{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Monday, Fintech Takers!

And happy 2026! A lot has happened already, which feels appropriate given the pace at which news moves these days.

Access to information is no longer a problem. The challenge is slowing down and trying to filter the signal from the noise.

Twitter is a terrible place for that (my feed this weekend was full of absolutely useless pontificating on Venezuela), but honestly? A lot of traditional news publications have become pretty bad at it as well.

These days, the news business feels like a competition in which all the players are trying to simultaneously be the first to have a take on the story of the hour (🚨Breaking News!🚨) and to ensure that their takes age as uncontroversially as possible. It’s a bizarre combination of carelessness and cowardice, which, I find, does not suit me.

And, if you’re reading this, I’m guessing it doesn’t suit you either. Here at Fintech Takes, we try to do it differently.

We don’t break a lot of news, and we don’t rush to Twitter whenever anything happens to be the first to post a “here’s what you need to know about X” thread.

We cover the stories that we think are important, and, generally speaking, our judgment on what’s important ages very well (if you want to understand the most important things that will be happening in banking 9 months from now, read Kiah Haslett right now.) Our takes aren’t always popular or even consistent (changing your mind is a virtue!), but they are honest and grounded in a sincere belief that financial products, when they work well, can make people’s lives better. Our hope is that by covering banking and fintech on these terms, we can earn your trust and, together, we can nudge our industry in a better direction. - Alex |

Was this email forwarded to you? |

|

|

Rendering of the Grand Gallery of Honor, Palazzo Paz, Buenos Aires, Argentina. |

|

|

#1: Credit Cards Have Become a Luxury Good |

The latest version of one of my favorite research reports was released:

This report represents the Consumer Financial Protection Bureau’s (CFPB’s or Bureau’s) seventh biennial review of the consumer credit card market as directed by the Credit Card Accountability Responsibility and Disclosure Act (CARD Act) of 2009.

In this report, we review how consumers use credit cards, practices of credit card issuers, and how the credit card market is changing. We revisit topics covered in earlier reports, such as deferred interest and innovations in the marketplace, while introducing new areas of focus this year. We analyze how cardholders spend by merchant category, review promotional interest rates, and take a deeper look into card transaction disputes. Consistent with the report’s mandate, we consider consumers with below-prime credit scores and cover topics related to the cost and availability of credit.

|

Heck yes. I’m so excited. 190+ pages of nerdy, data-driven goodness about the state of the U.S. credit card market.

I haven’t had a chance to read the whole thing in depth yet (I tried very hard to take an actual vacation over the last two weeks), but in my initial perusal, I noticed an interesting trend: credit cards have become a luxury good.

Consider these facts: -

Annual growth in credit card spending was around 5% in 2024; virtually all that growth is attributable to cardholders with prime and superprime credit scores. Growth in credit card spending among cardholders with near-prime and subprime credit scores has been flat since 2023 (despite an increase in the number of those cardholders).

-

Growth in credit card balances is similarly concentrated among cardholders with higher credit scores. The average credit card balance for prime cardholders increased in 2024 to about $8,700.

-

The share of cardholders making only the minimum payment in 2024 was at its highest since at least 2015. About 15% of general-purpose cardholders made only the minimum payment, up from 13% in 2022. The increase was largest for cardholders with subprime, near-prime, and prime credit scores.

-

Credit card delinquencies and charge-offs reached historically high levels in early 2024 but have since fallen to pre-pandemic levels. Prior CFPB research attributes some of the rise in delinquencies to a period of less restrictive underwriting. By year-end 2024, the delinquency rate for general-purpose cards was about 3%.

-

About 56% of below-prime balances are held by issuers with less than $100 billion in assets, while larger issuers hold 95% of superprime balances.

