Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Hospitalogy.

{/if}

How about them Longhorns?! I decided to buy some tickets to the game last minute and man, what a game. Did you know OU has yet to score a touchdown on Texas since starting SEC play? Crazy stat.

Alright, I’m done now. On to this week’s Hospitalogy news roundup. But first - I do have one favor to ask you guys. Starting this week (AKA right now) you’ll have the chance to submit anonymous questions to Hospitalogy for me to ask my community / network and feature their responses in the newsletter around tactical challenges, trends, or anything in your role you want to learn more about.

Ask a question here! This ‘Ask Hospitalogy’ segment will be included in newsletters from here on out.

Which side of the Medicare Advantage see-saw are you on?

The bearish camp would say the current crop of managed care players - both small and large - are structurally unequipped to deal with ‘hard times’ in Medicare Advantage.

The bullish camp would say healthcare - and MA more specifically - sees a reset every so often, and this current challenging environment is a healthy reset. That there are still pockets of growth (like in C-SNP / duals) and that clinically excellent models are still finding growth and success.

Recently I’ve seen a bunch of data and notable commentary emerge on the current state of MA and wanted to aggregate some of those viewpoints and visuals for you guys here.

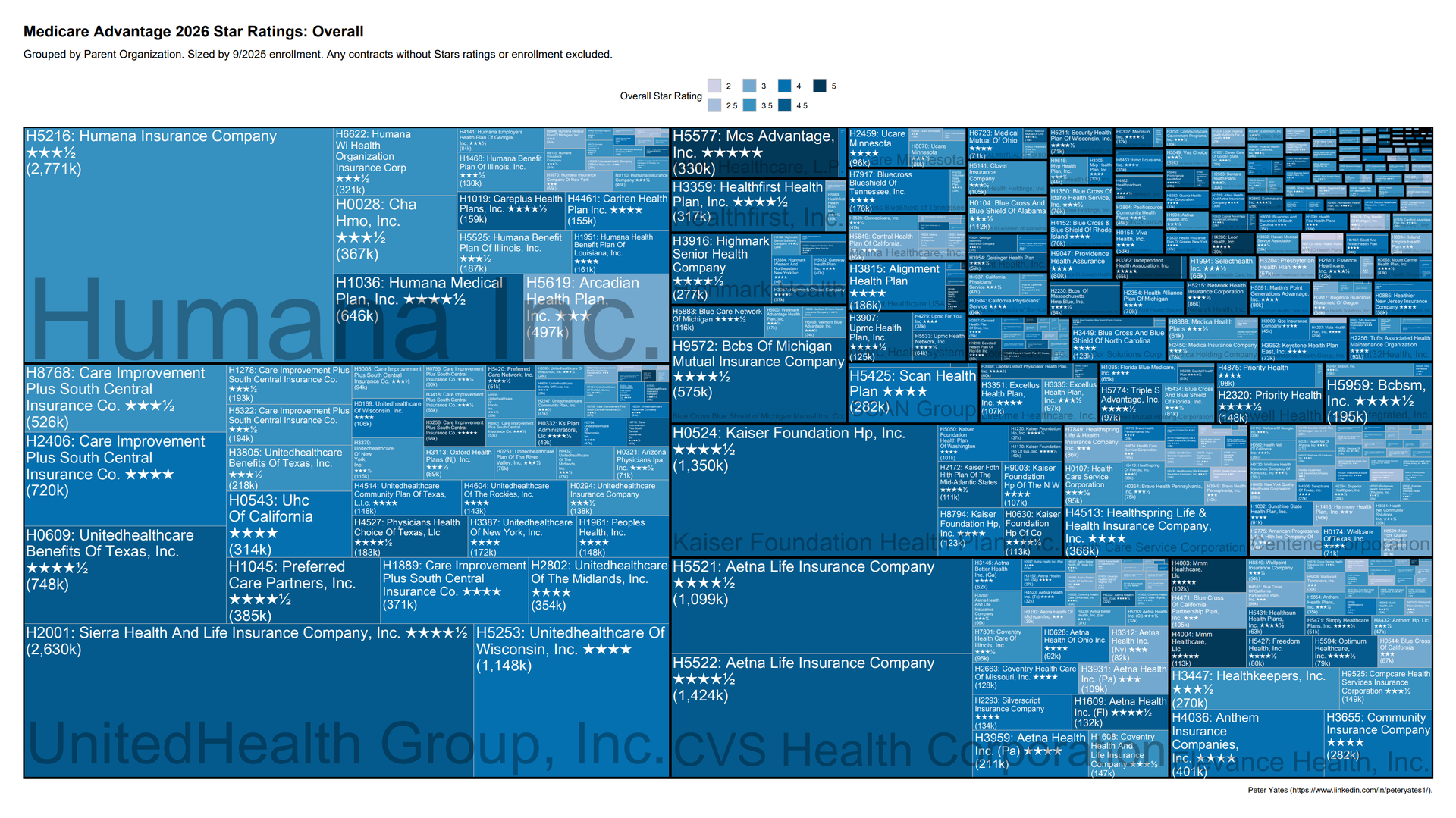

First off, I would highly recommend following Peter Yates for his wonderful visualizations of all things MA star ratings (released last week here) like the tree maps below. Find his posts here. He often highlights the results for each managed care player’s outlook on stars for the upcoming year. Overall, star ratings have declined and since stabilized after CMS tightened up the scoring post-pandemic (leading to certain lawsuits you’re all probably familiar with). Here’s a good overview from Healthcare Dive on winners and losers. Clover continues to complain about having to play the game by the same rules as everyone else instead of coming up with fake metrics like normalized MLR every quarter (though they do have a point about star ratings methodologies).

As a reminder, many MA players shrank their footprints drastically after the 2024 and 2025 utilization/risk disasters. The collective large carrier contraction creates an interesting phenomenon where Medicare Advantage could shrink or stay flat in 2026, while market exits will cause weird member growth dynamics for those who remain in those local markets. Considering some of the projections out there around continued MA penetration folks were throwing around a couple of years ago, the possible contraction is pretty crazy.

