{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Friday, Fintech Nerds!

Well, it has been A WEEK. If all of 2026 is going to be like this, I may need to make some significant adjustments to my personal and professional habits (starting with time spent on Twitter). Today’s topic is a fun one … if you’re a nerd about fintech, banking, crypto, and public policy, which I know all of you are! I hope you enjoy it! - Alex

P.S. — For my banking friends, I’m considering hosting an intimate AI event for banking leaders during NY Fintech Week. Trying to get a sense of who might be interested. If you’re keen to come, let me know here.

|

Was this email forwarded to you? |

|

|

Who Gets to Give People Money?

|

This week, the U.S. Senate Banking Committee was scheduled to vote on the Clarity Act, which would have advanced the bill to the Senate floor.

The bill, which congressional staff have been working on for months, aims to define regulatory jurisdiction for crypto between the SEC and the CFTC, and create a federal framework for overseeing digital-asset markets. It would materially reshape compliance obligations for all players in the crypto space, including exchanges, stablecoin issuers, and DeFi platforms.

That vote did not happen because, at the last minute, Brian Armstrong, CEO of Coinbase, said he did not support the latest draft:

|

Two things about this are interesting to me.

First, other crypto companies, trade associations, and lobbying organizations are PISSED about Coinbase’s sudden decision to oppose the bill. Sander Lutz at Decrypt reports: Crypto policy leaders have scrambled Thursday to voice their commitment to the bill and mitigate what some see as the damage done to its chances of passage by Coinbase’s abrupt about-face. “They’re on an island here,” one crypto policy insider told Decrypt, speaking of Coinbase.

Second, although he lists a number of concerns about the current draft of the bill, Armstrong’s decision to oppose it is reportedly centered on a single issue. Here’s Sander at Decrypt again:

Coinbase’s last-minute decision to protest the bill likely centered on an ongoing battle between crypto companies and the banking lobby over stablecoin yield—one Coinbase appears to have felt it was starting to lose.

The banking industry has pushed hard to add language to the market structure bill limiting the ability of crypto companies to offer yield, essentially rewards similar to interest payments, on stablecoin holdings. … As of Tuesday, Decrypt reported, Coinbase signaled it was willing to accept the latest bill language on the issue. But by Wednesday, it looked likely that bipartisan amendments to the bill supported by the banking lobby—which would have made stablecoin yield language more restrictive—were going to pass at Thursday’s markup, sources familiar with the matter told Decrypt.

Yield-bearing payment stablecoins! One of my favorite topics!

For today’s essay, let’s review where the prohibition on yield-bearing payment stablecoins came from, how the Clarity Act might change that prohibition, and, most importantly, why Coinbase and the banking lobby care so much about this issue. |

To understand how we got here, we need to go back to the GENIUS Act, the stablecoin bill Congress passed earlier this year.

The basic idea behind Congress’s approach to GENIUS was to treat stablecoins as safe (i.e., fully backed by stable, highly liquid assets) payment instruments, hence the term “Payment stablecoins”. Users would be able to use them to safely store funds and to make payments, but not much else. Think of them, roughly, as the on-chain equivalent of a checking account, provided by a narrow bank. Crucially, Congress did not intend for payment stablecoins to become the on-chain equivalent of a savings account. The GENIUS Act bans payment stablecoin issuers from offering yield. Issuers can earn interest on reserves and keep that income; they just can’t pass any of it on to the holders of the stablecoins. However, the problem is that the ban on yield only applies to issuers, not to the exchanges, wallet providers, or other intermediaries that sit between stablecoin issuers and stablecoin holders.

The loophole allows, for instance, Coinbase to offer rewards to customers for holding USDC while preventing Circle (the issuer of USDC) from doing so, even though Coinbase is an investor in Circle and maintains a shockingly lucrative distribution deal with them.

|

This is, quite obviously, not in the spirit of the GENIUS Act, nor is it something that the banks (which make most of their money from net interest income, the difference between the money they pay depositors and the money they charge borrowers) are happy about.

