{if hosp_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy. |

|

|

{/if}{if profile.vars.hew_transition}

A reminder: You’re receiving this because you were previously subscribed to HealthExecWire. Hope you enjoy. | |

|

{/if}

Hospitalogists,

Another month down (nearly) in 2026. The year is a quarter over already - how have you gotten better today?

I’m kidding. Take a breath. The world demands you constantly be in motion. You don’t have to be. Have some compassion for yourself today

I have had a crazy March, so I took a beat and reviewed all of the major stories (at least…I THINK I caught all of them) from the month. Let me know if any flew under the radar that I need to look at.

Let’s dive in!

P.S. Primary care is becoming the most strategic asset in a health system's portfolio. And AI is about to make it doubly so. Join me next month for a conversation on how leading organizations are turning primary care into an intelligence model, not just a staffing one. RSVP here!

|

Was this email forwarded to you? |

|

|

Going deeper on an interesting topic, theme, or trend

|

Recapping top news in March |

Here’s how this is broken down: - Top 10 headlines from the month

- 5 key categories

-

Each category starts with the stories I consider the most relevant and tail off from there

- Summaries are AI-generated. This is intended to be a news aggregation piece, not a deep think or analytical piece.

Let me know if this format is helpful! |

Top 10 Healthcare Headlines from March |

1. Sutter Health to acquire Allina in $26B mega-merger. Cross-market consolidation builds scale, tech investment capacity, and insurer leverage beyond local markets. More to come from me on this one!

2. Select Medical to go private at $3.9B enterprise value. Take-private by consortium of Ortenzio, Jackson, and WCAS. Renewed investor interest in post-acute and OP rehab assets. PS - how in the absolute hell did I miss this headline in early March? I have been asleep at the wheel and I apologize. Deep dive coming on this one imminently.

3. FTC launches healthcare task force targeting M&A enforcement. Signals tougher federal scrutiny of healthcare consolidation as costs and competition concerns intensify.

4. Providence explores sale of health plan amid losses. Shows provider systems may shed insurance assets to preserve liquidity and refocus operations.

5. UHS acquires Talkspace for $835M. $835M deal creates first national end-to-end behavioral health platform; Talkspace had $229M rev in 2025.

a. UHS CEO: Talkspace $835M acquisition builds first national end-to-end behavioral health model. UHS acquiring Talkspace for $5.25/share (~$835M); gains 6,000 licensed therapists serving all 50 states.

6. MA enrollment declines month-over-month for first time in at least 12 years. CMS Dec 2025: MA enrollment fell ~6,500 to 35.62M — first decline since 2013.

a. Regional MA plans surge as national payers retreat. Froedtert ThedaCare posts record MA growth; small plans credit stability over nationals' turbulence.

7. CMS phases out fax machines, saves $782M annually. Digitization can cut administrative waste, accelerate claims exchange, and modernize government healthcare infrastructure.

8. 47K comments on '27 MA rate proposal break CMS record. Record-breaking public comment volume signals massive industry opposition to proposed rate methodology.

9. A month of hospital divestitures and portfolio realignment continues. CHS to sell 9 hospitals, Ascension's remodeled hospital footprint, CommonSpirit divestitures continue, Providence too.

a. Ascension shrinks from 139 to 90 hospitals, calls it growth. 49 fewer hospitals since 2022; refocusing on ambulatory/ASC via $3.9B Amsurg acquisition.

b. CHS to sell 9 hospitals for more than $1.2B. CHS divesting AL, TN, AR, PA hospitals to tighten footprint and reduce debt.

c. CommonSpirit sells hospital, plans 6 more divestitures. Major Catholic system continues asset rationalization; also exiting Conifer RCM deal.

d. Providence to sell California hospital. Continuing divestiture trend among large nonprofit systems; strategic footprint reduction.

e. Tenet to merge 2 Texas hospitals. Consolidation play in high-growth Texas market; part of Tenet's ongoing portfolio optimization.

