Hello! Kiah here. Welcome to Fintech Takes Banking, my weekly newsletter where I highlight things I think are interesting or important for bankers and the surrounding environs.

Hopefully, you’ve had a great holiday week and are as excited about 2026 as you are nervous, if at all. Below are my summaries and analysis of the biggest stories and developments in the quarter that I think we’ll see continue developing in the first quarter. | Was this email forwarded to you? |

|

|

Putting a Bow on it: A TL;DR of 4Q’25 |

We did it. We made it to the end of the year.

I know it was tough going for a bit (you can pick which bit you thought was the toughest), but the year is finally ending, as it promised it would. The winter solstice has passed, the presents are open, the gift wrap is discarded. You don’t have to buy anyone a gift for about six weeks, and you can keep your decorations up until at least Jan. 20. Ahead of the year-end, let’s take about 15 minutes to reflect on the fourth quarter, as well as how the trends of the third quarter continued developing and what that might mean for 2026.

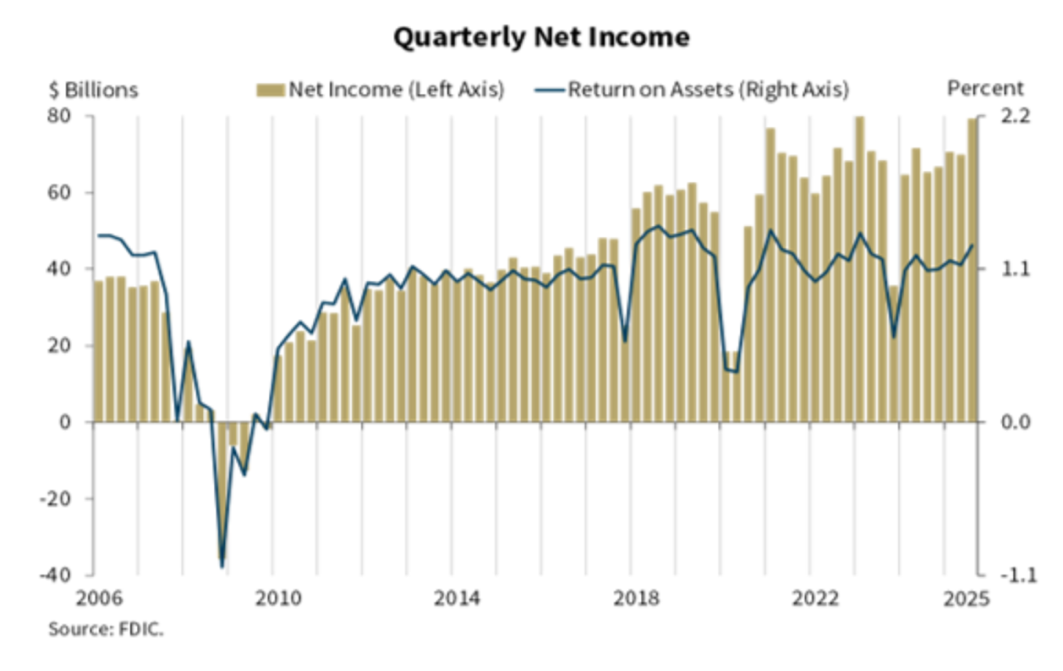

The third quarter wound up being another good quarter for the banking industry, according to the Federal Deposit Insurance Corp. Net income for the quarter was up 13.5% from the second quarter, to $79.3 billion, driven by net interest income growth and declining provision expense tied to the Discover Financial Services acquisition by Capital One Financial Corp.

The return on assets hit 1.27%, up 13 basis points from the quarter prior and 18 basis points from a year ago, while the sector’s net interest margin grew nine basis points to hit 3.34% in the third quarter. Higher net interest and noninterest income at community banks boosted third-quarter net income by 9.9% from the second quarter, to $8.4 billion. NIM hit 3.73%. |

