{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Monday, Fintech Takers!

I hope you had a wonderful weekend. Mine was mostly kids and college basketball. Peak living, basically. Speaking of which, here’s a trivia question for you (the answer to which can be found at the end of this newsletter): What is a Billiken?

- Alex

P.S: Cash flow data is one of the most underutilized levers for reducing credit losses — and the lenders figuring out the sequencing now are pulling ahead. Join me on Weds to get a practical roadmap for getting there. Happening in 2 days — save your spot here!

|

Was this email forwarded to you? |

|

|

Women by the Sea (1885–1897) by Jan Toorop. |

|

|

#1: Confidence in the Face of Uncertainty |

Jeff Kauflin at Forbes wrote an excellent article on the growing division between fintech ‘haves’ and ‘have-nots’. He uses Stripe as his first example:

Take San Francisco payments company Stripe, which helps millions of merchants accept credit cards, process stablecoin transactions and manage billing tasks. In 2025, it brought in $6.9 billion of net revenue and $1.2 billion of earnings before factoring in interest, tax, depreciation and amortization expenses, according to a person familiar with its finances. Revenues were up more than 30% from 2024.

That’s world-class scale and growth, but its recent valuation of $159 billion, which has afforded each of the Collison brothers a $17.5 billion fortune, means its private backers think it’s worth nearly five times Adyen, a Dutch fintech and close competitor. Unlike Stripe, Adyen is publicly traded. It processed $1.6 trillion in payments last year compared with Stripe’s $1.9 trillion. Stripe loyalists will point out that it has more business lines than Adyen and is growing faster off of a larger base. But the chances that Stripe could maintain a $159 billion valuation if it went public today are slim. Public investors value e-commerce platform Shopify at $165 billion, and it grew nearly as fast as Stripe last year and had more than double the profits. A Stripe spokesperson declined to comment.

|

As always, I am extremely jealous of Jeff’s ability to identify and report on important macro stories in fintech before they become mainstream.

This is a trend that I’ve been thinking about for a while, especially regarding Ramp, the late-stage fintech company that seems completely immune to the physical laws of the universe. Ramp is the second example Jeff cites in his article:

New York-based corporate-card company Ramp is another “have” among fintechs that carries a head-scratching price tag. In September 2025, it announced $1 billion in annualized gross revenue and two months later, fetched a $32 billion valuation. Here’s what many observers don’t realize: its gross sales figure doesn’t subtract out the card-swipe interchange fees and rewards that Ramp gives back to banks, other partners and customers. So Ramp’s net revenue, the top-line sales metric reported by most publicly traded payments companies, is likely at least 40% lower than its gross revenue. That means its net-revenue valuation multiple was probably around 50 (or higher) as of last fall, a level reminiscent of fintech’s 2021 bubble days. Ramp’s head of communications Lindsay McKinley declined to comment on the company’s net revenue but said it’s growing by more than 100% annually and is cash flow positive.

Ramp’s corporate-card rival Brex had 30% less revenue than Ramp as of September 2025. Four months later, in January 2026, Brex was valued at $5.15 billion when Capital One announced it would acquire it. Even with its impressive growth, is Ramp worth six times Brex? That’s exactly the right question. Why was Ramp able to raise [checks notes] more than $1 billion last year, while Brex — a slightly smaller and less successful but very similar company — was acquired by Capital One for $5.15 billion?

I might be completely off base here, but my sense is that Brex didn’t have much more room to run as a private company. There wasn’t a lot of demand for new Brex equity, especially at a higher valuation, which is probably why the company jumped at the chance to be acquired by Capital One when the bank came knocking. (The deal closed in 40 days, which speaks to how motivated both parties were to do the deal.)

What makes Ramp different? Why do investors like Keith Rabois seem to have an unquenchable thirst to keep giving it more money? Why does it seem possible, at least at this moment, that Ramp and Stripe might never go public? As great as the businesses themselves are, I think the answer is mostly about vibes. Both companies exude a general sense of hypercompetence, which gives investors the confidence that no matter what is thrown at them, they will figure it out. And confidence in the face of extreme uncertainty has become a very desirable feeling for investors over the last 3-4 years. Here’s Jeff again: Steve McLaughlin, the founder and CEO of fintech-focused investment bank FT Partners, says that over the past couple of months, hopes and concerns about AI “have gotten more pronounced than ever, and it's creating a fog for both investors and companies to determine the opportunities and risks.”

