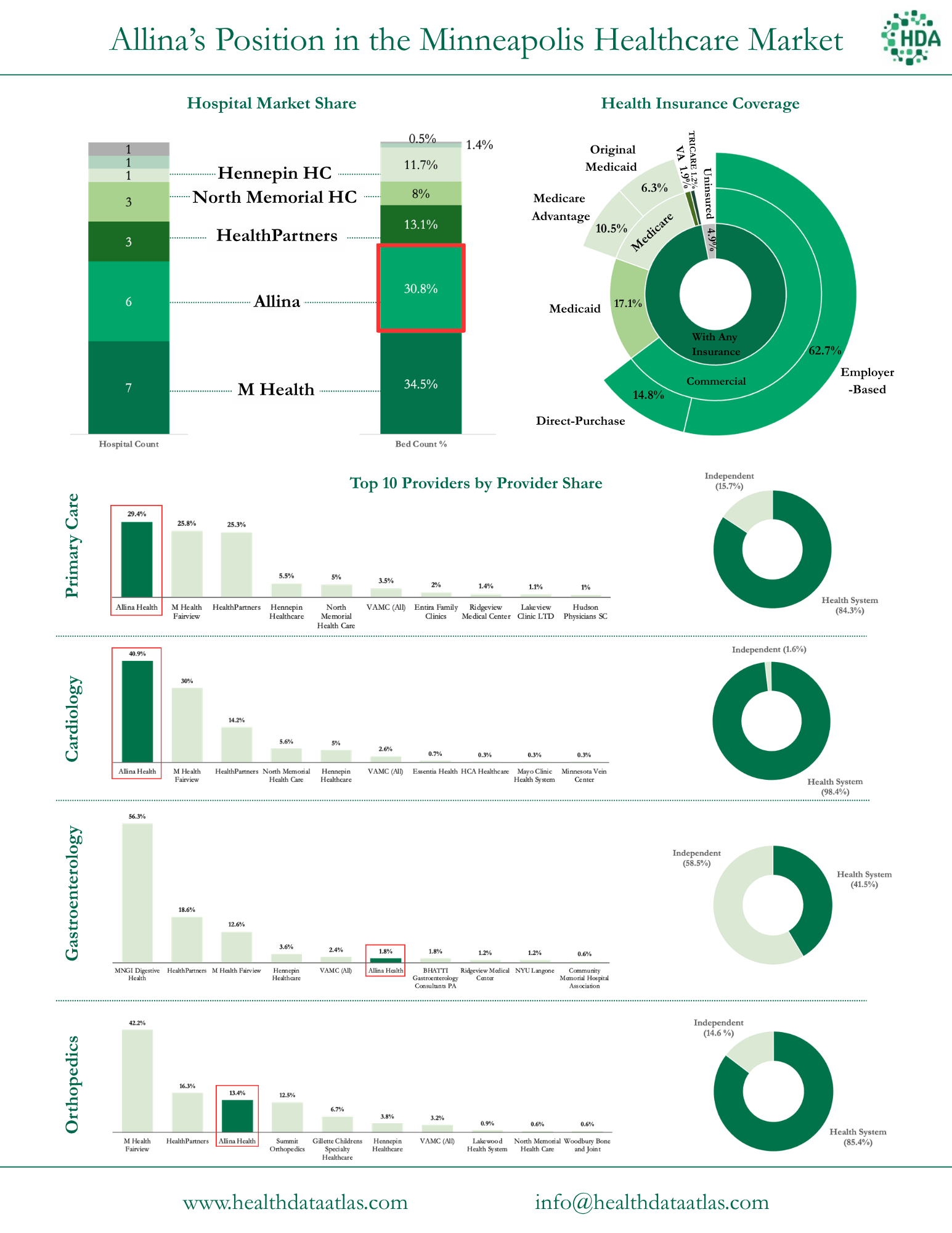

The short answer is that Sutter doesn’t have anywhere else to go in its core markets. Despite the fact that they're the largest hospital operator in the Bay Area with 27% of the bed count and tied with Kaiser for the number of hospitals, the California market is competitive with many players as seen below, and Sutter wants another area to flex its wings further while increasing its own scale for growth purposes. |

Allina’s market growth potential as compared to California’s presents more compelling economics given its current positioning. More on that in a sec.

