Welcome to Fintech Takes Banking, my weekly newsletter where I highlight things I think are interesting or important for bankers and the surrounding environs.

You’ve maybe noticed I like writing about big themes in banking and connecting the dots, which means I don’t try to closely follow news stories when they break (that’s what podcasting is for). Imagine my surprise when this topic, which I have been working on since November, had two items of news break the week I was writing?! Thanks to the FDIC and to Affirm for making my newsletter this week look extra-timely. |

Was this email forwarded to you? |

|

|

Everything You Wanted to Know about ILCs but Were Too Afraid to Ask |

In March 2024, the Federal Deposit Insurance Corp. levied a civil monetary penalty of $6,097.72 against Salt Lake City-based Pitney Bowes Bank for failing to pay its fourth quarter 2023 deposit insurance assessment.

If you did a double-take at the name, SAME. (If you wondered how exactly a bank fails to set up its bill pay for FDIC insurance, also same.)

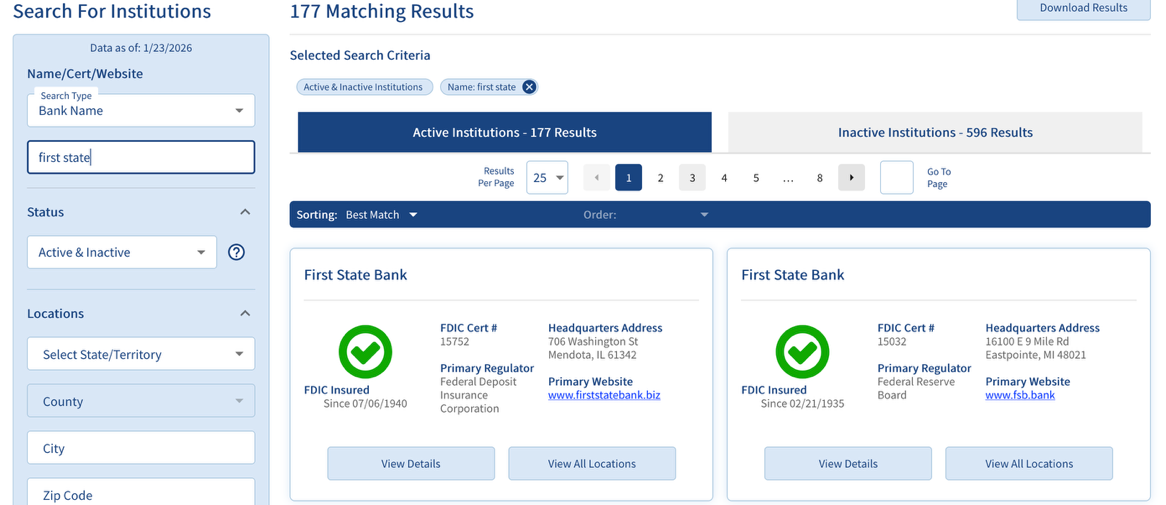

There are more than 4,000 banks, which means they sometimes have similar names to other banks. For instance, there are 177 results for banks that have “First State” in their name, which I do promise to write about someday. |

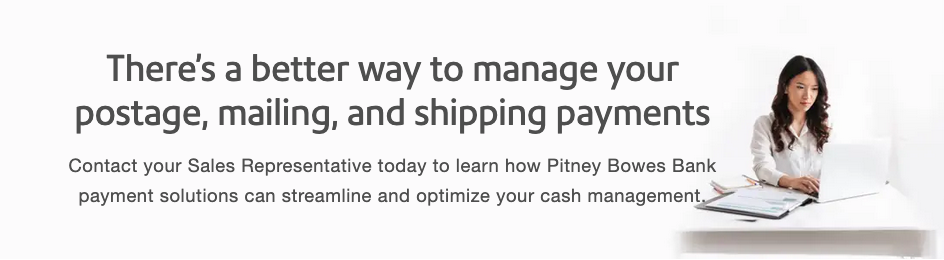

But not many banks share a name with the printer in the office copy room. Pitney Bowes Bank is an $811 million state-chartered nonmember bank that has been insured since 1998. It is owned by Pitney Bowes, which is a “technology-driven company that provides digital shipping solutions, mailing innovation, and presort mailing services.”