Source: FDIC Quarterly Banking Profile |

Other macro trends within the bank space included merger and acquisition announcements and concerns about credit quality. It was both surprising and deeply unsurprising to see superregional banks position themselves as buyers during the quarter, some banks hit the “buy” button more than once and for deals to close so much faster than we had seen a year prior. While I think the pace of M&A will continue in 2026, the buyers may shuffle as those who announced acquisitions this year take some time to integrate the deals. I also wonder what the pace of acquisition activity will do to pricing and (to hint at a newsletter) whether all these deals will be good long-term purchases that build shareholder value. Please email me your thoughts on the latter. 😏

Broadly and thankfully, credit quality during the quarter seemed fine, and losses are manageable. But there were some eyebrow-raising frauds announced tied to bankruptcy filings, which were embarrassing to the players involved and led to everyone, including me, asking what the hell is going on. Similar announcements in fourth-quarter earnings will not help quell these perceptions, but it is reassuring to see banks that have recorded fraud conduct more thorough reviews of similar loans and assert they’ve found nothing else amiss.

One interesting variable that emerged in the latter half of 2025 and gained steam during the fourth quarter was shareholder activism from HoldCo Asset Management. The investment advisory firm has targeted several midsized and regional banks for various strains of underperformance through a somewhat quaint and low-tech campaign of press releases and presentations with odd capitalization styles. But the presentations themselves are long, sarcastic, thorough and savage. There are now at least four presentations directed at Dallas-based Comerica for peer underperformance and its hasty deal announcement to Cincinnati-based Fifth Third Bancorp. Not to be left out, it has issued presentations about Cleveland-based KeyCorp; Billings, Montana-based First Interstate BankSystem; Tacoma, Washington-based Columbia Banking System; and Boston-based Eastern Bankshares. I’m sure little will change in this arena in 2026.

Charter application momentum stayed high during the fourth quarter, something I chatted with Dan McGonegle, a senior manager at Crowe, in an episode of Bank Nerd Corner aptly titled “Why Everyone Wants a Bank Charter.” Brazilian neobank Nubank kicked off the quarter by announcing it applied for a national bank charter; the U.S. institution will have Brian Brooks, former acting comptroller of the currency, on the board. Nubank had 122.7 million customers in its Brazilian, Columbian and Mexican markets as of June, according to Banking Dive. To close the quarter, payments company PayPal Holdings announced it applied for an industrial loan charter from the Utah Department of Financial Institutions and business banking fintech Mercury announced it applied for a national bank charter and deposit insurance.

In October, Erebor Bank N.A. received preliminary conditional approval for its full banking charter from the Office of the Comptroller of the Currency and deposit insurance from the FDIC. Also in October, the OCC gave conditional approval to give digital asset firms that had applied for national trust bank charters or to convert their state charters to national ones.

|

The Economy: The prolonged government shutdown impacted the release of economic data during the quarter. Employers added 64,000 jobs in November and the unemployment rate rose to 4.6% during the month, up from 4.4% in September, the last month of complete collection before the shutdown. Inflation rose 2.7% in November, relative to the same time a year ago, below economists’ expectations of 3.1%. The cancellation of October’s release and the subsequent need by the Bureau of Labor Statistics to make “certain methodological assumptions” about October’s inflation that “were not clear to economists and not fully explained in the release,” according to CNBC. The U.S. economy grew 4.3% in the third quarter, according to the initial estimate released by the U.S. Bureau of Economic Analysis on Dec. 23. That is up from 3.8% in the second quarter.

Visa, Mastercard settlement: In November, the two major card networks announced they were nearing a settlement in a 2005 case that would lower the interchange fees merchants pay. It would also change the standing rule that if merchants accept one card on the network, they must accept all of them, potentially allowing them to reject certain credit cards altogether or add surcharges. The Wall Street Journal reported in November that under the settlement talks, credit card acceptance could be divided into several categories, such as rewards credit cards, credit cards with no rewards programs and commercial cards.

U.S Court of Appeals for the Tenth Circuit in National Association of Industrial Bankers v. Weiser: In November, the U.S. Tenth Circuit upheld Colorado’s 2023 decision to impose interest rate ceilings on loans made by out-of-state banks with a state charter to Colorado borrowers. The decision brings uncertainty to the settled provisions within the Depository Institutions Deregulation and Monetary Control Act of 1980 statute for state-chartered banks, especially for institutions that are active in the banking as a service space. Andrew Grant, a regulatory attorney at Runway Group, joined me on Bank Nerd Corner to discuss the 1978 case that led to DIDMCA and the potential implications of the Tenth Circuit ruling; the episode is called “The Old and New Legal Challenges to Exporting Interest Rates.”

