{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Friday, Fintech Takers!

I am finishing up today’s newsletter while sitting out at the Bonneville Salt Flats in Utah, drinking a beer and listening to a live concert by the Piano Guys.

My thanks to Colton Pond and the LoanPro team for their typically exceptional hospitality. Now, on with the newsletter!

- Alex |

Was this email forwarded to you? |

|

|

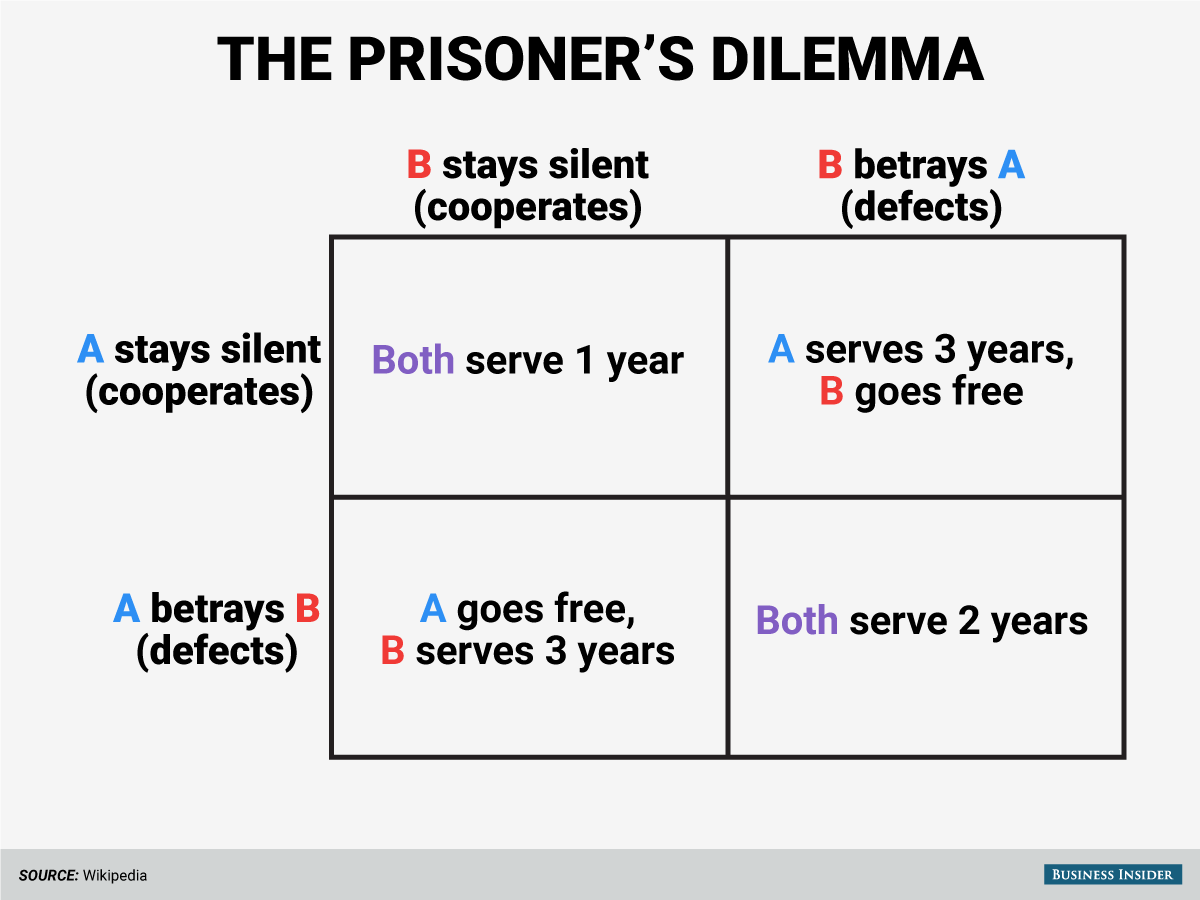

It occurs to me that I didn’t properly explain the prisoner’s dilemma last time I mentioned it in the newsletter, so let’s do that now.

The prisoner’s dilemma is a game theory thought experiment involving two rational agents, each of whom can either cooperate for mutual benefit or betray their partner ("defect") for individual gain. The dilemma arises from the fact that while defecting is rational for each agent, cooperation yields a higher payoff for each. The thought experiment was dreamed up by a couple of mathematicians at the RAND Corporation in 1950.

The canonical version (which is where the thought experiment gets its name) has two people who have been arrested under suspicion of committing a crime. The cops offer a deal to each prisoner. If they testify against the other person and that person stays silent, they go free, and their partner in crime gets three years in prison. If both people choose to testify, they each get two years in prison. If neither person testifies, they each get one year in prison.

|

In related news:

Plaid Inc. agreed to pay JPMorgan Chase & Co. for its consumer data, the latest accord in a battle between financial technology firms and banks over who can access the sought-after information.