Here’s Jeremy Barnum, CFO at JPMorgan Chase, responding to a question about this concern on the bank’s Q4 earnings call (emphasis mine):

The creation of a parallel banking system that is sort of — has all the features of banking, including something that looks a lot like a deposit that pays interest, without sort of the associated prudential safeguards that have been developed over hundreds of years of bank regulation, is an obviously dangerous and undesirable thing

And to put a fine point on why it’s so dangerous and undesirable, I will tell you that JPMC reported roughly $95B of net interest income in 2025. If it has to pay more to fund its lending (because there is more competition for consumers’ deposits), that number will go down.

So, JPMC and the rest of the banking industry have gotten very involved in the lobbying efforts around the Clarity Act, hoping to close the GENIUS loophole and keep deposits where they are. |

What Clarity Would Change |

As evidenced by Brian Armstrong’s last-minute defection on Clarity, I think it’s safe to say that the banks have been winning round two of the fight over stablecoin yield. They are doing this by being smart and putting big-bank lobbying muscle (and money) behind the friendly, non-threatening faces of community banks (emphasis mine):

“This is probably one of their biggest lobbying efforts we’ve seen in a long time,” said Summer Mersinger, chief executive of the Blockchain Association, a crypto-industry group. The organization’s advocacy helped lead last year to a new stablecoin law and an executive order by Trump establishing a new crypto-regulatory framework. “They are using the community banks to deliver a message that’s really a much bigger deal for some of these larger banks,” she said.

That’s not actually true, of course. According to my calculations (using FDIC data), community banks (defined, roughly, as banks with less than $10 billion in assets) make approximately 80% of their revenue from net interest income, while the biggest banks (those over $250 billion in assets) make only about two-thirds of their revenue from net interest income.

Regardless, it’s been an effective lobbying strategy. And it produced some notable changes to the prohibition on stablecoin yield. The current draft of the Clarity Act attempts to close the GENIUS loophole by extending the prohibition on yield beyond issuers to the rest of the stablecoin ecosystem — particularly exchanges, wallets, and other crypto service providers. In doing so, it draws a formal distinction between “passive yield” and “activity-based rewards.”

On the prohibited side, the bill states that digital asset service providers may not pay interest or yield solely in connection with the holding of a payment stablecoin. In plain English, no one — not issuers, not exchanges, not wallets — is supposed to be able to pay users just for sitting on stablecoin balances. On the permitted side, however, the current draft of the bill allows rewards, incentives, or consideration that are tied to specific activities, rather than mere holding. These include rewards linked to: -

using a platform or wallet,

- making payments or transfers,

- participating in loyalty or promotional programs,

-

providing liquidity or collateral,

- or participating in governance, staking, or other network-related activities.

To return to our earlier analogy, if a GENIUS Act payment stablecoin can be thought of as an on-chain checking account, a Clarity Act payment stablecoin might be considered something closer to an on-chain checking account and rewards debit card. Some in the crypto industry have dubbed this rewards-for-using-but-not-for-holding compromise “stablecoin interchange”.

The compromise was one Coinbase appeared prepared to live with because the definitions of permitted activities that can be incentivized through rewards were so broad that they, functionally, left the GENIUS-era yield loophole in place. For example, Coinbase could have easily argued that holding USDC on Coinbase qualified for the “using a platform or wallet” activity, or subscribing to its One membership program qualified for the “participating in loyalty or promotional programs” activity.

From what I can tell, the banking lobby figured out Coinbase’s strategy to maintain this loophole and was working to line up support for amendments to the Clarity Act that would have closed it. Hence, why Armstrong reversed course.

And now it is unclear (ba-dum-tss!) where the Clarity Act will go from here.

If I had to guess, I think the crypto industry will line up behind Armstrong and Coinbase on this issue, and they will work with allies in Congress and the White House to exert pressure on banks to drop their insistence on closing the yield loophole in Clarity.

What kind of pressure, you ask?

Well, it may not be a coincidence that President Trump has recently been focusing his populist instincts on ideas that are radioactive to the big banks, such as capping credit card interest rates at 10% and lowering credit card interchange fees.

In fact, Patrick Witt, the Executive Director for the President’s Council of Advisors for Digital Assets, seemed to indicate on Twitter that if the banks didn’t get on board with the current Clarity Act draft, the White House would make the President’s credit card ideas a bigger policy priority.

