{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Hi All,

If Donald Trump’s administration cared about its own legitimacy in the eyes of the American people, all of its representatives and spokespeople would have said variations of the same thing after Alex Pretti, a 37-year-old intensive care nurse, was shot and killed by Border Patrol agents in Minneapolis: “We are shocked and horrified by Mr. Pretti’s death. We are working to understand why this happened, and we will ensure that anyone who acted illegally or recklessly will be held responsible.”

That’s not what they said.

Instead, Stephen Miller, White House Deputy Chief of Staff for Policy and Homeland Security Advisor, tweeted, “A domestic terrorist tried to assassinate federal law enforcement,” and Kristi Noem, the Secretary of Homeland Security, said, “This looks like a situation where an individual arrived at the scene to inflict maximum damage on individuals and to kill law enforcement.”

Let’s be perfectly clear. It would have been profoundly irresponsible to say these things before a full and impartial investigation, even if you had strong reason to believe they were true. And there is ZERO reason to think they are true. Video evidence shows that Pretti approached the scene to aid a woman, holding only a phone in his hands. And while he was carrying a gun (legally, he was licensed to carry a concealed weapon), he never brandished it and was disarmed by border patrol agents *before* being shot by them, multiple times, while in a prone position.

The Trump Administration is lying. And they are lying with such a flagrant disregard for the plain and self-evident truth that there is absolutely no reason for any of us to believe anything they say. Not about immigration. Or crime. Or law enforcement. Or its respect for the Second Amendment to the U.S. Constitution. Not about anything. Kristi Noem should be impeached. Stephen Miller should be fired. And Immigration and Customs Enforcement should leave Minneapolis immediately.

My thoughts are with the families of Alex Pretti and Renée Good, and with all of you. - Alex |

Was this email forwarded to you? |

|

|

The Lost World (1925) chromolithograph art by First National Pictures. |

|

|

#1: This isn’t advertising. It’s a tax. |

Shopify merchants now have the ability to sell their products directly within ChatGPT. And they will pay for the privilege:

When Shopify enables sales through artificial intelligence (AI) chatbots later this month, the merchants using its platform will pay OpenAI a 4% fee on sales made through the ChatGPT checkout, on top of the fees charged by Shopify, The Information reported Wednesday, citing a Shopify spokesperson. Sales made through the chatbot checkouts offered by Google’s AI Mode and Gemini and Microsoft’s Copilot will have no additional fees, for now, according to the report. Shopify will begin making merchants’ products available through these checkout features on Monday (Jan. 26), through a data-sharing program the company announced late last year, the report said. |

4% feels a little steep, especially when you consider that it is being charged in addition to all the other fees that merchants are already paying Shopify (which, at minimum, will likely include a payment processing fee of at least 2.9% + 30¢ per transaction).

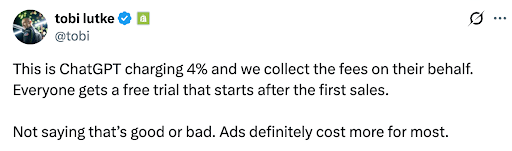

But not so fast, says Shopify CEO Tobi Lutke:

|

“Ads definitely cost more for most.” That’s an interesting point, and worthy of interrogation. But first, some quick background.

This functionality is being enabled through ChatGPT Instant Checkout, which lets a shopper discover a product in a ChatGPT conversation and complete the purchase without leaving the chat. When a merchant has opted in via Shopify, ChatGPT can show real-time product details (price, availability, variants) and handle checkout using a built-in payment flow (powered by Stripe). If the user completes the purchase inside ChatGPT, the order is routed to the merchant’s existing Shopify backend for fulfillment, and OpenAI takes a 4% fee on the transaction for enabling the in-chat checkout experience; if the user clicks out to the merchant’s site instead, that fee does not apply.

Putting our merchant hat on for a moment (and accepting Lutke’s premise that this is just a different, cheaper form of advertising), here are a few questions I would ask: -

For products purchased with Instant Checkout, does the merchant have any visibility into who the customer is? Do they have any ability to communicate with that customer or build a relationship with them that will lead to additional (cheaper) sales in the future?

-

Can Shopify or OpenAI prove that they drove an incremental sale for the merchant? Or is OpenAI simply capturing and monetizing a customer who would have found the merchant either way?

-

Can OpenAI explain to the merchant why their product(s) were shown to the customer? Does the merchant have any ability to target specific customers?

- Can the merchant dynamically manage the cost of participating in Instant Checkout? Can they set budgets or throttle spend based on volume and/or conversion rate?

From what’s been disclosed so far, the answers to these questions appear to be no, no, no, and no.

