{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Friday, Fintech Takers!

And happy Valentine’s Day Eve!

My wife and I have a very chill approach to celebrating Saint Valentine, which I feel is appropriate given that he was originally the patron saint of people with epilepsy, plague victims, and beekeepers, rather than the patron saint of lovers, as he was later cast.

Still, we love love here at Fintech Takes, and I hope everyone’s Valentine’s Day is wonderful. If you need some bank-nerd inspiration for your Valentine’s card, Kiah Haslett has you covered. - Alex

P.S. — Tea withdrawal update. It has now been 7 days without the caffeinated tea that I organized my entire life around. It’s still terrible, though I feel slightly less exhausted than I did earlier in the week. All other teas remain uninteresting to me, although I am becoming increasingly enamored with the idea of trying to deconstruct the Fast Lane recipe and brew my own replacement.

P.P.S — If you’re interested in sorting fact from fiction when it comes to the application of LLMs and agentic AI in financial services (And you should be! This is probably the most important topic in fintech in 2026!), be sure to sign up for this webinar with me and Alloy’s Jason Ioannides on February 25th.

|

Was this email forwarded to you? |

|

|

Tricked by Product-Market Fit |

Defining product-market fit is difficult.

I’ve never built a startup, so I’ve never experienced that moment of finding product-market fit. However, from everything I’ve heard and everything I’ve read, when that moment comes, you can feel it. Here’s how Marc Andreessen describes it:

You can always feel when product/market fit isn’t happening. The customers aren’t quite getting value out of the product, word of mouth isn’t spreading, usage isn’t growing that fast, press reviews are kind of “blah”, the sales cycle takes too long, and lots of deals never close.

And you can always feel product/market fit when it’s happening. The customers are buying the product just as fast as you can make it—or usage is growing just as fast as you can add more servers. Money from customers is piling up in your company checking account. You’re hiring sales and customer support staff as fast as you can. Reporters are calling because they’ve heard about your hot new thing and they want to talk to you about it. You start getting entrepreneur of the year awards from Harvard Business School. Investment bankers are staking out your house.

I quote Andreessen because this is how he (and the rest of the tech VC ecosystem) trains founders to think. Your first and only job, as a startup founder, is to find product-market fit. Until then, nothing else matters. Your job is to keep iterating until you find it.

The most successful serial founders develop an uncanny intuition for finding product-market fit.

The problem is that in financial services, that intuition can lead to disaster.

Many of the signals that tech founders are trained to associate with product-market fit — fast early adoption, passionate users, organic growth, and a willingness to pay for the product — can be deeply misleading in financial services. In some cases, they don’t signal that you’ve built something durable or valuable. They signal that you’ve removed a constraint that exists for a good reason. This essay is about how fintech founders get tricked by product-market fit, and why, in financial services, success can be the earliest warning sign that something is terribly wrong. |

Why Financial Services Breaks Product-Market Fit Intuition |

Andreessen’s definition of product-market fit assumes something important: that satisfied customers equal a healthy business.

In most software markets, that assumption is valid. Customers adopt a product because it helps them do something better or cheaper. If they aren’t getting value, usage drops. If the product is bad, growth slows. If the business model doesn’t work, the problem shows up quickly and locally. Financial services doesn’t work that way.

Financial products don’t just deliver utility. They mediate risk. They decide who gets access to money, how losses are distributed, who bears liability, and when consequences show up. A user choosing your product doesn’t necessarily mean the product is good, or even that it’s working. It often just means that, for this user, the tradeoffs you’ve made are attractive. That difference matters because it breaks the feedback loops founders rely on.

In financial services, the costs of bad decisions are delayed. Losses show up months or years after growth. Fraud scales faster than detection and often impacts others in the ecosystem more than it impacts you. Regulatory consequences lag market behavior and typically only appear after something breaks in catastrophic fashion. Reputation damage comes last, after everything else has already broken. As a result, early success can actively suppress the signals that would normally tell you something is wrong.