One circumstance helping drive the continued rise of fintechs’ haves is the companies’ skillfully crafted narratives around artificial intelligence. Stripe and Ramp have convinced investors that the AI wave will boost their business, continuously blasting out press releases about AI agents and other AI-centric features. Jeff also gives an interesting counter-example to punctuate his point:

Klarna, the publicly traded buy-now, pay-later company based in Stockholm, has tried to do the same, with billionaire cofounder and CEO Sebastian Siemiatkowski even saying his company is already using AI to replace enterprise software from tech giant Salesforce. His public-market investors have remained skeptical. Klarna is now trading at a $6 billion market value, down significantly from both its IPO price and 2021 private-market valuation of $46 billion.

That’s a tough one to parse. Are investors lukewarm on Klarna because it can’t tell a coherent story about AI? (The AI storytelling from Klarna has been abysmally bad.) Is it because Klarna is a public company, and public market investors are brutally realistic? (According to Forbes, of the 11 fintechs that went public last year, only three are trading above their IPO price.) Or maybe it’s a bit of both? Maybe Klarna had to become a public company and a target for harsher public investor scrutiny because private market investors thought it couldn’t surf the emerging technology waves as well as the Stripes and Ramps of the world? I don’t know.

Regardless, it’s a weird situation to find ourselves in.

The manic enthusiasm reminds me of the fintech bubble of 2021, but the difference this time is that the investment isn’t being spread out. Even the most promising fintech startups, with well-rehearsed AI stories, are difficult for investors to buy into when the fog of uncertainty is so thick. Instead, many investors seem to think it’s better to just keep doubling down on the biggest bets that they and their peers have already made and hoping they’re the right ones. |

Fuse, a fintech infrastructure company, raised some money:

In 2023, after three years of building an automotive lending startup, Fuse co-founders Andres Klaric and Marc Escapa realized that LLMs could modernize something even more significant: the loan origination system (LOS), which is the backbone of the lending industry. Frustrated by the limitations of legacy software, Klaric and Escapa pivoted their business to build Fuse, an AI-native LOS.

On Monday, Fuse announced that it has raised a $25 million Series A led by Footwork, Primary Venture Partners, NextView Ventures, and Commerce Ventures. |

Despite my concerns about a more concentrated fintech bubble, Fuse managed to raise a very healthy Series A round. Congrats to them! I’m sure putting AI at the center of the product helped with the fundraising, but I will say that I am fairly impressed with how Fuse is positioning the product and taking it to market. Here are the Cliff Notes: - While the company appears to work with a range of different types of lenders, credit unions are its primary focus.

-

From a product perspective, it claims to support a wide range of loan types, from auto (where the founders got their start) to unsecured consumer lending to small business and commercial.

-

Fuse emphasizes the importance of automation. It uses an AI copilot to highlight where application processing slows down and what to automate next. It even contractually commits to meeting with clients every 2 weeks throughout the contract term to surface automation opportunities and ties its account managers’ bonus pay to their clients’ automation lift.

-

Fuse also offers something called a “rescue fund,” which is essentially a pot of money that the company has set aside to subsidize the cost of its software for clients that commit to Fuse, for the duration of their contracts with their legacy LOS providers.

