{if hosp_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy. |

|

|

{/if}Happy Thursday Hospitalogists!

We’re 15 days into 2026. What have you done so far to get better? I’m kidding. Take a breather. Not everything has to be go, go, go.

Today we’re diving into OpenAI’s acquisition of Torch, developing AI strategies, and analyzing nonprofit health system presentations from the JP Morgan Healthcare Conference wrapping up as we speak. PS - one of the most popular resources in my community is that I upload all of the nonprofit health system presentations from JPM as they become available, so I will be making those available for Plus members within the week to help with your own strategy planning. Join here.

Enjoy! |

Was this email forwarded to you? |

|

|

Going deeper on an interesting topic, theme, or trend |

OpenAI just paid $100M for a four-person team. Here's what that tells you about the healthcare AI race. |

This piece was co-written with Rik Renard, who shares weekly insights on healthcare AI and strategy on LinkedIn. One week after OpenAI announced ChatGPT for Health, Anthropic dropped Claude for Healthcare. On the surface, same playbook: connect your health records, ask questions in plain language, get personalized answers. Claude partnered with HealthEx for the medical records part (OpenAI went with b.well). But if you look at how they're positioning, you see two completely different strategies.

OpenAI led with the consumer story. Their whole announcement was about helping people understand lab results and prep for doctor visits. The enterprise stuff—tools for hospitals, insurers, pharma—came in a second announcement as almost an afterthought.

Then this week, OpenAI acquired Torch for reportedly $100M in equity. Four people.

Torch was building an app that unified all your medical information—doctor visits, lab tests, wearables, consumer wellness tests—into what they called "a medical memory for AI." It’s the same team that co-founded Forward Health, the AI-powered doctors' offices company that raised $400M before abruptly shutting down in late 2024. So OpenAI just paid eight figures for a team that knows how to build consumer health products, even if their last company imploded. That's a bet on consumer-facing healthcare AI, not enterprise infrastructure.

Diverging Healthcare AI strategies.

Anthropic did almost the opposite. Their press release has a quote from the CTO of Banner Health. They're talking about Medicare coverage databases, ICD-10 coding systems, clinical trial platforms like Medidata. The consumer health record thing feels like obligated counter-positioning vs OpenAI, but the real story is "hey pharma companies and health systems, let's do business." This makes sense for two reasons:

1) Follow the money. Last week Chai Discovery (backed by OpenAI) reportedly signed a mid-eight-figure annual contract with Eli Lilly. That's the game Anthropic wants to play: selling software to enterprises that actually have budgets. One pharma contract can match thousands of consumer subscriptions. 2) Brand awareness asymmetry. Most people still don't know Claude exists. I was literally explaining at a party this weekend where people were discussing "Have you heard of Claude??" (they pronounced it super funny). Meanwhile everyone knows ChatGPT (230M people already asking health questions weekly). So while OpenAI fights for consumer mindshare, Anthropic is quietly building tools that pharma companies will use to draft FDA trial protocols and hospitals will use to speed up prior authorization. Different strategies. Both probably smart for where each company sits in the market. |

Nonprofit Health System Takeaways from JPM Presentations |

One of my favorite times of the year is diving into commentary out of the JP Morgan Healthcare conference and the presentations made available to get a sense of how the top quartile of health system performers (from a financial perspective) are thinking about their strategies headed into the year. From a high level perspective, these health systems are entering 2026 with strong balance sheets and strong growth across inpatient and ambulatory service lines, with plans to push forward in key specialties, developing centers of excellence, and digital engagement strategies.

So here’s a glimpse at several of the nonprofit health system slide deck presentations and how they’re pitching investors and partners going into 2026. I do want to note that I consider the slides chosen to be the more unique aspects of each health systems’ presentations. There are many, many commonalities across these players including distinct margin expansion, growth in key service lines, and a focus on ambulatory and digital transformation.

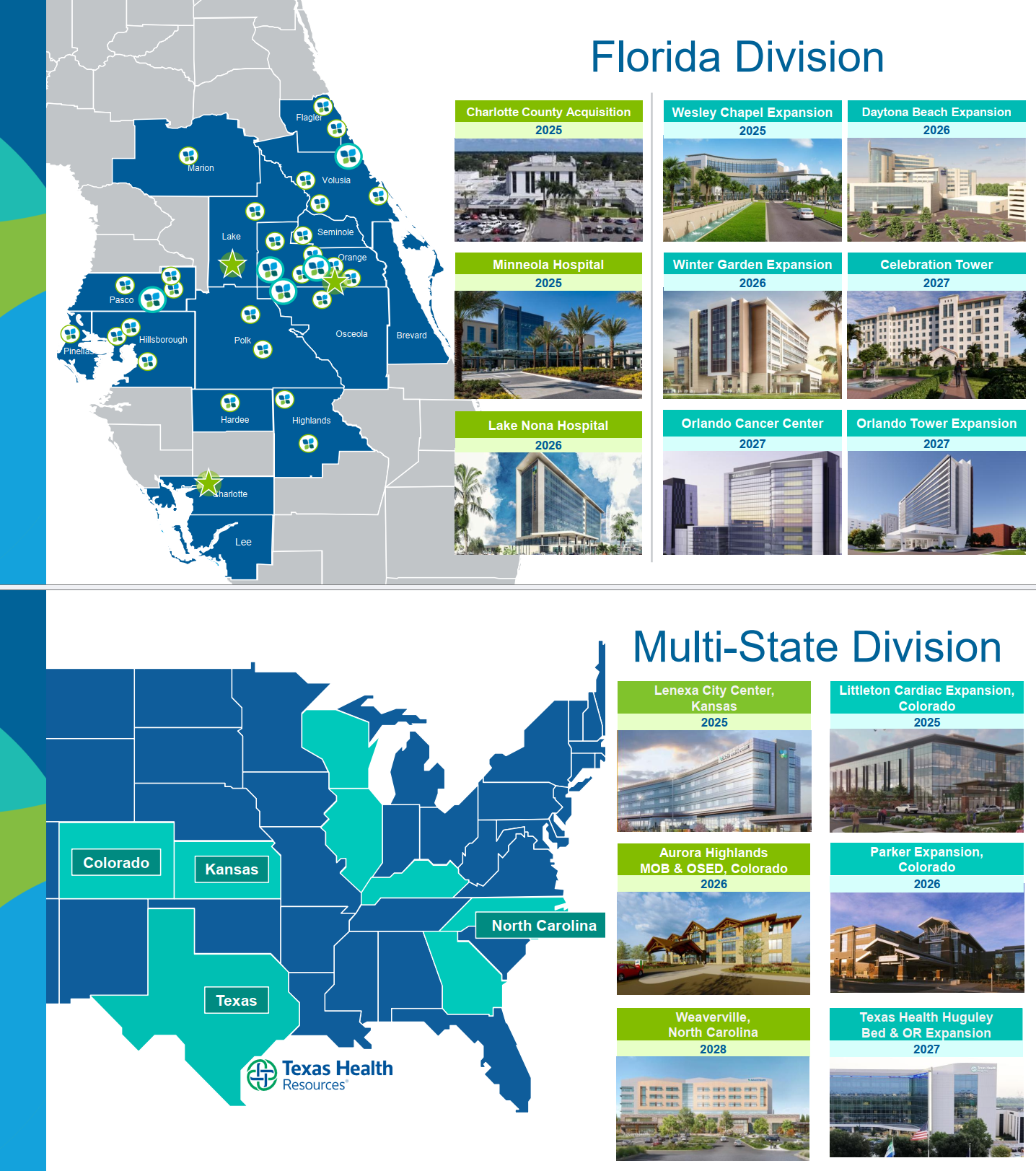

AdventHealth: As one of the most profitable health systems by operating margin, AdventHealth is nearing a whopping $24B in total revenue in 2025, placing the nonprofit at formidable size and scale (with plans to reach $31.3B in revenue by 2030), with an incredible amount of capital to invest and experiment in consumer-forward, technology driven strategies. AdventHealth’s main presence in the greater Orlando area situates it within a market that is growing like crazy demographically. Its commercial payor mix is something like 57% of revenue.