The graphics above and below paint the clearest picture: Kaiser controls 40% of the primary care market, UC health holds ~15%, and Sutter sits at ~14%. Given the competitive dynamics and forces at play, our thought is that Sutter is saying

“It’s easier for us to land and expand and grow an existing book of business elsewhere than it is to hit growth targets in our existing markets.” |

So why are they even in a good financial position at all? Well it comes down to those sweet sweet Nor Cal Commercial Payer Rates. Because Kaiser is a closed system, if you’re a payer that isn’t Kaiser, you basically have to have Sutter in your network, and that affords them very strong negotiating leverage (hence the anti-trust concerns). That leaves them sitting in a consolidated market, with a strong balance sheet, and the state watching every move…. So where else is there to go, other than Minneapolis?

Another interesting, probably under-reported aspect of all of this is Sutter’s somewhat-sketchy past with antitrust consideration in its home state. In the past 6 years alone they have settled antitrust provocations multiple times, spending hundreds of millions of dollars in the process. Buying a health system in ho-dunk Minneapolis, however, doesn’t present the same state-level antitrust concerns. While antitrust issues persist with the state of California, similar to other cross market health system mega mergers or vertical integration deals, it’s nigh on impossible to prove potential harm stemming from the deal when there is no geographic overlap or market concentration concerns. In the short history of health system cross-market mergers and health insurance vertical integration deals, none have ever been blocked, but the FTC has succeeded in getting some concessions in the form of divestitures.

|

Have you ever heard the expression “Buy the worst house in the best neighborhood”? A similar theme rings true for Allina, both from a market dynamic standpoint and health system asset assemblage standpoint.

On the market demographics side, Minneapolis is one of the most naturally VBC-ready markets in the country. Minnesota essentially invented the HMO, their state legislation (1971) enabling prepaid health plans predated the federal HMO Act by two years (fun fact: this legislation is what led to the creation of United Healthcare - hence their headquarters.)

Minneapolis’ patient population skews older, more insured, and more employer-covered than the national average. Exactly the demographic profile where risk-based contracting economics work best, and an area where ambulatory buildout is necessary - something Allina seems to sorely lack. |

What’s ironic about Allina’s positioning is the fact that the health system literally started as a payer-provider back in 1994. It was formed from the merger of HealthSpan (the old Medica health parent plan) and HealthOne, specifically to integrate insurance and care delivery. The whole point of the organization’s existence was managed care integration...only to divest the plan assets and keep the hospitals in the early 2000s after the late 90’s HMO fallout.

If Allina had held onto its payer assets, we probably wouldn’t be having this conversation. Hindsight is always 20/20.

But they didn’t. Now Allina is struggling a bit operationally - not doomsday levels, but enough to receive some downgrades after multiple years of slim to negative operating margins. For instance Allina posted a $164M operating loss in 2023, a minor recovery in 2024 from selling their lab assets to Quest (so adjusted negative operating loss), and an $87M loss in 2025. Stated differently, Allina needs to move to a strategic position that requires capital and operational chassis/expertise it doesn’t have.

The other irony is that Allina’s position is not all that different from Sutter’s. They’re also running a fee-for-service hospital business from the #2 market position on the inpatient side; Allina just lacks rates and ambulatory presence to juice its margin. But there’s a core difference in one extremely interesting area to Sutter: Allina holds the leading primary care footprint in Minneapolis. While they missed the boat on the higher $$ ambulatory specialties, they actually employ the most PCPs of anyone in their market:

|

This physician alignment matters enormously. As we’ll see in Warner Thomas’ Ochsner playbook, VBC economics, and the rumblings of health system transformation (revenue diversification, ambulatory buildout, patient acquisition and network entrapment) run through primary care. You can’t manage total cost of care, close care gaps, or control referral patterns without a deep PCP footprint. You can’t send patients to the ER, OR, or ASC without seeing them in your system first.

Allina also has decent market positioning. Mayo as an elite national academic institution dominates the highest acuity and destination care and the Rochester corridor while M Health Fairview operates the local academic medical center (for now) and the U of M relationship. Allina’s lane is community-based, primary-care-led, metropolitan healthcare, and on the physician practice side the system also needs to contend with large independent multispecialty groups.

|

Finally, and pure speculation here, but Allina is also just big enough to be a platform for future add-on acquisitions in the midwest (hypothetically speaking of course). It fits the size and mold other acquirers, like Risant, would have liked to get its hands on, and it’s not out of the realm of possibility that Sutter, led by an M&A savant in Warner Thomas, wants to push and expand its presence further even beyond Allina.

