{if hosp_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy.

|

|

|

{/if}{if profile.vars.hew_transition}

A reminder: You’re receiving this because you were previously subscribed to HealthExecWire. Hope you enjoy. | |

|

{/if}

Happy Thursday Hospitalogists, and March Madness to those who celebrate. I know most of us are “working” today when in reality we have the quad box Youtube TV setup going praying for Siena to pull off the upset against Duke (so close…)

Don’t forget to add your bracket to the Hospitalogy group on ESPN here. I think you can still join as long as you made a bracket through ESPN beforehand. Winner gets a random shoutout of their anonymous username! We’ve still got 2 perfect brackets in the thing whereas I’m already in the 26th percentile…classic. You guys really shouldn’t listen to me for anything predictions-based. You’ve been warned.

Today is a quick breakdown of Sutter and Allina - a RETURN of the cross-market mega merger! Who would have thought! Let’s dive in. |

Was this email forwarded to you? |

|

|

Going deeper on an interesting topic, theme, or trend |

Return of the Cross-Market Mega Merger |

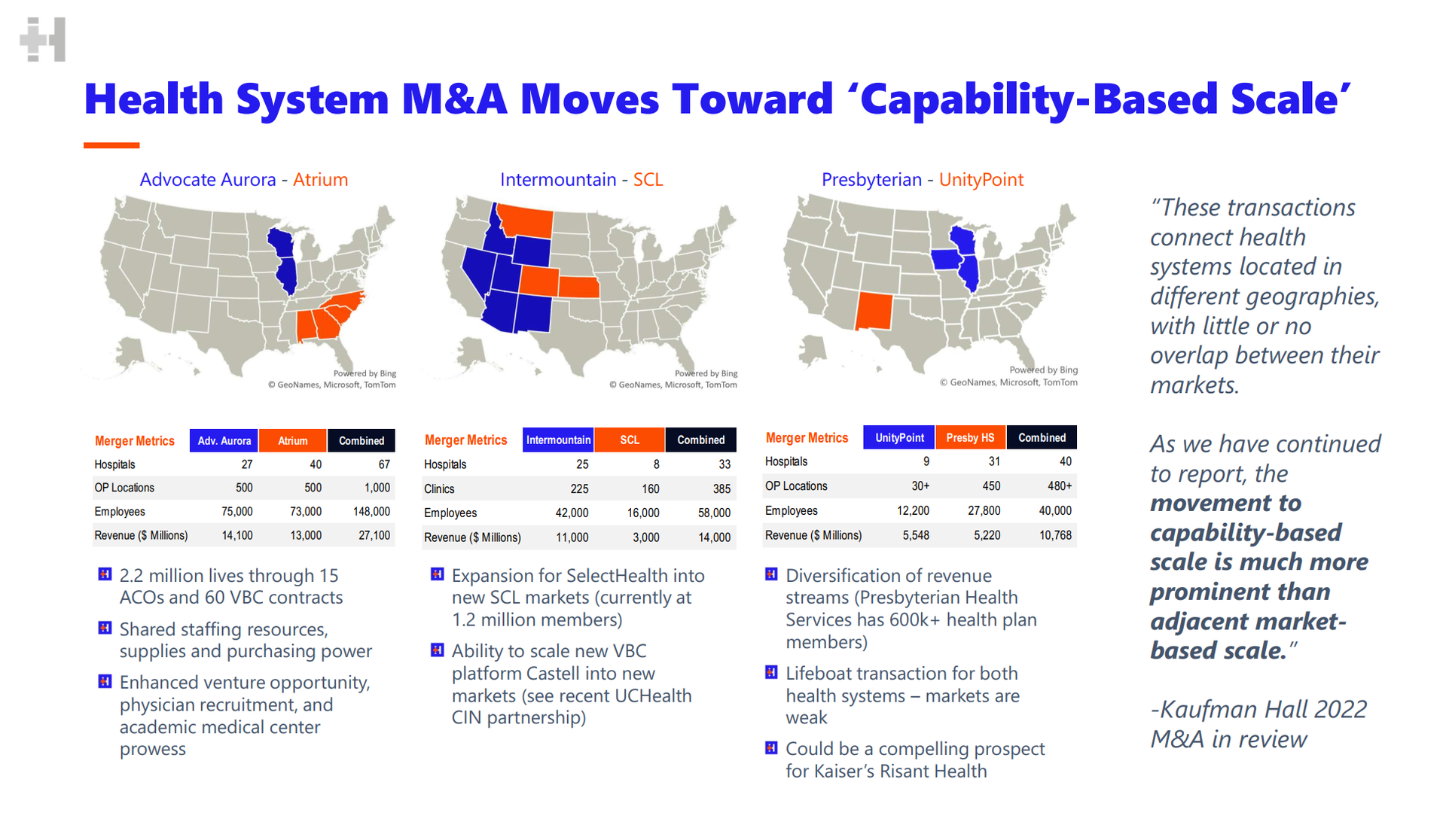

Eons ago - that is, back in 2022 - several health systems decided to embark on a new trend of merging despite disparate geographies. North Carolina and Illinois, for instance. There wasn’t a clear initial understanding of the benefit of doing so, despite scale for scale’s sake. But hey, most of the time in healthcare, bigger is better and you can find ways to make it work. |

(A slide I made back in 2022. Note that the Presbyterian-UnityPoint merger was called off)

Welp, Sutter Health and Allina Health decided to reignite this trend, announcing their intention to merge into what would create a $25.9B health system spanning Northern California, Minnesota, and western Wisconsin. |

Instant Analysis: I’m doing further research and analysis on the deal, but what I can tell you is that large hospital M&A has been all but dead (mostly divestitures and portfolio resizing), and I can’t believe it revived in this fashion. During peak post-pandemic times, as mentioned, we saw a plethora of ‘cross-market’ mega merger deals - deals in which the synergies and expected benefits are based on capabilities rather than raw market strength. Health systems in non-adjacent markets combining forces to develop better purchasing power and other ‘national’ economies of scale.

|