|

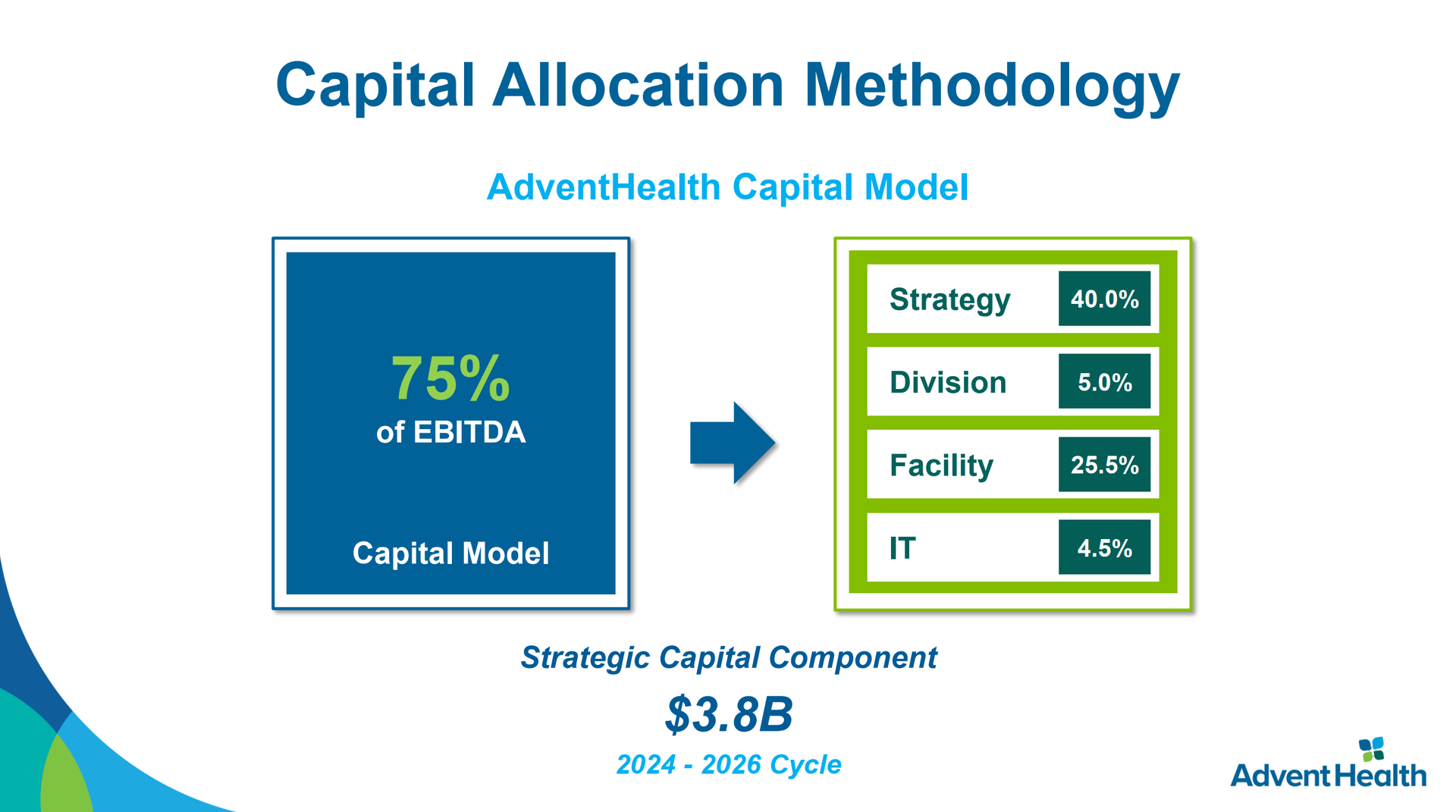

AdventHealth’s capital allocation breakdown was an interesting slide to see how a profitable, forward-thinking, consumer-centric health system thinks about where to invest its resources. |

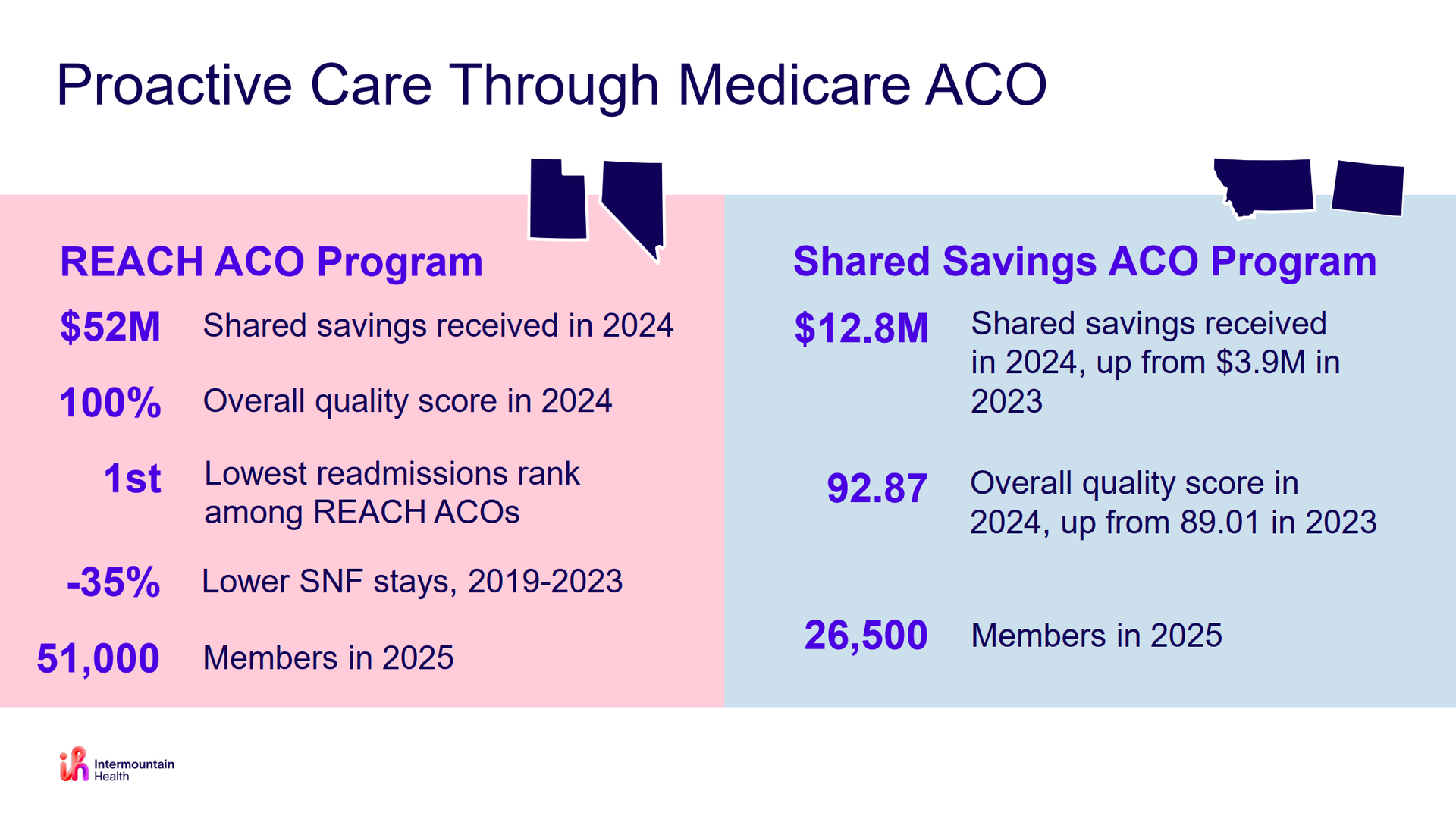

Intermountain: The baby darling of the Mountains, Intermountain’s presentation took much more of a population health-laden focus and a business as usual approach to their overall (working) strategy. On the financial front Intermountain experienced a stronger balance sheet and expanding operating and EBIDA margins. |

