{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Monday, Fintech Takers!

Today’s newsletter comes to you from The Mandalay Bay, site of Fintech Meetup 2026.

It’s delightful to be back at Fintech Meetup. It’s weird to be somewhere other than The Venetian (I know that hotel way better than I’d like, but there’s a certain comfort to the horrific familiarity). And, as always, it’s mildly depressing to be in Las Vegas, although I will say that this city is slightly more fun to visit when a sporting event like March Madness is happening. And speaking of madness, what a game! I knew better than to trust Duke. I’ve mistakenly picked them to go deeper in the tournament than I should have so many times over the years. Never bet on Duke! I knew that, and yet my bracket is now completely busted. Ah, well. There’s always next year. - Alex |

Was this email forwarded to you? |

|

|

Job (1896) by Alphonse Mucha. |

|

|

#1: Did MrBeast Know What He Was Buying? |

Senator Elizabeth Warren has expressed some concerns about MrBeast’s acquisition of Step:

Senator Elizabeth Warren, Democrat of Massachusetts, sent a 12-page letter today to Jimmy Donaldson, the popular YouTuber better known as MrBeast, requesting more details about his company’s plans to expand into financial services. In February, his company, Beast Industries, purchased a banking app called Step that had planned to promote cryptocurrency to its young users.

Though Ms. Warren did not accuse the company of any wrongdoing, she asked over a dozen questions and requested additional information about its move into the highly regulated world of finance. She also raised concerns about the company’s banking partner, Evolve Bank & Trust, but much of the letter was devoted to Beast Industries’s plans to potentially push cryptocurrency to children. |

Senator Warren’s concerns essentially boil down to three facts: 1.) MrBeast has 473 million YouTube subscribers, most of them being kids or young adults, 2.) Step has exercised some extremely questionable judgment regarding its operations and products in the past, and 3.) MrBeast and Beast Industries have flirted with crypto products in the past, including in their filing for a trademark for ‘MrBeast Financial’. It’s worth pausing, briefly, on point #2, because the evidence that Senator Warren’s team discovered is pretty alarming. From her letter:

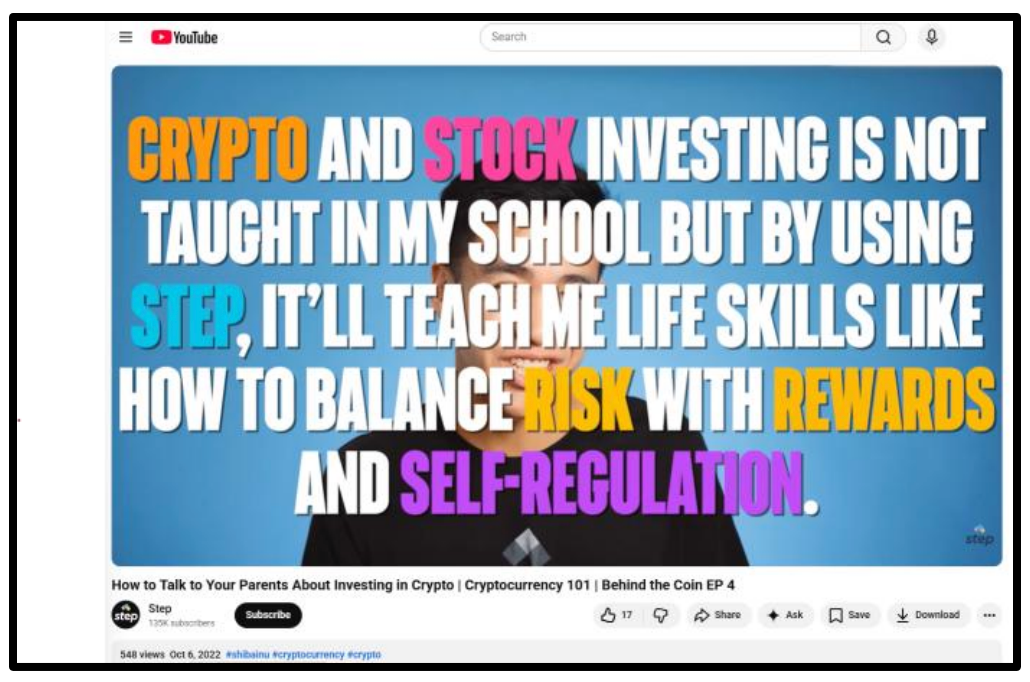

Step for example, produced a video titled “How to Talk to Your Parents About Investing in Crypto,” which was targeted at kids whose parents “want nothing to do with crypto,” “think [they’ll] end up losing all [their] money,” or “simply [do] not understand crypto in general.” The video coaches children on how to convince their parents to let them make investments their parents may not want and includes specific scripts for children to use while talking to their parents.

About half way through the video, the speaker directs the viewer to “tell them something like,” and then gives a direct script with text on screen. |

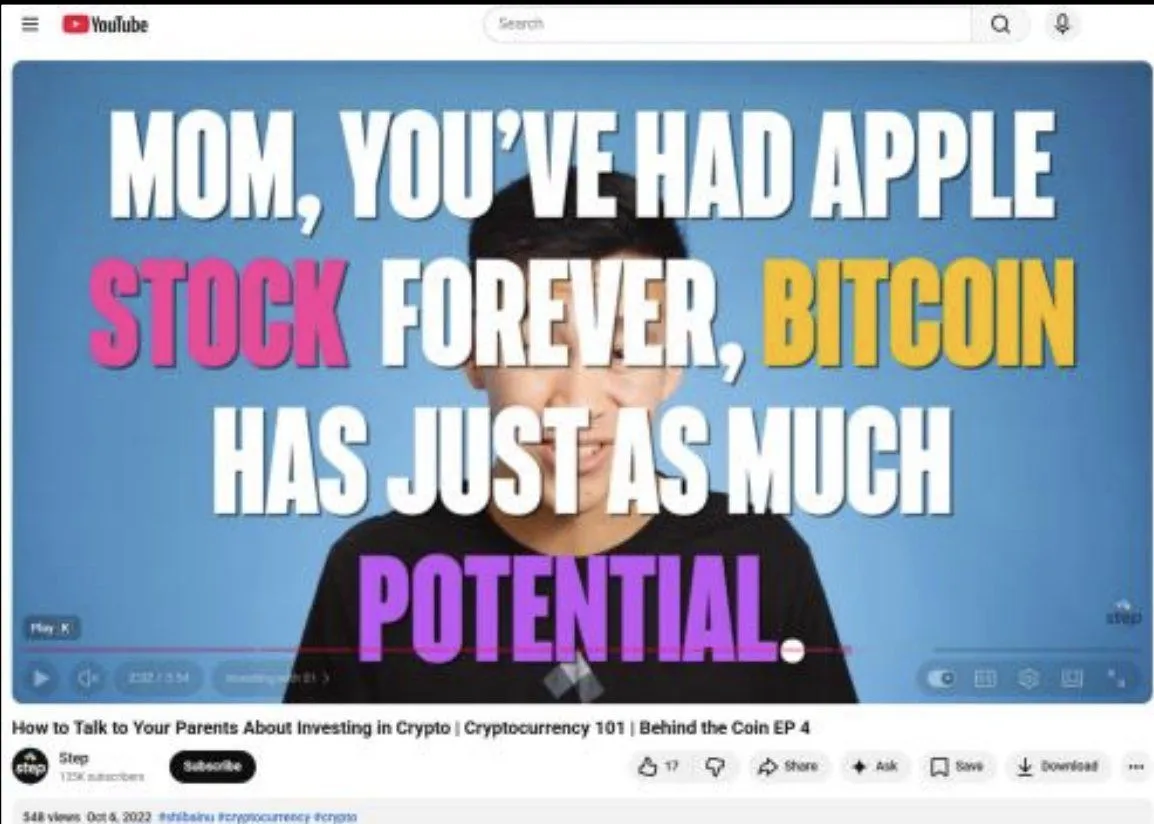

Soon after, the speaker directs the viewer to “throw in something relatable like, ‘Mom, you’ve had apple stock forever, Bitcoin has just as much potential.’” |

Then the speaker advises the viewer to go “in for the kill” and suggest starting with a small investment.