On Pitney Bowes Bank’s website, the company says it decided to start a bank when its small-to midsized businesses encountered financial challenges that existing credit facilities couldn’t solve. Today, the bank offers small business capital, including equipment finance, lines of credit and term loans, payment solutions “for all your postage, mailing and shipping cash management” needs and carrier payments. |

To me, these products are silly because it’s silly that a digital shipping and mail company owns a bank. But to a business that works with Pitney Bowes, these specialty solutions might make sense; it also might make sense to get them from the same place that you lease your bulk mailing equipment from.

Pitney Bowes Bank is one of two dozen industrial loan charter institutions, or industrial banks, in the United States. These banks are owned by a nonbank parent company and are set up for the express purpose of addressing the financial needs of the company’s customer base. BMW Bank of North America and Toyota Financial Savings Bank can finance new vehicles from their industrial banks; Medallion Bank finances taxi medallions. Nelnet and Sallie Mae will issue student loans and Optum Bank administers health savings accounts and flexible spending accounts. Square Financial Services offers small business loans.

“The companies or entities that form these banks — they're very much niche banking,” said Frank Pignanelli, executive director of the Industrial Bankers Association. “They are, for the most part, servicing or lending to a selective group of customers: small businesses or to consumers, based on where they work or the products they use.”

Today, industrial banks are a relatively small piece of the banking industry, but more could join their ranks soon. Several companies have applied for ILCs since the beginning of Donald Trump’s presidency; most recently, this includes PayPal Holdings’ December 2025 application for PayPal Bank and Affirm Holdings’ January application for Affirm Bank. Renewed interest in this charter from a variety of enterprises — auto manufacturers, payment firms and consumer finance companies — led the Federal Deposit Insurance Corp. to issue a request for information in July 2025 as to how it evaluates the statutory factors of the ILC applications it receives. Suddenly, and not for the first time in the last 12 months, a decades-old charter that had seen little application activity was rejuvenated by prospective applicants seizing the moment.

|

If it Walks Like a Bank…. |

Industrial banks in the United States date back to 1910, with Arthur Morris’ establishment of the Fidelity Savings and Trust Co. of Norfolk, Virginia, according to the FDIC’s RFI. Banking was very different in 1910; state-chartered and state-supervised entities like Morris Plan banks made short-term uncollateralized loans to consumers when few banks were doing so, according to the Virginia Museum of History & Culture.

In 1987, the Competitive Equality Banking Act “generally made all banks that were insured by the FDIC ‘banks’ for the purposes of the [Bank Holding Company Act], with certain exceptions, including industrial banks that meet certain statutory requirements,” according to the FDIC. That exclusion makes ILCs extremely attractive to commercial and financial firms: corporations can control an industrial bank without being subject to activity restrictions outlined in the BHCA or Federal Reserve Board supervision.

Under CEBA, industrial banks must meet one of three conditions: not accept demand deposits, have less than $100 million in assets, or “another company has not acquired it since August 10, 1987 and be chartered in one of six states that prior to March 5, 1987 required FDIC insurance,” according to a 2025 study about industrial banks from researchers at the University of Utah that was funded by the university’s Fintech Center. That bit about “the six states as of 1987,” coupled with no interest rate ceilings, is why so many applications today are domiciled in Utah.

But the parent corporation can’t do whatever it wants with the bank unit. ILCs have laws and regulations that govern their relationship to and transactions with their parent companies and affiliates. They can’t fund or backstop their commercial parent companies, and parent companies must capitalize the bank and agree to act as a source of strength; Pignanelli said mandated capital ratios can be quite high. “[Industrial banks] and other banks have similar activity restrictions to ensure there is no unfair competition stemming from government subsidies to lower the capital costs of banks,” according to the University of Utah study.

In other legal and operational ways, ILCs are like any other state nonmember bank. The FDIC specified that they are generally subjected to the same restrictions, requirements, regulatory oversight and safety and soundness exams. They must comply with laws and regulations related to anti-money laundering, consumer protection and fair lending, the Community Reinvestment Act, information technology and trust services. Deposit insurance allowed them to raise lower-cost funding to deploy in lending programs. The prohibition on demand deposits means most industrial banks attract NOW, or negotiable order of withdrawal, accounts or time deposits; technology has made NOW and DDA accounts indistinguishable for most consumers.