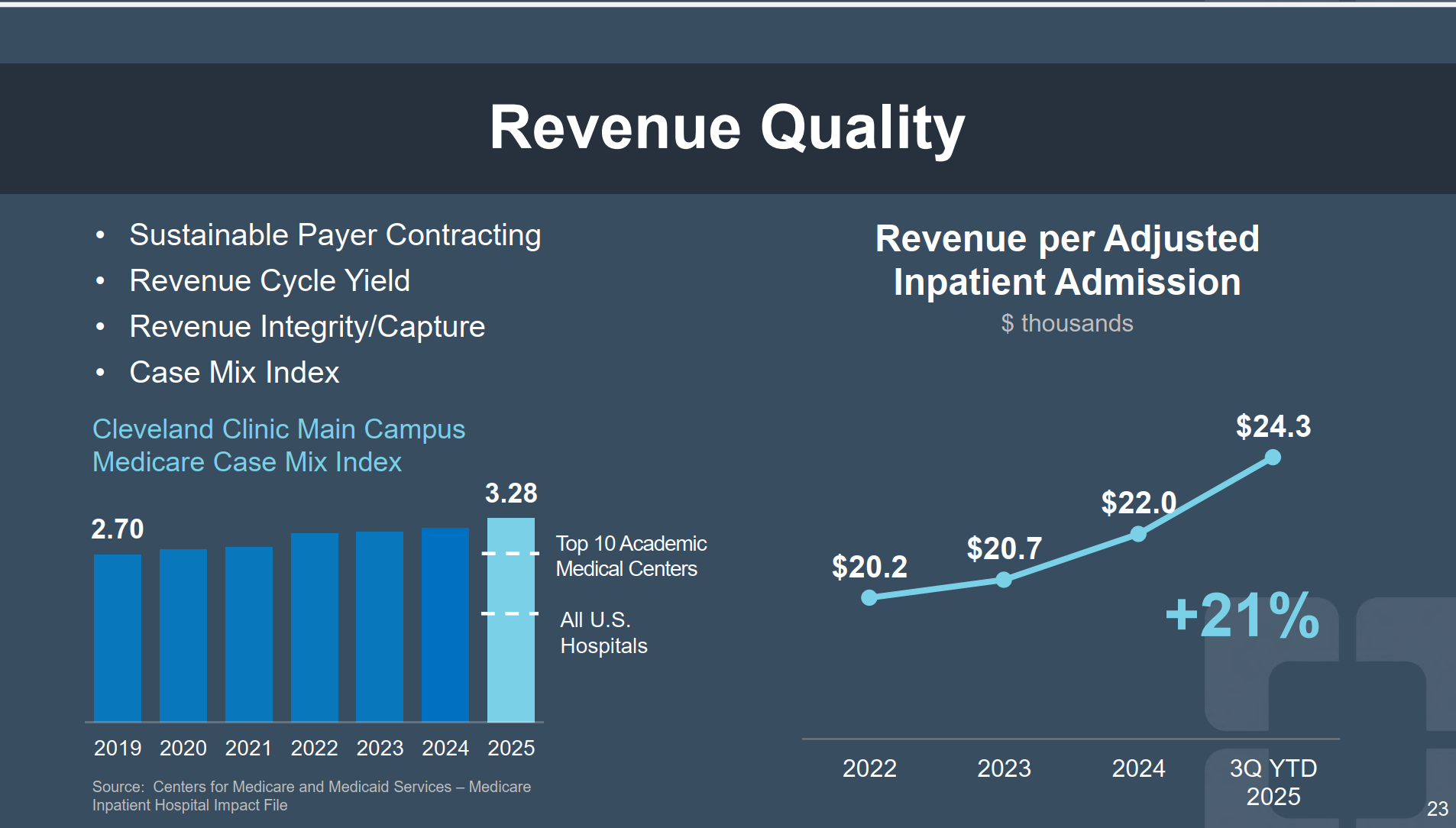

Cleveland Clinic: Apart from being in Cleveland (Browns, what are you guys doing??), Cleveland really heavily emphasized its global efforts first in its report, establishing itself as at the forefront of global healthcare innovation. It called out 4 select partners on the AI front, including Bayesian Health (sepsis), ambient documentation (Ambience), and Palantir and Akasa for operations, throughput, and CDI capabilities. On the volume front, Cleveland Clinic sees some of the MOST complex patients on the planet, and is in the top 0.1% (probably) of acuity, which is crazy.

|

Cleveland Clinic also devoted a slide to its RCM transformation, noting several partners working in tandem to make that happen. I imagine we’ll see some permeation from some of these players into the other areas listed here: |

