Hello! Kiah here. Welcome to Fintech Takes Banking, my weekly newsletter where I highlight things I think are interesting or important for bankers and the surrounding environs.

Before we get into this week’s newsletter, I wanted to clarify that in last week’s newsletter, the anecdotes in the “Interesting Things I Learned about the New York Fed” section were fully sourced to independent research and did not come from the tour of the New York Fed.

| Was this email forwarded to you? |

|

|

What We Mean When We Say “Make a Loan” |

I am about to share something extremely stupid and basic: I don’t know what it means to make a loan anymore.

In the last two months, I have never felt dumber or more confused than trying to ascertain what it means to make a loan, where loans are made and why this is even a question I find myself asking in 2026. Please don’t tell anyone; this is obviously an extremely embarrassing thing for a bank reporter to admit. What was once a simple, almost intuitive answer to a straightforward question now sends me down a spiraling rabbit hole — but I’m getting ahead of myself. Let’s start at the beginning.

I have borrowed money while living in the following states: Nebraska, Virginia and Tennessee. Without going through almost two decades of my credit history, I am pretty sure I have never borrowed money from a bank headquartered in the state where I resided. All of these states have interest rate caps, percentages that legislators thoughtfully considered in balancing my interests as a borrower against the interest of lenders. In all the research I have done into looking up different loans and cards, I have never looked up these percentages.

This is all to say: Where I have lived, and where the bank is located, has never meaningfully figured into my decision to borrow money. I’m sure this is true for many borrowers, and it is one of the consequences of living in a world with interest rate exportation and charter parity. (And I will acknowledge the blessing and privilege of not needing high-rate loans that are at issue here.)

For decades, where a loan was made mostly didn’t matter. Now it does. Dueling court decisions have unsettled this previously stable foundation, injecting a shot of uncertainty into the definitions and applications of an old law. In the long run, these decisions — and the legislative efforts behind them— threaten to complicate and significantly handicap state-chartered banks’ ability to compete with their nationally chartered counterparts. These decisions could signal a serious challenge to the future utility and powers of the state bank charter, potentially weakening or collapsing the country’s dual banking system. See what I mean by spiraling?

And it all comes down to how courts determine where a loan is made. |

While I never cared about my state’s interest rate cap, the banks headquartered there certainly do. States set interest rate caps and rules for different types of loans; some don’t have a cap at all. Banks that are headquartered in that state and lending to residents of that state are subject to the cap. Easy! And for decades, most lending featured these physical aspects. But what about banks in one state lending to customers in a different state? What state matters then when the loan is made?