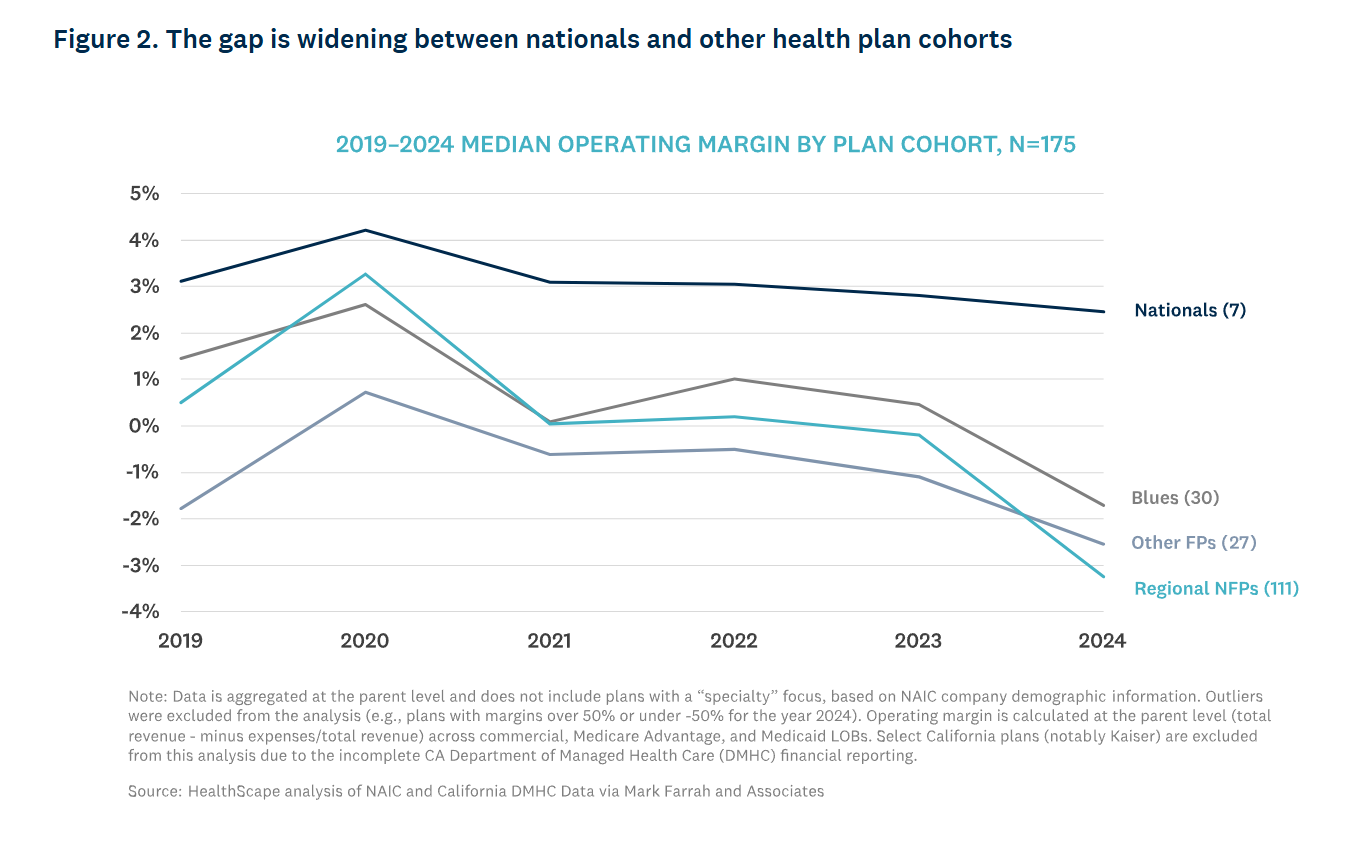

Along with the contraction, HealthScape put out an analysis on the unsustainable trajectory of regional health plans noting that many have less than 2 years of runway, and operating results are worsening given rising administrative and medical costs in their markets. All of that stuff you’ve been hearing hit the national carriers? Yeah, it’s exacerbated at the regional level. An unsustainable dynamic - with the OBBA looming - will only cause consolidation for mere survival purposes. The Blues plans seem to be right there with them too given their federated structure.

Finally, this think-piece by Duncan Reece made its rounds over the past few days and I can always appreciate someone throwing a thesis out there to zig when others zag. Personally I’m with the jive of the article - that there is still plenty of opportunity in MA. This is healthcare. We’re not talking about drastic boom and bust cycles here.

Nonetheless, there’s your aggregation of MA datapoints for collective review. Where does your camp sit with MA?

THE WEEKLY EXECUTIVE SUMMARY

Notable moves, policies, and strategies from around healthcare.

Amazon is doing its best CarePods impression (sorry, couldn’t resist) by setting up self-serve kiosks for One Medical and Pharmacy customers to grab prescriptions for common medications. While specialty drugs and those needing refrigeration will stay behind the counter, Amazon is in talks to roll out the kiosks to health system partners in an attempt to extend pharmacist capacity while cutting down on logistical costs.

