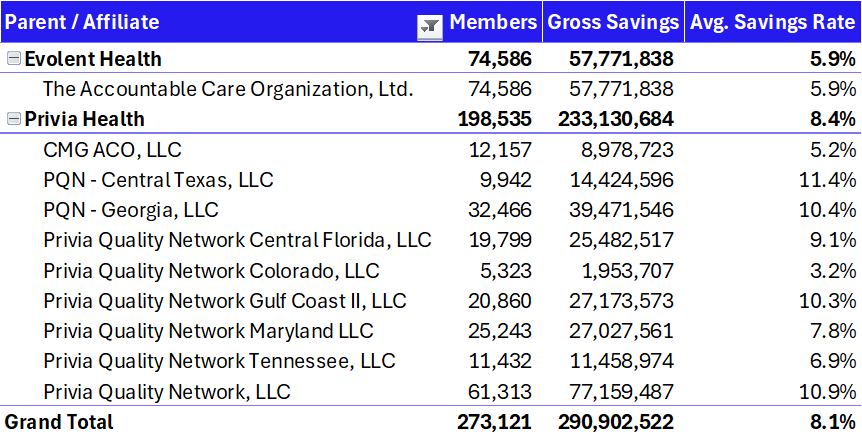

Privia’s purchase of Evolent Care Partners brings 120k+ attributed lives across MSSP and other contracts. Along with the lives and demonstrable savings (as seen in the combined MSSP results table above put together by yours truly), Privia continues to invest in assets that align with its culture and economics: i.e., a physician base oriented around independent practice, and a portfolio that swells its density and ability to enter new markets with associated platform acquisitions. Privia paid $100M in an all-cash deal, with $13M in contingent consideration based on MSSP PY 2025 final results - around a 10x EBITDA multiple.

Stephens broke down the deal in a recent report, stating Privia has a track record with deals similar to Evolent Care Partners:

-

“Following its Feb. 23 purchase of VMG in Connecticut, Privia grew MSSP beneficiaries 20%, increased savings rate by 150bps, and has implemented 100+ new providers in the market. Here, Privia needs to retain ECP providers in multiple markets, but MSSP results speak for themselves”

-

“We estimate >60% of the ECP lives are in the MSSP program…$42M in shared savings would yield ~$17M in care margin.”

Translation being Privia has a defined, calibrated playbook for new acquisitions and as a company, Privia thinks it can build upon Evolent’s success within MSSP and the broader market strategy. But what exactly is that playbook? I had the chance to pick Privia’s Sam Starbuck’s brain for a conversation on how they think about strategic M&A, growth, and current macro landscape.

What stands out most from that conversation is how much Privia cares about fit. From the beginning, Privia’s core mantra as a company aims to secure the future of independent practice. Evolent’s ACO portfolio and partner physicians is tailored to that same belief and culture. There’s a reason why Privia holds a 98% physician retention rate dating back to the company’s origins in the early 2010’s. Adding to the general culture fit, MSSP is Privia’s bread and butter, and within that space, they’re not rebuilding an unprofitable operation. In fact, Evolent Care Partners (ECP) is profitable and large, generating 5-6% in savings. We’re not talking rocket science here. No, the simple thesis is that Privia’s physician-led governance, scale, analytics, and tech flywheel can turn a steady baseline into higher sustained performance over a 2-4 year window - not overnight, but steadily through disciplined compounding and 1% better operations every day.

Density also matters...a lot. From the Stephens analysis, the investment bank sees immediate exposure in California, Florida, Kentucky, North Carolina, and Texas, with large practice clusters in Florida and North Carolina and historical relationships with Blues affiliates in North Carolina and Texas. The potential on ramp extends to Hawaii, Michigan, New York, and Pennsylvania, with possible anchor practices in New York and Pennsylvania. That mix gives Privia near term lanes to standardize contracts and clinical cadence where it already operates while laying groundwork in several attractive new states.

All of that sets up the levers Privia has available to pull on these assets over the coming years. Sam broke down those levers into 3 primary buckets: talent, tools, and technology.