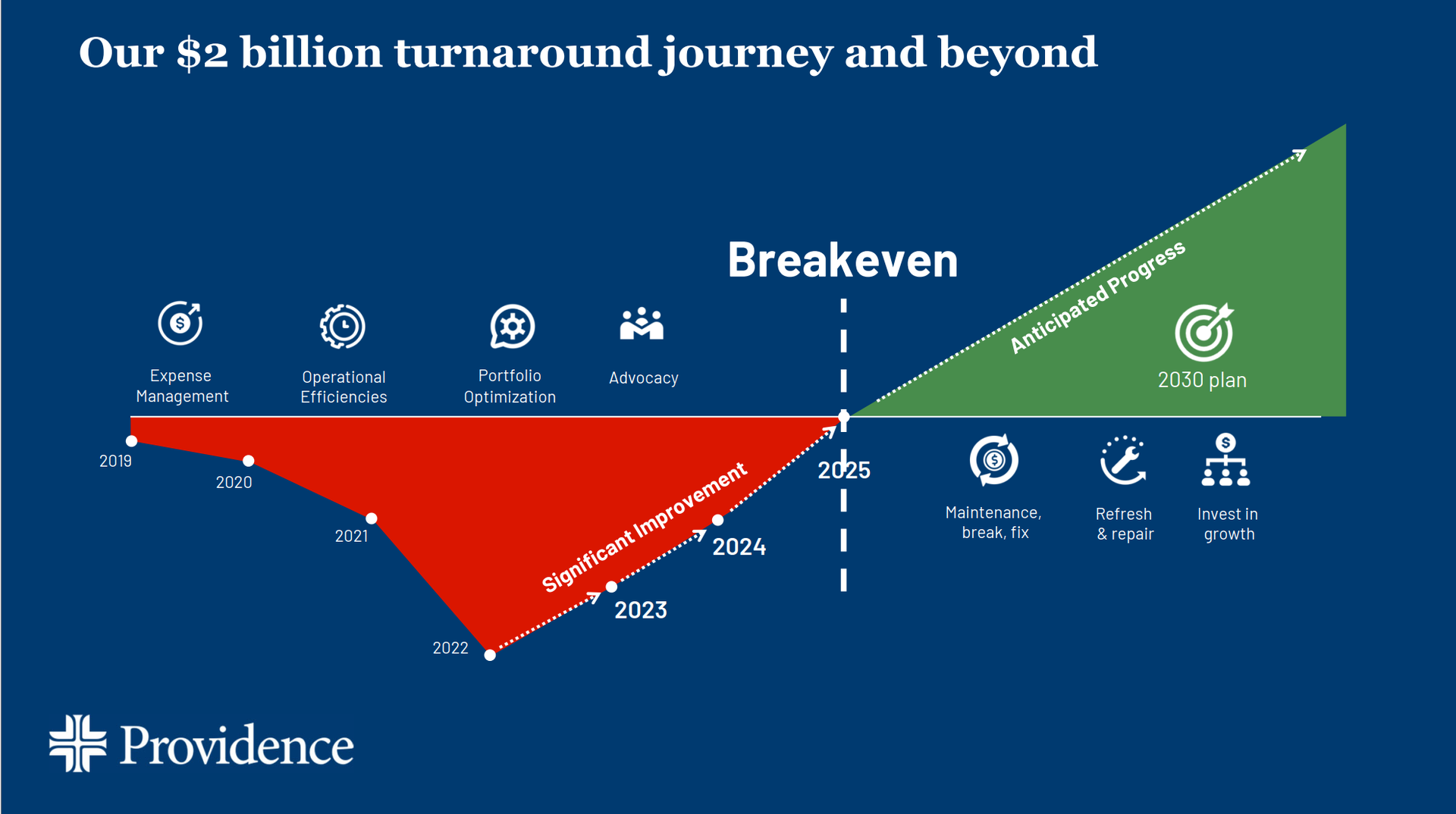

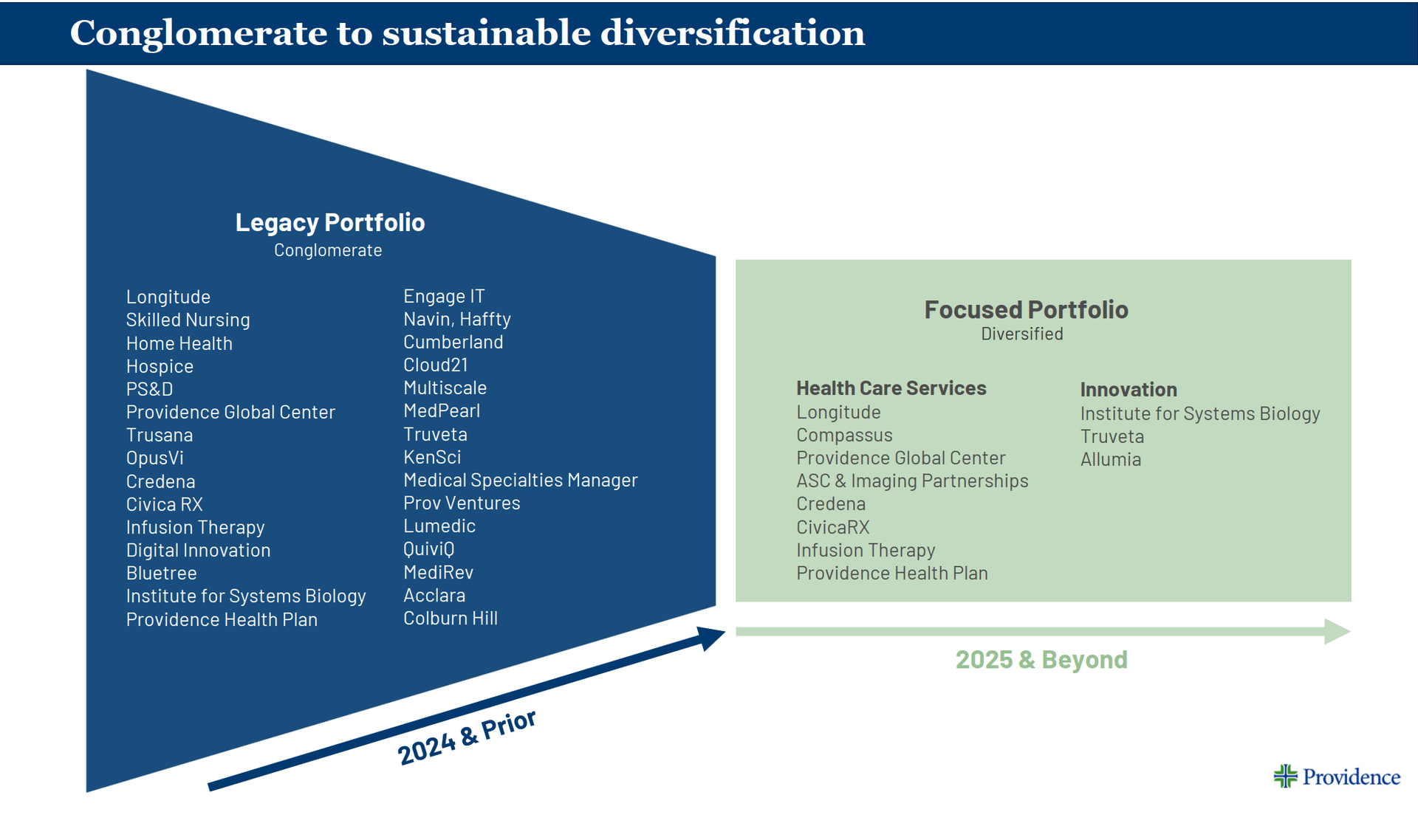

Providence: Overbloated, sprawling health systems like Providence and Ascension are spending the bulk of their time pitching their respective turnaround stories. These playbooks include initiatives like service line optimization and cost efficiencies while analyzing where they can better spend capital for better returns in the ambulatory and technology settings (and reconfiguring their portfolio in the process).

