{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}

Happy Monday, Fintech Takers!

I hope you had a nice weekend and enjoyed The Oscars/March Madness Selection Sunday/[insert fun and relaxing activity here].

My third and (for the moment) final trip to D.C. is this week. I’ll be moderating a panel at the FDX Global Summit on liability and risk management in open finance, which is a topic I’ve been wanting to dive deeper into for a while.

Should be fun! - Alex |

Was this email forwarded to you? |

| |

Electric Discharges (1909), a collection of colorful and different drawings of electrical currents models. |

|

|

#1: If you don’t own distribution, you don’t own anything. |

Upstart, a fintech lender, has applied for a national bank charter:

The firm has applied to the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC) to establish an insured national bank, Upstart Bank.

Founded in 2012 by a group of former Googlers, Upstart operates an AI lending marketplace, connecting millions of consumers to more than 100 banks and credit unions that use its models and cloud applications to deliver credit products.

The firm enables personal loans, automotive retail and refinance loans, home equity lines of credit, and will soon offer a revolving line of credit, with more than 90% fully automated.

Upstart says that a bank charter will allow it to reduce operational, regulatory, and financial costs and complexity for itself as well as for its third-party capital sources. Annie Delgado, Upstart’s chief risk officer, is the proposed CEO of the bank. |

For Upstart, this move makes a ton of sense. Acquiring a bank charter usually works best if you’ve cracked the hard, profitable part of banking (lending money) first, and then you work on funding that part of the business with customer deposits. This is what LendingClub and SoFi did, and it’s what Affirm is doing now. For Upstart’s 100+ bank and credit union partners, this move hurts.

For years, Upstart went out of its way to tell the market that it was not just another fintech renting a bank charter. In 2019, the company wrote that it would maximize its impact “not by becoming a new-age bank, but by powering banks looking to thrive,” and said the “Powered by Upstart” model let banks “enforce their own credit policy and lending terms” while using Upstart’s risk models and automation. The company reinforced this message in its 2021 S-1, describing itself as a platform that “connects” borrower demand to “our network of Upstart AI-enabled bank partners.”

That is a very different framing from the classic fintech lender model, where the bank is mostly there to originate loans while the fintech company owns the experience, economics, and underwriting logic. The rent-a-charter model was about using a sponsor bank as regulatory infrastructure. Upstart’s model was about making banks and credit unions better lenders. Upstart’s S-1 claimed that bank partners benefited from “access to new customers, lower fraud and loss rates, and increased automation,” while the company’s current partner testimonials and press materials use similar language about helping institutions “grow” portfolios, “attract new members,” and serve more borrowers digitally.

And now Upstart is becoming a bank.

It says that it will still sell “the overwhelming majority of loans” to lending partners and other capital providers, and its press release claims that “banks, credit unions, and institutional funds will continue to be the capital source for the vast majority” of originations. It has also said explicitly that it is “not seeking to compete with our depository partners for local customer deposits and checking accounts.”

But if you were one of the company’s bank or credit union partners, would you believe them?

I’m sure Upstart will still sell a lot of its loans (many banks do the same), but it absolutely will compete with those partners for deposits (just by offering deposit products over the internet, it will be competing with them), and it will have the ability, whenever it wants, to retain any of the loans it originates on its own book. Much like what we’re seeing right now in BaaS, with large fintech companies moving away from their partner banks and acquiring their own charters, the reality in any bank-fintech partnership is that if you don’t own distribution, you don’t own anything. |

