{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Friday, Fintech Takers!

I hope it’s been a good week. I feel like I’ve been talking for five days straight. Bit tired, but we’ve got lots of good content coming your way (keep an eye on the Fintech Takes podcast feed!).

And next week I’ll be at Fintech Meetup (Vegas! Yay!). If you’ll be there and want to say hi in person, let me know! - Alex

P.S. — The world feels pretty chaotic right now. And all of that chaos has a way of finding its way into financial services: into how lenders price risk, how borrowers think about protection, and how everyone tries to make smart decisions when nothing feels certain. That's what we're digging into in my next virtual event — how uncertainty is reshaping credit from both sides of the table, and what tools and frameworks actually help when the fog won't lift. Coming up soon; save your spot.

|

Was this email forwarded to you? |

|

|

Many people are concerned about the destructive effect that AI will have on the job market and it’s not hard to understand why. The builders of AI are telling us, in no uncertain terms, that we should be very afraid.

In May of last year, Anthropic CEO Dario Amodei said that AI is not just a threat but a "bloodbath" for entry-level professional roles and predicted a 50% reduction of all entry-level white-collar jobs — particularly those in tech, finance, and law — within 1–5 years. This prediction sounded a bit insane at the time (50%? As soon as one year? Come on), but fast-forward to February of this year, and Block laid off nearly half of its workforce, citing the emergence of “intelligence tools” as the reason. And you know what happened? Block’s stock price jumped over 20% immediately after the announcement, marking its best single-day performance since February 2022.

Over a longer time horizon, AI luminaries are painting an even grimmer picture. Sam Altman believes that AI will enable sole proprietorships to scale up to billion-dollar valuations. And Dwarkesh Patel imagines a future populated by fully automated firms, in which all workers and managers are AIs, and the whole firm behaves more like a single scalable mind than a collection of separate people.

Will this happen? In ten years, will the global economy be entirely populated by fully automated firms locked in a fierce competition with the few unicorn sole props that humans managed to find before AI made us completely irrelevant? I suppose it’s possible.

There are certainly companies (*cough* Prediction Markets! *cough*) that are operating right now with the type of reckless abandon that would only be logical if the people running those companies were irreversibly convinced that they only had 1-5 years to escape the permanent underclass. However, if I had to bet (or invest in an event contract), I would say it’s unlikely we will see anywhere near the level of job market destruction that Amodei, Altman, and crew are forecasting. I recently had a conversation with a fintech friend that clarified my thinking on this topic. She said that the right way to think about the effect of AI on jobs is that it likely won’t eliminate any category of jobs entirely, but it will reduce the number of humans we need working in pretty much every job. This strikes me as a much more sensible way to think about this question.

The SaaSpocolypse is overstated, but it’s not entirely illogical. SaaS software was an unnaturally profitable business for a very long time. It led to a lot of bloat in the tech industry. As many observers pointed out after the layoffs were announced, Block did not need 10,000 employees, regardless of how effectively it has learned to leverage “intelligence tools”. Shit, Elon cut Twitter’s headcount down from 7,500 to 1,500 employees after he took over and well before AI-fueled firings were all the rage. Despite the pessimism of many (including myself), Twitter continues to work about as well/as poorly as it did before.

And while the notion that blue-collar jobs like plumbing will be safe from AI disruption has become conventional wisdom, that also seems highly unlikely. The master plumber who helps you design and execute your new build or remodel should be safe, but the third-rate plumber who you call to fix your clogged toilet will be rendered unnecessary when homeowners are empowered with the “intelligence tools” they need to learn how to unclog the toilet themselves.

Put simply, it’s complicated. The impact of AI will be felt widely, but the exact effects will differ depending on the industry, and it seems unlikely to me that the most catastrophic scenarios will manifest for workers in any industry. The reason I’m optimistic about this is that one of the most instructive case studies ever on this question just so happens to be a financial services case study that I know fairly well … |

The Automated Teller Machine |

Let’s take a brief stroll through the history of the ATM, because, as you will see, that history has also functioned as something of a Rorschach test for economists on automation, competition, and economic dislocation. We can divide that history, roughly, into four chapters. |

Chapter 1: This is a fad. |

As wages rose in the 1950s and 1960s, companies began to search for ways to reduce their labor costs. This led to the rise of a number of more efficient businesses, operating models, and technologies, including supermarkets, self-serve gas stations, and, of course, ATMs. It took a while to work out all the kinks (magstripe cards and computers small enough to be housed inside ATMs were very new technologies at the time), but by the 1970s, bank technology vendors had perfected a version of the ATM, which was fairly similar to the ones we have today. The result was a machine that could functionally replace much of what the average bank teller would ordinarily do by hand, at a cost that was significantly lower (each ATM transaction cost the bank 27 cents, compared to $1.07 for a human teller).