|

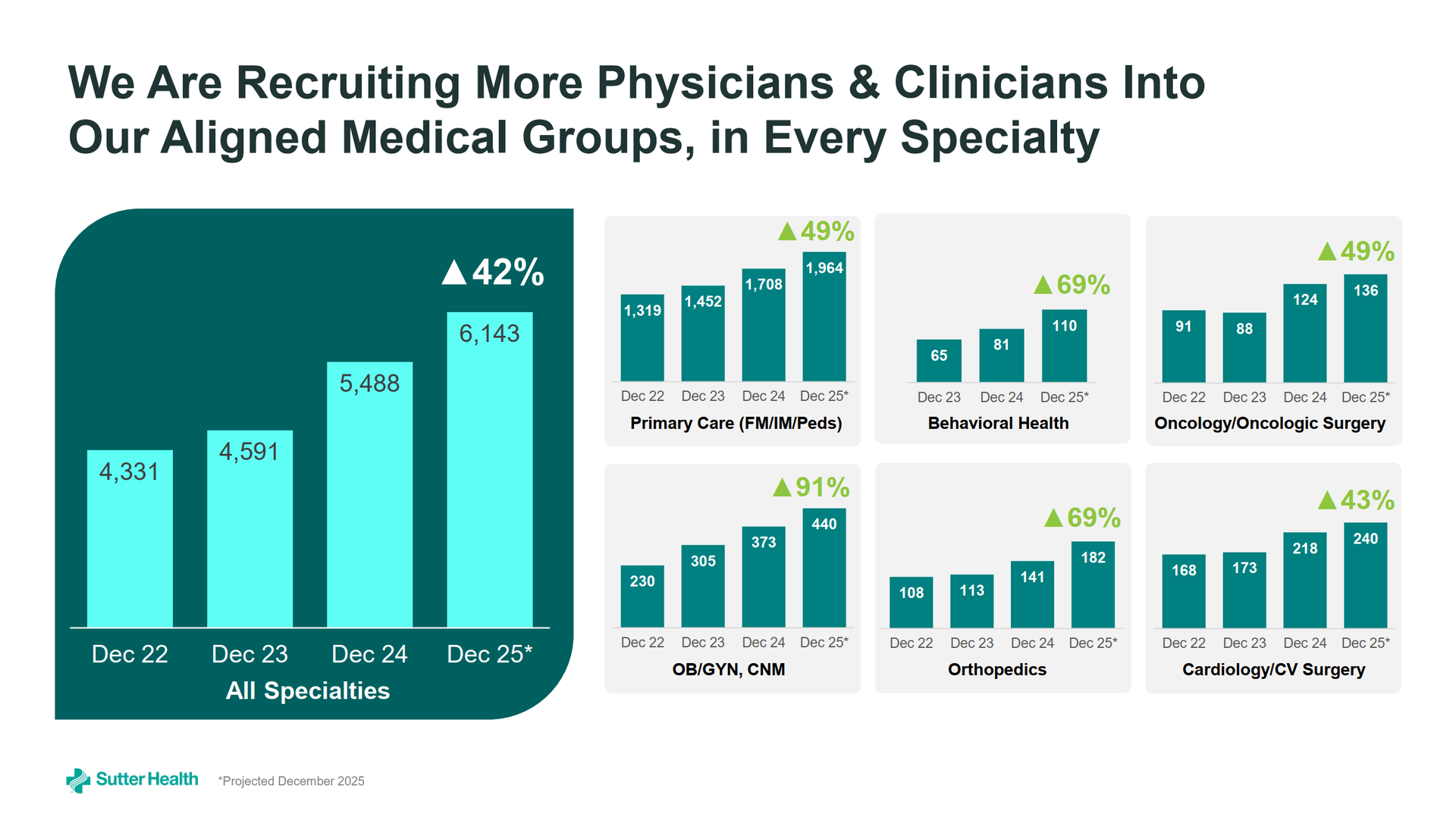

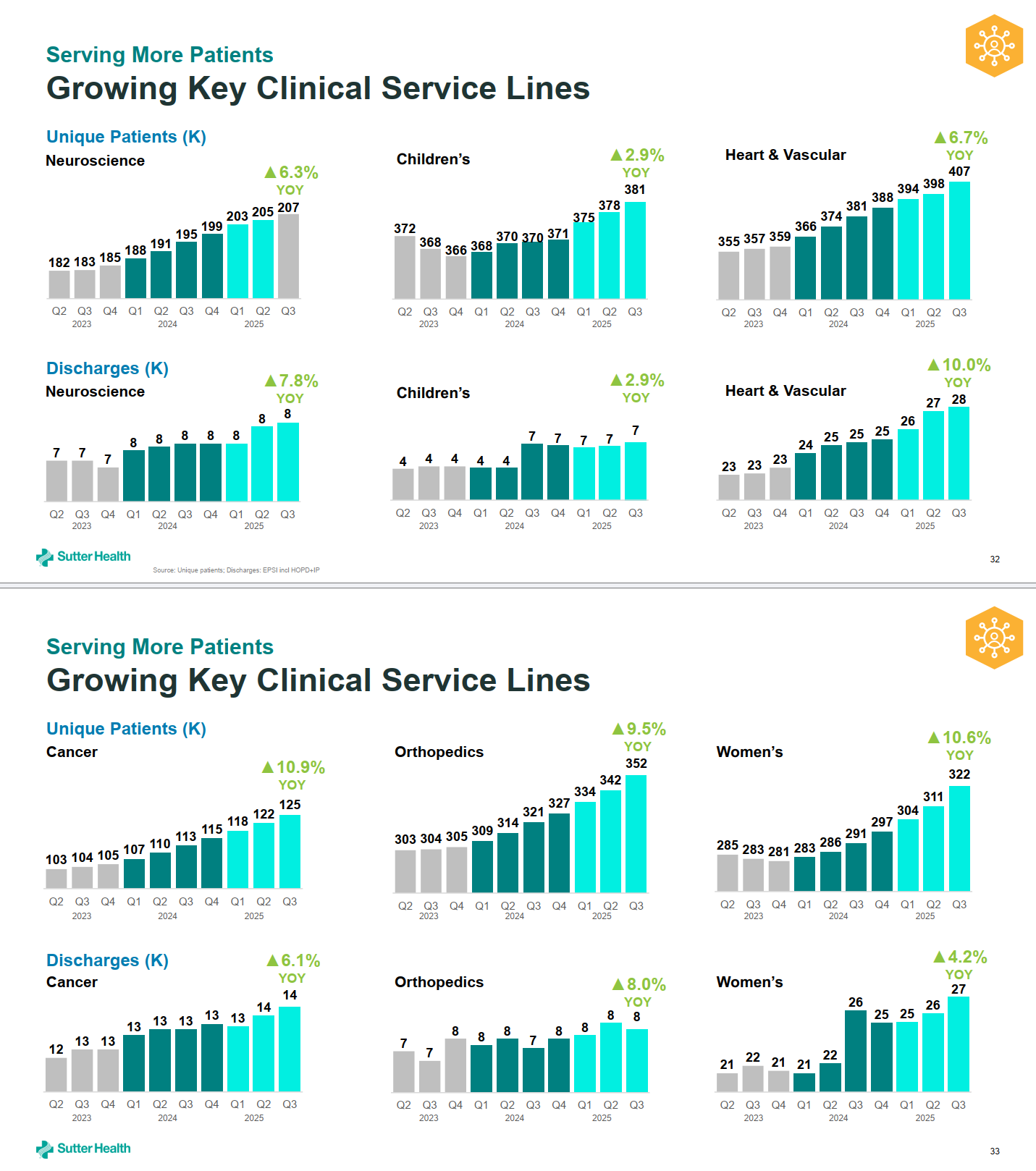

Sutter: Sutter gave an incredibly information dense deck covering key service line growth, progress on all strategic initiatives since last year, and key service line growth (and physician alignment as a key component) detailed below. Sutter also noted $450M+ of investment into ambulatory settings like urgent care, ASCs, and home health & hospice (as well as leveraging primary care as an acquisition strategy for commercial patients) along with providing updates on its digital platform - 1.2M active monthly users, up 152%, and 28% of all appointments scheduled online in 2025.