The largest US bank and Plaid, which connects apps with bank accounts, updated a data-sharing agreement with a set pricing structure, according to people familiar with the matter, who asked not to be identified discussing nonpublic information. Plaid and JPMorgan confirmed the fees but wouldn’t disclose the amount. In addition to a fee structure, the updated pact includes commitments from both firms “to ensure that consumers can access their data safely, securely, quickly and consistently into the future,” according to a joint statement Tuesday. Plaid defected!

JPMorgan Chase put all the data aggregators in a situation where they were collectively better off to cooperate, but individually better off to defect, and Plaid defected!

I did not expect Plaid to be the one to give in first. So, let’s analyze this decision by asking a series of questions about what happened and what it means for the ecosystem. |

What exactly did Plaid and JPMorgan Chase agree to? |

JPMC and Plaid had a data access agreement in place, which governed how Plaid used the bank’s open banking APIs on behalf of its customers. That agreement (like all of JPMC’s data access agreements) included a clause that allowed the bank (with some advanced notice) to start charging for access to those APIs.

The initial pricing that JPMC gave to each of the aggregators (taking advantage of the clause in its contracts) was prohibitively high. It’s unclear to me if the bank was always planning to lower its prices in negotiations or if the CFPB’s U-turn on the Bank Policy Institute’s lawsuit reduced its leverage to the point where it had to lower its prices (I think it’s a bit of both), but JPMC did indeed lower its prices significantly in its final deal with Plaid.

The structure of the pricing remains unchanged, however, which means that payments use cases will be significantly more expensive for Plaid than non-payments use cases. Plaid is reportedly not planning to pass the costs of paying JPMC on to its customers (at least not right now), which means it is eating the costs itself and reducing its margin. Plaid is best positioned, among all aggregators, to do this, as it is the most expensive provider in the market (meaning it has the biggest margin) and it processes the most volume (which means it receives the biggest volume-based discount).

The agreement between Plaid and JPMC also includes changes to the way that the two companies integrate and exchange data. The Bloomberg article is fairly vague about this, writing that, “the updated pact includes commitments from both firms ‘to ensure that consumers can access their data safely, securely, quickly and consistently into the future.’”

My understanding is that each company will make specific technical investments to reduce the operational burden on JPMC’s systems (which is something that the bank has been complaining about incessantly over the last few months) and improve the experience of using Plaid for the company’s end customers.

A specific example is webhooks, which essentially act as “reverse APIs” allowing JPMC’s system to notify Plaid in real time when a specific customer’s account data has changed. This will help reduce the number of calls to the bank. Instead of an earned wage access app checking every day to see if a customer’s income has changed, it will only hit JPMC’s system after the bank notifies Plaid that the customer’s income has, in fact, changed.

|

This is the multi-million dollar question. I think the simplest explanation is that Plaid is planning to go public in the near term (it just raised a funding round, so it doesn’t need to go public right away, but it seems like it's in the cards in the next year or two).

When a private company files to go public, it is required to disclose information about its business, including “risk factors” that could negatively impact the performance and value of the company. If you want to boil this decision by Plaid down to its most elemental form, I think the reason that it decided to strike a deal with JPMC is that it didn’t want to have to disclose this specific risk — that JPMorgan Chase (and perhaps other banks) might impose prohibitively high fees or cut off access entirely to the critical fuel that powers Plaid’s business — in a future S-1.

This is about protecting Plaid’s downside.

Now, to be clear, it’s possible that Plaid won’t need this protection. The CFPB has initiated the process of revamping the open banking rule. There is a chance that a revised rule still ends up prohibiting data providers from charging fees. Plaid, ironically, is going to argue for this in its lobbying efforts and comments to the CFPB moving forward (the agreement with JPMC allows Plaid to continue arguing whatever it wants on the policy/regulation side).

However, it’s clear that Plaid was unwilling to risk it. This is understandable given that the current CFPB is … unpredictable. And the Loper Bright and Corner Post decisions mean that any new rule that the CFPB comes up with (even if it keeps the status quo on fees) will likely be immediately and endlessly challenged in court. |

Doesn’t Plaid’s decision screw over the other data aggregators? |

Indeed, it does!

I was hanging out with a bunch of open banking people this week, and trust me, they were pissed. They didn’t know this was coming, but they understand perfectly what it means.

JPMC just changed the facts on the ground. Paying for open banking data access is now a market practice in the U.S. The CFPB and the courts will take that fact into consideration.

