{if hosp_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy. |

|

|

{/if}{if profile.vars.hew_transition}

A reminder: You’re receiving this because you were previously subscribed to HealthExecWire. Hope you enjoy. | |

|

{/if}

Happy Tuesday, Hospitalogists,

Today, we’re talking about whether payor-provider relationships are still in vogue, MedPAC’s report to Congress, and Omada Health’s bet on building a real between-visit care engine at scale. Enjoy!

P.S. Last call for my community event this Friday - a roundtable discussion talking about the current state of healthcare finance. Don’t miss it. Register now. |

Was this email forwarded to you?

|

|

|

Join me for my first virtual event of the year! The great folks at Lumeris and I will be talking about all things agentic AI and primary care in health systems.

Primary care is becoming the most strategic asset in a health system’s portfolio. And AI is about to make it doubly so.

This virtual event aims to rethink primary care — not as a subsidy, but as the front line of patient relationships, revenue, and AI strategy. We'll get into: - What an actual agentic AI strategy looks like in primary care

- Which workflows are ready for disruption now

-

How to tell the difference between a real platform play and a solution dressed up in AI language

- How leading organizations are turning primary care into an intelligence model, not just a staffing one

If your health system treats primary care as a cost center, it’s time to switch gears. You'll leave with a framework you can bring back to your team. Save your spot here! |

|

|

Are Payor-Provider Relationships Still In Vogue? |

|

|

Do you think payor-provider partnerships are still in vogue or are they falling apart? Honestly, after hearing different arguments internally, I'm curious to get some others' perspectives on why they feel one way or another. |

|

|

THE MISALIGNED INCENTIVES TAKE |

Anonymous

“Most partnerships were sold as alignment plays, but in reality they’ve struggled under misaligned incentives and asymmetric power. Providers took on operational risk without real control, while payors kept the data, the adjudication logic, and the downside protection. My thoughts, but with a distinction: -

Traditional JV-style partnerships or MA co-branded plans? Momentum has slowed. Rising utilization, tighter margins, and regulatory scrutiny have exposed how fragile those arrangements are.

-

More targeted, transactional collaborations? Very much alive if you're thinking in terms of shared data infrastructure, delegated risk in narrow populations, or payor-funded enablement tied to clear ROI.

I definitely think the era of ‘let’s partner and figure it out later’ is over. What’s replacing it are much more conditional, data-driven relationships where both sides know exactly who owns the risk, the margin, and the decision-making.

If a partnership doesn’t materially change who controls utilization, pricing, or capital allocation, it’s probably just a nicer-looking contract, not a partnership.” |

THE IDEA VS EXECUTION TAKE |

Anonymous “They’re not falling apart, but they’re definitely not having the moment people promised five years ago. The idea of payor-provider partnerships is still in vogue. The execution is where things keep breaking down.” |

THE FISCAL CONDITIONS TAKE |

Ann Kempski - Consultant

“If fiscal conditions on Medicaid, Medicare remain tight, it of course adds more tension in payor-provider partnerships. Both parties need to take the long view and build long term contractual relationships because it's during tough times when integrated care can differentiate itself. I think it's harder for publicly traded payors to take the long view on these relationships. I have no inside info, but from the outside, a relationship that looks pretty win-win-win to me is Oschner and Humana. They've been at it a long time and both seem committed to sharing some risk.”

Hospitalogy members can join this discussion here. Not a member yet? Apply to join here. |

|

|

MedPAC’s March 2026 Report to Congress |

MedPAC released its March 2026 Report to Congress: Medicare Payment Policy. At 671 pages, it's not exactly beach reading. But buried inside is a detailed blueprint of where Medicare's money is going, where it's being wasted, and, critically, what MedPAC thinks Congress should do about it. The full report is worth sharing with your finance, strategy, and policy teams. Some key takeaways:

|

-

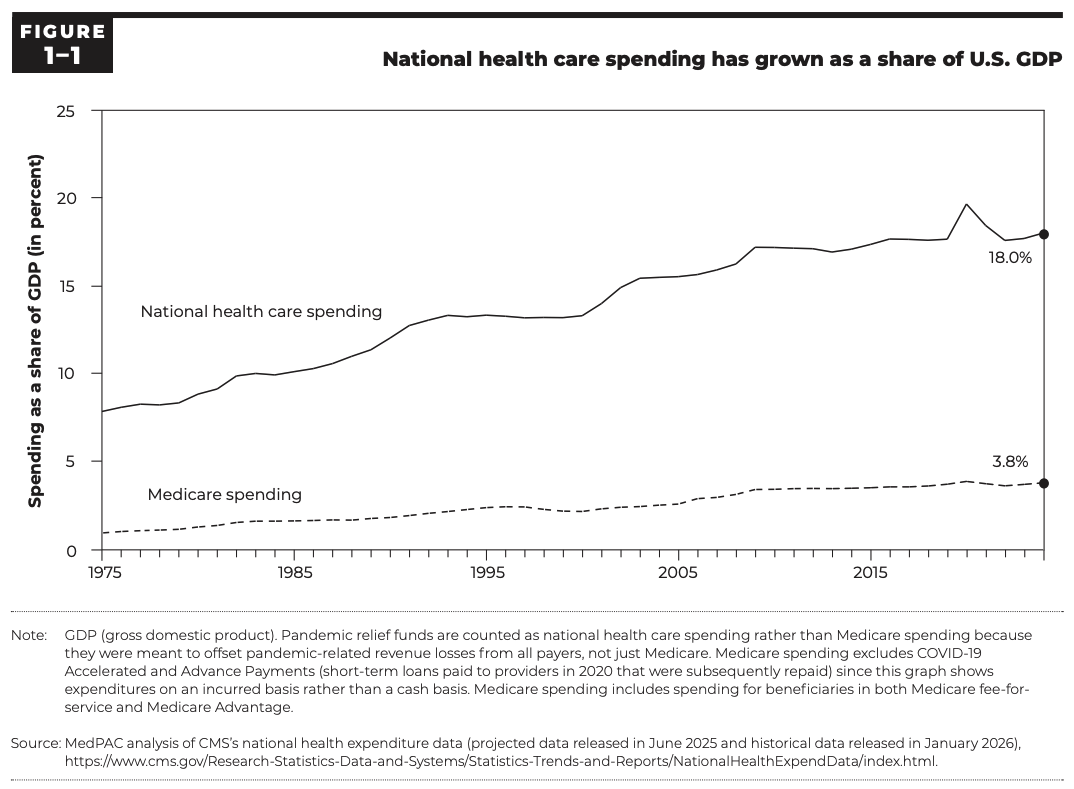

National healthcare spending grew 7% in both 2023 and 2024, reaching $5.3T, 18% of GDP. Medicare's growth outpaced even that, rising 9% in 2023 and 8% in 2024, landing at $1.1T in total Medicare spending, 21% of national healthcare spending and 3.8% of GDP.