Or, more bluntly, nice credit card business you’ve got there. Be a shame if anything happened to it:

|

I have no idea if this pressure campaign will work or not, or if the rest of the crypto industry (which seems happy with Clarity as is) will rally around Coinbase, but I wouldn’t blame you at this point for asking an obvious question: Is it really that big a deal if stablecoins are allowed to offer yield?

This is an excellent question, and one that has been the subject of much research and debate. So, I thought I’d end this essay by summarizing that debate and giving my take on whether yield-bearing payment stablecoins really are the existentially important threat/opportunity everyone seems to think they are.

|

Yield-Bearing Payment Stablecoins: So What? |

The reason that Coinbase wants to continue to offer yield is that it believes that giving away money is an effective customer acquisition strategy. The reason that banks don’t want Coinbase (and other crypto companies) to be able to offer yield is that they believe that it is as well. Of course, that’s not a good basis for an argument to policymakers, so Coinbase and the banks both tend to reframe the argument in more consequential, less self-interested terms.

Coinbase argues that consumers deserve yield on their money and that competition is beneficial for the market overall. The banks argue that yield has to be paid for and that the loans that banks make to consumers and businesses are the most socially useful way to do that.

So … there are a couple of different questions here that we need to pull apart and answer: - Would yield-bearing payment stablecoins cause banks to lose deposits?

- If yes, would we see less lending to consumers and businesses?

Fortunately, a lot has been written on these questions, so there’s no need to start from scratch. Instead, we can build upon the following pieces:

The first question is the most important: Will stablecoins cause deposit flight? And would adding yield into the mix accelerate that flight? |

The Impact of Stablecoins on Bank Deposits |

In their lobbying efforts, banks have consistently cited a scary-sounding estimate from the Treasury Department. Here’s a group of community banks, writing to the Senate:

Under the law, stablecoin issuers cannot pay interest because allowing inducements like interest payments, yield, or rewards could incentivize customers to park their savings not in a bank, but in stablecoins. Congress recognized that this could significantly disrupt community lending because banks use those deposits to provide individuals and businesses with the loans they need to get a home or expand a local business. Without this prohibition, Treasury has estimated that $6.6 trillion in bank deposits are at risk.

$6.6 trillion at risk, if stablecoin providers are allowed to offer yield! That’s a big number!

But is it a realistic estimate?

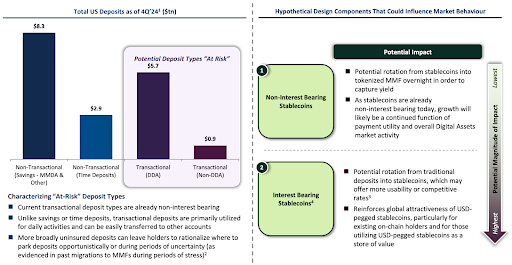

Here’s the actual slide from the Treasury research presentation, which everyone is citing:

|

Careful observers will notice that the $6.6 trillion number comes from the highlighted columns on the left side of the graphic. Those are the total deposits held in transactional (i.e., non-interest-bearing) deposit accounts by all U.S. banks at the end of 2024.

So, is Treasury saying that 100% of deposits held in checking/NOW/prepaid accounts will flow into stablecoins?

No, obviously not. It’s saying that $6.6 trillion is the total size of the domestic addressable market for non-yield-bearing stablecoins as checking account replacements. If Congress allows a yield loophole to remain open for Coinbase and others, the other side of the chart (savings accounts and CDs) would come into play as well, adding $11.2 trillion in additional deposits to that theoretically addressable market. If bank lobbyists want to mislead Congress about the disruptive threat posed by yield-bearing stablecoins, they should at least do it right. Add $6.6 trillion (transactional, non-interest bearing) and $11.2 trillion (non-transactional, interest bearing) and get an even bigger number! YIELD-BEARING STABLECOINS PUT $17.8 TRILLION IN DEPOSITS AT RISK! RUN FOR YOUR LIVES!!!!!!!! Patently absurd.

However, the other side of the debate isn’t making great arguments either.