In software, removing friction is usually the point. In financial services, friction is often the product. Credit checks, transaction monitoring, and compliance requirements don’t exist because incumbents are lazy or hostile to customers. They exist to help prevent losses, abuse, and systemic harm. Often, they exist to positively select for customers who will be profitable over the long term.

When a financial product grows quickly, it’s frequently because some form of friction has been relaxed, deferred, or shifted elsewhere. That can feel exactly like product-market fit. Customers are happier. Growth accelerates. Revenue shows up early. But what’s being tested isn’t whether the product works — it’s how long the consequences can be postponed. This is why intuition for finding product-market fit, honed in software, can be so dangerous when applied to financial services. The same signals that tell founders to lean in can actually be telling them to slow down. After studying fintech for the past 20 years, I’ve noticed a few recurring patterns that founders fall into when they are tricked by product-market fit. |

Pattern 1: “Everyone wants what I want.” |

One of the most common ways founders get tricked by product-market fit in financial services is by building a product for themselves.

This usually starts innocently enough. The founder has a problem in or adjacent to financial services. They build the product they wish had existed. They assume (reasonably) that if they can just get the product right, everyone else will want it too.

Early on, everything looks great.

The first users, often comprised of the founder’s friends and family, love the product. They adopt it quickly. They use it frequently. They tell their friends. They’re even willing to pay for it. It feels like product-market fit.

The problem is that the founder is not the market.

Personal financial management (PFM) is the clearest example. For decades, founders have tried to build tools that help people budget, track spending, and actively manage their money. The implicit belief is that most consumers want to behave like financially disciplined power users, but lack the right software.

However, as I wrote a few years ago and as Max Levchin and I discussed recently, this is a flawed assumption. Most people don’t want to actively manage their finances, even if taking a more active approach to budgeting and financial planning would benefit them enormously. Conversely, the small number of people who get excited about budgeting tools (who are overrepresented among startup founders) are often the people who need them the least.

This creates a dangerous illusion. Early adoption is strong precisely because the product resonates deeply with a small, unrepresentative slice of users who think like the founder. That passion feels like validation. It feels like inevitability. But when the product tries to cross the chasm, growth stalls. The result is a product that is well-designed, loved by users, and permanently niche.

In financial services, this form of deceptive product-market fit is especially seductive because the early signals are all positive. There are no losses. No blowups. No regulatory issues. Just a quiet realization, years later, that the market you thought you were building for never actually existed at scale. |

Pattern 2: “I can say yes where everyone else says no.” |

The second way founders get tricked by product-market fit in financial services is by misunderstanding the product they are selling.

This pattern shows up most clearly in lending.

Every generation of fintech produces founders who believe that traditional lenders are overly conservative. Incumbents are slow. Their models are outdated. Their underwriting rules are blunt. With better data, better technology, and better product design, the thinking goes, it should be possible to responsibly say yes to customers everyone else rejects.

Early on, everything looks great.

Demand is enormous. Approval rates are high. Customers are grateful. Growth comes easily because free money is, shockingly, something that everyone wants. It feels like product-market fit.

The problem is that saying yes is not the same thing as making a good loan. In lending, demand is infinite. Repayment is the product.

As I like to say around here, lending is a learning business. The conservative decisions made by traditional lenders aren’t merely the result of laziness or inertia (though there is always some of that). They are also the result of those companies having gotten their teeth kicked in multiple times and learning the hard way where losses tend to concentrate.

When a new entrant grows by approving borrowers that others won’t, it often isn’t discovering an overlooked market. It’s rediscovering known risks.

And the real problem is that the feedback loop in lending is slow. Losses don’t show up immediately. They arrive later, after cohorts season, after economic conditions change, or after capital markets tighten. Until then, growth looks like confirmation that the model works. When the feedback finally does arrive, it often arrives all at once.

This is what makes this pattern so dangerous. The early signals aren’t just misleading — they’re reinforcing. The faster the business grows, the more convinced everyone becomes that they’ve cracked the problem that those risk-averse bankers were just too dumb to solve. |

Pattern 3: “Growth is good, and friction is bad.” |

The third way founders get tricked by product-market fit in financial services is by over-applying one of the most sacred bits of conventional wisdom in tech: that growth is always good, and friction is always bad.