|

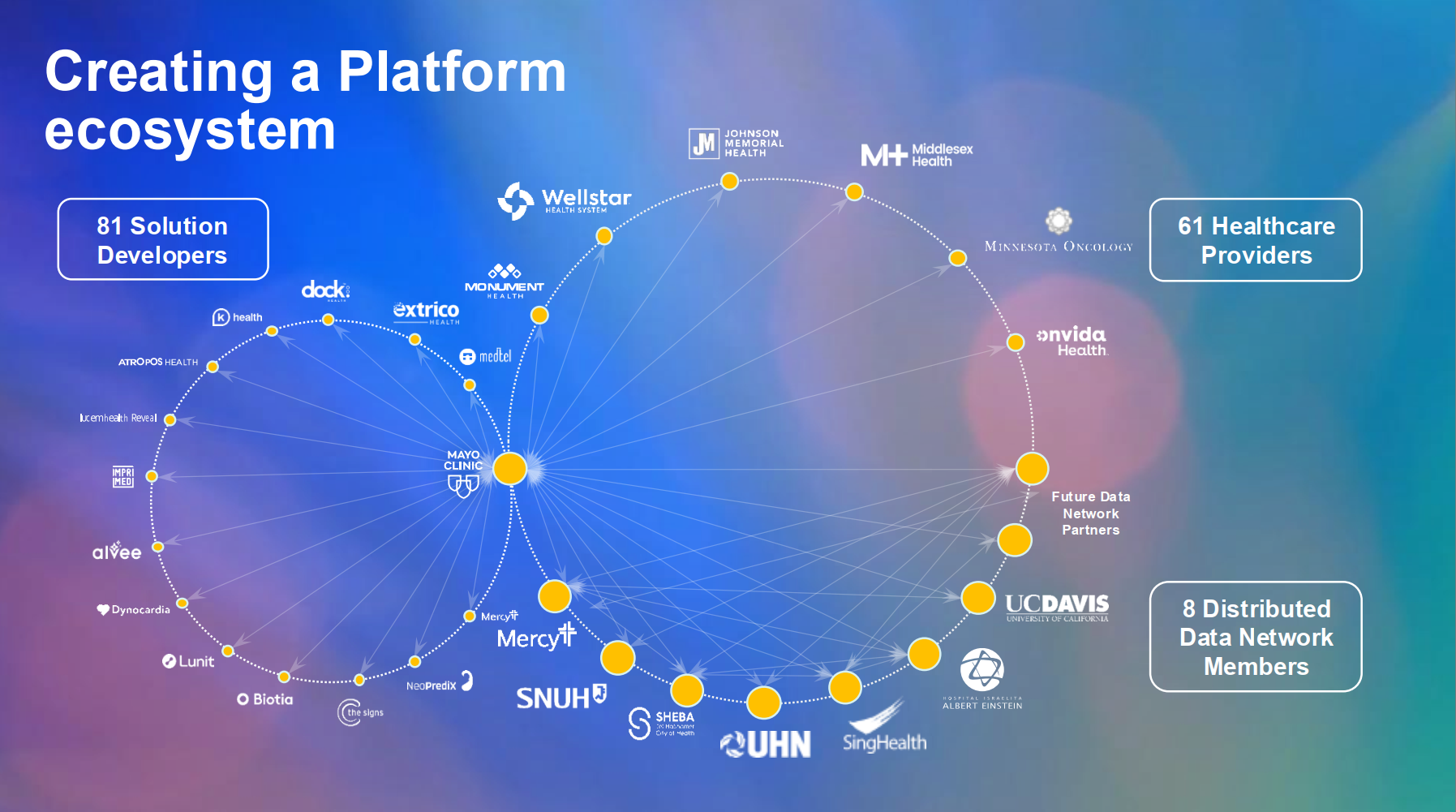

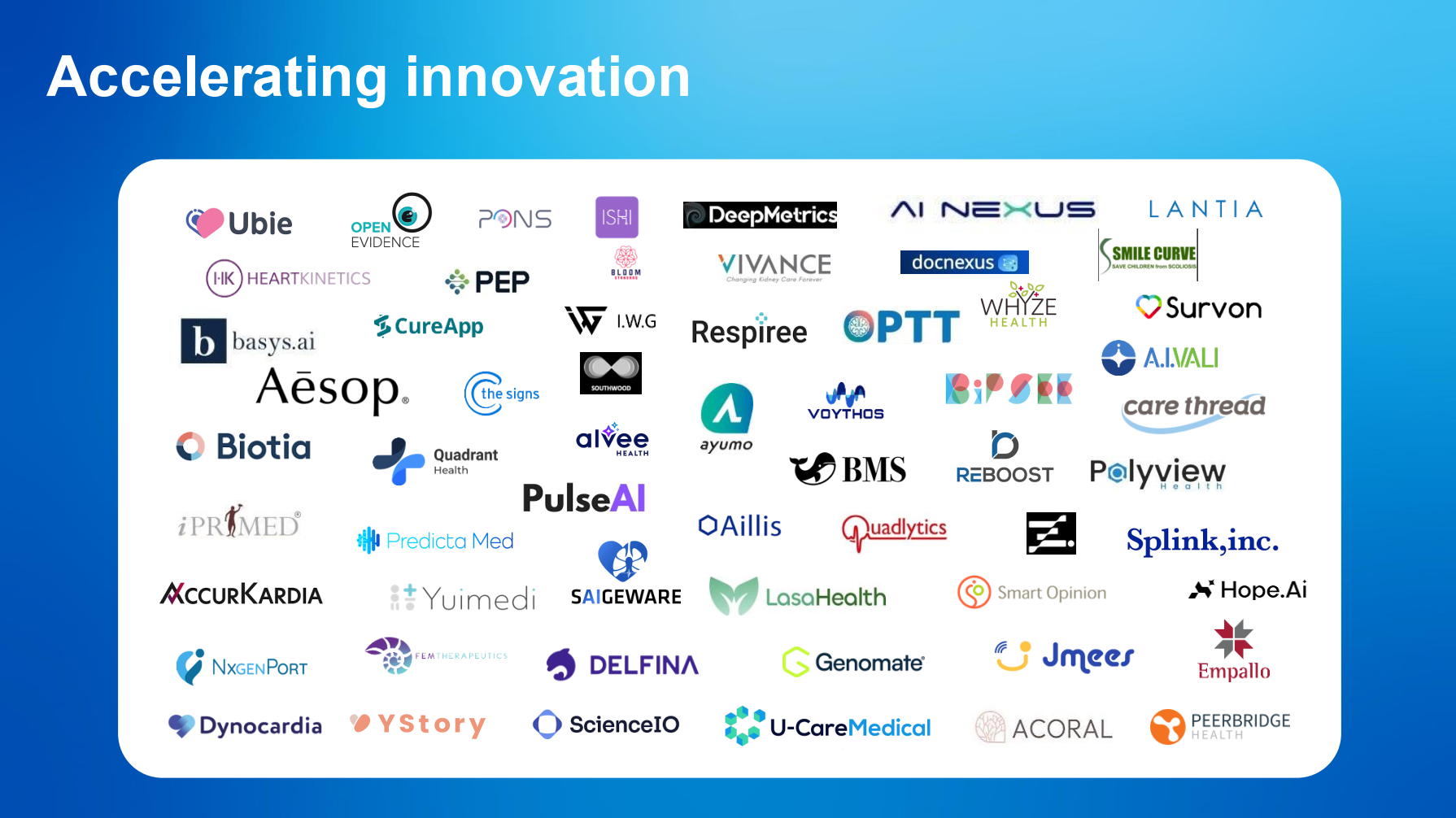

Mayo Clinic: Mayo is simply doing Mayo things. I mean, it’s like my 3rd favorite condiment, but besides that, Mayo Clinic continues to dominate. One other theme you’ll hear from health systems over the coming years (especially with AI) is that disruption comes from within, and that health systems need to disrupt themselves along with shifting to ‘platform’ or ‘enterprise-wide’ thinking, and the Mayo Clinic’s presentation led with these pillars in mind.

|

Mayo’s presentation was chock full of logos signifying how the powerhouse academic medical institution is a beacon for healthcare innovation across AI, life sciences, and more. |