10. Bill introduced to ban Medicare funding for PE-owned hospitals and nursing homes. Murphy (D-CT) + Scanlon (D-PA) 'Take Back Our Hospitals Act' targets ~488 PE-owned facilities; cites 11% higher nursing home mortality. |

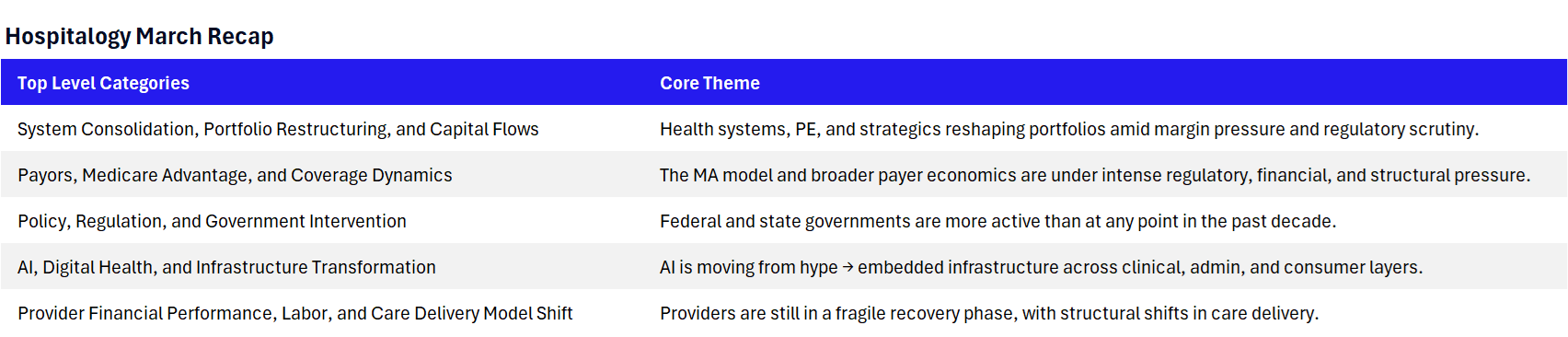

System Consolidation, Portfolio Restructuring, and Capital Flows |

-

Cigna CEO Cordani retiring; COO Brian Evanko named successor. 17-year CEO tenure ends July 1; Cigna grew from $18B to $275B revenue under Cordani.

-

UnitedHealth rolls back subsidiary disclosures. SEC filings cut from 3,100 subsidiaries to just 10; reduces market visibility into Optum/UHC.

-

Qualtrics / Press Ganey merger collapses. Banks halted the $6.75B deal due to AI-related concerns in the debt markets. Announced in Oct '25; quietly imploded in March. A rare data point on AI's impact on deal financing.

-

Olympus sells EyeSouth retina business to Cencora for $1.1B. Divestiture underscores continued outsourcing and consolidation in specialty physician practice management.

-

New Mountain Capital scraps $32B deal with ex-partner Matt Holt. NM sent letter to LPs saying Holt missed deadlines and submitted a lower offer with uncertainties. Abrupt end to what would have been a massive healthcare AI platform — Datavant, Swoop, Machinify, Smarter Technologies, and Office Ally.

- Abbott completes $21B Exact Sciences acquisition. Big diagnostics deal expands vertically integrated testing platforms as large medtech pursues growth.

-

DoseSpot + Arrive Health merge → "Interra Health." Combines e-prescribing with pharmacy/medical benefit data. $100M projected 2026 revenue, 40% growth target. Bain Capital takes majority; Providence, UPMC Enterprises, PSG as minority investors.

-

Aveanna Healthcare acquires Family First Homecare. Aveanna expanding home health footprint. Tuck-in.

-

Premise Health + Crossover Health complete merger. Worksite and near-site care combination is now complete.

-

Quantum Health acquires CirrusMD. Second recent acquisition for Quantum after Embold Health. Adds virtual care to its employer navigation platform.

-

TPG invests $250M in FindHelp. SDoH platform from TPG's impact fund. FindHelp expanding into Medicare/Medicaid benefits enrollment verification.

-

CommonSpirit exits Conifer RCM deal. Major system dropping Tenet's RCM subsidiary; signals shift in outsourced RCM relationships.

-

Optum Health new CEO charts strategic reset. Leadership change reflects pressure to restore growth, execution, and trust at Optum.

-

Cigna/Evernorth quietly acquires hospital pharmacy CarepathRx. CarepathRx serves ~10% of US hospitals; deepens Cigna's pharma supply chain control.

-

Geisinger seeks relaxed capital rules post-Risant acquisition. Integration with Risant is testing how nonprofit restructurings affect insurance regulation and capital.