“Go in for the kill.” Yikes. That’s extremely bad, and I’m not at all surprised that Step deleted this video and the others like it, likely around the same time that the company quietly turned off crypto investing in its product. Senator Warren also asks MrBeast about Step’s bank partner, Evolve Bank & Trust, referencing the extensive compliance problems the bank has had in the past few years, including and especially its disastrous tie-up with Synapse.

Overall, I think Senator Warren is trying to suss out which of the following three possibilities most accurately describes MrBeast’s purchase of Step: -

MrBeast and his team conducted thorough due diligence before purchasing Step. They were fully aware of Step’s aggressive and ultimately unsuccessful pivot into crypto and its choice of Evolve Bank & Trust as its banking partner. Beast Industries is planning to make extensive changes to Step’s operations and product roadmap to address the types of concerns raised by Senator Warren.

-

MrBeast and his team bought Step because of its brand and its focus on delivering innovative financial products, including crypto, to young Americans, and it intends to expand and accelerate on that mission.

-

MrBeast and his team bought the first dirt-cheap consumer neobank that they could find. They did little to no due diligence in advance of the purchase, and they are considering all of their options for how to move forward with the brand and its products.

I don’t know which of these is closest to the truth, but based on a statement from a Beast Industries spokesperson to the New York Times, I suspect it’s #3 (emphasis mine):

Our primary motivation behind this deal is to improve the financial future of the next generation … Now that we’ve completed the transaction and have ownership control, we’re examining all existing offerings and marketing approaches to ensure that Step’s future is developed thoughtfully and deliberately, meets our very high quality standards, and is in compliance with applicable laws and regulatory requirements. We appreciate Senator Warren’s outreach and look forward to engaging with her as we build the next phase of the Step financial platform. That’s not exactly what you want to hear from the world’s most influential content creator, but perhaps this letter from Senator Warren will nudge things in a better direction. |

#2: Private or Permissionless? |

Payy, a stablecoin payments provider, raised a $6 million seed round:

Payy was originally founded as Polybase, a web3 database project, before pivoting in 2023 toward stablecoin payments. [Payy co-founder and CEO Sid] Gandhi said the shift was driven by the realization that the zero-knowledge technology built for its database could address what he sees as a key limitation in stablecoins — the lack of privacy.

"Today, sending a stablecoin payment is like posting your bank statement on a public website. Every amount, every recipient, every balance, visible to anyone," Gandhi said. "Enterprises will never move meaningful payment flows onchain if every transaction is visible to the world."

Payy aims to solve this by enabling private transactions by default. The startup offers a self-custodial wallet and a Visa card that allows users to spend USDC anywhere Visa is accepted while keeping onchain transactions private. It is also developing the Payy Network, an Ethereum Layer 2 rollup that uses zero-knowledge proofs to shield transaction details such as sender, receiver, and amounts. |

Payy is attacking a real problem. Public blockchains are extremely transparent, and that transparency is often a bug for payments. Most people don’t want their balances visible. Most businesses definitely don’t want competitors or counterparties mapping their cash flows in real time. If stablecoins are going to become real payment infrastructure, privacy likely has to improve.

But that creates a second, deeper issue: a big part of the compliance case for stablecoins has been their transparency.

Today, most stablecoins run on public blockchains like Ethereum. That means transactions are visible on a shared ledger. You might not know someone’s name, but you can follow the money — where it came from, where it’s going, how fast it’s moving. That visibility powers an entire ecosystem of compliance tools. Exchanges, analytics firms, and law enforcement all monitor these flows to detect fraud, sanctions evasion, and money laundering.

In other words, the pitch has been: stablecoins may move like cash, but they don’t behave like cash — because they leave a trail.

Payy wants to change that.

By hiding the sender, receiver, and amount, Payy removes the public trail. That makes payments more usable — but it also makes them harder to monitor. And that matters because stablecoins already sit in a riskier part of the financial system.