While Allina is sitting with some mild financial stress and a lot of opportunity, they need someone with the expertise to execute the turnaround… and that’s where Warner Thomas enters the fray. |

Warner Thomas the Operator |

For a struggling nonprofit whose dominant strategy involves selling itself to survive or thrive, it can’t get much better than a nonprofit acquirer led by the guy who built Ochsner.

Warner Thomas is known as a transformative CEO leading Ochsner and now Sutter toward consumer-oriented, ambulatory-driven model. That reputation is earned, but not for the reasons most people assume. |

The Conventional Narrative |

It is impossible to understand Warner without understanding Oschner, and that would require a multi part series… so we’ll try to hit the key points:

Thomas joined Ochsner in 1998, became President/COO in 2005 and played a key role in navigating them through post-Katrina. He finally took over as CEO in 2012 as the first non-physician CEO.

At the time it was an 8-hospital system doing ~$1.8B in revenue with 1.4% operating margins.

By the time he left in 2022, Thomas had grown Ochsner into a 46-hospital, $5.7B system including a clinically integrated network covering a whopping 400,000+ lives, a nationally recognized digital medicine program, and top-decile ACO performance. By this account, the standard telling is that Thomas transformed a traditional FFS system into a value-based care powerhouse. By health system standards, this is true by all accounts.

But we’re still talking about health systems here. FFS still dominates Ochsner’s financials, comprising 85-90% of total revenues. Their Humana capitation arrangement was $298M in 2011 and $435M in 2022 - growing over that time horizon but shrinking to a rounding error by the end of Thomas’ acquisition spree. For context, less than 1% of hospital system revenue nationally comes from downside risk contracts. So Ochsner is ahead of the pack. Much of this is out of necessity given Ochsner’s presence in Louisiana, a heavy Medicare/Medicaid market - so to his credit, Thomas found areas to diversify into including risk and value-based care as well as consolidating the market for scale and density - growing his way out of troubled waters.

Ochsner wasn’t the only operator growing and taking advantage of market exits during this distinct time in Louisiana’s history. For instance, consider LCMC Health during this same time period Thomas operated Ochsner - in similar markets and dynamics. LCMC was born out of the ashes of Katrina through a series of distressed acquisitions. By 2024, it had grown to $3.5B in revenue riding the same market forces as Ochsner. So while both VBC and revenue diversification initiatives along with opportunistic M&A drove much of Ochsner’s rebound, Thomas’ operating framework provided the rest of the secret sauce. |

Warner Thomas’ Four Pillars of Operating Rigor |

Let’s dive into the Warner Thomas Execution Playbook. Thomas’ real playbook involved operational discipline engine with four interlocking components:

1. Technology Integration: Thomas implemented Epic system-wide early in his tenure to serve as a strong data foundation. In 2026 (and of course, back then), running a single instance of Epic is a notable competitive differentiator. On the VBC side you can’t run population health analytics, identify care gaps, or measure physician performance without a unified data foundation (take it from the Health Data Atlas team which lives and breathes this stuff every day). That infrastructure enabled Ochsner’s digital medicine program: remote patient monitoring for hypertension and diabetes at a scale few systems matched (22,000+ patients, independently validated at $2,200+ PMPY in savings, blood pressure control rates of 80% vs. 20% in controls).

(Sidenote: Warner, if you’re reading this, I’d love to hear about your AI side projects.)

2. Physician Alignment: The Ochsner Health Network, a clinically integrated network, was the organizational mechanism. Rather than forcing an overnight shift in how physicians practiced, Thomas created a parallel incentive structure. Physicians joined the CIN, participated in shared savings programs (and got a nice boost to their commercial rates due to some FTC loopholes), and received distributions when they hit quality and cost targets. Critically, the engagement started with primary care and expanded outwards to specialists as the financial proofpoints accumulated.

3. Network Integrity: This is the unsexy pillar that probably mattered the most financially. The CIN gave physicians a financial reason to refer within the Ochsner network rather than out of it. Every patient kept in-network is a patient generating FFS revenue across their entire care journey: primary care, specialist visits, imaging, procedures, inpatient admissions. Leakage reduction is a VBC/FFS agnostic concept that directly inflates FFS revenue. Both sides care about keeping patients within the network, and it’s a mechanism by which building VBC capabilities made the traditional business better.