How might this benefit Allina and Sutter? It’s a fun thought experiment. Take for one, the fact that Allina holds a 30%+ inpatient market share but still lost money on operations in 2025 AND 2024, and was downgraded with a negative outlook because of persistent losses. So maybe Allina has the inpatient prowess but doesn’t hold the ambulatory assets needed to compete in the new age health system game. Because the health system has been losing money on operations, maybe they’re looking for a capital partner and more sophisticated health system to help finance and guide them through the next journey of health system transformation. Maybe some of this deal is still a simple arbitrage game where Allina can refinance bonds at better Sutter rates (pure conjecture). Capabilities I can think of that are worth mentioning, and incentive for merging, include:

- Ability to combine expertise and consolidate leadership

- (Potentially) better financing terms or other balance sheet mechanisms

-

Ability to scale incubated and/or owned AI-enabled digital health solutions or companies across a $26B enterprise and test or pilot across different markets

- Combined purchasing power and recruitment / retention capabilities

-

Other considerations including things like 340B or supplemental payments eligibility

- Creation of national service lines and standardization

|

Bigger picture: Along with Advocate-Atrium, SCL-Intermountain, or even Ascension-AmSurg, health systems more than anything are looking to survive, and by combining forces and cross-subsidizing winning and losing markets, capability-based scale allows them to stay in the game and remain competitive against payors and disruptors. |

Final point is on regulatory review. What state reviews this? Who has the final say? These deals are so weird structurally in being across multiple markets that it’s mighty hard (I imagine) to prove anything from an anticompetitive standpoint, similarly to vertical integration deals. For this reason alone we should expect to see it go through (if they still want it to at that point).

How else might Sutter and Allina benefit from this deal? Hit me with your thoughts. It feels like I am missing something big, but maybe it’s as simple as what I’ve laid out. More thoughts and analysis on this guy coming next week. |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Blake |

|

|

{if profile.vars.board_room_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Hospitalogy Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}{if !profile.vars.board_room_user_fitness && profile.vars.board_room_user_fitness != false}I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

|

|

{/if}

Get your brand in front of 67,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|