In software, this is usually true. Removing friction makes products easier to use. Easier products grow faster. Faster growth is evidence that you’re delivering value. In financial services, friction often exists for a reason. Identity verification. Transaction limits. Manual review. Fraud checks. Account freezes. None of these make a product more delightful. All of them slow growth. But they also protect the institution and the broader system from abuse. When a new financial product removes friction, growth accelerates. Early on, everything looks great. Signups surge. Accounts are active. Money is moving. Transaction volume climbs rapidly. The product spreads because it is faster and easier than the alternatives. Users are clearly choosing it. It feels like product-market fit.

During fintech’s “steroid era,” companies like Chime and Cash App experienced explosive growth. Millions of new accounts. Rapidly growing payment volumes. Strong engagement. It looked like a generational shift away from traditional banks. Some of that growth reflected real improvements in user experience. But a large portion of it reflected something else: the fact that these products were easier to access and easier to use — including for people whose behavior traditional institutions had worked hard to screen out.

Fraudsters select for low-friction financial products the same way that lions select for sickly gazelles. Third-party fraud — in which a bad guy uses someone else's personal information to steal funds, open new accounts, or make unauthorized purchases — thrives when financial services providers choose to prioritize UX over KYC. Scams — in which a legitimate customer is tricked into authorizing a payment to a fraudster — similarly depend on a relaxed approach to identity verification and transaction monitoring because they need to open the accounts that the victims send their money to.

First-party fraud — in which a consumer uses their own true identity or legitimate accounts to deliberately defraud financial institutions or merchants for personal gain — is even worse. It doesn’t exploit financial services providers’ lax KYC processes (the customer is using their real identity), but it does exploit those providers’ tolerance for shitty behavior (fraudulent ACH disputes, chargebacks, etc.) And that tolerance teaches consumers exactly the wrong lessons, as I bemoaned a few years ago:

One of the things I really don’t like about fintech’s recent tolerance for first-party fraud is the message that it sends to consumers, particularly young consumers – cheating is OK. It’s acceptable to game the system. It’s OK to lie.

This concern isn’t hypothetical. Humans have a remarkable capacity to justify almost anything to ourselves if we are provided with the proper incentives. Indeed, we can go much further than simple justification. We can convince ourselves that the bad thing we’re doing is, in fact, morally right.

The reason that this tolerance for fraud persists for so long is that the immediate consequences are only felt indirectly, or not at all, by the companies that cause them.

Sure, tolerating ACH fraud might create massive problems for merchants (to the point where certain merchants, like rental car companies, stop accepting your debit card), but is that really Chime’s problem? Sure, lots of consumers are getting scammed through P2P payments tools, but as long as that activity is leading to more account sign-ups and higher monthly active user numbers, is that really a problem that Cash App should care about?

Put simply, the feedback loop is slow and weak.

Growth shows up immediately. More users. More activity. More revenue. The dashboards are green. The press is positive. Investors are impressed.

Growth fueled by relaxed constraints can be indistinguishable, at first, from growth fueled by genuine value creation. It’s only later, once you start rebundling and trying to cross-sell your way into a higher customer LTV, that you realize that the foundation you are trying to build on is rotten. |

Pattern 4: “Compliance with rules I don’t agree with isn’t my problem.” |

The fourth way founders get tricked by product-market fit in financial services is newer, more global, and in some ways more seductive than the others.

It starts with a moral argument, which goes something like this:

The global banking system excludes people. It over-collects data. It freezes accounts without explanation. It enforces economic sanctions against ordinary consumers who didn’t do anything wrong. It prioritizes compliance over customer experience. It needs to be disrupted by any means necessary. So, that’s exactly what founders try to do. They build new products, using alternative infrastructure and clever workarounds, promising to serve the underserved, protect privacy, or route around unfair systems. And you know what?