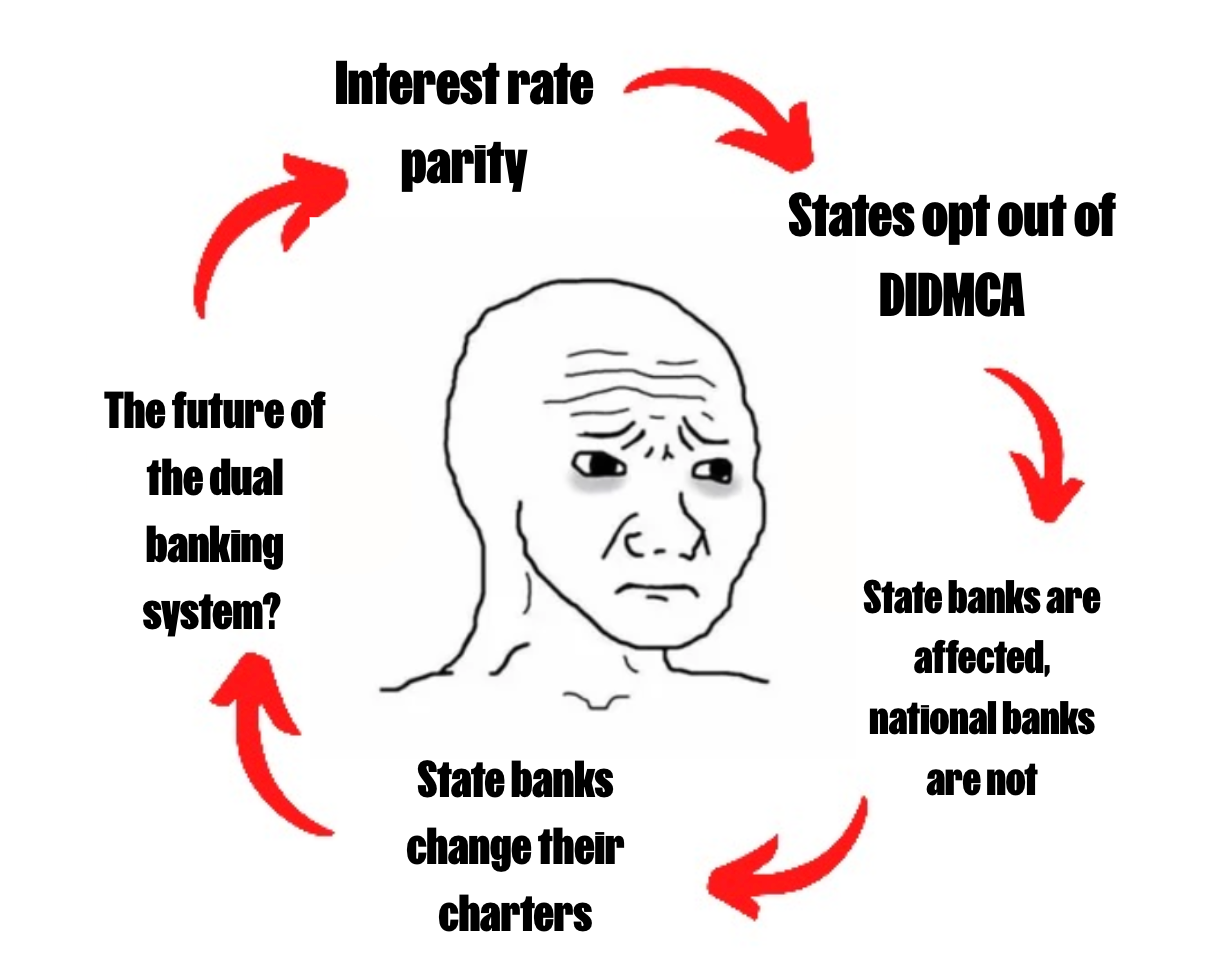

Banks with a national charter from the Office of the Comptroller of the Currency can charge interest rates that are permitted in the state where the bank is headquartered — regardless of where the borrower lives and the laws in that state. The ability of national banks to export their interest rates was codified in the 1978 U.S. Supreme Court case Marquette National Bank of Minneapolis v. First of Omaha Service Corp., which involved two national banks. In this case, where the loan was made referred to where the bank was based, which then determined the maximum interest rate a bank was allowed to charge a borrower.

At a minimum, this approach simplifies a bank’s compliance by having to follow only one state’s laws. But it also allows a form of arbitrage; in this case, Marquette was based in Minnesota, which had capped rates at 12%, compared to First of Omaha, which operated under Nebraska’s 18%. State banks didn’t have the same ability to export their home state’s interest rate to borrowers in another state until the Depository Institutions Deregulation and Monetary Control Act of 1980, also called DIDMCA. Think of this as establishing interest rate parity or uniformity between state-chartered banks and national charter banks.

“State banks and national banks have the same powers basically,” said Michele Alt, a partner at the consulting firm Klaros and a self-described survivor of the “preemption wars” of the early 2000s, when she worked at the OCC. “To the customers, the distinction is murky. They can't tell the difference between the two.”