However, the problem, in the early days, was that bank customers weren’t in love with the idea of interacting with a machine instead of a person. Here’s an excerpt from an excellent article written by David Oks:

In 1977, the ATM finally got its big break. Citibank, then the second-largest deposit bank in the United States, decided to make ATMs the subject of a large push: they spent a large sum installing the machines across its deposit branches. The New York Times reported it as “a $50 million gamble that the consumer can be wooed and won with electronic services.” But the response was tepid. In the same New York Times article, we encounter a scene from a bank branch in Queens where one of Citibank’s ATMs was installed: “most of the customers,” the article reports, “preferred to wait in line a few moments and deal with the teller rather than test the new machines.”

|

Chapter 2: Tellers are screwed. |

As with most new technology, this consumer aversion didn’t last. Once they became accustomed to ATMs and the advantages that they could provide (24x7 availability was a big one), consumer usage started to spike. And given the cost advantages over tellers, plus the opportunity to generate new fee revenue for out-of-network transactions, banks leaned into ATMs in a big way. Here’s Oks again:

In 1975 there were about 31 ATMs per one million Americans; by the year 2000, that number had grown to 1,135, a 37-fold increase in just 25 years.

During these decades, it was widely believed that the emergence of ATMs would decimate bank tellers. But that’s not exactly what happened … |

Chapter 3: Automation isn’t so bad after all. |

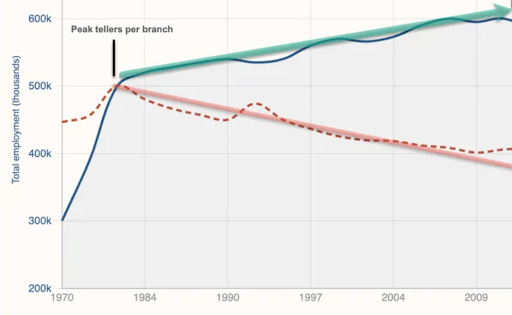

While the ATM did reduce the number of tellers needed per branch (from roughly 21 per branch to 13 per branch), it did not lead to a decline in the number of people working as bank tellers overall.

Take a look at this chart, courtesy of Paul Kedrosky. The dotted red line represents the average number of tellers per bank branch in the U.S., while the blue line represents the total number of tellers working in the U.S.:

|

Two things about this chart are interesting.

First, the unexpected result of total teller employment increasing despite the emergence and heavy use of ATMs became THE case study for economists who wanted to believe that automation doesn’t automatically lead to unemployment. Here’s Kedrosky again:

Economists and anti-anti-automaton types answer with a parable: automation transforms jobs rather than eliminating them. Tellers shifted from cash-handling to relationship banking. Everyone won. It's a clean story. It's a compelling story.

However, as Kedrosky goes on to explain, this story — ATMs free up tellers to focus on higher-value tasks like relationship banking — is deceptively incomplete. Total teller employment went up between 1970 and 2010 because the number of bank branches in the U.S. exploded during that time for reasons that had nothing to do with technology or automation:

While overall employment grew, tellers per branch fell steadily from ~1985 onward. That is the ATM effect, technology working exactly as you'd expect. Teller employment fell, even if it was masked by more branches appearing. What caused all the new branches? Technology? No. It was banking deregulation. The Riegle-Neal Act of 1994 and the preceding wave of state-level branching liberalization caused the number of U.S. bank branches to roughly double between the mid-1980s and 2009. More branches, each needing fewer tellers, produced flat-to-rising total employment.

|

Chapter 4: Falling off a cliff. |

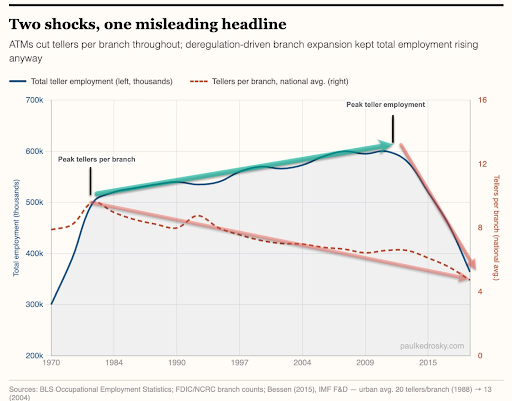

Careful readers will note that our discussion of these trends ends at 2010. Total teller employment went up until 2010. But what happened after that? Here’s the complete version of the prior chart: |

After 2010, teller employment fell off a cliff! Why? What happened in banking in the 2010s?!?

I’m guessing you already know the answer, but here’s Oks again (lengthy quote, my apologies):

In 2010, there were 332,000 full-time bank tellers in the United States; by 2016, there were 235,000; by 2022, there were just 164,000.

This was not a long-delayed ATM shock: the ATM had reached full saturation long before. It was, rather, the effect of another technology, one that had nothing to do with banking. It was a product of the iPhone.

The mobile banking vision was simple: the banking customers of the future would do all their banking via their banks’ mobile apps. They would buy things via payment cards or, later, via Apple Pay; they would check their balance or make deposits through the banking app; the customer’s relationship with the bank would be mediated entirely via the app. In this new world, there was no reason for the physical bank location to exist. Indeed there were new entrants, like Revolut or Klarna, that existed entirely as mobile apps. The branch was a thing of the past.

And so the rise of mobile banking removed any real reason to have bank branches. Visits to bank branches declined dramatically throughout the 2010s, and banks aggressively redesigned the banking experience around the digital interface. The number of commercial bank branches per capita peaked in 2009 and has fallen by nearly 30 percent since, with most of the decline occurring in wealthier areas that were more likely to adopt digital banking first.