-

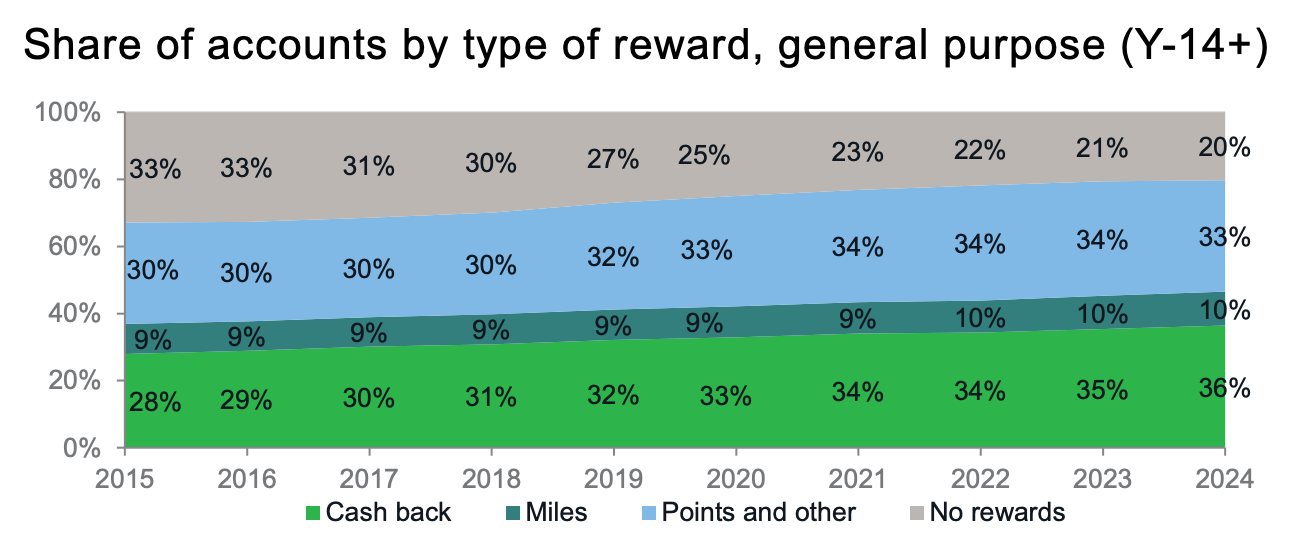

And finally, the share of no-reward credit cards (which are most common for subprime and near-prime segments) has plummeted, as reward credit cards (particularly cash back cards) have surged in popularity.

|

A story you could tell about the U.S. credit card market is that after the big credit card issuers helped consumers burn through their pandemic-era savings and get their spending levels back to usual, those issuers made a conscious choice to tighten their underwriting (and reduce their outstanding exposure) and focus all of their resources on growing spend and borrowing within the coveted superprime customer segment, while leaving many prime consumers and most near-prime and subprime consumers to be served by smaller, more risk-tolerant credit card issuers and fintech lenders (BNPL, EWA, etc.)

Obviously, trends like this are cyclical, and the big issuers’ current focus on superprime consumers is likely due to their caution about taking on too much risk at a time of significant economic uncertainty. However, it will be interesting to see if there are any long-term consequences from the choice that the big issuers have been making to abandon the majority of the market (and the opportunity that has afforded their fintech and small bank competitors). |

#2: The Everything Exchange |

Coinbase announced a bunch of stuff:

U.S.-listed cryptocurrency exchange Coinbase (COIN) is introducing stock trading and incorporating prediction markets, along with a slew of other new products and assets that aims to cement the platform’s position as the “Everything Exchange,” the company announced during its System Update stream on Wednesday. Coinbase said it is dramatically expanding the assets available to trade on its platform, including novel cryptocurrencies, perpetual futures, stocks and prediction markets, starting with Kalshi with more integrations to come later. |

When analyzing a company, I try very hard not to let my intuition run too far ahead of the facts.

In the case of Coinbase, my intuition has, for years, screamed at me that this is a company that wants to be in the gambling business, and that all its talk about greater economic freedom through crypto was just that … talk.

However, in my more optimistic moments, I’ve considered the possibility that my intuition is wrong. That Coinbase really is sincere in its stated desire to help advance the cause of human progress. That, despite its horrifically depressing and cynical commercials, the company genuinely cares about the long-term financial health of its customers and believes that the best way to help them succeed is by building the cryptoeconomy.

This latest set of product announcements has extinguished my last remaining spark of optimism.

This “Everything Exchange” strategy has nothing to do with advancing human progress, guaranteeing economic freedom, or even building out the cryptoeconomy. It’s simply an admission that Robinhood has been beating Coinbase in the race to own the financial nihilism market, and Coinbase is willing to do whatever it takes to catch up.