This combination of charter privileges, legal findings and legislation created a groundwork for nationwide lending. It provided some certainty around what interest rates banks could charge as they grappled with how interstate banking and the digitization of financial services changed where they could find and compete for customers in far-flung cities. It’s why it didn’t matter what state I lived in when I borrowed money from a bank based in a different state.

|

What does it mean to opt out? |

That is, with one very important exception: DIDMCA allowed states to opt out of the interest rate parity for state-chartered banks. DIDMCA is an opt-out system, not an opt-in one: states’ interest rate caps would be preempted unless the state explicitly opted out of the legislation by statute, constitutional amendment or referendum, or repealed previously enacted legislation, according to a white paper from the American Fintech Council. Iowa and Puerto Rico have long opted out; other states opted out and then opted back in. But this wasn’t frequent or common, and there hasn’t been much change or disagreement about interest rate exportation and parity for decades.

“It's interesting, because no one has really talked about or focused on this law for years,” said Robert Savoie, a partner at Womble Bond Dickinson who was a contributor to AFC’s white paper. “It was all very quiet for a long time.”

That’s changed. There is new interest and new interpretations of what a DIDMCA opt-out entails. The surest thing I can say right now is that only state-chartered banks are impacted by a state’s DIDMCA opt-out. But which state-chartered banks making loans are subject to this cap? This, I was surprised to learn, is less settled than I had imagined. “The whole purpose of that litigation is to decide that very question,” he said. “The core question is, ‘Does it restrict out-of-state banks lending into the state? Or does it just limit the ability of the banks in that state to lend outside of it?’” |

How Everything Became Worse and More Confusing |

The litigation Robert is referring to is National Association of Industrial Bankers v. Weiser. The case originated from Colorado’s 2023 efforts to opt out of DIDMCA, a decision that was supposed to go into effect in July 2024 before industry participants sued to block it.

Supporters of the opt-out wanted to throttle the ability of the high-rate lenders that partnered with state banks located in states without rate caps to offer short-term, high-rate loans to Colorado residents, according to Colorado media reports. The Colorado Consumer Credit Code generally caps the annual percentage rate on closed-end consumer loans and non-credit card open-end loans above $1,000 at 21%.

The district court in Colorado held “that where a loan is ‘made’ turns only on where the originating bank is located and performs non-ministerial functions (e.g., where the credit decision is made, where the decision to grant credit is communicated from, and where the funds are disbursed),” according to the AFC white paper. Given that analysis of where a loan is “made,” which state-chartered banks need to follow the rule?

According to the AFC white paper: “The Court’s conclusion meant … Colorado was not able enforce its interest-rate caps with respect to loans to Colorado residents that were made by a bank outside of Colorado. Instead, the opt-out only impacted banks located in Colorado that ‘make’ loans in that state, and thus its primary impact is that the opt-out eliminates the ability of Colorado-based, state-chartered depository institutions to export their home state law.” (Emphasis mine.)

So, a state’s DIDMCA opt-out means that its state-chartered banks are the ones that must comply with the state’s interest rate cap when they lend outside the state? Do I have that right? Well, actually, that is not what the 10th U.S. Circuit Court of Appeals decided.

In a 2-1 decision, the circuit court found that the opt-out applies “when either the borrower or lender was located in Colorado, and thus applied the opt-out to any loan made to Colorado residents,” according to the AFC white paper. (Emphasis mine.)

|

Many groups had thoughts on this contradicting set of decisions and the specific interpretation the court of appeals decided on. Many did not like it. A group of trade associations applied for an en banc rehearing in December 2025, where the entire circuit court would review the decision. In their petition, the associations said the circuit court’s decision splits with a decision from the 8th U.S. Circuit and incorrectly decided an issue critical to consumer lending and interstate banking.

Twenty states’ attorneys general signed an amicus brief in support of a rehearing. Comptroller of the Currency Jonathan Gould issued a statement that stated the 10th U.S. Circuit’s decision “disadvantages state banks that wish to lend in Colorado compared to national banks and Federal savings associations. Such an outcome is fundamentally inconsistent with Congress’s efforts to create competitive equality between state and federally chartered banks.”