The demand for the products is immediate and overwhelming. Growth is explosive, particularly outside the United States and Western Europe. Account signups and transaction volume skyrocket. Communities evangelize the product. The company positions itself as principled rather than reckless — as fixing a broken system rather than evading it. And in some cases, the founders genuinely seem to believe it.

Helping a Venezuelan consumer store and move money, despite economic sanctions, can feel like the right thing to do. Enabling pseudonymous payments can feel like protecting civil liberties. Offering financial access without intrusive documentation can feel humane.

It feels like the most morally justified version of product-market fit.

The difference between this pattern and the others is that the feedback loop is even weaker. There are no immediate credit losses. No angry customers demanding refunds. The activity itself doesn’t automatically lead to a direct financial hole in the balance sheet or a flood of customer complaints. The legal and regulatory risk exists, but it is abstract. It sits in the background, contingent on enforcement. And enforcement, particularly in global and crypto-native systems, can be slow, fragmented, or jurisdictionally unclear. That makes this pattern uniquely tempting for founders focused on the short term. Growth is strong. Users are grateful. The moral framing is compelling. The downside feels distant.

But once again, what feels like product-market fit may simply be the removal of constraints that exist for good reasons. Sanctions regimes, AML rules, and KYC requirements are not purely bureaucratic obstacles. They are tools that countries use to achieve important policy goals through the financial system. When you decide that you disagree with those policy goals or that the tools used to achieve them are illegitimate, you aren’t just democratizing access to the financial system. You are purposefully stepping outside the regulatory perimeter. Sometimes that perimeter pushes back. And when it does, it rarely does so gently.

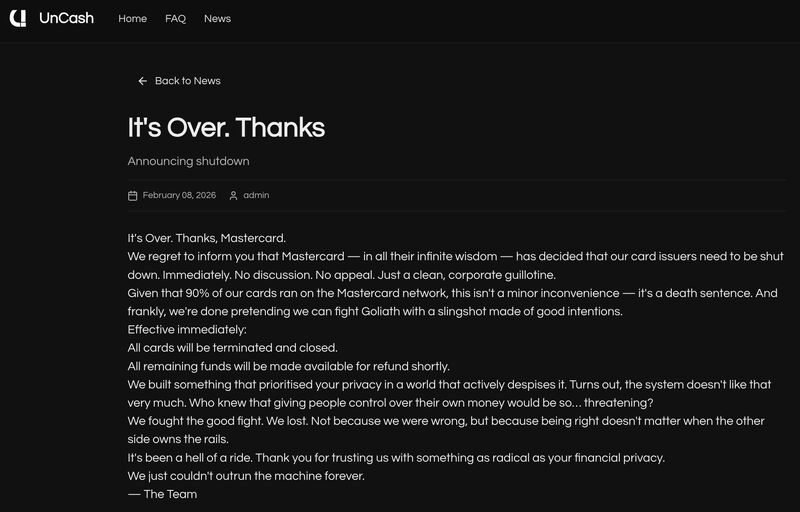

“No KYC” crypto spending cards are an instructive example. These products, which exploit a compliance loophole for corporate cards, have received scrutiny in recent weeks thanks to the reporting of Jason Mikula. And that scrutiny has led to the abrupt shutdown of some of these products, such as UnCash:

|

Two things are important to note from this statement.

First, notice the framing of the product and its purpose. “We built something that prioritized your privacy in a world that actively despises it.” That’s a very common sentiment in the crypto ecosystem, and it helps explain why a lot of founders who fall into this fourth pattern aren’t just tiptoeing through these compliance loopholes. They are sprinting through them and giving regulators and incumbents the middle finger while they’re doing it.

Second, we should be asking why it took Jason’s reporting on these “no KYC” cards for Mastercard to take action to stop Uncash from breaking the law. |

All This Infrastructure is Making the Problem Worse |

On an anecdotal level, these four patterns of mistaken product-market fit are interesting, but hardly alarming. After all, what’s the harm if another generation of niche PFM products gets built in pursuit of the elusive “Mint.com, but more popular” vision? Who is getting hurt (apart from a few VCs who don’t know to stay away from PFM)? The systemic concern isn’t about the choices that individual fintech founders make. It’s about the infrastructure that those founders build on top of and how that infrastructure influences those choices.