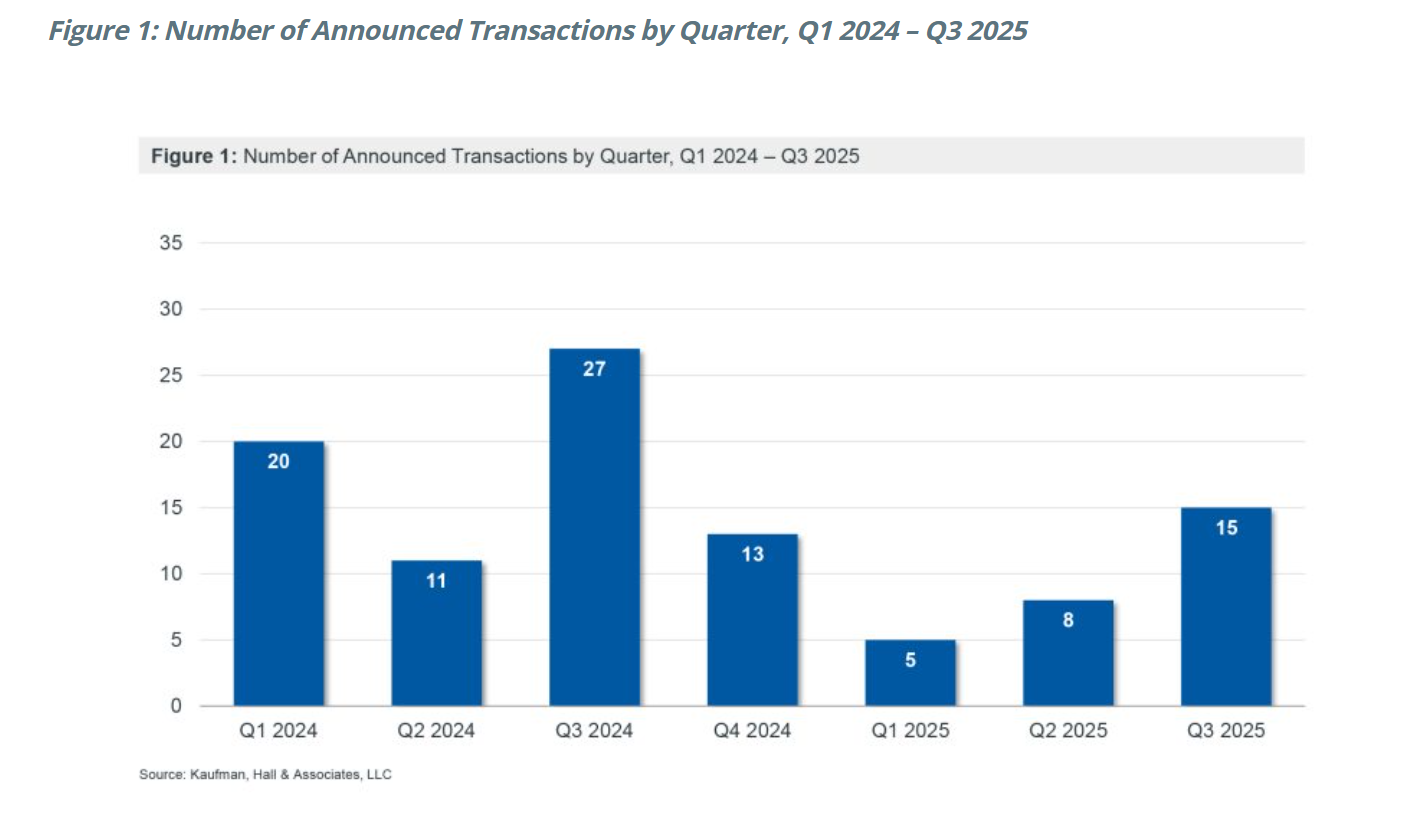

Kaufman Hallreleased its hospital Q3 M&A report, signaling a bounce-back in M&A activity in Q3. In general, anecdotally it seems like Q3 was pretty busy with activity. Notable hospital transactions included joint venture ‘portfolio realignment’ transactions like Baylor and Geode Health. Notably, ALL 15 of the buyers in Q3 were nonprofit health systems.