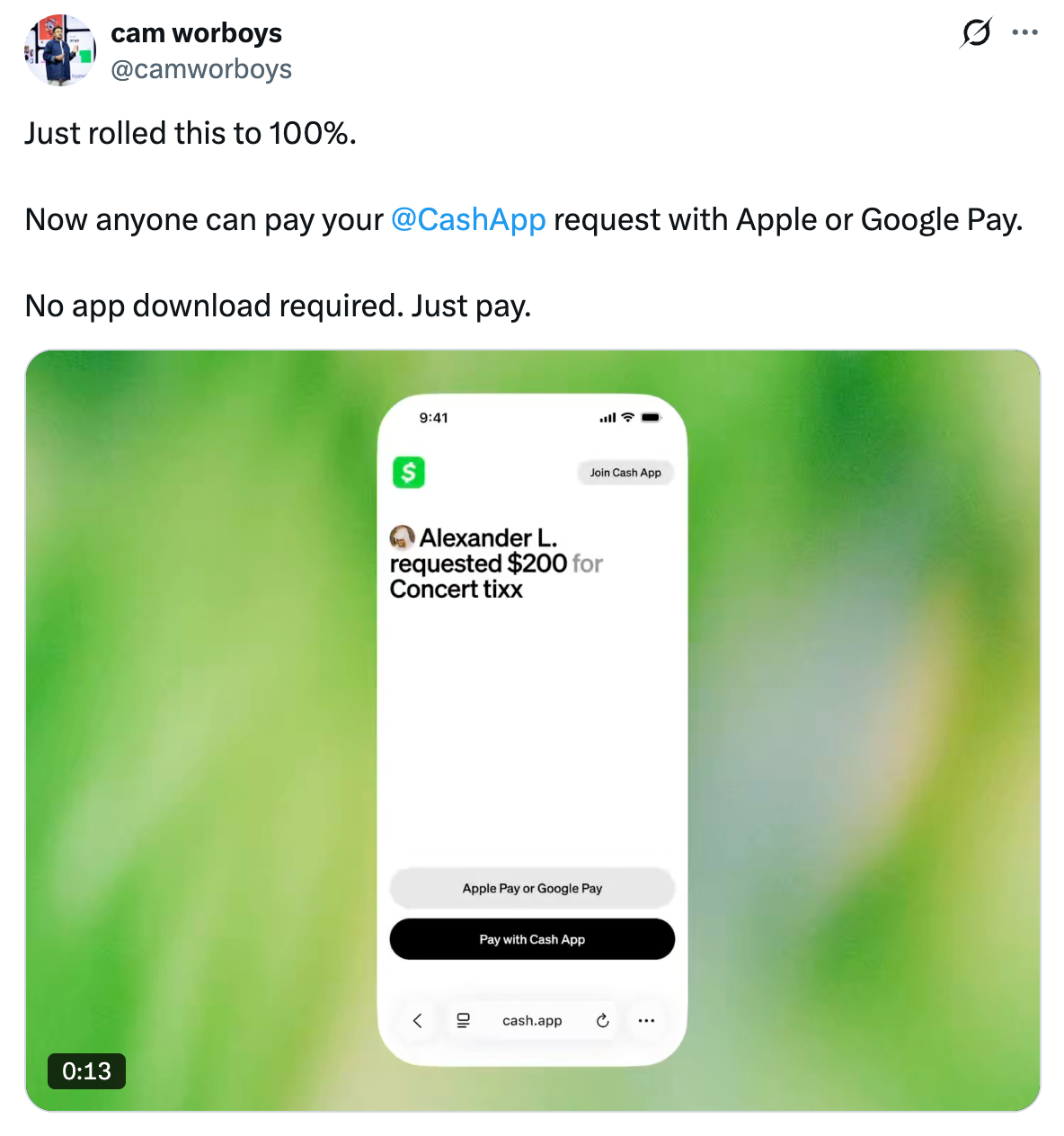

#2: Cash App’s Open Loop Payments Pivot |

Cash App just gave up one of the best growth hacks in fintech. For most of the past decade, P2P payments doubled as an organic user acquisition engine. Cash App and Venmo were built as closed-loop networks: if you wanted to pay someone, they usually had to download the app and become a user to complete the transaction. That’s why Venmo and Cash App had famously low customer acquisition costs. P2P payments weren’t designed as a profit center; they were a referral engine. Sending money to a non-user worked a lot like a signup bonus: Hey! There’s money waiting for you if you download this app.

Banks largely ignored this dynamic at first because P2P payments themselves weren’t very profitable. But they eventually realized that what looked like a simple payments feature was actually a powerful distribution machine. Zelle was the industry’s response: a bank-owned P2P network designed to keep transfers inside bank accounts rather than letting fintech wallets capture the customer relationship. By the time Zelle arrived, though, the market was already crowded. Today, the P2P landscape is saturated: Venmo, Cash App, Zelle, Apple Cash, PayPal, and even crypto wallets all compete for the same basic use case. And now Cash App is changing the rules.

In addition to these shareable payment links, the company introduced Pools, a group payment feature that allows people to contribute to a shared goal or expense without having a Cash App account, paying instead through Apple Pay or Google Pay. In practice, this means someone can settle a bill, chip in for a group gift, or reimburse a friend without ever downloading Cash App.

Taken together, these features represent a subtle but important shift. Cash App is making it easier for money to flow through its network, even if not every participant is a Cash App user. That runs counter to the closed-loop viral growth playbook that helped build the product in the first place. Opening the loop increases the likelihood that a payment actually gets completed. And for Cash App in 2026, completion matters more than squeezing every transaction for user acquisition.

The company’s strategy today is about monetizing activity within its ecosystem — through the Cash App Card, stock investing, crypto trading, lending, and other financial services — not simply maximizing downloads.