I mean, stock investing? Not, like, tokenized stock investing (which Coinbase says is coming in the future). Just the regular old buying and selling of individual public company stocks and ETFs. That is jarringly off-brand for them. Did anyone think Coinbase was going to launch that in 2025? Prediction markets were probably an easier guess, given their explosive growth last year. But still, what do those markets have to do with building out the cryptoeconomy? And if you think prediction markets and crypto do fit together, why didn’t Coinbase partner with Polymarket, the crypto-native prediction market, rather than Kalshi?

Even Base, the company’s DeFi wallet app, has been redesigned, much to the frustration of crypto folks who liked the product’s former focus on developers and real utility, and bemoan its attempt to become a “decentralized casino for memecoins, low-quality launches, and vaporware.”

Feel free to continue straining your own credulity, giving Coinbase the benefit of the doubt, and trying to square these moves with the mission that Brian Armstrong outlined in the company’s S-1. I’m done. |

#3: Payments innovation may not be the Federal Reserve’s problem to solve. |

The Federal Reserve is asking for feedback on the idea of a “skinny” Fed master account:

The Board of Governors of the Federal Reserve System seeks public input on a special purpose Reserve Bank account prototype (a Payment Account) tailored to the risks and needs of institutions focused on payments innovation. A Payment Account holder would be expected to use its account for the express purpose of clearing and settling the institution's payment activity. Payment Accounts would be designed to pose limited risk to the Federal Reserve Banks (Reserve Banks) and the overall payment system, and Reserve Banks would generally conduct a streamlined review of requests for these accounts. Any institution that is legally eligible for Federal Reserve accounts or services (accounts and services) under the Federal Reserve Act would be eligible to request a Payment Account from a Reserve Bank. The Payment Account prototype does not seek to expand or otherwise change legal eligibility for access to accounts and services.

|

Kiah and I covered the idea of skinny master accounts on Bank Nerd Corner back when Fed Governor Waller first floated the idea.

It appears to be more than just a passing fancy for Governor Waller. The Fed has published an RFI outlining the proposal and soliciting feedback from the industry, which means that it is seriously considering creating a new type of reserve bank payment account.

I admire the ambition, but I think it’s a bad idea.

In case you don’t know, a Fed master account is an account held at a Federal Reserve Bank that lets an eligible financial institution hold money directly at the Fed and send and receive payments over the Federal Reserve’s payment systems. Having a master account is beneficial because it reduces counterparty and settlement risk and eliminates reliance on correspondent banks to clear and settle payments (which also reduces costs).

Put simply, it’s critical infrastructure for any company whose business depends heavily on payments. And the current leadership at the Federal Reserve really wants to spur payments innovation. As Governor Waller said when he first floated the idea of skinny master accounts, “payments innovation moves fast, and the Federal Reserve needs to keep up.”

Indeed, but the challenge for the Federal Reserve is that it doesn’t have much wiggle room when it comes to solving this problem.

First, as a matter of law, the Fed can only grant master accounts to national banks, state banks that are members of the Federal Reserve system, other “depository institutions” (which include state-chartered non-member banks and credit unions), and a few other niche legal categories. They cannot grant them to fintech companies or large retailers like Walmart, as Governor Waller later clarified:

There's a misunderstanding out there that somehow just a fintech can show up and say, 'Hey, I'd like a skinny master account … You have to have a bank charter to do this, so if you're not a bank and you don't have a bank charter, you don't have the right to ask for one at all. Second, even for institutions that are legally eligible to apply for master accounts, the Fed retains broad discretion over whether to grant them. This discretion allows the Fed to protect financial stability, safeguard the resiliency of the payments system, and mitigate money laundering and other illicit-finance risks.

Historically, this review process has been opaque. More recently — after significant criticism — the Fed disclosed additional details, including a three-tiered review framework. Tier 1 (federally insured and regulated institutions) receives the least scrutiny; Tier 2 (institutions with federal supervision but no deposit insurance) receives moderate scrutiny; and Tier 3 (eligible institutions without federal prudential supervision or deposit insurance) receives the most scrutiny.