4. M&A Execution: Ochsner went from 8 hospitals to 46 through a disciplined series of acquisitions: Lafayette General, Rush Health Systems, Slidell Memorial, and others. Each deal expanded the geographic footprint and the attributed population for ACO contracts. In MSSP, larger populations reduce savings variance and improve financial predictability. Every acquisition was simultaneously a FFS volume play and a VBC infrastructure play.

The common linking thread across all of these playbook components is simple, but drives success organizationally: get the plumbing and infrastructure figured out first (data, system of record) then M&A, physician alignment, and integration becomes easier, resulting in more revenue growth and diversification opportunities. |

VBC as a Turbocharger for FFS: |

The two models compounded one another. VBC infrastructure investment improved FFS performance and economics (physician alignment, network entrapment), and FFS revenue provided the bastion to fund VBC and other infrastructure investment - also incentivizing outpatient migration. As a result, Ochsner’s operating margin went from 1.4% to 3.4% over Thomas’s tenure - in an extremely government-pay-heavy health system. This transformation happened while absorbing multiple acquisitions and in a market with some of the worst chronic disease burden in the country, outperforming peers like LCMC in the process.

The four pillars that built the VBC capability also made the FFS business drastically better: -

Higher quality scores and ACO performance coupled with larger scale and market density across key assets gave Ochsner leverage in commercial rate negotiations. You couldn’t ignore them as a health plan.

-

Reduced readmissions protected Medicare revenue under the Hospital Readmissions Reduction Program, meaning fewer financial penalties on the FFS book.

- Digital health programs retained patients inside the network, driving FFS encounter volume and pioneering digital front doors as a patient acquisition and consumer-facing vehicle.

- VBP bonuses from CMS added directly to Medicare base payments.

- The VBC branding put Ochsner on the map, increased brand goodwill, and drove physician recruiting

One more thing the VBC framework provided that pure operational discipline doesn’t: air time. “We’re building a value-based care system to improve population health” is nearly unchallengeable with regulators, politicians, and physicians. It gave Thomas the narrative permission to consolidate markets, rationalize service lines, tighten referral networks, and restructure physician compensation. All of which are operationally correct but politically difficult if framed as cost cutting.

Organizations don’t do deals, people do. If you’re Allina’s board evaluating options while beaten down (cough or any other midwestern or similarly sized health system), Warner’s track record is hard to ignore. And this fact is one of the reasons why the deal came together, along with Thomas’ belief that any organization needs to grow and scale to get through short-term pain. |

Warner Thomas’ Sutter-Allina Journey Beginnings: An Ochsner Re-run? |

We’ve already established Allina’s positioning, both competitively and financially. The health system is far from dead, but with some capital in the right places, it can thrive.

Thomas is betting he can make Allina thrive, and reinvigorate Sutter’s growth prospects in the process. If he runs the 2026 version of the Ochsner playbook, and there’s no reason to think he won’t, we’d expect to see the following sequencing. |