-

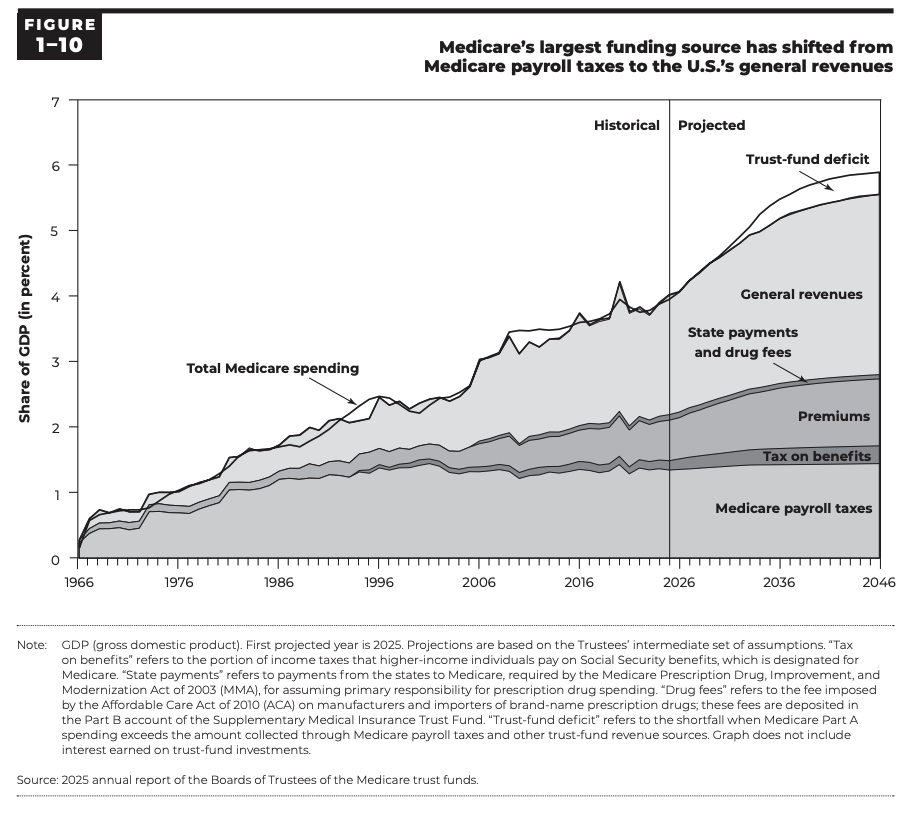

By the mid-2030s, Medicare spending is projected to double in nominal terms and exceed 5% of GDP.

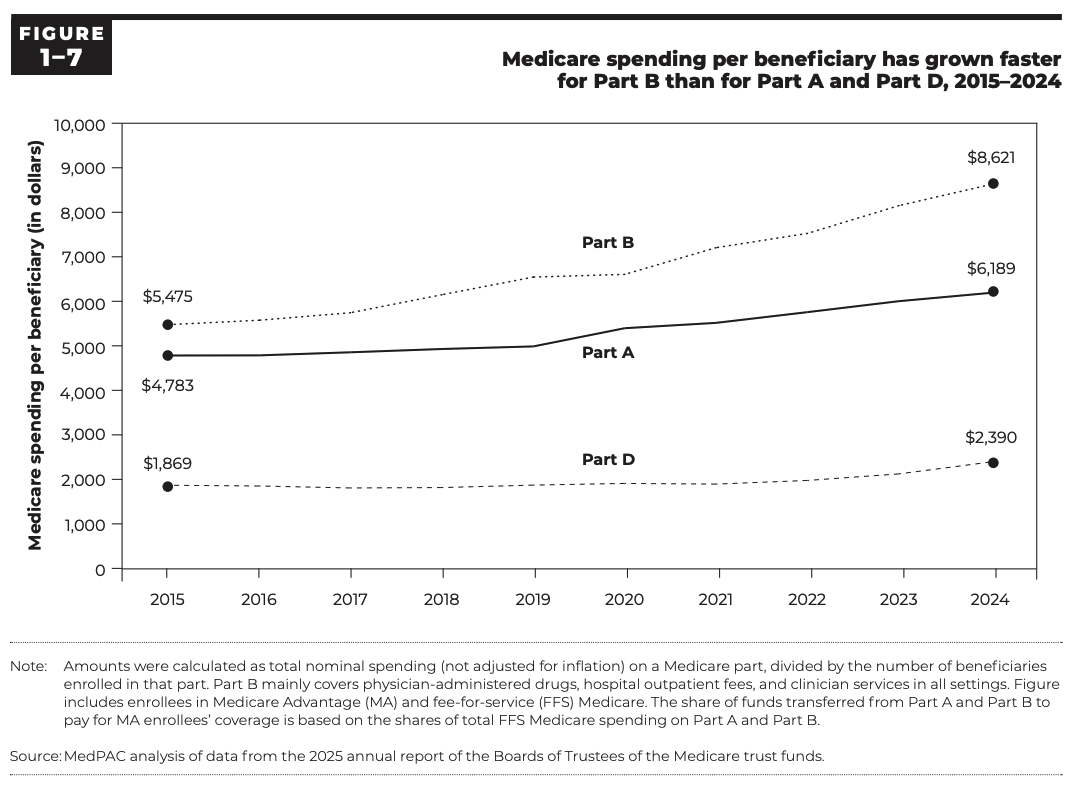

- In 2015, Part A constituted 43% of Medicare spending and Part B was 45%. By 2024, Part A had dropped to 38% while Part B climbed to 49%.

|

- ACHs: no change in law.