Coinbase commissioned a report from Charles River Associates, which focuses on the impact of growing stablecoin adoption on community bank deposits (since community banks are the group that policymakers seem most motivated to protect). You’ll be shocked to hear that the report concluded that stablecoins pose little to no threat to community banks’ deposit franchises.

But how did they come to that conclusion?

Well, they compared monthly changes in community-bank deposits from 2019 to 2025 to growth in USDC market cap (used as a proxy for stablecoin adoption). Again, careful observers might notice a few problems with this approach: -

While they tried to control for macro conditions and market shocks in their analysis, the last six years were extraordinarily disruptive to banks’ deposit franchises. In that window, we had a pandemic, economic stimulus, inflation, interest-rate increases, and a regional bank crisis, just to name a few. Is it even possible to disentangle these conditions in a quantitative analysis of deposit displacement?

-

During this window of time, stablecoins were mostly non-interest-bearing. This tells us very little about the effect of a robustly competitive yield-bearing stablecoin market on bank deposits.

-

Focusing on community banks is a smart scoping choice by Coinbase, but the types of deposits that these banks have tend to be pretty sticky and relationship-based. It’s likely, in the short-to-medium term, that payment stablecoins (especially if they can offer yield) will be more disruptive to large, uninsured transactional balances, rate-sensitive cash management accounts, and institutional treasuries and high-net-worth cash sweep accounts. Community banks don’t have a lot of these deposits. The big regional and national banks do.

-

And speaking of the community banks, the report notes that their customers tend, demographically, to be older and less tech-savvy than the typical stablecoin users, which limits the potential disruptive effects on community banks. I buy that. However, and not to be morbid, but what happens when those customers die? Do community banks just die with them? A relevant question that the report could have asked is: How do stablecoins impact community banks’ ability to acquire and retain their next generation of customers?

The realistic impact of stablecoins on bank deposits will likely fall somewhere in the middle of these two extremes.

More neutral academic work (including the Whited et al. paper) suggests that allowing yield on a deposit-like digital instrument could plausibly lead to deposit losses on the order of 20–30%, which feels like a reasonable upper-bound benchmark for serious analysis. Our experience with money market funds (MMFs) — introduced in the 1970s as a higher-yield alternative to bank accounts — supports this intuition. When a non-bank product offers meaningfully better returns, rate-sensitive depositors will move. At the same time, those depositors have also historically been more prone to runs when conditions deteriorate.

That said, I still don’t think we have enough real-world data to model with confidence how stablecoins — yield-bearing or not — will reshape the deposit landscape. A few additional considerations help bound the debate: -

Banks can compete on price. Unlike the 1970s, banks are no longer barred from paying competitive rates on deposits. Regulation Q, which capped deposit rates and helped fuel the rise of MMFs, was phased out, starting in the 1980s. If stablecoins pressure deposit pricing, banks can respond by raising rates. That compresses margins, but it doesn’t imply permanent disintermediation.

- Many deposits aren’t especially rate-sensitive. Most households and small businesses aren’t constantly chasing the best yield. They value convenience, trust, bundled products, and established relationships. They are also, if we’re being honest, lazy. Yield alone — even if it’s meaningfully higher — doesn’t automatically overcome those barriers.

-

Stablecoins may not consistently offer superior yields. The yields offered by crypto platforms like Coinbase have already shown signs of compression. And if the Clarity Act expands regulators’ ability to supervise digital asset providers, it should limit the kinds of risk-taking needed to sustain above-market returns. Paying yield is easy; paying it safely and durably is not.

-

MMFs were products; stablecoins are infrastructure. For the most part, money market funds never became full-fledged transaction accounts. You couldn’t easily build a modern payments or banking experience around them. Stablecoins, by contrast, are programmable, composable infrastructure. That makes them a more serious competitive threat, particularly to banks that rely on Banking-as-a-Service (BaaS) models and fintech partnerships for deposit growth.

-

Deposits are more likely to be redistributed than destroyed (and some may be newly created). When U.S. customers move money into stablecoins, those dollars typically reappear as reserve deposits at the banks used by stablecoin issuers. That shift is likely negative for community banks but potentially a net positive for large banks that specialize in custody and institutional cash management. At the same time, stablecoins may pull new dollar demand into the U.S. banking system from abroad, as non-U.S. users acquire dollar-denominated stablecoins that must ultimately be backed by reserves held at U.S. banks. The catch is that these reserve deposits are large, uninsured, and highly rate-sensitive — very different from core relationship deposits, and generally harder to lend against safely.