Years 1-3: Plumbing Time. Fix the Engine & Lay the Transformation Foundation

|

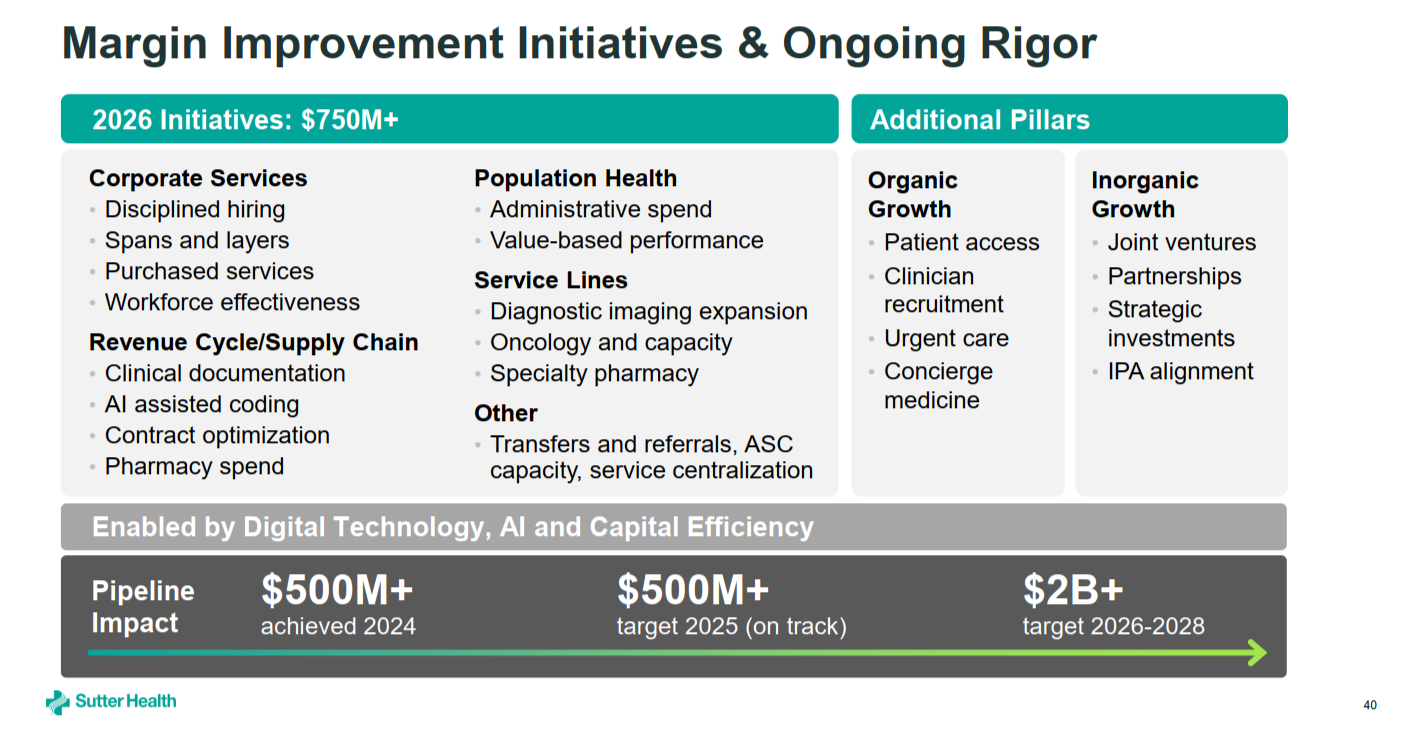

This is where the money actually gets made and where several other health systems like Ascension or CommonSpirit have spent a few years figuring out. Operating discipline and infrastructure investment comes first. Consolidate EMRs, cost structure rationalization, supply chain, labor optimization, denials management, care setting migration, identifying core markets, areas to divest, and areas where Allina needs ambulatory network buildout. Warner doesn’t need to reinvent Allina - he needs to tighten it and inject capital into the right spots.

From a cursory financial review, Allina’s supplies & services (presumably professional services) costs as a % of revenue grew 3.7% - entirely responsible for its unprofitable operation (along with poor topline revenue growth). Quick back of the napkin math pulls these expenses up as a post-transaction synergy, where Sutter and Allina can consolidate GPOs and buying power - as one example where a cross-market mega merger can flex its muscles. One other interesting area to watch (and we’re definitely not experts here) is labor. California is notorious for being one of the toughest labor markets in the U.S., and I (Blake) would bet my bottom dollar Sutter finds some sort of way to cut labor costs by somehow tapping into the Minnesota workforce. Another cost lever likely lies in financing costs. Interest rates have dropped a touch and Sutter-Allina CombinedCo can and will command low cost of capital compared to Allina alone. This factor alone should translate into material borrowing cost savings and help finance more projects across the enterprise.

|

This slide above from Sutter is a great snapshot of where they look to find strategic and financial value / levers to pull in the years ahead, and good areas to look at when perusing Allina’s footprint.