The core idea behind a skinny master account is to descope many of the ancillary benefits that come with a full master account — interest on reserve balances, intraday credit, and uncapped balances — in order to make access for riskier eligible institutions (primarily Tier 2 and Tier 3) more palatable. However, as Jonah Crane at Stripe points out, the descoping of those ancillary benefits kinda ruins the appeal of a master account: The proposed prototype is beyond skinny--it is too frail to support any meaningful payments activity.

The limited account features of the prototype make it unattractive as a settlement account, and would likely increase operational risk in the payments system. Payments accounts would be subject to balance caps (the lesser of $500 million or 10% of the account holder’s assets), would not pay interest, and would not be able to access intraday overdraft services or the discount window. In addition, the account would offer access to Fedwire and Fednow but not FedACH–one of the primary rails used to process billpay, payroll, and other bank transfers.

While payments companies could do without discount window access, the combination of balance limits and lack of intraday credit would materially increase the risk of failed payments. The lack of interest on account balances would make holding large balances unattractive even in the absence of limits (nonbanks like Stripe can receive interest from their correspondent banks).

That’s exactly the problem. If you have the scale and sophistication to benefit from a master account, you want most of the bells and whistles. And if you can’t get them directly from the Fed, you’ll simply use your scale and sophistication to negotiate highly favorable arrangements with correspondent banks that already have full access. With this new payment account, the Fed is trying to find the perfect balance between skinny (low risk) and fat (feature-rich), and I’m just not sure it’s possible.

Fortunately, a much simpler path to payments innovation exists: make it easier for fintechs and other payments-focused firms to obtain federal bank charters, thereby qualifying for Tier 1 or Tier 2 treatment.

The Federal Reserve lacks chartering authority, so it can’t expand the universe of institutions eligible for master accounts. The OCC can — and increasingly is. The surge of interest in national trust bank charters, including from Stripe (via its subsidiary Bridge), reflects their potential to unlock more straightforward access to master accounts.

Perhaps payments innovation is ultimately the OCC’s problem to solve. |

|

|

As we head into the NFL playoffs, here's a stat that should give you pause: The most financially vulnerable consumers spend nearly twice as much on gambling.

Welcome to the 1st edition of MX’s monthly Data Takes. Every month this year, I'll share an interesting data point from MX to help you better understand and support consumers.

I've said it more than once and I'll say it again: gambling is THE #1 threat to consumers' financial health. New data from MX shows the real scale of the fallout—and how fast it’s accelerating. |

|

|

2 READING RECOMMENDATIONS |

If you’re not reading all of Marc’s stuff, you should be. |

Apparently, this is a recurring thing? He didn’t do it last year, which is possibly why I didn’t know about these letters. Dan just popped up on my radar this year, thanks to his book Breakneck, which I can’t recommend enough.

Dan’s 2025 letter is also really good. Long, and a bit meandering (look who’s talking!), but very good.

|

There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network. [Warning … this question has a lot of set-up … please bear with me.]

We do not allow children in public elementary schools to use calculators to complete their math assignments because we want them to learn how to do arithmetic. There's not really a concrete reason for this (most adults don't do much long division in their jobs or personal lives). We just want, as a society, to produce adults whose brains are capable of arithmetic.

AI chatbots (powered by LLMs) are kinda like general-purpose calculators for teenagers and adults. They are a powerful tool for doing basic tasks and entry-level work across a lot of different domains (ironically, one of the few areas they're not very good in, as probability machines, is arithmetic). So, here's my question: Is there a case to be made that we should be restricting access to AI chatbots for people who are still mastering basic tasks and entry-level work in order to ensure that we are producing middle-aged adults who are capable of them?

And if the answer is yes (and I think it might be), how in the world would you implement a restriction like that?

Should we restrict access to LLMs to anyone under 18? What about college students? What about entry-level workers with less than 10 years of experience in their field?

At what point does using LLMs change from "shortcuts that prevent students from learning" to "tools that help busy professionals be more productive"?

If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email. — Alex |

|

|

{if !profile.vars.fintech_takes_user_fitness && profile.vars.fintech_takes_user_fitness != false}Join 2,444 other finance and fintech leaders in the Fintech Takes Network |

|

|

{/if}{if profile.vars.fintech_takes_user_fitness == true}The conversation doesn't have to stop here

Keep learning and connecting in the Fintech Takes Network

EVENTS | FEED | LIBRARY | DIRECTORY

|

|

|

{/if}Get your brand in front of 56,200+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|