My best read on the situation is that JPMC is now going to take this revised deal to all the other data aggregators and point expectantly at the signature line.

(Editor’s Note — JPMC doesn’t have to offer the other aggregators the same deal it agreed to with Plaid. The others don’t have Plaid’s leverage. However, I think it probably will. The bank doesn’t see these fees as a revenue generation opportunity, and the anti-trust risk of offering different terms to different aggregators is real.)

But which of them will sign it? Here are my best guesses at the moment: - Yodlee? Yes. It works with a lot of the big banks to enable “data in”.

- MX? Probably. It won’t be great, but MX can (and probably will) live with it.

- Finicity/Mastercard? Yes. It values its broader commercial relationship with JPMC.

- Tink/Visa? Nope! It chickened out and left the U.S. market! Might have been a bit premature!

-

Akoya? Yes, but the larger question is whether JPMC and Akoya’s other owner banks will continue to put money in now that Plaid has been brought to heel.

-

Trustly? Maybe, but it’s tricky. Trustly’s entire business is pay by bank, and JMC’s pricing is intentionally designed to screw up the economics of pay by bank. And unlike Plaid, I think JPMC would be willing to cut off Trustly’s access to its APIs if Trustly doesn’t agree to its terms. In this scenario, Trustly could fall back to screen scraping, but that’s not ideal for anyone.

-

Stripe? This is the one I can’t figure out. Stripe aggregates data directly from some of the big banks and then wraps other aggregators (MX, Finicity, etc.) to round out its coverage. From what I can tell, pay by bank is a good and growing business for Stripe, but it’s not so existentially important to the future of the company to make not paying fees a hill it would obviously want to die on. And yet, Stripe has been one of the most aggressive companies in the open banking ecosystem at pushing back on JPMC’s attempt to charge fees (it submitted a very early comment letter to the CFPB on that topic), and it has the money and political influence to make JPMC’s life much harder on this issue, if it wants to. I have no idea what it will do.

|

How will the other banks react? |

I’ve analogized the other banks to penguins that have been watching one of their own (JPMC) dive off an iceberg and waiting to see if it gets eaten by seals. My best guess is that this news will embolden a few of the other penguins to make the leap (PNC, Citi, U.S. Bank, Capital One, and Wells Fargo are the most obvious candidates).

Now, to be clear, it will be more difficult for the other banks to do what JPMC just did. As I understand it, none of them have the same clause in their data access agreements that would allow them to add pricing into their existing contracts. This reduces these banks’ leverage and likely will make the negotiations with Plaid and the other aggregators a more drawn-out process.

Additionally, the other banks aren’t as big as JPMorgan Chase. I know that’s an obvious statement, but it’s an important part of the story. JPMC represents 10-15% of Plaid’s total traffic. None of the banks in the next tier (Citi, Bank of America, Wells Fargo, U.S. Bank) are close to that, and when you start getting into the back half of the top-10 banks by deposits (PNC, Truist, Capital One), it gets really, really small (think less than 1% of Plaid’s traffic).

These banks are going to ask Plaid for the same deal that JPMC got, and they’re not going to get it. Rather, they are likely to get JPMC-level pricing, prorated according to their contribution to Plaid’s total traffic. I would expect the other aggregators who decide to sign up to pay fees to take a similar approach in their negotiations. And for banks and credit unions outside the top 12-15 in deposits? They’re probably not getting any deal at all.

If that ends up being how this goes, it will further entrench the competitive disadvantages that the 8,000+ banks and credit unions at the bottom of the market face, relative to their largest peers. This will become clear as banks and credit unions begin to go on offense with open banking. First National Bank of Somewheresville will have to pay to access Chase’s data, but Chase will get First National Bank of Somewheresville’s data for free (or very cheaply).

| What will the CFPB choose to do? |

To be blunt, the CFPB is screwed. This deal between Plaid and JPMC shifts the facts on the ground, but it doesn’t materially change the position that the bureau is in.

If the CFPB listens to the data aggregators and fintech companies and decides to keep the prohibition on fees in the revised rule, the Bank Policy Institute will sue it immediately.

If the CFPB adjusts its approach based on this deal and decides to simply stay silent on the question of fees in the revised rule (leaving it up to the market), the fintech trade associations will sue it immediately.

(Editor’s Note — There was a lawsuit against JPMC that the Financial Data and Technology Association of North America was about to file, before this deal with Plaid was announced.)

If the CFPB decides to take on the extraordinarily complex work of calculating data providers’ costs for supporting open banking and setting a specific permitted cost-recovery fee in its revised rule, it will be sued by everyone immediately, and until the end of time (Editor’s Note — For an example of what this would look like, check out the legal hell that the Durbin Amendment has been mired in.)