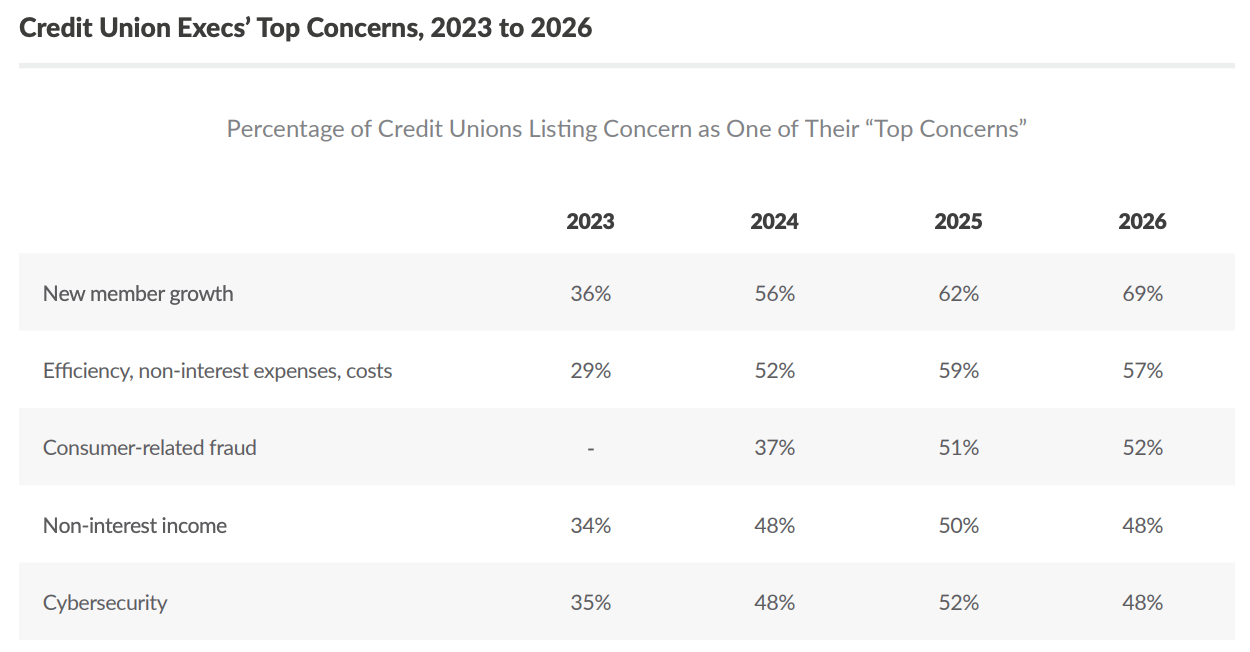

These points of emphasis suggest to me that Fuse has a deep understanding of its target market, and a glance through the most recent edition of Cornerstone Advisors’ always-excellent What’s Going On In Banking report supports this conclusion. Helping credit unions grow in an automated way that prioritizes efficiency? Take a look at credit unions’ top concerns for 2026: |

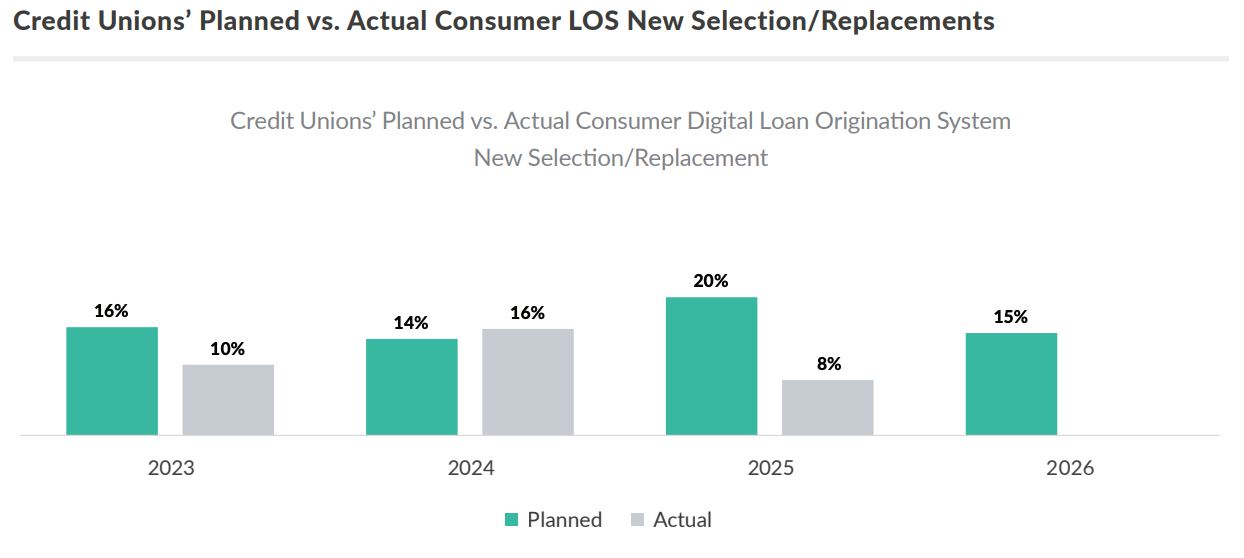

A rescue fund for making the actual process of switching LOS providers more realistic and achievable? Take a look at the discrepancy between credit unions’ planned LOS replacements versus actual LOS replacements: |

Fuse seems to be focused on the right challenges. My only two concerns are: -

According to Cornerstone, after auto lending (which Fuse is very well-positioned for, thanks to its founders’ prior experiences), home equity and mortgage are the two highest lending priorities for credit unions in 2026. These are both product areas where LLMs and agentic AI can (theoretically) provide a huge lift, but they are not product areas where Fuse appears to be active.