“This decision risks undermining state banks’ ability to effectively administer multi-state lending programs and, perhaps more importantly, disadvantages state banks that wish to lend in Colorado compared to national banks and Federal savings associations. Such an outcome is fundamentally inconsistent with Congress’s efforts to create competitive equality between state and federally chartered banks. Courts or, if necessary, Congress should remedy this outcome,” said Comptroller Gould in a statement released a month later. The OCC later filed an amicus brief supporting the petitioner’s appeal for an en banc circuit rehearing.

|

The Federal Reserve Board was a locus of activity in the fourth quarter. The rate-setting arm, the Federal Open Market Committee, lowered interest rates in both meetings this quarter. The target federal funds rate is now 3.5% to 3.75%. Dissent within the FOMC about the pace and magnitude of rate changes increased during the quarter. In December, FOMC members voted 9-3 on whether or not to cut rates — the first time in six years that three officials cast dissenting votes.

In October, the FOMC announced it would end quantitative tightening in December and would stop pulling liquidity from markets. Quantitative tightening is the process that it used to reduce its balance sheet by not reinvesting the proceeds from maturing US Treasuries and mortgage-backed securities. The end of QT was seen as an economic positive that could have a potentially stimulating effect, according to an article from S&P Global Market Intelligence. I discussed the potential implications of this announcement with Invictus Analytics CEO Adam Mustafa in an episode of Bank Nerd Corner titled “What Banks Need to Know About the End of Quantitative Tightening.”

At the start of October, the U.S. Supreme Court issued a short, unsigned order that allowed Gov. Lisa Cook to remain on the board until the full case could be argued in January 2026.

Gov. Christopher Waller caused some excitement, and then confusion, around a proposal he offered for a “skinny master account.” His iteration included an account that would have access to the Fed’s payment rails, but no daylight overdrafts, discount window access or ability to receive interest, and the Fed could impose balance caps. These comments set off industry speculation as to which companies might be interested in them at events like the 2025 Money 20/20 conference, until Waller clarified that potential eligible applicants would still need to have a bank charter. In late December, the Fed issued a request for comment on payment accounts “which eligible financial institutions could use for the limited purpose of clearing and settling their payments.”

|

Rulemaking around the Genius Act has begun at the federal banking agencies. The FDIC announced proposed rulemaking for supervised institutions that seek the agency’s approval to issue payment stablecoins through a subsidiary.

No matter what happens with Gov. Cook, there will be a 2026 transition at the Fed. Jerome Powell’s term as Fed chair expires in May 2026. As of late December, President Donald Trump has indicated there are four potential nominees.

|

|

|

Quantifying some of the best parts of my year. |

📋 This year in resolutions: I did not finish a single pen, but I did finish two notebooks, including a reading journal. In an attempt to use up pens, I started writing greeting cards to friends during my travels, a practice I recommend and plan to continue. I handwashed all my chef’s knives and wooden spoons this year. I did not always wait 24 hours before buying something online.

📖 This year in books: I read 65 books this year (my most ever!); 45 came from the library, saving me roughly $675 if you assume an average of $15 a book. Some great picks I read included Murderland by Caroline Fraser, An Immense World by Ed Yong, James by Percival Everett and Our Hideous Progeny by C.E. McGill.

💳 This year in credit card redemptions: I broke my New Year’s resolution for 2025 of no new credit cards by adding the Bilt card and the IHG Premier (neither are affiliate links). I paid about $1,800 in annual fees this year and recieved $7,800 in net value: five round-trip flights (including 2 international trips), 21 free hotel nights and about $1,100 in ancillary travel benefits. I keep track of all my redemptions in a tracking spreadsheet that dates to 2019. Eagerly awaiting the Bilt card update coming later in January!

|

Thanks for reading! And happy New Year, hope you have a great start to 2026 and wish you all the luck in keeping your resolutions, if you’re in that camp.

– Kiah |

|

|

Get your brand in front of 55,000+ financial services execs. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|