Physician alignment starts here too. Get the primary care network, arguably their biggest strategic asset, organized, incentivized, and pointed in the same direction. Start measuring referral patterns, identify leakage, and build the data infrastructure (Allina looks to already be on Epic, which removes the longest lead-time item from the Ochsner playbook). None of this requires a VBC contract to justify. It just makes the FFS business immediately better.

|

Years 3-5: Build the platform |

Building and scaling begins. Years 3-5 is where revenue diversification and initiatives like deep VBC infrastructure gets layered in. CIN formation, ACO participation, risk-based contracting with Minnesota’s already sophisticated payer market. ASC de novo builds, micro hospitals, and more are ready to open, or are 12 months into operations. Minneapolis is an easier environment than New Orleans was: HealthPartners, Medica, and BCBS of MN already speak this language and are eager to see a new invigorated competitor willing to play ball and perhaps move site of service or engage in more risk.

This is also probably a good time to mention Sutter likely didn’t hire Scott Nordlund to lead Corporate Development just to run a single integration. Once Allina is stabilized and there’s a Midwest operating base to manage from, the aperture widens and M&A opportunities manifest. |

Years 5+: The Midwest Beachhead

|

At this point, or even before this point, a now-stabilized, profitable Allina gives Sutter something it currently doesn’t have: a Midwest platform. A launchpad. The upper Midwest holds several health systems in varying degrees of strategic stress given their local market demographic realities: subscale, desperate for capital to fund transformation, geographic isolation, or caught in the same FFS-to-VBC transition gap that Allina is in. A well capitalized acquirer with a proven integration playbook, operating from Minneapolis, is positioned very differently than one calling from San Francisco and it’s a fun thought experiment to think of health systems with similar chassis to Allina that would consider aligning with these cross market national behemoths - Advocate, Risant, and now Sutter.

So, who do you think is next? |

It’s not all Rosy - Potential Execution Risks |

While Warner is the right man for the job and everything points to this being the perfect setup for his capstone career move, this move is far from a layup.

Geographic distance is real. Managing a health system integration from 2,000 miles away is operationally difficult in ways that don’t show up in the deal model. Culture, pacing, talent decisions, physician relationships are all high-touch, in-market problems. Ochsner’s acquisitions were all within driving distance of New Orleans. Minneapolis to San Francisco is not that. Governance structure and leadership consolidation can be a disaster.

He’s doing two hard things at once. Transforming a health system by building a forward-thinking VBC operating system while simultaneously integrating a financially stressed system is the healthcare equivalent of building the plane while flying it. At Ochsner, Thomas had the luxury of a market where competitors were exiting: Tenet sold, HCA left, Charity Hospital never reopened. The competitive field cleared for him. In Minneapolis, Mayo, Fairview, and the major payers aren’t going anywhere. There’s no post-Katrina vacuum to fill, and competitors are formidable.

At a macro level, VBC environment is harder than it was. CMS’s V28 risk adjustment changes are squeezing Medicare Advantage economics. Major insurers are pulling back MA plan offerings (even Ochsner exited MA at the end of 2025). Star Ratings methodology shifts are creating uncertainty. The provider-sponsored health plan path is more expensive and less forgiving than when Ochsner deepened its Humana relationship a decade ago. Tailwinds Thomas had nationally in 2012 are headwinds in 2026.

The timeline is long and the margin for error is thin. If the Ochsner playbook is the template, we’re talking 7-10 years before VBC infrastructure meaningfully changes the economics. While this is no time in health system land, that’s a long time to execute in a market you’re new to, with a system that was running operating losses 18 months ago. Not to mention, their home market competitor, Kaiser/Risant, is also out there scouting similar acquisitions which will likely accelerate the M&A timelines for any health system willing to sell to or merge with these groups before they have the foundation in place.

But. Conditions for this play are about as favorable as they’re going to get. Allina, the target, is right-sized and has the right chassis to springboard future growth initiatives outside of its core competencies. The market is VBC-native and holds revenue diversification opportunities. Allina’s PCP footprint is already there. And finally, Sutter as the acquirer has the cash and the operational expertise. If Warner Thomas can’t pull it off, then who could?

|

|

|

For those who partake in the fine game of golf, it’s peak golf season as the Masters kicks off in Augusta. But for those who are trying to find a tee time, this weekend is the unfortunate emergence of the ‘weekend hacker’ from hibernation as they clog up tee times for a few months before inevitably giving up the game until next year.

Happy hacking, Hospitalogists - and my money is on Bryson this year! |

| |

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

{if profile.vars.board_room_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Hospitalogy Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}{if !profile.vars.board_room_user_fitness && profile.vars.board_room_user_fitness != false}I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

|

|

{/if}

Get your brand in front of 68,100+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|