-

Given its sharpened focus on credit unions, it would have made sense (in a perfect world) for Fuse to have raised at least a bit of its funding from an investment fund backed by credit unions, such as TruStage Ventures or Curql. When pursuing the long tail of the market (there are more than 4,000 credit unions in the U.S., most of them very small), it helps to be able to tap into existing relationships.

|

#3: Credit Score Monitoring Needs to Learn From Agentic Commerce |

Experian launched a credit score benchmarking tool inside ChatGPT:

Experian, the data and technology company, today announced the launch of the UK’s first ever credit score app within ChatGPT apps – introducing a new postcode based credit score comparison tool that brings Experian’s trusted data directly into one of the world’s most widely used AI platforms. The tool uses aggregated and anonymised Experian Credit Score data, the UK’s most trusted score, to show how typical scores compare across postcode areas and age groups. In a few seconds, consumers can see local and demographic score averages, providing helpful context as part of everyday financial education. |

This is a classic incumbent half-step: present in the interface, but not nearly as useful as it could be.

The tool doesn’t give you your credit score. It doesn’t help you improve it. It doesn’t enable you to take action. It simply shows how you compare to others your age and in your geographic region, and then pushes you back to Experian’s own properties to do anything meaningful. That’s not integration. That’s lead gen.

The deeper issue is that Experian is optimizing for traffic preservation, not user outcomes. Credit score monitoring has always been an ad-driven business: give away the score, capture attention, and monetize through credit card and loan offers. The value is in owning the funnel. AI-native distribution breaks that model.

In an AI-driven world, users won’t tolerate being bounced between surfaces. If I’m asking ChatGPT about my credit score, I should be able to retrieve my real score, understand what’s impacting it, get personalized recommendations, and compare and apply for products — all in one flow. That’s already the direction of agentic commerce. Companies building in that space assume the transaction will happen inside the AI, not after a redirect. They’re building the infrastructure (payments, identity, fulfillment) to support that.

Credit score monitoring should follow the same path. It’s arguably even more suited to it. The underlying data is highly structured, the decisions are repeatable, and the user journey is already linear — check your score, understand what’s driving it, improve it, then shop for and apply to products. That kind of workflow maps cleanly to an AI-native, end-to-end experience.

But incumbents have no incentive to go there. Embedding the full experience inside AI would mean giving up direct traffic, compressing their ad inventory, and weakening their control over distribution. For companies whose business models depend on owning the funnel, that’s just not an option. So instead, you get tools like this: informational, but inert.

The opportunity is obvious. Someone will build a fully agent-native credit stack, where monitoring, advice, and product selection live entirely inside AI interfaces.

And when that happens, the companies that optimized for keeping users on their site instead of meeting them where they are will be in a bad spot. |

|

|

2 READING RECOMMENDATIONS |

I write about agentic commerce quite a bit, but so far, I’ve just been scratching the surface. Simon goes much deeper in this article. Thought-provoking stuff! |

Great article (and a perfect title). Prediction markets in 2026 feel like a very instructive reflection of our society: who we trust and what we value. |

There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network. What conferences/events will you be attending this spring?

My spring travel schedule is basically set at this point, but I’m always curious to hear where others are going. Let me know!

If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network! |

The Billiken is a charm doll created by an American art teacher and illustrator, Florence Pretz of Kansas City, Missouri, who is said to have seen the mysterious figure in a dream. In 1908, she obtained a design patent on the ornamental design of the Billiken — a monkey-like creature with pointed ears, a mischievous smile, and a tuft of hair on his pointed head. The Billiken was designed to symbolize "things as they ought to be," and it was thought that buying a Billiken doll would bring the purchaser luck, but receiving one as a gift would bring better luck.

This is relevant in 2026 because the Billiken is the mascot of St. Louis University, and the St. Louis men’s basketball team made this year’s March Madness tournament (they lost in the second round to Michigan). Why is St. Louis University’s mascot the Billiken? Excellent question. An early St. Louis University football coach, John R. Bender, was the inspiration. During the 1911 season, local sportswriters commented that Bender bore an uncanny resemblance to the Billiken charm doll. His squad became known as "Bender's Billikens," and the name stuck.

Here’s coach Bender and a Billiken side by side: |

Brutal. Just brutal. Those local sportswriters did him wrong. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network

|

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 60,900+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|