If you forced me to guess, I would bet on option #2 (removing the prohibition on fees and letting the market figure it out), but the CFPB really doesn’t have any good options at this stage. | Will anyone in this ecosystem ever trust anyone else in this ecosystem ever again? |

No. At least not anytime soon.

In game theory, there’s a derivation of the prisoner’s dilemma called the iterated prisoner's dilemma, in which you have the agents participate in multiple rounds of the game. In this version, the agents remember what everyone did in the prior round, which allows for cooperation to emerge organically over time. However, the most effective strategy in the iterated prisoner’s dilemma is something called “tit-for-tat with forgiveness”. This strategy requires that individual agents punish those who defect (tit-for-tat) until they stop, at which point the agents can stop retaliating (forgiveness).

Put simply, any rational strategy for cooperation in an iterative game (which is exactly what the free market is) requires disincentives for betrayal. In the U.S. open banking ecosystem, the nexus for cooperation is the Financial Data Exchange (FDX). While FDX’s mission was always fairly narrow (defining technical standards for open banking), it had become, over the years, an informal organizing mechanism for cooperation and coordination between banks, data aggregators, and fintech companies.

There has always been tension inside FDX, largely stemming from questions about how the organization apportioned influence between banks, aggregators, and fintechs. However, that tension boiled over when BPI sued the CFPB over the open banking rule last year. It got worse when JPMC pushed for fees (which not all banks were thrilled about). And now Plaid is fracturing what little trust still existed between the aggregators.

Take the technical improvements that Plaid and JPMC are making as a part of this deal as an example. That is essentially the creation of two different tiers of APIs in open banking: the basic FDX API (which will, perhaps, remain free or, at least, low cost) and premium APIs (which will be proprietary to specific banks and aggregators and will, for a higher price, deliver better service). That two-tiered structure might be preferable for Plaid and JPMC, but it may not be for the smaller guys. Nor is it necessarily the best outcome for the ecosystem as a whole. And that brings us to our final question … |

Are fees the best model for the U.S. open banking system? |

I’ve been wrestling with this question for months.

On the one hand, most other countries that have regulated open banking do allow data providers to charge fees. The models in these countries differ. Some take a premium API approach. Others define a simple cost-recovery fee. But most allow data providers to charge fees in some capacity. There’s probably a good reason for this.

There is value in aligning the interests of all participants in a market. If you don’t, you run the risk of certain participants (incumbents, most notably) subtly working to sabotage the system. This problem should not be underestimated. Companies can be surprisingly petty when they feel motivated to be. Banks can (and will) rub sand in the gears of open banking in ways that are difficult or impossible for regulators to stop, but that subtly degrade the effectiveness of the entire system.

It may be worth allowing fees, even if they are fairly small and unevenly distributed across the ecosystem, just to reduce the odds of this petty behavior. Or, perhaps, we shouldn’t over-index on what the rest of the world does, given how different the composition and competitive dynamics of the U.S. market are from other, similarly mature financial services markets. Truly, I don’t know.

We may need to just wait and see how this deal between Plaid and JPMorgan Chase, and other deals that are likely to follow, play out. |

|

|

MORE QUESTIONS TO PONDER TOGETHER |

Big news for the endlessly curious (yes, you): I’m collecting your fintech questions on a rolling basis.

What’s keeping you up at night? What great mysteries in financial services beg to be unraveled? Think of it this way, if a stranger is a friend you just haven't met yet, your question is a Fintech Takes conversation waiting to happen.

One that could headline a Friday newsletter or be answered in an upcoming Fintech Office Hours event.

Drop your question here, whenever inspiration strikes! |

|

|

FINTECH TAKES: BUILDERS SUMMIT |

As you may know, Fintech Takes is hosting our first-ever in-person event on November 12th and 13th in the mountains outside Bozeman, Montana.

The Fintech Takes: Builders Summit is the industry event that I’ve always wanted, but have never quite been able to find. We are bringing together experienced founders and operators from banking and fintech — the folks who are actually building products in our industry — and giving them the content and networking opportunities they need to find (and understand) the next big problem they are going to tackle.

If that sounds like something you’d be interested in participating in, apply to attend or hit reply to this email to get more information on sponsorship opportunities. We still have room, but it is going fast! |

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if profile.vars.rh_reflink_11}  | Share with Fintech Takes, get cool stuff! | Have friends who'd love Fintech Takes too? Click the link below to share with your friends and get awesome rewards when they subscribe! | |

|

PS: You have referred {{profile.vars.rh_totref_11}} people so far | | Share Fintech Takes! | |

|

{/if} |

|

|

Get your brand in front of 56,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|