According to the FDIC, there were 23 industrial banks at the end of the first quarter of 2025 with $247.4 billion in assets. Almost half of those assets — $116.3 billion — are associated with UBS Bank USA, which is controlled by a bank holding company supervised by the Fed. Six ILCs have more than $10 billion in assets, eight have between $1 billion and $10 billion and the remaining nine have less than $1 billion. “A significant number of the existing industrial banks support the commercial or specialty finance operations of their parent company and are funded through sources other than core deposits,” the FDIC said. |

As with the national trust bank charter application surge, it’s not terribly surprising that ILC deposit insurance applications have poured into the FDIC. Interested entities rightly understand that new agency heads are more amenable to their applications and are shooting their shot.

It remains to be seen if all pending applications will be approved (but put me down on the bet futures event contract for “yes.”) But Mickey Marshall, vice president and regulatory counsel for the Independent Community Bankers of America, told me in mid-January that the trade group is optimistic that the FDIC will be “more discerning” on these applications and that it’s not “as clear cut as ‘we just want more competition.’”

He said the ICBA would ask the FDIC to review and incorporate the ILC feedback into a new rule “before making a decision on any of these applications” in its objection letter to PayPal Holdings' application. He envisioned this new rule laying out some of the groundwork for the agency, including the acceptable and unacceptable risks posed by applications. “Without that kind of clear framework, we're still operating in the dark here,” he said. “Before they make a decision, they should proceed to a rulemaking.”

I don’t think that’s an unreasonable request. And yet, that is not going to happen. On Jan. 22, less than 10 days after Mickey and I spoke, the FDIC board approved deposit insurance applications for both Ford Credit Bank and GM Financial Bank. Ford Credit’s deposit insurance application was submitted in July 2022, and GM Financial Bank’s was submitted in January 2025.

The proposed business models of both Ford Credit Bank and GM Financial Bank would provide automotive financing through independent dealers; both intend to gather funding through retail savings accounts and time deposits on their respective banks’ websites and mobile apps. Both banks are also required to maintain a minimum 15% tier 1 leverage ratio, and their respective parent companies are required to support their bank unit’s capital and liquidity positions, the FDIC release said. Ford will be required to have $1.5 billion of paid-in capital; GM is required to have $667 million.

I was surprised by the announcement and what it means for how the FDIC will proceed. It wasn’t clear last summer if the RFI was a de facto pause on application assessments until the FDIC published any updates. It is now. The FDIC is assessing the deposit insurance applications it has received for proposed ILCs; it is also maybe digesting feedback on the information it asked for at the same time. It’s not clear if it will make any changes to its process and how that would impact other pending applications, but for now, the board approved these two insurance applications.

But these actions don’t settle the debate about these charters, their structures, their addressable market and the competition they pose. They might even inflame it. We’ll look at this debate — and how worried banks should be — in a future newsletter. |

|

|

How is your financial institution capitalizing on its largest revenue opportunity: commercial payments and treasury management?

I’m writing a report focused on how modern technology can fuel growth and revenue opportunities within treasury management, but I need your help.

- What capabilities are most important to your commercial clients?

- How good is your existing technology, and what factors are limiting your growth?

-

What do you care most about when it comes to technology partners in this area?

It’s short and anonymous, and I would LOVE your input. You can fill it out here. Thanks! |

What I’ve been reading, watching and listening to this week: |

🏒 I know I seem normal, but: a percentage of my brain is now preoccupied by “Heated Rivalry” and so I loved this article from The Wall Street Journal about how Bell Media, the television studio behind the production, made it. (The joke is that Jacob Tierney had five Canadian dollars and a dream.)

🐊 A new paper looked at how alligators in South Florida unexpectedly adapted to development in their habitat with the aid of … wait for it … jet skis, according to this Defector article. Come to learn about evolution and adaptation, stay for the photos.

🎧 In the latest episode of Bank Nerd Corner Squared: Alex and I chat about the M&A sub-trend of fintech buying banks, President Donald Trump’s proposal to cap credit card interest rates at 10% and the subpoenas sent to the Federal Reserve Board. I also have a small rant about news in the credit card space.

🛬 Catch me at: the 2026 Fintech Xchange, hosted by the University of Utah, from Feb. 4-6.

|

Thanks for reading! As always, let me know your thoughts. Also, if you’re keeping track at home, I received my first check of 2026 last week. 😐 – Kiah |

| |

Get your brand in front of 60,000+ financial services execs. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|