Hello! I am thrilled to be writing once again about CECL, something I have done sporadically since the standard went into effect in 2020 for bigger banks. I am, sadly, a little rusty, but in my defense, the double count was a particularly complex aspect of an already complicated standard.

This piece assumes both a working knowledge of bank M&A and a baseline knowledge of financial accounting and reporting, but also that you, dear reader, are not an accountant. You might get a little lost in the sauce of this piece, and to some extent, that’s part of the point. I don’t have a ton of background resources here to share, so just console yourself that this M&A double-count madness is ending. |

Was this email forwarded to you? |

|

|

Why Two (Accounting Entries) Wasn’t Better Than One |

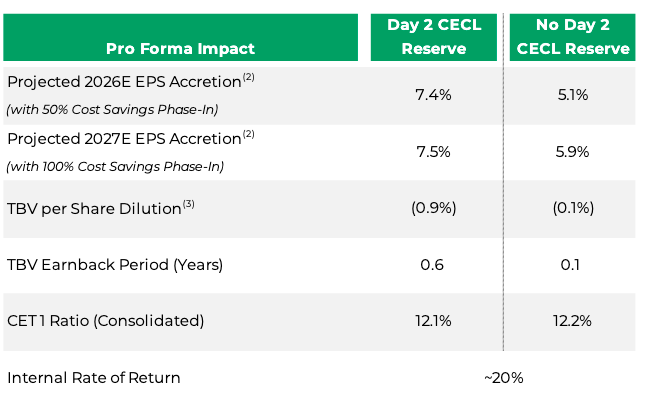

In June, Glacier Bancorp announced it agreed to acquire Mount Pleasant, Texas-based Guaranty Bancshares for $476.2 million. The deal values the $3.2 billion Guaranty at 162% of its tangible book value per share. According to the $29 billion Glacier’s investor presentation, acquiring Guaranty will dilute the combined bank’s tangible book value per share by either 0.9% or 0.1%, and it will take the bank either 0.6 years or 0.1 years to earn that dilution back. The combined bank’s common equity tier 1 ratio will either be 12.1% or 12.2%.

Wait, what? Why the difference between these deal metrics? |

Glacier’s presentation had two sets of numbers in anticipation of a broad accounting adjustment that will impact all bank deals announced in 2026, and some in 2025. The group that sets accounting policy in the U.S. — the Financial Accounting Standards Board, or FASB — changed how banks account for loans they’ve acquired in a deal. This update eliminated what was colloquially called the “CECL double count” — a complicated, layered accounting approach that made acquired loans appear more expensive and made it harder for acquirers to report the performance of these loans as they paid off. So let’s break down why it’s a big deal and what the new procedure is.

|

You Can Skip This Section if You Know About CECL |

The layers in this joke. Believe it or not, this was from the OCC’s accounting update presentation at the 2021 AICPA Bank & Savings Conference, and yes, I have had this screenshot in my files since then. |

If you’re one of the few people who work in banking but have managed to make it to 2025 without knowing what CECL is, well: Today is your lucky (unlucky?) day. The loan loss standard that all companies, including banks, follow today is called the current expected credit loss model, or CECL. CECL went into effect in 2020 for most big banks (which was honestly crazy timing with the pandemic) and in 2023 for all banks.

CECL was the largest change to bank accounting in 40 years and was designed so that banks would set aside money for loan losses before the losses happened. It stipulates that banks calculate a loan’s lifetime credit losses at origination, using a mix of historical losses and economic outlook to come up with a reasonable estimate, and update that loss figure over time as the borrower’s financials or the economic outlook change. Quarterly changes to a bank’s loan loss outlook are recorded as a provision for credit losses on the income statement; the total amount set aside for loan losses is recorded in the allowance for credit losses, or ACL, on the balance sheet.

|

Brace Yourself for Some Painful Accounting Discussions |

Can a meme from my favorite movie soothe the pain that I’m about to inflict on you, dear reader? |

When these bank accounting rules were applied to bank M&A, the result wasn’t always pretty or useful. But let’s back up to the due diligence phase, way before a deal gets inked. A bank buyer does a lot of due diligence on its target, especially around the seller’s credit quality. Buyers normally buy all or most of the loan book, but they need to mark the acquired loans to what the buyer thinks they’re worth. This valuation, or mark, is usually a discount that reflect the interest rate the loan carries, its credit risk, the underwriting or other variables, like whether the buyer wants it (maybe the loan is in a business line the buyer doesn’t really want to be in, or it’s in a state or city the buyer doesn’t want to grow in).