It remains to be seen what happens in the future. The 10th U.S. Circuit, which covers Colorado, Kansas, New Mexico, Oklahoma, Utah and Wyoming, is not required to grant a rehearing en banc. “By rule, a rehearing en banc is ‘not favored,’ and according to the Tenth Circuit, considered an ‘extraordinary procedure,’” wrote attorneys at Husch Blackwell in a legal update.

So a rehearing en banc in the 10th Circuit is one possibility. There’s also continued legislative interest in DIDMCA. Oregon legislators are currently debating HB 4116, which would apply to consumer finance loans. And of course, DIDMCA is an act of Congress. Senators Bernie Moreno (R-Ohio) and Rep. Warren Davidson (R-Ohio) introduced a bill that would eliminate a state’s ability to opt out of interest rate exportation. The bill “preserves states’ authority to regulate in-state chartered institutions, protects interest rate exportation, and promotes competitive parity with national banks.” But that seems like a long shot: The sources I interviewed universally said it seemed unlikely that Congress would be able to pass a bill due to general partisanship.

So for now, a group of banks enters legal purgatory when it comes to lending to Colorado residents, under a decision that could extend to up to five other states in the circuit. There were 48 state-chartered banks in Colorado at the end of 2024, according to the state banking agency. By contrast, there were more than 3,600 state-chartered banks as of the second quarter of 2023. Either only Colorado-chartered banks need to comply with the interest rate cap when lending to out-of-state borrowers, or all state-chartered banks in the country need to comply with Colorado’s cap when lending to borrowers in the state — either with a fintech partner or not.

|

These actions and decisions raise big questions for the banking industry — questions we haven’t had to actively think about for decades. Where is a loan actually made?? What does it mean to opt out of interest rate exportation? Will any other states follow Iowa and Colorado? And if the circuit court’s decision stands, what does that mean for the outlook for the powers of the state bank charter in an increasingly technologically driven economy?

I don’t have the answers, and we likely won’t have them for a while. But next week, I will have even more DIDMCA findings and considerations for you to spiral over. Stay tuned! |

|

|

Hey there! Are you a financial institution exec? I need to hear what's most important to you.

I'm writing a report on commercial payments, and how modern tech can fuel growth & revenue in treasury management. It's anonymous, takes 5 minutes, and as an added thank you, we've added some prizes: one $500 gift card, one $100 gift card, and 6 Fintech Takes zip-ups.

You can fill out the survey here. Also, favor: if you're not the right person to take the survey, could you forward it to the person who is? Thanks! |

What I’ve been reading, watching and listening to this week: |

🥖 Congrats to: Sithamparappillai Jegatheepa, a Sri Lankan baker whose Parisian bakery, Fournil Didot, recently won this year’s Grand Prix de la Baguette de Tradition Française and will supply the French president’s residency with baguettes for a year. Related: How do I become one of these civilian taste testers? It’s hard to see people living your dreams.

🏃🏽 Rest in Peace: Jeff Galloway, Olympian and pioneer and promoter of the run-walk training method. Jeff’s training method turned walking during a run from a sign of struggle into a sustainable tool to help beginners (and everyone else) go farther distances with less impact on the body. Thank you, Jeff, for making running a more inclusive and accessible activity and helping millions of runners cross a finish line on their terms.

🎙️ On Bank Nerd Corner: I chat with Bernadette Ksepka, senior vice president and deputy head of product management for the Federal Reserve System’s FedNow Service, about FedNow as the instant payment network nears its three-year anniversary. We discuss the adoption of the network by financial institutions, the use cases and the shifts and adjustments that institutions need to make to adopt this and other digital-forward technologies.

|

Thanks for reading, and thanks once again to my colleague Claire Monterroyo for working so diligently on these memes! Any mistakes are solely my own. As always, let me know your thoughts on this piece. And if you know anything about the Iowa banking system post-DIDMCA opt-out, let me know. – Kiah |

|

|

Get your brand in front of 65,000+ financial services execs. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|