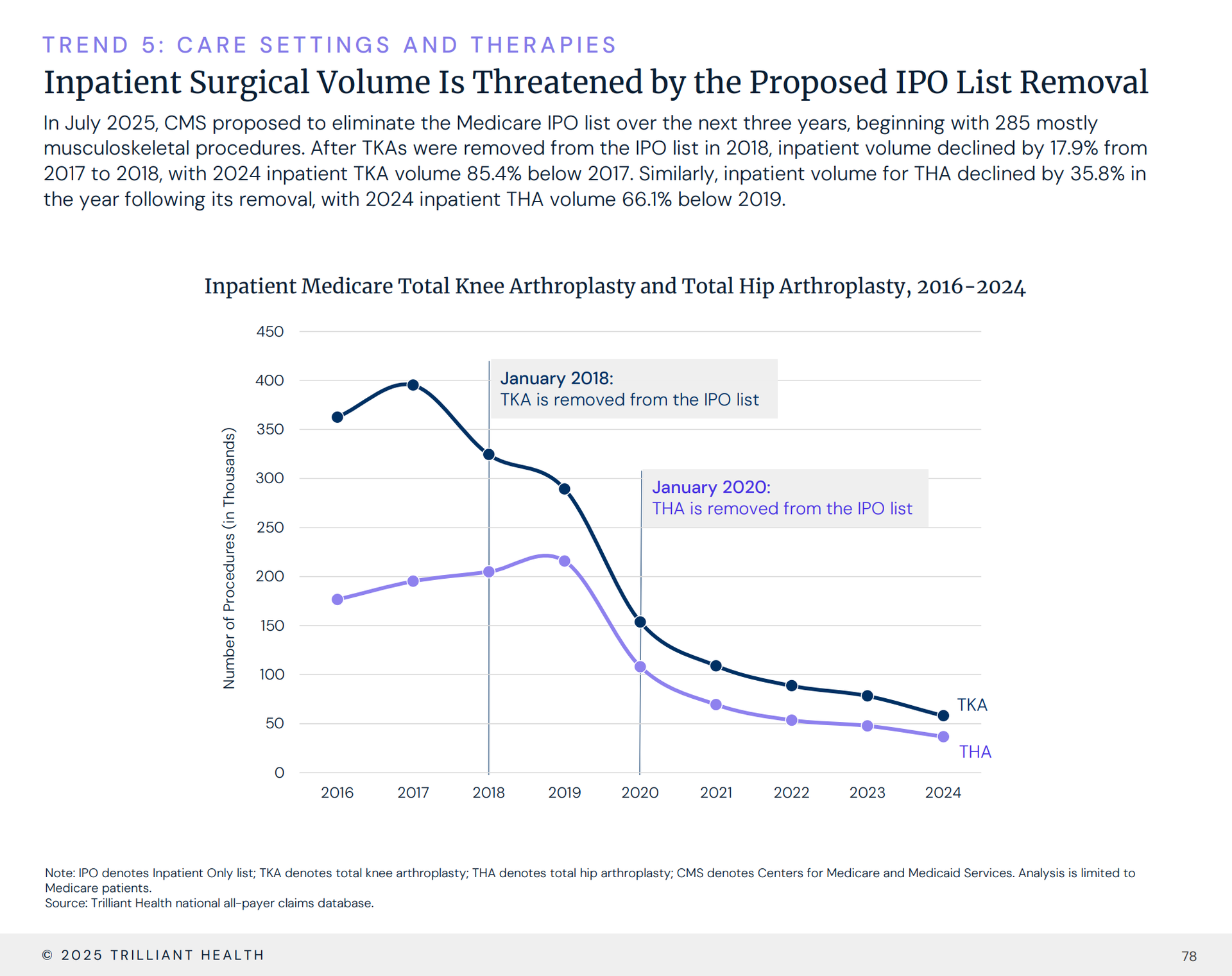

Trilliant’s 2025 Trends Shaping the Economy report is always chock full of great information on the current state of things, with some spin from the firm on what might be coming next highlighting the research and intel platform’s capabilities. Interestingly, ICHRA is one of the first trends mentioned in the report, along with price variation, population health factors, and other interesting utilization information.

Qualtrics is buying Press Ganey for nearly $7B as the mammoths of patient survey data take over the patient survey, feedback, & insights market. I also find it really great and not problematic at all that they are 2 out of the 3 vendors listed in Epic’s Showroom.

OneOncology isacquiring GenesisCare which you’ll hopefully hear more about in Hospitalogy soon! 100 clinics, 104 physicians. GenesisCare will rebrand as SunState Medical Specialists under the OneOncology umbrella.

Talkspaceacquires Wisdo, a peer support platform for loneliness.

NeueHealthgoes private after a beleaguered run on the public markets. Rest easy, child.

California’s Governor Newsom signs a bill clamping down on private equity activity in healthcare, allowing the California AG to intervene when investors ‘interfere’ with the control over healthcare decisions of doctors / healthcare assets in which they invest. The bill, also, VERY notably, gets rid of non-compete clauses.

General Catalystannounced the formation of Percepta, a firm aimed at helping enterprise-level players in all industries (but probably a lot of healthcare) build infrastructure needed for an AI future.

{ad_content_secondary}

TOP READS & RESOURCES

My favorite reads & resources from the week

Thatch’s deep dive by Not Boring, covering ICHRA, benefits, and everything in between for the startup. Given Not Boring Capital is an investor in Thatch, it’s a bull case on the future of ICHRA, and a great overview of the space.

Have health systems, ACOs, FQHCs, and others involved in value-based care finally found a framework that drives real, tangible value? My deep dive shows they have.*

.png)