Let’s start with the Consumer Reports Fairness by Design Playbook, as it is product-agnostic and principles-driven (whereas the Financial Health Network’s product standards are more focused and prescriptive).

The Consumer Reports Playbook is focused on moving the market towards greater levels of fairness and trust, which, Consumer Reports (CR) argues, will also result in a more innovative and profitable market for providers:

Every interaction shapes a consumer’s perception, and acquiring new customers has become more expensive than ever before for fintechs due to intense competition, trust barriers, regulatory compliance, and complex onboarding. Designing for fairness at every touchpoint builds lasting relationships, drives higher transaction volumes, and turns consumers into word-of-mouth advocates. Ultimately, that leads to business success in the rapidly growing digital economy. Especially as consumers grow increasingly wary of financial risk, they are demanding safe, user-friendly products that keep them at the center.

CR also argues that designing for fairness and trust will align providers’ products and processes with the expectations and requirements of regulators, which will ultimately reduce compliance costs and minimize regulatory risk. This particular argument strikes me as a bit theoretical at the moment, given the state of the CFPB, but not unreasonably so.

To design for fairness, the CR Playbook encourages focusing on six pillars:

- Safety

-

Privacy

- Transparency

- User-Centricity

-

Support for Financial Well-Being

- Inclusivity

For each pillar, the Playbook makes a set of specific recommendations, along with real, in-market examples for providers to use as inspiration, and some potential metrics that providers can use to assess themselves and their customers.

Let’s briefly walk through each pillar.

Safety

This section includes some fairly obvious data security recommendations (encryption, multi-factor authentication, etc.)

However, it also specifically calls out the importance of communicating to customers how their money is (and isn’t) protected (this seems to be a direct response to the consumer confusion regarding deposit insurance coverage in fintech, as revealed by the Synapse mess) and talks quite a bit about the importance of real-time fraud prevention tools and consumer education (perhaps in response to the growth of authorized payment scams).

JPMorgan Chase, Chime, and BECU are all cited as positive examples in this section.

Privacy

This section feels like it was written by Rohit Chopra, which makes sense given the amount of influence that consumer advocacy groups had in the Chopra-era CFPB.

Many of the recommendations are similar to the principles expressed in the bureau’s Personal Financial Data Rights Rule (minimize data collection to what is essential, make it easy for consumers to see what access they have allowed and revoke that access easily, etc.)

CR cites Plaid as a positive example here (while noting that the granularity of the permissioning could be better), as well as Albert and Klarna.

(Editor’s Note — I did not know that Klarna offers a “sign in with Klarna” service for customers to use with merchants, which apparently includes the ability to share their purchase history data with merchants? Fascinating!)

Transparency

The CR Playbook argues for a level of transparency that is, in my opinion, quite a bit further than where financial service providers are today.

Recommendations include terms and conditions that use plain language (the old neobnak Simple was SO GOOD at this), straighforward and easy-to-understand pricing, explanations of how the product or service that the customer is using work behind the scenes (this would have been illuminating for consumers that were unknowingly using Synapse), and standard, and compliant APR disclosures (many fintech lenders argue, not unreasonably, that APRs aren’t always the most understandable way to disclose pricing to consumers).

Apple, Bank of America, and SoFi are listed as positive examples for transparency.

User Centricity

The recommendations under this pillar seem split between ones aimed at banks (greater use of first-party data, better training for customer service reps, dashboards and user-driven customization) and the ones aimed at fintech companies (robust real-time, multi-channel customer support, focus on customer outcomes in addition to business performance).

Overall, the theme is better, more personalized customer support.

PayPal, Fidelity, and Varo are mentioned as positive examples.

Financial Well-Being

This pillar is a little different.

It contains roughly twice as many recommendations as any of the other pillars, and the recommendations span a wide range.

There are recommendations focused on measurement and metrics (conduct user research, create financial health KPIs, etc.) There are ones focused on customer engagement and habit formation (create financial health metrics/scores/benchmarks for users, promote financial resilience, incorporate nudges into product/UX design, etc.) And, building on a recurring theme, there are ones focused on transparency and fairness (no mandatory arbitration clauses, rely more on ability to pay data, etc.)

CR lists Cash App, Ally, and Brigit as good case studies.

Inclusivity

In the midst of the current political and regulatory backlash against DEI, I suppose you could argue that this pillar is the one that financial services providers will see as the least urgent.

In my opinion, that would be a mistake.

The recommendations in this section of the Playbook aren’t about virtue signalling. They are practical, granular suggestions for making financial products and services work better for all customers.

They include ensuring compliance with web accessibility guidelines, providing multi-lingual customer support (as needed for the customers a provider serves), and incorporating cultural differences into behavioral product and UX design (e.g., peer-to-peer lending and group savings accounts).

Comun, Greenwood, and Chime (second mention!) are all listed as examples for this pillar.

OK, that’s Consumer Reports.

Now let’s get to the Financial Health Network (FHN).

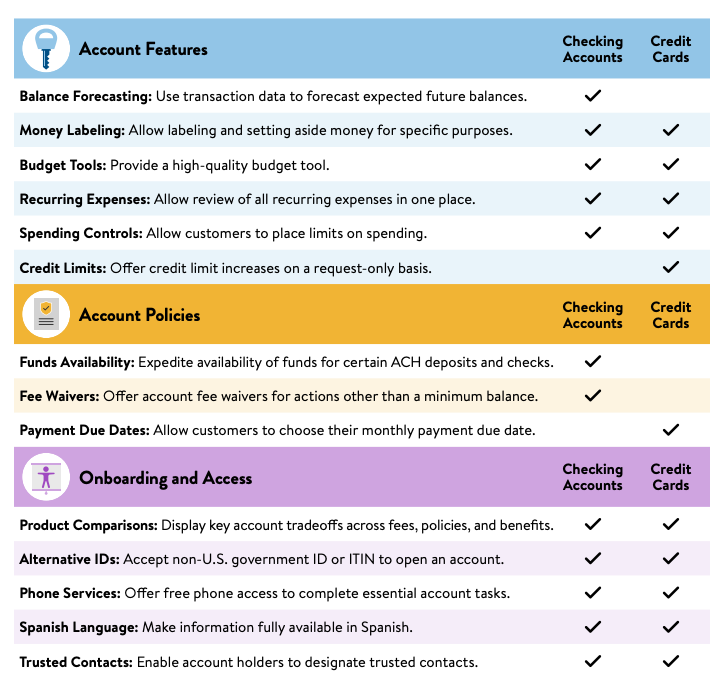

As I mentioned earlier, the standards created by the FHN are much more specific and prescriptive. They focus exclusively on checking accounts and credit cards — the foundation of daily consumer money management — and each standard includes research demonstrating the financial health impact, in-market examples, and implementation advice.