-

Merck acquires Terns Pharmaceuticals for ~$6.7B. $53/share (31% premium to 60-day VWAP) for TERN-701, oral CML asset; expected Q2 2026 close.

-

Surgery Partners hits $3.3B revenue, acquires vascular ASC operator. $3.3B in 2025 revenue; expanding into vascular ASC vertical through acquisition.

-

Maimonides Medical Center – NYC Health+Hospitals merger may be delayed after AG intervention. NY AG ruled merger requires Brooklyn Supreme Court approval, blocking planned April 1 close; could take months.

-

CommonSpirit Health and Humana reach 3-year MA contract deal. 3-year national deal covers 140+ hospitals across 24 states; restores CO and TX markets after 2025 split.

-

Janus Living REIT debuts on NYSE, valued at $5.9B. Public markets are reopening for senior housing, reflecting investor appetite for aging demographics.

-

Beth Israel Lahey Health CEO to step down. Major leadership transition at large integrated system in competitive Boston market.

-

Faith-based investor coalition sues UnitedHealth to force M&A impact disclosure. Fond des Missions filed suit after UnitedHealth excluded shareholder proposal on decade-long acquisition impacts from 2026 proxy.

-

MUSC Health acquires primary care group for $111M. $111M primary care acquisition signals AMC appetite for employed physician growth.

-

PE's outpatient buying spree accelerates. Continued PE capital deployment into outpatient surgery and physician practice acquisitions.

-

Prime Healthcare reveals 2 criteria for acquiring hospitals. Distressed-hospital M&A remains selective, with buyers demanding mission fit and operational turnaround potential.

-

Palladium acquires majority stake in DME Express. Private equity keeps targeting home medical equipment, betting on recurring demand and fragmented markets.

-

MedArrive acquires Inbound Health assets for home care expansion. Hospital-at-home assets are consolidating around logistics and AI orchestration, not standalone platforms.

-

Blue Water Acquisition IV healthcare SPAC prices $125M IPO. SPAC issuance suggests speculative healthcare financing is alive, though still risk-heavy and selective.

-

Harrison Street sells San Jose medical office building to Santa Clara County for $340M. Newly constructed 230,506 SF build-to-suit MOB sold to County of Santa Clara; houses Valley Health Center.

-

Wellgistics signs $105M LOI for Neuritek Therapeutics. Shows distributors are seeking biotech upside beyond traditional pharmaceutical logistics.

-

Biopharma funding dropped 20% in 2025 to $82B as IPO haul hit 10-year low. IQVIA: biopharma funding and IPOs dropped sharply; markets remain constrained.

|

Payors, Medicare Advantage, and Coverage Dynamics |

-

CMS suspends new enrollment in Elevance MA plans. Rare sanction over 7 years of risk adjustment data noncompliance; Elevance stock dropped 8%+.

-

Aetna pays $117.7M to settle DOJ MA upcoding allegations. Two separate issues: $106M from a chart review program + $11.5M from morbid obesity codes.

-

No-premium MA plans face 50% benefit cuts under '27 proposed rate. AHIP warns zero-premium plans could lose half of supplemental benefits under CMS proposal.

-

Managed Medicaid flips from profit center to loss leader. Wakely analysis: MCO margins went from +2.4% in 2023 to 1.0% in 2024 ($2.8B aggregate loss).

-

Moody's: Insurer 2026 outlook negative — cost pressures continue. MA rate pressure + MLR blowouts + OBBBA Medicaid cuts = sector-wide negative outlook.

-

MA $76B overpayment: MedPAC documents the paradox of who benefits. MedPAC: MA costs 14% more than FFS in 2026; $76B excess payments projected, $1.2T through 2035.

-

Trump admin considering automatic default enrollment into Medicare Advantage. CMS Medicare Director Klomp floated auto-enrolling beneficiaries into MA or ACOs — straight from Project 2025.

-

Highmark Health posts $674M operating loss in 2025. $32.4B revenue but $674M operating loss — 3x worse than 2024's $209M loss; insurance arm lost $609M.

-

Mount Sinai and Anthem officially split (out of network). 9,000 physicians + all facilities now OON as of 3/4; Anthem owes $450M+ per Mount Sinai.

-

CommonSpirit Health and Humana reach 3-year MA contract deal. 3-year national deal covers 140+ hospitals across 24 states; restores CO and TX markets after 2025 split.