Over the past two decades, the financial services industry has become deeply layered and modular. Banks and fintech companies partner with each other (sometimes with the help of BaaS middleware platforms). Card programs run through program managers and processors before they ever reach a network. Loans are originated in one place, funded in another, and bundled into securities somewhere else. In crypto-native systems, that layering is even more extreme — sometimes with no regulated institution at the center at all.

This modularity has real benefits. It lowers barriers to entry. It increases competition and speed to market. It allows specialists to innovate on discrete pieces of the stack. But it also fragments responsibility and obscures visibility.

As Jason Mikula observed in his article on “no KYC” crypto cards:

Responsibility for BSA/AML compliance is often passed down a chain of partners, with collection of necessary information typically resting with the user-facing entity. But, all too often, the data doesn’t flow back up to the regulated entity — the bank — standing behind a given card program, blinding financial institutions to the true risks hidden beneath multiple layers of service providers. The “Nth party” risk management issues posed by these relationships should already be well known and well understood after the 2022-2024 wave of consent orders focused on BSA/AML and third-party risk management failures in bank-fintech partnerships. Yet a number of existing players and new entrants are still exposed to outsized risk through their third-party relationships.

The reason this problem has been difficult to fix is that it’s a structural weakness.

Traditionally, in banking, the institution that designed the product, onboarded the customer, held the deposits, and took the losses was the same entity. Feedback loops were imperfect, but the consequences were aligned: if you underwrote poorly, you lost money; if compliance failed, your charter was at risk; if fraud spiked, your balance sheet and reputation suffered.

In a modular system, those feedback loops are distributed: - The fintech company controls the user experience and drives growth.

-

The sponsor bank holds the charter.

- The processor moves the money.

- The network enforces its own rules.

- Capital providers fund the loans or buy the assets.

Each participant sees only a slice of the activity. No single party sees the whole picture … at least not until something goes very wrong. Three real-world examples make this clear.

Synapse is, obviously, the canonical example. Funds flowed across sponsor banks, program managers, middleware providers, and end-user accounts in ways that made it unclear who owned what. On paper, responsibility for custody and reconciliation existed. In practice, that responsibility was diffused across a wide range of participants, many of whom turned out to be deeply incompetent. When the system seized up, customers were locked out of their money, and no single party was able to reconcile the full picture.

Kontigo, another recent subject of Jason’s reporting, illustrates how layered risk can evade detection until secondary signals appear. In that case, sanctions evasion was, very explicitly, the product, and that product had a strong product-market fit in Venezuela. However, it wasn’t regulators or Kontigo’s partners discovering the sanctions evasion that led to corrective action. It was elevated ACH disputes noticed by JPMorgan Chase through its partner Checkbook. That was the trigger, not proactive compliance monitoring — because the compliance signals were obscured behind multiple intermediaries and blended into normal payments activity. Only when a secondary effect emerged did anyone notice something was off.

Pagaya is an example that I am personally obsessed with. It has, so far, lacked the dramatic fireworks that we have seen with Synapse and Kontigo. However, as I wrote about last year, the potential for problems, based on the sheer, multi-layered complexity of the company’s product and business model, is obvious. Pagaya offers an embedded second-look lending network, which seamlessly and invisibly allows its lender partners on the front end to say yes to more borrowers, while funneling the resulting loan assets to its investor partners on the back end. The conflicts inherent in this model are obvious (lenders want to say yes more and offload risk onto investors, and Pagaya needs to facilitate that activity in order to grow), but the specific risks are fiendishly difficult to quantify because of the complex, multi-party network that Pagaya has assembled.

Regulators, by design, supervise legal entities — not distributed systems. When activity is spread across jurisdictions, counterparties, contracts, and networks, proactive supervision and risk mitigation become impossible. Federal regulators completely missed the risks posed by BaaS middleware platforms like Synapse and stablecoin-assisted financial crime enablement services like Kontigo. And I can tell you from personal experience that credit infrastructure providers like Pagaya are, despite their size and systemic importance, nowhere on regulators’ radar screens.