Global regulators are increasingly focused on this exact issue. The Financial Action Task Force (FATF), the international body that sets anti-money-laundering standards, has warned that stablecoins are especially vulnerable to illicit use when they move peer-to-peer between self-hosted wallets — wallets that aren’t controlled by a bank or exchange (like the one offered by Payy). In those cases, money can move quickly, across borders, and through multiple hops without a regulated intermediary in the middle.

Historically, stablecoins have leaned heavily on traceability to offset their risks. Payy is trying a different approach: keep the payments private, and replace open visibility with more targeted controls, such as identity checks at entry and exit points, rules embedded in the network, and cryptographic proofs that certain compliance conditions are met.

That’s a very different approach, one that I’m not sure the regulators focused on detecting and preventing money laundering are going to be willing to accept.

With stablecoins, we may have to choose: private or permissionless? Both may not be feasible. |

#3: Supply-Driven Financial Nihilism |

Some interesting market research was recently released. First, this from Northwestern Mutual: A sizeable number of Americans – particularly young adults – are investing in or are considering investing in high-risk/speculative assets such as prediction markets, sports betting, and cryptocurrencies. And second, this from the Federal Reserve Bank of New York: We find that legalization increases spending at online sportsbooks roughly tenfold, but betting does not stop at state boundaries. … At the same time, consumer financial health suffers. Our analysis finds rising delinquencies in participating states, with spillover effects across state lines. |

New research! Yay! Let’s start with the New York Fed research and then work backwards to the Northwestern Mutual survey.

The Fed’s analysis found that the legalization of sports betting in specific states leads to an increase in sports betting in those states. That’s not at all surprising. However, there were some interesting surprises, including: -

Average deposits per bettor have leveled off since 2022, suggesting that long-run growth in total betting is driven less by rising deposits among existing bettors and more by broader participation and continued market expansion.

-

Legalized sports betting is supposed to be done on a state-by-state basis, but because the enforcement of gambling eligibility is determined by physical location rather than legal residency, consumers who live in counties adjacent to legal states can easily access sports betting by hopping in the car and driving across state lines. The Fed finds that this out-of-state gambling activity is roughly 15% of the in-state activity, a significant amount. One notable consequence of this is that states that are not legal themselves bear negative consequences of sports betting without the tax revenue to offset the costs.

-

Following legalization, the share of under-40 borrowers who are delinquent on their credit cards rises 1.02 percentage points (and 0.55 percentage points for auto loans). It’s important to put this finding in context. Only about 3% of a state’s population takes up sports betting after legalization, which implies that the negative impact of that activity on their credit performance is significantly worse for that group (the delinquency rate effectively doubles).

OK, so that’s … not great. Though very much in line with the warnings that I’ve been giving in the newsletter for a while. Spending on gambling diverts money away from savings and investments and leads to increased delinquency.

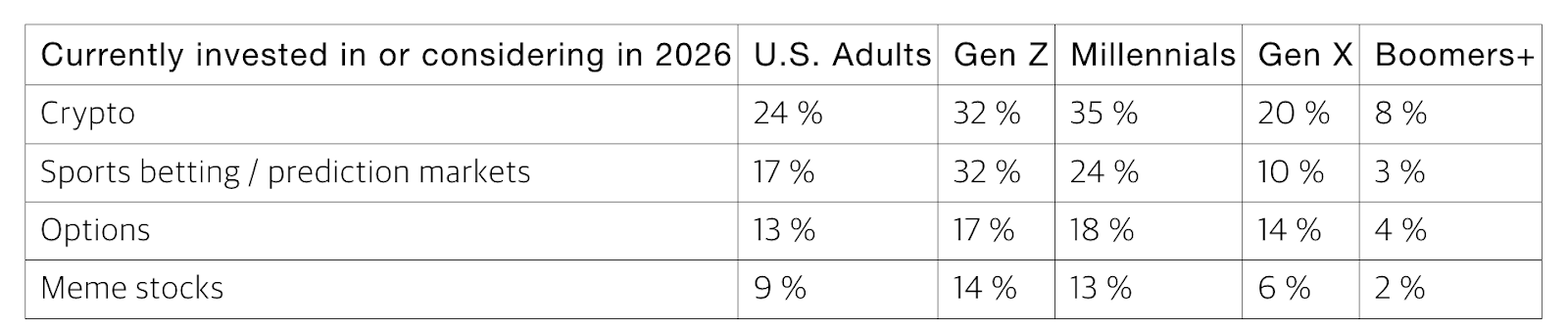

Now, let’s get to the Northwestern Mutual consumer survey data. In their analysis, they found that the percentage of consumers who are invested in crypto, sports betting/prediction markets, options, or memestocks (or are considering it this year) is relatively low overall, but significantly elevated for Gen Zers and Millennials: |