And as the branch disappeared, so did the teller. ATM had been an innovation within the existing world of physical banking, and thus its replacement of the bank teller could inevitably only be partial; as long as people were still visiting the bank branch, it was useful to repurpose tellers as “relationship bankers.” But when branch visits declined that stopped making sense. The iPhone represented a wholly different way of banking, and within it there was no real need for the bank teller: and so a large institution like Bank of America was able to reduce its headcount from 288,000 in 2010 to 204,000 in 2018.

Oks’ theory is that while the ATM automated many of the jobs that tellers traditionally did, it did not fully eliminate the need for humans working in branches, in some capacity, because the basic paradigm of banking — accessing banking services through physical storefronts — hadn’t fundamentally changed. But when the iPhone came along, it changed the paradigm. It killed branch banking and, as a result, rendered tellers irrelevant.

This line of reasoning would suggest that the number of bank tellers in the U.S. will continue to dwindle, eventually reaching near-zero, as the new paradigm (digital-only banking) fully takes hold, perhaps accelerated by AI. But is that true?

Or will there be a fifth chapter in this story? |

Chapter 5: Are branches really dying? |

In 2024, JPMorgan Chase announced a multi-year plan to expand its already massive branch network. That plan has the bank slated to open more than 500 new branches (160 of which will be built in 2026), renovate 1,700 existing branches, and hire 3,500 employees to work in them.

The bank’s goal is to drive organic growth (it’s not allowed to grow through acquisitions anymore), specifically in deposits, in which it is hoping to grow its share to 15% of all U.S. consumer deposits. To do that, the bank believes that it needs to have a branch within 10 minutes of at least 70% of the U.S. population. This is motivating the bank to focus not on increasing branch density in markets where it is already strong, but to open branches in new, fast-growing markets, particularly in the Southwest and Southeast.

This is weird!

I thought smartphones had ushered in a new paradigm? One in which branches were unnecessary and tellers irrelevant?

We can assume that JPMC knows about mobile banking and understands that many of the fintech competitors that Jamie Dimon so publicly worries about operate entirely through digital channels, with no branch network (and no tellers) to speak of.

Given that, and given how smart we know that Dimon and the rest of the folks running JPMC are, we should probably assume that they know something that others don’t. Something about the value of branches and in-person, human-to-human interactions, even in a digital-first world. I don’t know what that something is, exactly, but I think we would be foolish to discount it. |

Depending on which chapter you stop at, the story of ATMs, branches, and mobile banking will leave you with a different lesson.

If you stopped in the 70s, right after Citi made its big bet on ATMs and then saw longer lines in its branches, you’d assume that ATMs would be utterly ineffective at replacing tellers. If you stopped anywhere in the 80s, 90s, or early 2000s, you’d assume the opposite and tell your kids not to choose bank teller as their profession. If you stopped in 2010, at the peak of bank teller employment (thanks to the explosive deregulation-fueled growth of branch banking), you’d assume that the fears about automation eliminating jobs are overblown and that tellers relationship bankers will be around forever. And if you stopped anywhere in the last 15 years and marveled at the disruptive success that digital-only fintech companies have had in the industry, you’d assume that branches are indeed dead and there won’t be any bank tellers working in this industry 50 years from now.

Maybe that’s true! Maybe JPMC is a dinosaur that is marching resolutely towards the comet that is coming to wipe it out. I don’t know. Nobody knows, and that’s the point.

The AI discourse is scary. Truthfully, at this moment, I don’t know what to tell my kids about what they should study in school, the likely return on an investment from a college degree, or what professions they should consider.

However, despite this uncertainty, I don’t think it’s unreasonable to be optimistic about the future of the job market in the age of AI.

My personal view is that AI will likely reduce the number of humans we need in virtually every job, while greatly expanding the range of work available for humans to pursue (including new ways to create value in financial services!)

But if I’m wrong, that’s OK. No one knows anything! |

|

|

MORE QUESTIONS TO PONDER TOGETHER |

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis.

What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

Drop your question here, whenever inspiration strikes! |

|

|

There are many fun events — virtual and in-person — coming up in the next few months. Here’s where I’ll be! |

This will be a busy one! In addition to meetings, I’ll be speaking at 3-4 sessions? Including as the host of the first-ever Fintech Family Feud gameshow? Are you intrigued? |

This will be my first B3! It’s hosted by the Bank of North Dakota, and I could not be more excited to visit Fargo! |

Kiah Haslett and I are going to be hosting an event with the marvelous folks at Team8 during New York Fintech Week. It’s about AI and how it is changing banks’ build, buy, and partner decisions. Great topic. Great venue. Space is limited, but let me know if you’re interested! |

There’s also going to be basketball at New York Fintech Week! Come hoop with us! |

Talk about a great topic and a great venue. We’ll be talking about bank - fintech partnerships at a ranch in the mountains in northern Montana. In June. Fuck yes. Space is very limited, but let me know if you apply, and I’ll put in a good word! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network

|

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 61,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|