- Some digital asset providers may internalize the banking function altogether. The resurgence of national trust banks means that, in some cases, stablecoin issuers or other crypto platforms may effectively become their own narrow banks — further shifting deposits away from traditional relationship-lending institutions and toward custody-centric balance sheets.

|

The answer to the second question — whether deposit displacement translates into less lending — is even murkier. The most helpful way to think about it is to think about the effect of deposit displacement on large banks versus community banks. To be honest, large banks will be fine, no matter how this stablecoin yield fight plays out.

Large banks are correctly perceived by customers and the market as too big to fail. They have lots of sticky retail deposits. They also have access to deep and relatively cheap wholesale funding markets. If they lose deposits, they can issue debt, tap brokered deposits, or lean more heavily on capital markets. That funding is more expensive than core deposits, but it is available. Lending at large banks is therefore less supply-constrained: when funding costs rise, they tend to reprice credit rather than stop lending altogether.

Lending at large banks is also, for lack of a better descriptor, coolly professional. These institutions didn’t get to be as big as they are by letting sentiment influence their lending decisions. They are data-driven, and they drive to where the ROI is greatest. If that means fewer loans for small businesses and more for large corporations (because the cost to underwrite is the same for both), then that’s just what it is.

Community banks are different.

Community banks rely overwhelmingly on customer deposits — not just as a funding source, but as the binding constraint on their balance sheets. When they have more deposits, they lend more. When deposits contract, lending contracts with them. This is not a theoretical claim; it shows up repeatedly in the data. One clean example that Andrew Nigrinis points out in his excellent paper on this subject is the shale boom era (mid-2000s), which led to sudden inflows of mineral royalties into community banks, which lowered their funding costs and expanded local credit. In fact, every dollar of new deposits produced roughly fifty cents of additional mortgage lending.

Yield-bearing payment stablecoins have the potential to put community banks in a particularly tough position: -

Stablecoin issuers’ reserve deposits do not flow to community banks; they concentrate at large custody and money-center banks, or at trust banks.

-

Community banks that have revitalized their deposit acquisition efforts through BaaS and fintech partnerships may feel the negative effects of competition from stablecoin infrastructure providers like Stripe.

-

Replacing lost deposits with wholesale funding is materially more expensive for community banks than for large banks, which directly tightens their lending capacity.

Crypto advocates often respond that this doesn’t matter because nonbank and fintech lenders (backed by private credit) have already filled much of the gap left by banks after the Great Recession, and the emergence of on-chain crypto lending can fill in the rest.

They’re not wrong that nonbanks already account for a large share of lending in certain markets, like mortgages. But this misses something important.

Community bank lending is delightfully under-optimized. It relies on soft information, long-term relationships, and local knowledge. Community bankers say “yes” in cases where a purely data-driven or securitized lending model would rationally say “no.” It’s closer to venture investing than to consumer finance — but without the power-law upside. That kind of lending is economically valuable precisely because it doesn’t scale cleanly and doesn’t fit neatly into nonbank or crypto-native models.

Crypto lending, in particular, is not a substitute. Today, it is overwhelmingly overcollateralized lending designed to support leveraged trading, not undercollateralized or unsecured lending to consumers and small businesses. While technically interesting, it does not replace the role community banks play in local credit creation. So, the most defensible conclusion is not that yield-bearing payment stablecoins would collapse lending across the economy. It’s subtler and more concerning than either side admits:

Yield-bearing stablecoins would likely shift deposits away from institutions that lend based on relationships and towards those that don’t — tightening credit in precisely the parts of the economy that depend most on it.

No one can say exactly how big that shift will be, and you could argue that it’s inevitable, regardless of what the final language in the Clarity Act says, but I’m glad that this has become such a contentious policy debate.

Deciding who gets to give people money is serious business. |

|

|

MORE QUESTIONS TO PONDER TOGETHER

|

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis.

What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

Drop your question here, whenever inspiration strikes! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network |

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 56,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|