-

Eli Lilly launches direct-to-employer GLP-1 platform (Employer Connect). Zepbound at $449/mo bypassing PBMs; 15+ program administrators; channel disruption play.

-

BCBS Michigan posts $246M loss in 2025. Part of broader Blues losses; regional plan model under severe pressure from rising medical costs.

-

BCBS Massachusetts posts $223M loss in 2025. Major regional Blues plan loss adds to ~$900M aggregate Blues losses reported this week.

-

Point32Health posts $301M loss in 2025. Largest single Blues loss this week; underscores structural profitability crisis.

-

9% of 2025 ACA enrollees now uninsured per KFF poll. Coverage churn shows affordability pressures can quickly reverse ACA gains.

-

Excellus BCBS posts $108M operating loss in 2025. Another regional Blues plan in the red; adds to mounting evidence of Blues model strain.

-

UHS expects 25-30% drop in ACA exchange volumes in 2026. Major volume decline forecast as enhanced subsidies expire; direct hospital revenue impact.

-

Indiana passes bill blocking Elevance's 10% OON hospital penalty. State legislative pushback against insurer OON penalty tactics; Elevance targeted directly.

-

Legacy Health, Regence BCBS face contract expiration. Contract standoffs show payer-provider leverage battles shaping access, pricing, and patient disruption.

-

Humana hit with class-action over tobacco surcharges. Lawsuits against wellness surcharges could reshape employer plan design and affordability enforcement.

|

Policy, Regulation, and Government Intervention |

-

Nebraska files 1115 waiver to eliminate retroactive Medicaid coverage. ~$100M projected federal + state savings. Hospitals screaming: Bryan Health estimates $35M annual loss. "We're inflicting $2 of pain to save $1." Big upstream fight for providers.

-

CMMI launches ASPIRE Model — accelerating state pediatric innovation. $125M, 10-year, up to 5 states, targets 23% of Medicaid kids with complex needs.

-

Iowa raises provider taxes to OBBBA limit — supplemental payment maneuvering. HMO tax spikes 0.925% → 3.5% retroactively; Iowa racing the April OBBBA deadline.

-

NC lawmakers target hospital property/sales tax exemptions. Lawmakers moving to strip nonprofit hospitals of property/sales tax exemptions — no fiscal estimate yet.

-

FDA warning letters to 30 telehealth companies. Over illegal compounded GLP-1 marketing. Major enforcement action that pairs well with the Hims/Novo saga (spoiler: Hims won).

-

White House unveils national AI legislative framework. White House AI framework favors innovation over restrictions, shaping clinical AI policy.

-

RWJF / Urban Institute: Medicaid work requirements could cause 5M–10M to lose coverage by 2028. Urban Institute models 4.9M–10.1M coverage losses under H.R. 1 work requirements; 3M–7M from requirements alone.

-

FTC nears proposed settlement with CVS Caremark over insulin price manipulation. CVS Caremark second Big 3 PBM to settle FTC insulin lawsuit; deal modeled on Express Scripts agreement.

-

Senate Dems lay out health insurance reform agenda. Democrats are previewing a broader 2026 fight over affordability, transparency, and insurer practices.

-

Federal Medicaid fraud probe expands to 10 states. Widening federal investigation into Medicaid billing fraud across 10 state programs.

-

Centene pitches CMS on 7 Medicaid fraud reforms. Largest Medicaid MCO proposing structural fraud prevention reforms ahead of HR1 implementation.

-

Lawmakers introduce bill to reverse HR1 Medicaid cuts. Counter-legislation to reconciliation bill's $880B+ Medicaid cuts; bipartisan implications.

-

Minnesota sues feds over ~$244M in frozen Medicaid funds. State vs. federal clash over frozen Medicaid payments; test case for other states.

-

House hearing dissects healthcare's cost problem: 8 takeaways. Cost debates are broadening beyond hospitals to insurers, drugs, middlemen, and policy design.

-

MedPAC again urges Congress to require ASC cost reporting to Medicare. MedPAC's March 2026 report renews call for mandatory ASC cost data; 'policymakers know little' as ASC spending grows.

-

CMS opens MAHA ELEVATE lifestyle medicine model applications. CMS is backing prevention models, elevating lifestyle medicine in chronic disease policy.

-

Louisiana bill requires human review of AI coverage denials. States are moving to curb opaque AI denials and preserve clinician accountability.