The result is an environment in which product-market fit can feel legitimate at every layer of the stack: - The startup sees growth.

- The bank sees fee income.

- The network sees volume.

- Investors see yield.

What no one sees — at least not clearly and not early — is the accumulation of risk across the system.

When something finally breaks, it rarely breaks neatly. Networks tighten rules. Banks retreat from partnerships. Capital dries up. Regulators overreact. And the same growth that once felt like validation is suddenly reinterpreted as excess.

This doesn’t mean that building all of this modular fintech infrastructure was a mistake. It just means the traditional signals that fintech founders rely on to judge success — growth, adoption, volume — are even less reliable today. |

In Financial Services, Product-Market Fit Is Harder Than It Looks |

There is no easy fix.

The default regulatory answer to these problems is third-party risk management. If banks supervise their various partners (and the partners, vendors, and customers of those partners) more closely, if networks tighten their rules, and if contracts clearly assign responsibility, the system should function. In theory.

In practice, third-party risk management quickly becomes nth-party risk management. Compliance obligations in complex bank partnership models are often pushed down the chain to the user-facing entity — but the information doesn’t always flow back up. The regulated institution that ultimately bears the responsibility may be structurally blind to what is happening higher up in the stack. That problem compounds as more layers of program management and technical abstraction are added to the stack.

And, of course, crypto makes everything more difficult.

The idea of permissionless, self-custodied digital wallets is interesting in an academic sense (and downright titillating if you are a technolibertarian), but it is an absolute nightmare for anyone trying to monitor and mitigate systemic risk or implement a universally-popular policy initiative like keeping money out of the hands of terrorists.

This isn’t to say that crypto and decentralized finance are inherently malicious. It just means that in an ecosystem where product-market fit is already easy to misread, adding a largely permissionless substrate amplifies the distortion. Having said all of that, just because this problem doesn’t have any easy solutions doesn’t mean we can’t make progress in the right direction.

Some improvement will come from clearer regulation and bringing more companies inside the regulatory perimeter.

After Synapse, regulators (temporarily) showed a renewed focus on third-party risk management in bank-fintech partnerships and proposed rules like the FDIC’s recordkeeping requirement to ensure banks can clearly reconcile custodial accounts. And if crypto-native companies like Bridge obtain national trust bank charters and are supervised like banks — and if regulators are properly resourced and incentivized — they will be better positioned to help executives at these companies learn to equate rapid growth with increased risk.

Some improvement will come from the maturation of fintech infrastructure.

It’s notable to me that, in a podcast last November, Stripe co-founder John Collison and Bridge CEO Zach Abrams were talking specifically about Venezuela as an underserved market and opportunity for Stripe to drive growth. And yet, according to a recent report from The Information, Bridge banned customers in Venezuela from using its services in January (after news broke about what a shitshow Kontigo was) and has added additional high-risk countries (Afghanistan, Belarus, Sudan, Yemen, etc.) to its block list. This gives me some hope that as the fintech infrastructure stack continues to become more complex, the providers in that stack may also become more responsible.

However, if we’re going to make meaningful progress in helping fintech founders avoid being tricked by product-market fit, the biggest improvement we will need to see first is in fintech startup culture itself.

Founders entering fintech need to understand that this industry is not software with money attached. It is a risk allocation system with software wrapped around it. The signals that feel like product-market fit are often signals that something is wrong. Growth can be the result of negative selection. Passionate users can be unrepresentative. Friction can be good.

In financial services, real product-market fit often feels slower and less glamorous. It involves saying no at least as often as yes. It requires aligning incentives with consequences. It demands that the same entity benefiting from growth also bears at least some of the downside risk. That is harder. It scales more slowly. It doesn’t always win awards. But it is durable. And in an industry built on trust, durability matters more than feeling like you’ve won. |

|

|

MORE QUESTIONS TO PONDER TOGETHER |

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis. What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

Drop your question here, whenever inspiration strikes! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network |

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 57,800+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|