This matters. Advertising spend is typically evaluated against a predicted lifetime value. Merchants are often willing to pay a meaningful percentage of revenue up front because they expect to recover that cost over time through repeat purchases and direct relationships. Instant Checkout, by contrast, appears to monetize a single transaction while potentially severing the customer relationship that creates long-term value.

With Instant Checkout, OpenAI is effectively selling merchants’ products to its own users, while leaving merchants with no control (beyond an opt-in), no visibility, and no ownership of the resulting customer relationship — even when that customer may well have found the merchant without OpenAI’s help. That’s not advertising. That’s a distribution tax — one paid on top of the costs merchants already bear for logistics, payment processing, and, yes, advertising. |

#2: You Can’t Spell “Haven” Without “Aven” |

Aven, the fintech company focused on unlocking HELOCs as a source of credit, has helped to start a credit union:

In an apparently unprecedented move, Sadi Khan, the 40-year-old CEO and cofounder of fintech startup Aven, says he and the company are donating "a few million dollars" to launch a new federal credit union. While the not-for-profit credit union will be independent, Khan hopes it will offer Aven products to its members and will advance his stated goal of lowering borrowing costs, particularly for homeowners.

Aven, based in the San Francisco Bay Area, offers credit cards grafted onto home equity lines of credit (HELOCs) of up to $400,000. The new financial institution it’s sponsoring, Haven FCU, will be based in Silicon Valley’s Santa Clara. Khan expects Haven to start offering digital banking products this year and to open a physical location over the next 18 months. He says the credit union’s management team will decide how many branches it opens.

|

Wow. This is weird as hell, and I am here for it!

For those who don’t know (which included me until very recently!), starting a de novo credit union often involves one or more “sponsors” — companies, associations, or groups of individuals — who provide the initial capital, help assemble a founding board and management team, and define the proposed field of membership and business plan. Those resources are effectively donated: the credit union is a not-for-profit cooperative owned by its members, not the sponsors. Once approved, the credit union operates independently. However, it can choose to partner with the sponsors for products, technology, or distribution — so long as the NCUA is satisfied that the CU remains member-focused and not controlled by the sponsor.

Aven is sponsoring Haven, which means that, technically, it will have no control over what the credit union does (this is why Kahn said the credit union’s management team will decide how many branches it opens). However, practically speaking, Aven will have a tremendous amount of influence over Haven’s decisions. Khan and one other Aven employee will sit on the credit union’s five-person board of directors. What will they do with this influence?

Jeff Kauflin at Forbes mentions a few possibilities in his article, including Haven selling Aven’s products to its members and Haven originating and buying Aven’s loans (thus helping Aven lower its funding costs).

I think both of these options are likely, but the sequencing is important.

Kiah Haslett (who originally shared this story with me) pointed out that Aven’s flagship product (a HELOC-linked credit card for prime and super-prime consumers) is a tough short-term fit with Haven’s primary field of membership (underserved consumers in California’s Santa Clara and San Mateo counties). Haven needs to acquire those members, help them get their finances to a place where homeownership is feasible, help them buy houses, and then wait till they build up enough equity in those homes to make the Aven home equity card a compelling option. That’s a long road to walk! Too long, quite frankly, to justify donating a couple of million dollars to start a credit union.

This is where the second option (originating and selling loans through Haven) comes in. Haven could become the primary originating partner for Aven (the company currently works with Coastal Community Bank).

When credit unions get into BaaS or other types of embedded finance partnerships, they need to “memberize” the fintech companies’ customers, because credit unions can only serve consumers who are members. While this may seem tricky in theory, it’s actually quite straightforward in practice. To originate a loan, Haven would first need to “memberize” an Aven customer by fitting them into Haven’s approved field of membership. For borrowers who live in Santa Clara or San Mateo counties, that’s automatic. For everyone else, Haven could rely on its associational fields of membership: borrowers could become members by joining the Community Impact Fund or the California-based homeowners association that Haven serves — both national organizations that are inexpensive and easy to join. Once the borrower qualifies, Haven opens a small “membership share” account — often as little as $5 — which legally converts the borrower from a customer into a member-owner of the credit union. At that point, Haven can originate the loan.

“But wait,” I hear you saying. “Why would Aven go through all of that work just to tap into Haven’s presumably small balance sheet? How many loans could Haven realistically take on?”

Not that many! However, as one of the brilliant members of the Fintech Takes Network pointed out during our most recent monthly Office Hours event (Editor’s note: Office Hours is a ton of fun. If you want to join the next one, apply for a Plus membership!), credit unions can sell their loans — or pieces of them — to other credit unions, without borrowers needing to become members of every credit union that ultimately holds the loan. In other words, Haven’s small balance sheet becomes a regulatory on-ramp to the roughly $2 trillion in deposits held by U.S. credit unions — institutions that, as not-for-profits, are often more focused on steady asset growth than on maximizing returns.