-

States propose new laws for healthcare real estate investors. States are expanding oversight of investor ownership and healthcare real estate control.

-

Hospice orgs call for CA Medicare enrollment moratorium (fraud). Fraud concerns may trigger tougher enrollment controls, balancing program integrity against patient access.

-

Congress launches investigation into rampant hospice fraud in California. House probes CA hospice oversight; fraud cases and federal crackdown intensify.

-

GuardDog Telehealth admits improper records access in Epic case. The case could tighten interoperability oversight and deter misuse of patient data pipelines.

|

AI, Digital Health, and Infrastructure Transformation |

-

AMI Labs raises $1.03B Seed at $3.5B pre-money valuation. Yann LeCun-founded AI "world model" company with Nabla as its exclusive first partner. Alex LeBrun (Nabla's former CEO) steps in as AMI CEO.

-

Verily raises $300M, Alphabet drops to minority investor. Series X Capital led, with UCHealth + Univ. of Colorado Anschutz participating. Alphabet effectively spinning out Verily after years of trying.

-

Translucent raises $27M (Google Ventures). AI agent for hospital finance departments. Northwestern Medicine and Duly among customers. Fast follow to its Aug '25 Seed.

-

AI scribing → E&M coding intensity. BCBS report specifically calls out Abridge, Nuance, Commure, Fathom, CodaMetrix, SmarterDx, Ambience, and Arintra.

-

Stryker cyberattack delays surgeries, disrupts supply chain. Highlights medical device cyber risk as outages increasingly threaten care continuity and hospital resilience.

-

Google AMIE passes first real-world clinical trial: 90% diagnostic accuracy, zero safety interventions. 100 patients at Beth Israel Deaconess; AMIE achieved 90% correct diagnosis, matched PCPs on differential quality.

-

Amazon launches Amazon Connect Health (agentic AI for healthcare). 5 AI agents for scheduling, documentation, coding at $99/mo per user; HIPAA-eligible.

-

Tampa General first to deploy Epic's 'Ask Art' AI tool. EHR-native generative AI is moving from pilots to frontline workflow deployment.

-

Maven Clinic expands AI with genAI agent on OpenAI, Google. Employers want scalable women's health navigation, signaling AI expansion into benefits and care coordination.

-

Rock Health: Share of US adults using AI for health questions doubled to 32% in one year. Rock Health 11th annual survey (8,000 adults): AI chatbot health use doubled from 16% to 32% YoY; 64% weekly users.

-

2,400 Kaiser Permanente mental health professionals strike over AI concerns. Northern CA Kaiser therapists struck March 18 over contract dispute and AI replacing clinical triage roles.

-

UMMC revenue dropped 20% in February due to ransomware cyberattack. University of Mississippi Medical Center lost $34.2M vs $194.1M budget after Feb 19 ransomware shut clinics for 9 days.

-

Medicare billing system software glitch delays millions in payments to rural hospitals. CMS system changeover caused enrollment data failures; Minnesota rural hospitals facing closure without payment resolution.

-

UnitedHealthcare launches 'Avery' AI assistant to simplify member care navigation. Avery available to 6.5M members now; UHC targets 20.5M commercial, Medicare, Medicaid members by end of 2026.

-

Latent raises $80M Series A for AI-powered medication authorization workflows. $80M from Spark Capital + Transformation Capital; now serves 50% of top 20 US health systems with prior auth AI.

-

Qualified Health raises $125M Series B for healthcare AI governance platform. $125M led by NEA; platform serves 500K+ users at health systems representing ~7% of US hospital revenue.

-

Optum expands Microsoft collab to add AI to claims platform. Deepening AI integration in claims processing; accelerating Optum Insight automation strategy.

-

RadNet acquires AI imaging firm Gleamer for €215M. €215M deal creates largest radiology AI solutions provider globally.

-

Procode AI launches as AI-native RCM rollup. AI-first strategy acquiring existing surgical billing businesses; new rollup model for RCM.

-

Suki and Optum Real collaborate on payment workflows. Linking documentation to claims in real time could reduce denials and admin burden.

-

Grow Therapy hits $3B valuation with $150M Series D. $1B+ revenue run rate; 7M visits in 2025; 26K providers; entering employer benefits channel.

-

Perplexity launches new AI health tool. Consumer AI is moving into regulated health use cases, intensifying privacy and accuracy questions.