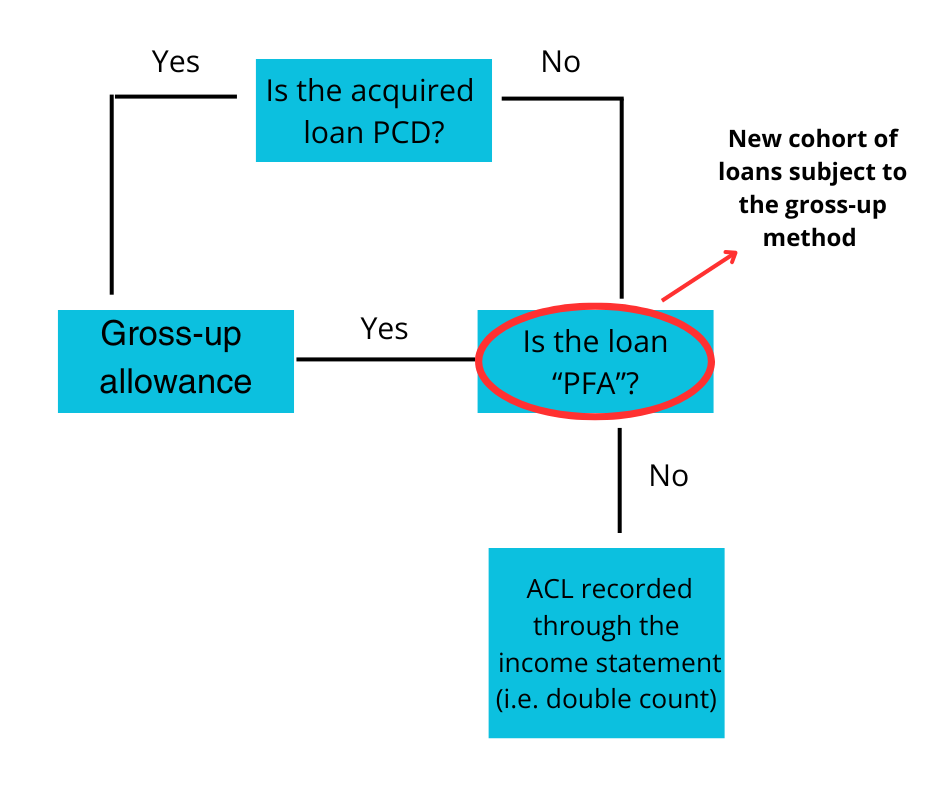

Acquired loans that show evidence of credit issues are called “purchase credit deteriorated,” or PCD; loans that are performing as underwritten are called “nonpurchase credit deteriorated,” or non-PCD. After the standard change, non-PCD loans will be called purchased financial assets, or PFAs.

If a bank acquired loans with credit deterioration, it would account for them under an approach called the “gross up” methodology. This approach allows the acquirer to record the fair value of the loan gross, with the expected credit losses recorded at purchase directly to the acquirer’s allowance. If the borrower pays off their credit deteriorated loan beyond what the acquirer thought it was worth, the bank records this better-than-anticipated credit performance as a reduction in the ACL and a decrease in the provision for credit losses.

“This ‘gross-up’ for credit losses recognizes that the credit discount is baked into the purchase price of such assets, and therefore does not impact earnings on the purchase date,” wrote Spencer Hathaway, a senior manager at Baker Newman Noyes. Believe it or not, this is the easy way!

Under current guidance, bank buyers use a different, harder approach for non-PCD loans. A buyer first had to assess the fair value of these loans, using their expectations on interest rate, credit performance or other factors. It records that loan at its fair or cost value, including its expectation for the loan’s lifetime credit loss, on its balance sheet the day the deal closes.

Then, after the deal closes, the bank takes its estimate of the allowance for credit losses and records it through a debit to the provision for credit losses on the income statement and a credit to the allowance, which impacts earnings. That Day Two allowance reduces the bank’s capital; the one-two punch of the fair value estimate’s credit component and the allowance for credit losses creates the deal’s “double count.” The double recording also makes the deal more expensive from a capital perspective for the acquiring bank.

Remember, this is all for a loan that doesn’t have credit issues, and right now, most acquired loans don’t. This loan’s expected lifetime losses are now in two places on the financial statements. It’s baked into the loan’s fair value on the balance sheet in the ACL and recorded through the income statement. “ What happens, essentially, is you have less capital from the double count of expected credit losses,” said Kevin Brand, a partner in the advisory group at Crowe. “You have more accretion on non-PCD loans going forward because you have more of a discount on the loan’s cost basis, but you start off with less capital and more tangible book value dilution.”

The double count hangs over the loan for its entire lifetime like a bummer accounting cloud. As the loan pays down, the buyer accretes both the interest rate mark and credit mark into income, along with the contractual interest of the loan. And because the fair value of a non-PCD loan includes both a credit mark and an interest rate mark, the bank needs to record more accretion income than is reflective to bring the loan’s yield to market rates. Recording more accretion income on the loan contributes to “noisy” earnings, which leads analysts and investors to discount, or apply haircuts to, any accretion income in the acquired bank’s quarterly results. Contrast this to a PCD loan, where the accretable mark basically excludes the Day One credit component.