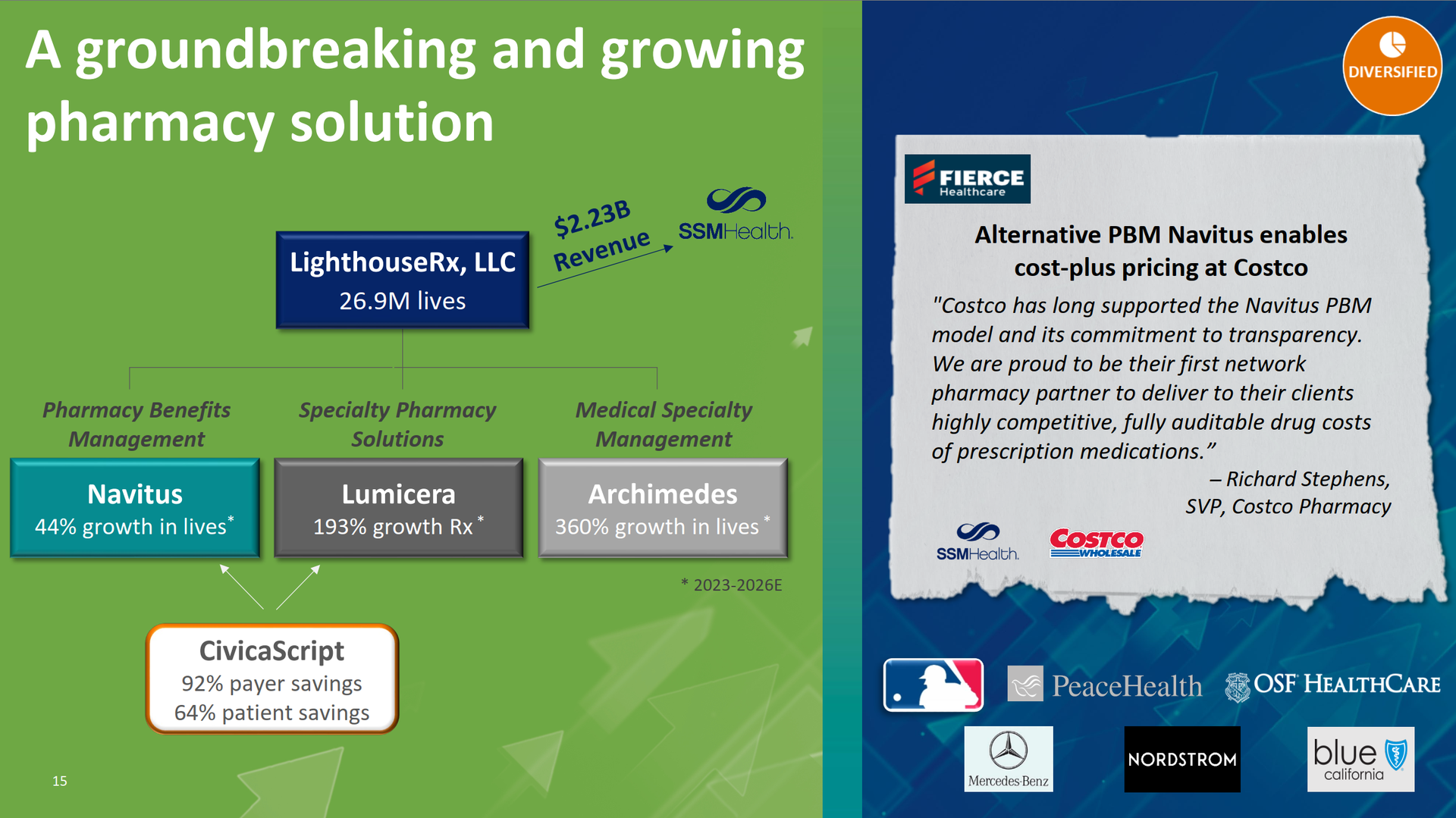

SSM Health: SSM had an interesting slide on its growing pharmacy segment - cost-plus PBM pricing, specialty pharmacy, and medical specialty management - all significant growth vectors for health systems in 2026. |