-

SNFs: reduce 4%.

- Home health agencies: reduce 7%.

- Inpatient rehabilitation facilities: reduce 7%.

- Outpatient dialysis: no update.

- Hospice: no update.

-

ASCs: MedPAC continues its recommendation to require ASC cost reporting.

- MSNI: implement the MSNI (originally proposed in March 2023), adding $1B to the MSNI pool.

-

Site-neutral payments: Extend site-neutral policies to on-campus clinic services and further expand off-campus outpatient site-neutral rules.

- Physicians and other health professionals: increase above current law. MedPAC is recommending a permanent update, baked into future rate bases, rather than another one-time patch.

|

-

Medicare will spend an estimated 14% more ($76B) on MA enrollees than it would if those beneficiaries were in FFS. That's down from a projected 20% overpayment in 2025, primarily because the V28 risk model phase-in is complete, but "down from 20%" is not a fix.

-

55% of eligible Medicare beneficiaries are now enrolled in MA (34.9M people, covered through 5,492 plan options from 164 organizations). Medicare's payments to MA plans are projected to hit $615B in 2026, including an average of $2,660 PBPY in rebate payments, rebates that have more than doubled since 2018 and now represent 15% of total MA payments.

-

8 MA organizations had average coding intensity more than 20% above FFS levels in 2024. 8 of the 10 largest MA organizations had coding intensity 5 or more percentage points above CMS's adjustment.

-

The higher MA payments increase Part B premiums for all Medicare beneficiaries, including those in FFS who see none of the supplemental benefits those extra dollars fund. MedPAC estimates that Part B premium payments will be about $11B higher in 2026 (~$175 PBPY) because of higher payments to MA plans.

-

MedPAC's reform agenda for MA centers on 5 priorities:

- reduce overall payment levels by addressing coding intensity and favorable selection,

-

reform the quality-bonus program (currently adding ~$16B to MA payments in 2026),

- restructure the benchmark system to eliminate inequities and "cliff effects,"

- better protect beneficiaries navigating plan transitions and network disruptions, and

- require comprehensive encounter data so policymakers can actually assess how MA dollars are being spent.

|

The Year of the G's: Sean Duffy on GLPs, GPTs, and Chronic Care's Inflection Point |

This is one of the conversations I’ve been most looking forward to sharing on the podcast. I sat down with Sean Duffy, CEO and co-founder of Omada Health, fresh off their first JP Morgan conference as a public company.

We got into everything — what it takes to build a real between-visit care engine at scale, the behavioral science of why pamphlets don't work, why Omada is now prescribing GLP-1s, how 9+ AI models are already live in their care workflows, and why engagement (not efficiency) is the real margin story. Listen to the full episode (Apple | Spotify) to hear why: - The “visit model” is structurally broken for chronic disease, and what Omada is doing about it

- GLP-1s don’t work like a “vaccine moment”; behavior and psychology still decide outcomes

-

AI can expand margins, but there’s a bigger unlock

- The moat is personalization: making a 23-year-old in Seattle and a grandma in Boca both feel like the program was built for them

Subscribe to my Claims Denied podcast! |

|

|

Resource: A new white paper explores how integrated data orchestration is amplifying virtual care performance by driving results like real-time assignment routing, 22% fewer physician hours, and greater program impact.*

Read: This article from Kaufman Hall examines the shifting economics of academic medicine, including results from their examination of funds flow data from 61 academic medical centers.

*This resource is brought to you by one of my brand partners who help make this newsletter possible! |

|

|

That’s all for this Tuesday. I would love to know your thoughts! Just hit reply to this email.

– Blake |

|

|

{if profile.vars.board_room_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Hospitalogy Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}{if !profile.vars.board_room_user_fitness && profile.vars.board_room_user_fitness != false}I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

|

|

{/if}

Get your brand in front of 67,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|