Payments can simply be payments again. The rest of the platform can do the work of turning users into profitable customers. |

#3: The Super App No One Asked For |

This isn’t news, per se, but I found this tweet from Brian Armstrong, CEO of Coinbase, to be interesting: |

The ambition to build a financial “super app” is not new. Plenty of fintech and fintech-adjacent companies in the U.S. have pursued it over the past decade. In fact, you could argue that the largest banks — including Coinbase’s arch-nemesis JPMorgan Chase — already offer an analog version of a financial super app. So it’s not surprising to see Coinbase trying to build a crypto-native version. What is surprising is how flawed the strategy appears to be, both strategically and tactically.

Let’s start with the strategic problem: there is very little evidence that U.S. consumers actually want a single financial super app.

The meme Brian Armstrong used to illustrate his argument accidentally explains why.

In the image, the protagonist is choosing between two equally convenient options. It isn’t eight buttons on one side versus one button on the other. It’s one button versus one button.

In financial services, the “button” is the smartphone. It’s already the universal interface through which consumers access financial products.

Thirty years ago, convenience favored consolidation. If you needed a checking account, a credit card, a mortgage, and investment services, it was easier to get them from the same bank than to visit four or five different institutions. One trip to one branch was better than five trips to five branches. That dynamic drove the rise of national, multi-product banks in the 1990s and early 2000s. Today, that advantage has largely disappeared. Consumers simply toggle between apps on their phones.

Indeed, what little friction that still exists in digital financial services is slowly getting scrubbed away, thanks to the emergence of open banking (a trend that large banks like JPMC have been fighting hard against). Agentic AI has the potential to go even further, giving consumers an intelligent orchestration layer that can optimize their financial outcomes by working autonomously across a range of different providers.

Now, reasonable people might disagree with this conclusion. And, indeed, I may be wrong! Consumers’ appetite for an unbundled finance stack has its limits. Trust is still the most important attribute in financial services, and it’s possible that trust could push consumers toward consolidating with a small number of providers. But even if you believe the super app thesis is correct, and that past attempts have simply suffered from poor execution, Coinbase’s implementation still raises serious tactical questions.