-

Dr. Oz envisions agentic AI for every Medicare beneficiary. Signals CMS interest in consumer-facing AI, raising stakes for automation, accuracy, and governance.

-

Doctronic raises $40M to expand AI doctor platform. Doctronic raised $40M to expand AI clinical platform amid strong investor demand.

-

Turquoise Health raises $40M to scale price transparency tools. Turquoise Health raised $40M; building infrastructure for price transparency compliance.

-

Heidi Health launches first clinical AI hardware device. Heidi launched offline clinical recording hardware, expanding AI software into devices.

-

Stanford study: Clinicians can easily steer LLMs toward harmful diagnostic decisions. Stanford study: clinician input reduced AI diagnostic accuracy; safety concerns remain.

-

Nadia Care raises $12M; Malama Health adds $9.2M. Investors are backing Medicaid-focused maternal care models with doula support and measurable outcomes.

|

Provider Financial Performance, Labor, and Care Delivery Model Shift |

-

Kaufman Hall: hospital expenses, bad debt won't ease in 2026. Persistent labor and uncompensated-care pressures suggest margin recovery remains fragile across hospitals.

-

UnitedHealth caps raises at 2%, plans layoffs (Bloomberg). 0-2% raises based on performance; first revenue decline since 1980s projected for 2026.

-

Mayo Clinic posts 6.8% margin on $21.5B revenue in 2025. Elite margin performance; $21.5B total revenue underscores financial strength of top-tier AMCs.

-

Cleveland Clinic triples operating margin to ~5%. Dramatic turnaround in operating performance at one of the nation's top AMCs.

-

12 AMC margins compared: -2.6% to 10.7% spread. Massive 13+ point margin spread across academic systems reveals deepening haves vs. have-nots.

-

Trilliant: patient care is less than half of hospital revenue. Hospitals increasingly rely on nonclinical revenue streams, exposing complexity in health system economics.

-

28 health systems cutting jobs or scaling back care in 2026. Widespread downsizing across hospital sector; layoffs, service line closures, department cuts.

-

HCA vs. Ascension competing head-to-head in Tennessee with ER builds. Two major systems racing to build freestanding ERs in Nashville's high-growth corridor.

-

'Death spiral' facing some Pennsylvania hospitals. Structural financial deterioration at multiple PA hospitals driven by payer mix and cost pressures.

-

Illinois hospital (West Suburban Medical Center) halts patient care amid payroll and billing crisis. Oak Park, IL hospital suspended patient care after EMR failure caused 90% revenue loss for 12 months.

-

Record Match Day 2026: 44,344 residency positions offered. Training slots keep growing, but demand still outpaces supply in key specialties.

-

Ardent Health net income falls to $135.8M in 2025. Publicly traded operator earnings decline; part of mixed Q4 picture across for-profits.

-

Corewell Health posts 1.6% operating margin, $17.6B revenue. Thin margin on massive revenue base; illustrates nonprofit margin compression at scale.

-

Surgery Partners earnings miss tied to surgical hospitals. Surgical hospital segment underperformance vs. ASC growth; mixed picture for diversified operator.

-

Bon Secours grows operating income and margin in 2025. Better margins suggest disciplined operators can recover, but sectorwide improvement remains uneven.

-

2,400 Kaiser Permanente mental health professionals strike over AI concerns. Northern CA Kaiser therapists struck March 18 over contract dispute and AI replacing clinical triage roles.

-

Jefferson Health hit with $108M malpractice verdict. Nuclear verdicts raise liability costs, accelerating malpractice fears and financial strain for systems.

-

Grady CEO to retire as $1B medical campus clears hurdle. Leadership succession coincides with capital expansion, showing long-term bets on safety-net growth.

-

Healthcare bankruptcies declined 21% in 2025, but hospital filings jumped 60%. Gibbins Advisors: Bankruptcies down overall, but hospital filings rising; distress persists.

-

Mental health spending growth driven by case volume, not cost. Spending growth reflects more people seeking care, not necessarily worsening unit prices.

-

PeaceHealth sued by ED physicians over ApolloMD staffing contract. Physicians sued PeaceHealth over ED outsourcing; autonomy and quality concerns persist.

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Blake |

|

|

{if profile.vars.board_room_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Hospitalogy Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}{if !profile.vars.board_room_user_fitness && profile.vars.board_room_user_fitness != false}I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

|

|

{/if}

Get your brand in front of 67,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|