My guess is that Aven will strongly suggest to Haven that it get into the BaaS and loan participation business soon, with a partnership to distribute Aven’s products to Haven-acquired members coming at some point down the road. |

#3: Stop Thinking of Credit Cards as a Single Product |

A couple of large credit card issuers are, apparently, taking President Trump seriously, if not literally. Bloomberg reports:

Bank of America Corp. and Citigroup Inc. are exploring options they could offer up as an olive branch to satisfy President Donald Trump’s demand to cap credit card interest rates at 10% for one year.

Both banks are separately mulling offering cards with a 10% rate as one potential solution, according to people familiar with the matter who asked not to be identified citing private information. |

Well, this was predictable. National Economic Council Director Kevin Hassett had already floated the idea that issuers might voluntarily offer new “Trump cards” with a 10% rate cap, and it appears that at least a few of them are exploring it as a way to appease the President and forestall more drastic executive actions. As I wrote about last week, this is all very dumb.

Credit cards are complex. We should think of them less as a single financial product and more as three different financial products, smashed into one very complex product construct, with a blended business model that is very tricky to untangle.

A credit card is a very safe and rewarding payments tool, allowing users to easily buy products and services online and in person. It is a strategic financing tool, allowing users to stretch out the costs of expensive purchases and better manage their finances. And it is a very flexible emergency liquidity tool, allowing users to bridge cash flow gaps.

The first product is quickly becoming its own high-cost video game/status competition. The second product is being disrupted by the growth of point-of-sale lending and its integration into debit cards (Affirm just announced a partnership with Fiserv on this front, following an earlier partnership with FIS).

And that leaves the third product — a highly flexible emergency liquidity tool.

This is the tough one. It’s very useful to have an open line of credit that you can use for pretty much any expense, at any time. However, it’s also extraordinarily risky for credit card issuers. Take me as an example. My credit card issuer needs to evaluate (and constantly re-evaluate) the risk of giving me on-demand access to tens of thousands of dollars. Am I likely to lose my job? If I lost my job, how soon would I turn to my credit card as a source of liquidity? How long would it take me to get a new job? Would it pay as much or more than my previous job? How likely would I be to repay the debt that I had accumulated while I was unemployed?

And that’s just job loss, which is a comparatively easy risk to evaluate. What happens if I get sick or injured?

The list of risks that lenders offering unsecured, open-to-buy lines of credit need to worry about is ridiculously long. And in order for them to be willing to take that risk, lenders need the ability to price it and to hedge it. Credit card issuers price risk using individual, risk-based pricing models, which determine cardholders’ credit limits and interest rates. And they hedge risk by smashing together three distinct products (and business models) designed for three very different types of customers and constructing portfolios that balance the risks and rewards associated with each product.

Artificially limiting issuers’ ability to price or hedge their risks may be the right thing to do from a public policy perspective, but we shouldn’t pretend there won’t be significant and unintended consequences. I’m not sure exactly what “Trump cards” with interest rates capped at 10% will look like, but they are guaranteed to be significantly less useful, less dangerous, less risky, and less profitable than the credit cards we are accustomed to. |

|

|

2 READING RECOMMENDATIONS |

I like that Adam separates the problem (credit cards don’t work well for many consumers) from the possible solutions. The President’s proposed solution is dumb, and enacting it would hurt much more than it would help.

However, I’m seeing too many folks in banking and fintech blow off this whole discussion without acknowledging how poorly credit cards work for a large number of people. To borrow some old Elizabeth Warren language on this topic, credit cards have a very poor safety rating. We should be talking about how we can improve it. |

This is a great post that gives us a (tiny) reason for optimism on a combination of topics that I normally find brutally depressing (especially today). |

Economic uncertainty shows up in the macro data and at the kitchen table. When confidence slips, financial fragility rises. My new piece explores why persistent uncertainty has become a risk factor itself, and how insurance design (one of the few tools designed to convert ambiguity into confidence at the payment level) must respond in kind.

*this rec is brought to you by one of our fantastic brand partners

|

There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network.

The lines between banks and non-banks have never been blurrier (make sure to read Kiah’s newsletter tomorrow for more details!), and I’m curious which of these models you think will become more popular and less popular over the next couple of years: A.) Existing banks getting into BaaS.

B.) Tech companies or entrepreneurs buying banks to get into BaaS. C.) Fintech companies or other non-banks buying banks.

D.) Fintech companies or other non-banks applying for bank charters. E.) Fintech companies sponsoring de novo credit unions (apparently, this is a thing!)

F.) Banks buying fintech companies. These obviously aren’t mutually exclusive, but I’m curious to hear which you think are waxing and which are waning. If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network

|

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 56,600+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|