And why are Gen Zers and Millennials making these bets (or considering them)?

Well, according to 80% of Gen Zers and 75% of Millennials, it’s because they feel financially behind and believe that high-risk/speculative investments will help them reach financial goals more effectively than traditional methods.

Financial nihilism! That precisely fits the definition of financial nihilism that we use around here, and I was cheered to see Northwestern Mutual use it as well.

But here’s the most interesting part: despite these depressing findings regarding gambling and speculative investing, the overall vibe from consumers in the Northwestern Mutual survey was incredibly positive. Here are a few of the headline findings: -

Half of adults in America now say that they feel financially secure, an increase from 44% last year. This was true across all generations, with the largest year-over-year gains coming from Millennials and Gen Xers.

-

The number of Americans who consider themselves to be 'disciplined' financial planners hit a high of 65% in 2020, during Covid. Four years later, it fell to a record low of 45% in 2024. Now it is on a two-year upward trend, hitting 53% this year.

-

Three-quarters of U.S. adults agree that homeownership is essential to building wealth. And among non-homeowners, the percentage who believe owning a home is financially affordable now or will be in the future went up, with notable increases for Gen Zers (from 42% in 2025 to 54% in 2026) and Millennials (from 34% in 2025 to 47% in 2026). Additionally, fewer Gen Z and Millennial non-homeowners are citing down payments, mortgage rates, or market competition as barriers to homeownership compared to last year.

This is great news, and it highlights something very important.

The companies that profit from financial nihilism (notably, the Horrible 7 — Robinhood, Coinbase, Kalshi, Polymarket, DraftKings, FanDuel, and Crypto.com) need consumers to feel hopeless about their financial futures. They need consumers to give up on goals like homeownership to stimulate demand for their own products.

This is why they work so hard to convince consumers, particularly young consumers, that they are financially screwed (Coinbase and Kalshi are particularly gross in their attempts to do this). Or, as Kyla Scanlon put it in her most recent newsletter:

Industries have formed to monetize this nihilism through promising solutions. But the solutions never arrive, because the nihilism, the giving up, must persist in order for these products to survive.

When the narrative that Coinbase, Kalshi, and the rest are pushing (the game is rigged so you should seize every slim chance at generational wealth) clashes with reality (consumers are increasingly optimistic about their financial futures), those companies don’t adjust their messaging and their products. They double down, trying to convince people that they can’t succeed without gambling. It’s supply-driven financial nihilism. |

|

|

2 READING RECOMMENDATIONS |

An excellent read, particularly on the societal changes that are underpinning all of these new gambling products. It really does feel like the pursuit of money has become the dominant motivator in many people’s lives. |

Some alarming statistics in this article. Here are a few of them: The median retail investor spends six minutes researching before buying a stock. Roughly 75% of price-chart "research" covers one day of data or less. Where does this research occur? Well, 61% of investors under 35 use YouTube for investing information. 76% of Gen Z rely on TikTok, YouTube, and Reddit for "financial education." A majority follow online personalities, many of which have achieved their platforms by purchasing bot engagement. As such, 70% of financial content on TikTok grades as misleading or worse. Research from Almond Financial put the figure for social media broadly at 87%. 55% of people who acted on social-media-based financial advice reported losses. We will need a better solution for “proof of personhood,” although I’m wary of any solution to that problem being built by Sam Altman. |

There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network. What cities would you most like to see a fintech conference in?

Can be big or small. U.S. and international. I have my favorites, but I’m curious what yours are! If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network!

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

| |

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network

|

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 61,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|