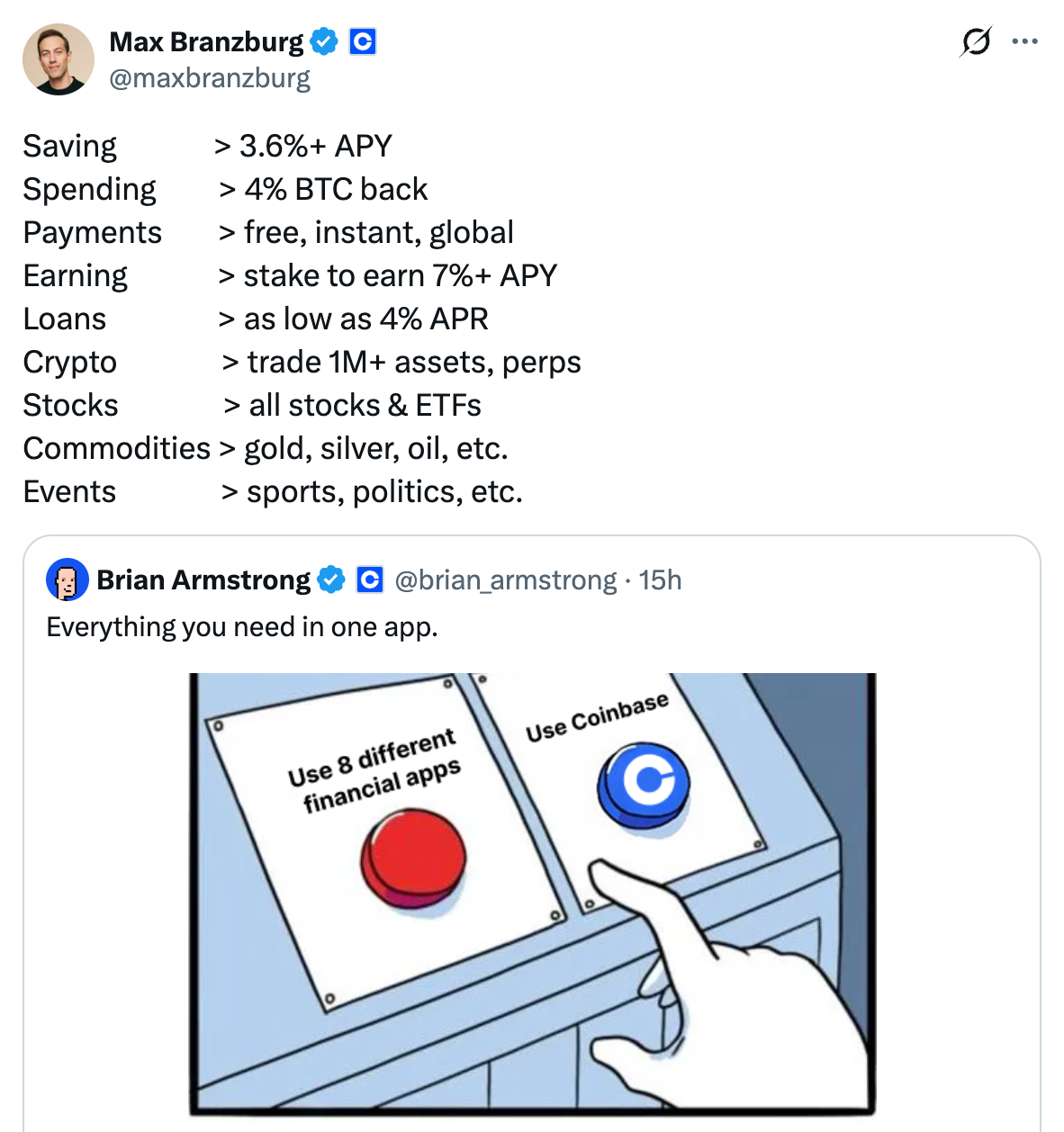

Here’s how a Coinbase PM, quote tweeting Armstrong, describes the Coinbase super app:

|

That’s a bunch of products! Let’s review them real quick: -

Saving: This is essentially a bet on yield-bearing stablecoins becoming legal. Coinbase is currently lobbying hard for this. Banks are fighting back. But even if Coinbase wins that fight, the economics here are weaker than many people assume. Stablecoin yield ultimately comes from returns on reserve assets like short-term Treasuries. Bank yields, by contrast, are driven by lending, a much deeper and more durable source of revenue. Over time, that makes it hard to imagine Coinbase consistently offering more attractive “savings” rates than banks.

- Spending: This one is appealing, assuming you love BTC as an asset.

-

Payments: This one makes sense conceptually. But crypto payment rails don’t magically eliminate the costs of moving money, especially across borders. Someone still has to absorb those costs, and it’s unlikely Coinbase will do so forever.

-

Earning: The term they are searching for here is “high-risk investing,” not “earning,” and it’s not obvious that most consumers are comfortable relying on staking rewards as a stable source of return.

-

Loans: This one drives me out of my mind. Coinbase’s loans are powered by the DeFi protocol Morpho and are typically overcollateralized. Users must pledge more crypto than they borrow, and the collateral can be liquidated if its value drops (which, you know, is a thing that happens in crypto). That’s a very bad way to borrow money unless the goal is simply to lever up on crypto exposure. In terms of utility, Coinbase’s loans aren’t even in the same universe as the loans offered by banks and fintech companies.

- Crypto: This is Coinbase’s core competency. This is the product that built the company.

- Stocks: A new addition, and a somewhat odd one until public equities migrate on-chain.

-

Commodities: Commodities markets are ruthlessly efficient, with very sophisticated traders on the other side, so I’m not sure this is a great fit for retail users.

-

Events: Ditto for sports betting! With the added bonus that it’s super fun and addictive and a great way to keep those MAU numbers high (as long as you don’t care about the negative effects that sports betting has on users and their families!)

Coinbase is such an odd company.

Compared to Bitcoin maximalists and DeFi purists, it is actually quite traditional in its ambitions. It really just wants to be a bank (while avoiding as much banking regulation as possible).

At the same time, compared to actual banks, Coinbase’s product vision feels wildly detached from the mainstream of consumer financial services.

Which raises a question: Does Coinbase actually understand what the average bank customer wants? |

|

|

2 READING RECOMMENDATIONS |

Tremendous piece by Matt. It’s such a great observation that the “we’re a software company, not a bank” framing that so many fintech companies adopted during the ZIRP years was, A.) not true, and B.) the worst possible thing you could say to investors in 2026. |

Not sure I completely agree with Mr. Thompson on this one, but it’s an interesting observation that many of the developments in AI over the last couple of years have likely increased the scale of the demand for compute, now and in the future.

Thought-provoking as always! |

There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network. I’m planning to spend some time on the Fintech Takes podcast demystifying different AI topics that are relevant to fintech. Is there anything, in particular, that you’re confused by or curious to learn more about? If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}

Join 2,444 other finance and fintech leaders in the Fintech Takes Network |

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 60,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|