“Several mergers in the last few years have resulted in significant provisions impacting earnings and capital in the quarter where the acquisition took place, only to be followed by several subsequent quarters of low or negative provisions as overall credit losses were reevaluated,” Spencer wrote. |

Having Explained All That, Feel Free to Forget It |

But all that’s going away! After the change goes into effect, buyers will be allowed to account for acquired, or “seasoned,” loans that are older than 90 days under the “gross up” method. (Loans less than 90 days old are considered essentially newly originated and would still have this double-count treatment.) This update reflects that most banks, analysts and investors think about the loans a bank originates as being different from loans a bank purchases, rather than merely focusing on acquired loans with credit deterioration and those without.

|

Credit for the flow chart goes to JP Shelly, Workweek design credit to Claire Monterroyo. |

“From a deal perspective, [getting rid of the double count] makes it more clear and aligned to what the value is you're actually acquiring,” Kevin says.

When FASB finalized the standard in 2016, it expected that there would be more acquired loans with credit deterioration, so the amount of assets accounted for under the “gross up” method would be higher. That didn’t happen, and by 2021, users of the financial statement were already telling the board that the double count was producing unintuitive figures that were difficult to calculate and hard to trust.

“The separation of PCD versus non-PCD overstates the initial tangible book value dilution in a deal, and it overstates the initial accretable yield in a deal,” said an analyst in a FASB roundtable.

This update is effective for annual reporting periods after Dec. 15, 2026, and the interim reporting periods within those annual reporting periods. Early adoption is permissible for any annual or interim reporting period where financial statements haven’t been issued.

There may be other, tack-on effects that follow the standard’s update. JP Shelly, a partner in Crowe’s audit and assurance practice, flagged that banking agencies may need to clarify regulatory capital rules about whether the allowance on PCA loans, which is included in the gross up, is included or excluded from the combined bank’s total risk-based capital ratio.

Some deals announced this summer have already included two sets of figures in anticipation of the standard change. These presentations and their dual numbers demonstrate that the double count made deals more expensive and took longer to pay off. Under the double count, Cincinnati-based First Financial Bancorp’s $325 million acquisition of Westfield Center, Ohio-based Westfield Bancorp would dilute the combined entity’s tangible book value by 8.1%, which would take 3 years to earn back. Excluding the double count, the deal dilutes tangible book value by 7.6%, which takes 2.9 years to pay off.

|

The motivations behind this change — only five years into CECL — reminded me about the point of accounting, of these rules and the process they create for, in this case, acquiring banks. I’m not an accountant, but I write about banks, and so I am a user of the financial statements they create. For me, accounting rules matter because they help create accurate and realistic pictures of a company’s financial statement (See also: Enron!). The CECL double count did the opposite.

“A lot of times, accountants say, ‘It's just numbers. It's just reporting. Don't change what you're going to do based on the accounting and how you have to report. You have economic reasons for doing things that are real,’” Spencer told me. “And most of the time, that's not an issue. But with this particular case, it was the tail wagging the dog — I might not do this deal because of the way I have to report it.”

It’s always a delicate dance to try to create an accounting system and rules that reflect the world accurately, in a way that’s fair to management teams and transparent and believable to investors and everyone else. It’s great, honestly, that the board listened to feedback on how the standard could be improved and picked an approach that is easy and low-cost to implement. Hopefully, after this change, the metrics and financials reported in a deal more closely reflect the actual way the acquirer thinks about an acquired asset as it moves through its pay down, and it makes more sense for everyone else.

|

|

|

What’s on my mind and filling my time: |

🛄 Manifesting: An app that helps friends and families manage group travel expenses. I read an article about friends who created a group travel fund by opening a shared bank account and making weekly contributions to it, and I absolutely need a fintech to fix this. It’s such a clunky solution, but there are real issues when it comes to paying for shared lodging or splitting a big meal! Someone hit me up, I have ideas.

|

🪟 Reading about: how pledging collateral to the discount window “increases the likelihood of borrowing primary credit in instances where a [depository institution] experiences a shock,” according to research from the Federal Reserve. That may be an obvious conclusion, but the demise of Silicon Valley Bank and Signature Bank both involved the inability to access the discount window borrowings in a timely manner. Also, this is a reminder that one way banks can request an advance (or borrow) from the discount window is by calling their local Reserve Bank.

|

Thank you to all the accountants who patiently explained the accounting treatments to me and reviewed the text for accuracy. Any mistakes are mine solely.

If you’re like Alex and you’re keeping a running list of “silly phrases accountants have come up with,” I hope you enjoyed the phrase in this newsletter. Thanks for reading!

- Kiah |

|

|

Get your brand in front of 55,000+ financial services execs. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|