-

On talent, the existing team is joining Privia with deep practice relationships. That relational capital matters in a business where performance gains come from dozens of small workflow choices rather than a single top down directive. Privia plans to plug those leaders into a physician governed operating cadence peer comparisons, accountable committees, and local clinical leadership that make results feel owned, not imposed. It is the same culture management points to when citing a retention rate near the high nineties since the early days of the company.

- On tools and technology, Privia’s emphasis is not on shiny objects. They’re focused on what actually moves the needle for their partner physicians in areas like workflow support for the provider and the care team. The company has spent the better part of twelve years building and partnering around technology with certain core pillar capabilities:

- Can this remove burden from the physician?

- Could it improve productivity of the care team?

-

Can it optimize the workflows of the practice and take work from them?

- Will it improve outcomes of patients?

The rule is pretty simple: no swivel chair and no second screen for the physician (e.g., maximal reduction of clicks and eyes moving to secondary dashboards) - meaning if a feature does not show up inside the actual visit or care team workflow, it’s typically a no-go for Privia. These decisions also presented themselves up in Connecticut where Privia supports a clinically integrated network across mixed records systems and has seen steady incremental improvements from rolling its stack into that EHR agnostic environment. The Evolent portfolio will be a similar challenge given disparate EHRs.

Patient engagement is the other technology theme that came through and seems to be a major sticking point in 2025 among provider organizations, risk or not. There is a surplus of data and outreach in healthcare, especially for the chronically ill. Everyone wants to touch the same high risk patient the hospital, the primary care practice, the plan, the care management vendor. The result is noise that masquerades as help. Privia’s aim is to engage patients in the right place, with the right message, at the right moment, and to do it in ways that reinforce what the practice is trying to accomplish rather than compete with it. That approach depends on better activation of staff and a care team model that delegates work away from the physician while still closing risk and quality gaps. If Privia can tame duplicative outreach while keeping practices at the center, the savings math gets easier across contracts.

There is also a timely operational angle that turns a policy mandate into a service opportunity. And that policy mandate is called electronic clinical quality measures, or eCQM - something I’d been previously unfamiliar with but, simply put, is a new CMS requirement for certain standardized electronic reporting within population health. And on paper, standardization like this should reduce burden. But in practice, especially across a network with many EHRs, it introduces new burdens. Are the systems equipped to produce the right file type? Do practices have to pay for a module to enable it? How will those files be normalized and validated upstream? Privia has already been normalizing data and producing comparable views across disparate systems in Connecticut. Bringing that discipline to the acquired network is an obvious early win that supports both compliance and performance. But this rule is also another example of how and why scale wins in healthcare.

I couldn’t help but ask Sam about his and Privia’s quick macro take given what’s been happening more broadly across the healthcare ecosystem. The macro take from Starbuck was refreshingly plain: healthcare runs in cycles. Right now the plan side is being right sized after several years of rapid growth in the senior product and exuberant assumptions. Organizations that concentrated too much risk in a single segment are feeling exposed. And so that’s why Privia’s model is so brilliantly flexible - Privia’s model is to play in all environments and dial up or down based on market conditions while keeping the shared savings program as the cornerstone. That flexibility has tactical value in a choppy year. It also pays strategic dividends as commercial and senior products align around standardized measures like eCQM. The more the market converges on common rules, the more a consistent, in workflow operating model matters.

And as a quick aside on Evolent, the sale clarifies the company’s story. Shedding primary care risk gives the company a cleaner focus on specialty enablement in oncology and cardiology - two specialties with extremely high spend and with areas of lots of opportunity - and improves cash flow as debt is prepaid. I can appreciate the specialization focus as Privia expands its prowess and density in MSSP and independent providers.

If we’re in inning 2 like was discussed at the Hospitalogy VBC retreat, then we’ll slowly creep into innings 3 and 4 through leverage of technology, continued consolidation of scaling models that are sustainable, and better policy.

.png)