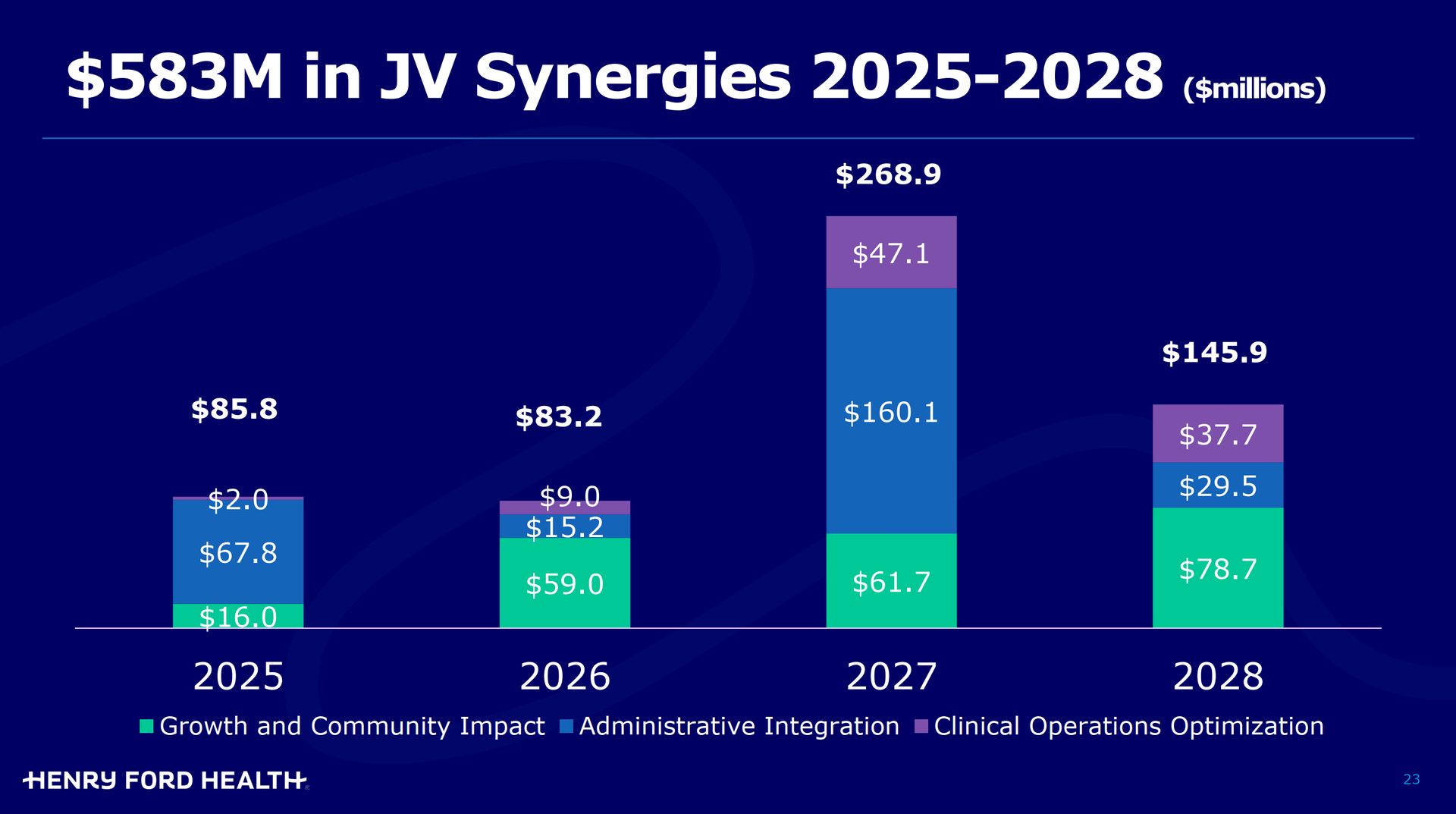

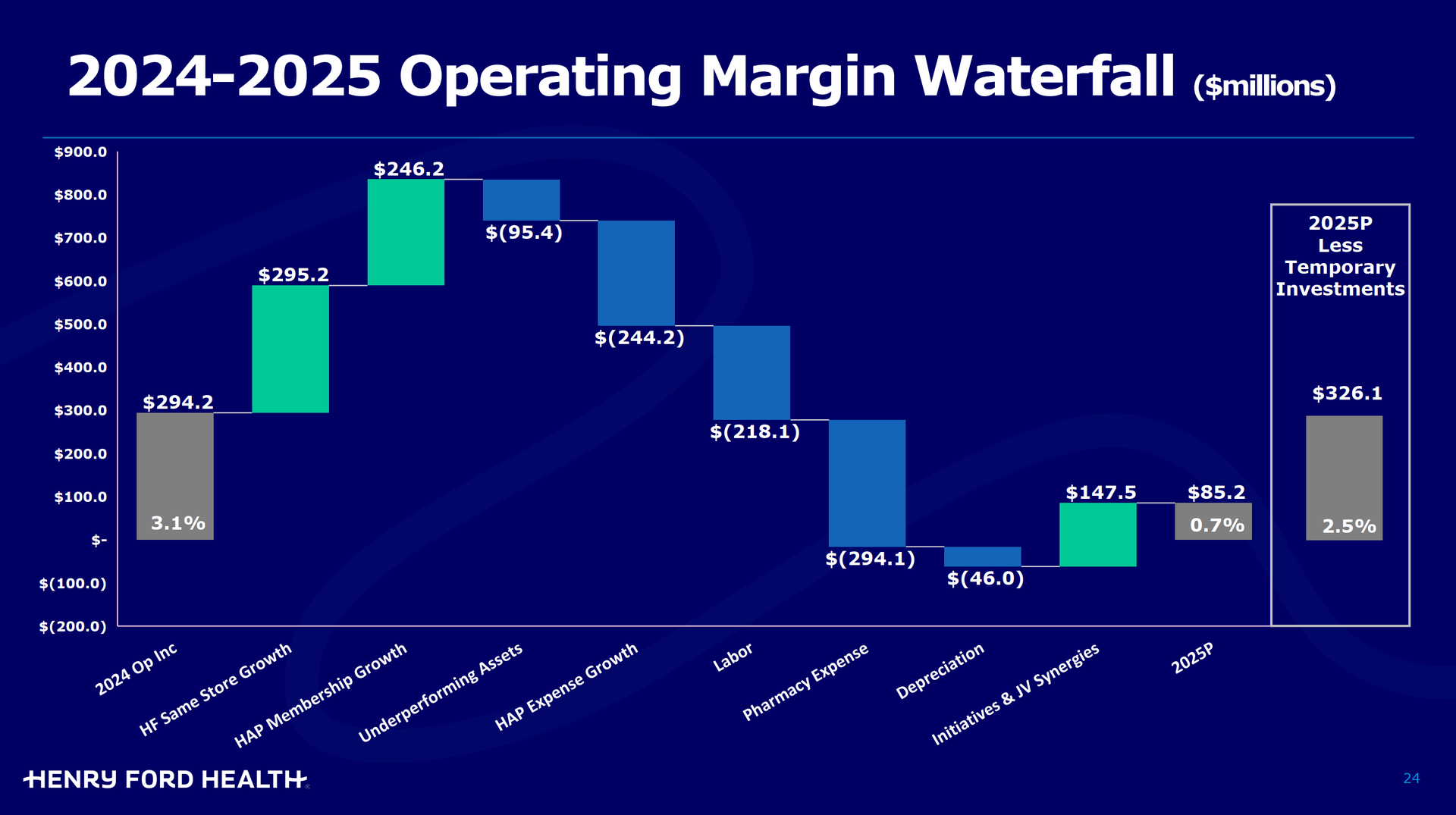

Henry Ford Health: HFH’s presentation is titled ‘The New Era at Henry Ford Health’ and rightfully so given the level of acquisition and portfolio transformation the health system has undergone these past couple of years. HFH has been doing some interesting things including a direct contracting partnership, M&A spree, and setting up certain population health initiatives like Mosaic (not, not the Elevance Mosaic) and Populance.

Plus a Jahmyr Gibbs cameo!! |

2 other slides to call out include Henry Ford’s operating margin waterfall from 2024 to 2025 along with its expected synergies via partnerships and joint ventures: |

Sentara: You’ll be hearing quite a bit about health system consumerism efforts in 2026 and Sentara looks to be headed down that path. Health system 2.0 is here, and KPIs will be focused on how to increase customer LTV:CAC with metrics like loyalty and retention taking center stage. |

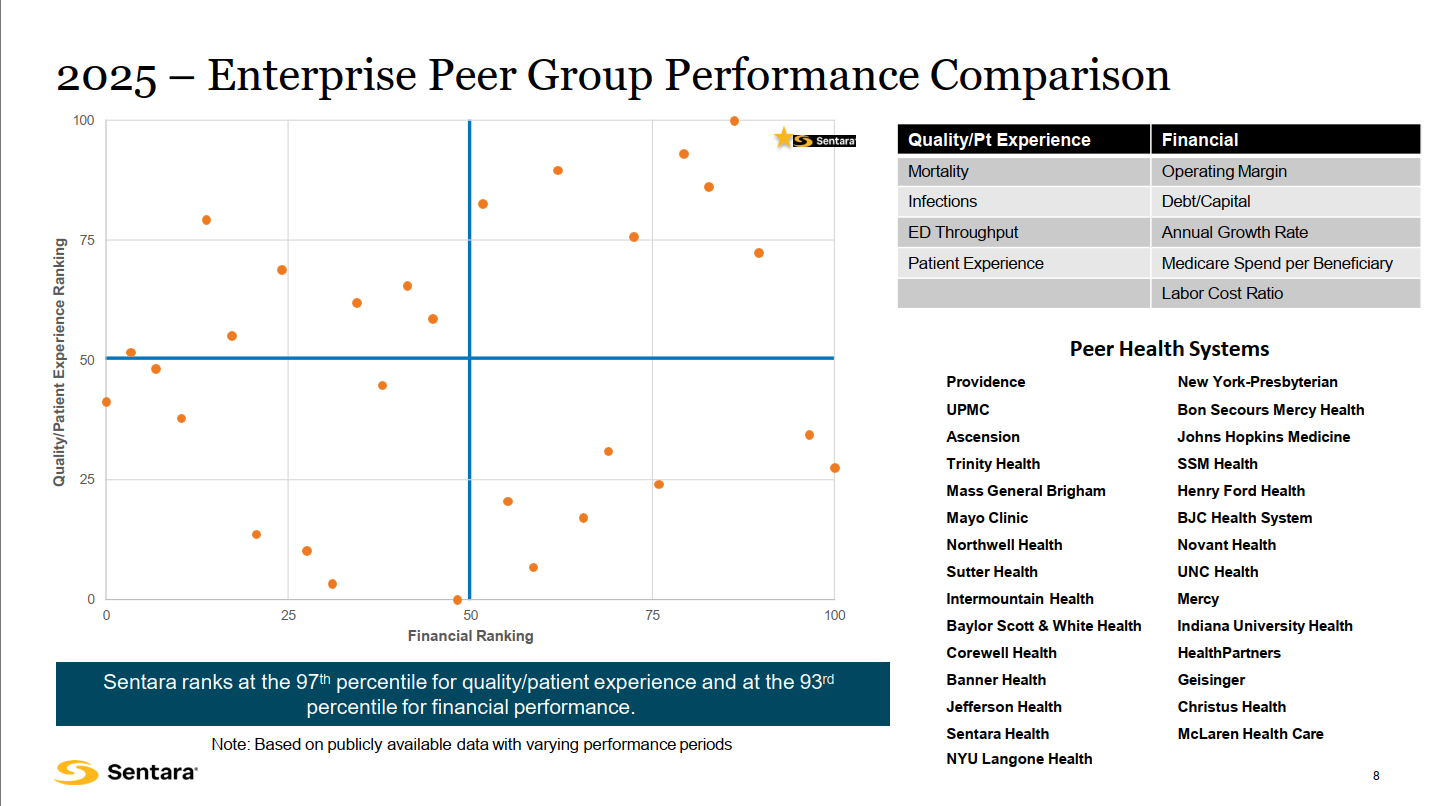

Bonus slide - Sentara must read Hospitalogy because I love this peer to peer performance graphic they put together as a scatterplot (very similar to my financial-only one). I have been looking for a way to combine metrics like this and I love this visualization, so if you know anyone at Sentara or if you’re reading this and you created this graphic, I would love to get in touch! |

More to come next week - stay tuned! All accessible JPM presentations will be uploaded to the community HUB for Hospitalogy plus members. |

|

|

In one (1) week our toddler managed to get sick and learn how to climb out of bed!! So it has been some sleepless nights in the Madden household. Nevertheless it’s a great start to the year and I’m getting my feet under me slowly after the blitz to the end of the year that was 2025. If you haven’t already, please download my new Hospitalogy state of Hospitals & Health Systems 2026 Report - it is chock full of information and my first go at an annual level report! I appreciate your support!!

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Blake |

| |

{if profile.vars.board_room_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Hospitalogy Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}{if !profile.vars.board_room_user_fitness && profile.vars.board_room_user_fitness != false}I'm building a community of leaders in strategy, finance, and ops

at hospitals and health systems to help us connect, learn, and grow together. |

|

|

{/if}

Get your brand in front of 51,000+ executives and healthcare decision-makers. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|