{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Monday, Fintech Fans

Football is stupid. College football is stupid. The college football overtime rules are stupid. Whatever. I hope your weekend went well. And I hope you’re ready for a big week. Fall fintech season is officially here! - Alex |

Was this email forwarded to you? |

|

|

Klarna is trying again:

The company has confirmed that its US initial public offering is back on. It has filed with the SEC to list on the New York Stock Exchange, with plans to sell 34.3 million shares at a range of $35 to $37 per share. This would see it valued at around $14 billion. In April, Klarna paused plans to list its ordinary shares on the New York Stock Exchange amid market turbulence sparked by President Donald Trump's tariffs. |

The hardest and most profitable thing to do in consumer finance is to lend money. And, as I like to say around here, lending is a learning business. Anyone who wants to get good at it needs to spend a few years getting kicked in the teeth.

This is why, in general, successful consumer fintech companies tend to start in lending and then expand into other areas like deposits, payments, and wealth management (possibly becoming a bank at some point along the way). You have to master lending at a small scale if you want to avoid losing your shirt when you scale up. Deposits, payments, and wealth management, while tricky in their own ways, do not tend to require the same long incubation period to build competence.

On a basic level, I think this is why things have worked out better for SoFi and LendingClub than they have for Varo. And why many industry observers (including myself) continue to worry about the long-term prospects for Chime, despite all the success that it has had to date. To win in consumer finance, you need to be good at lending money.

This is a helpful lens through which to view Klarna, and the BNPL market more broadly.

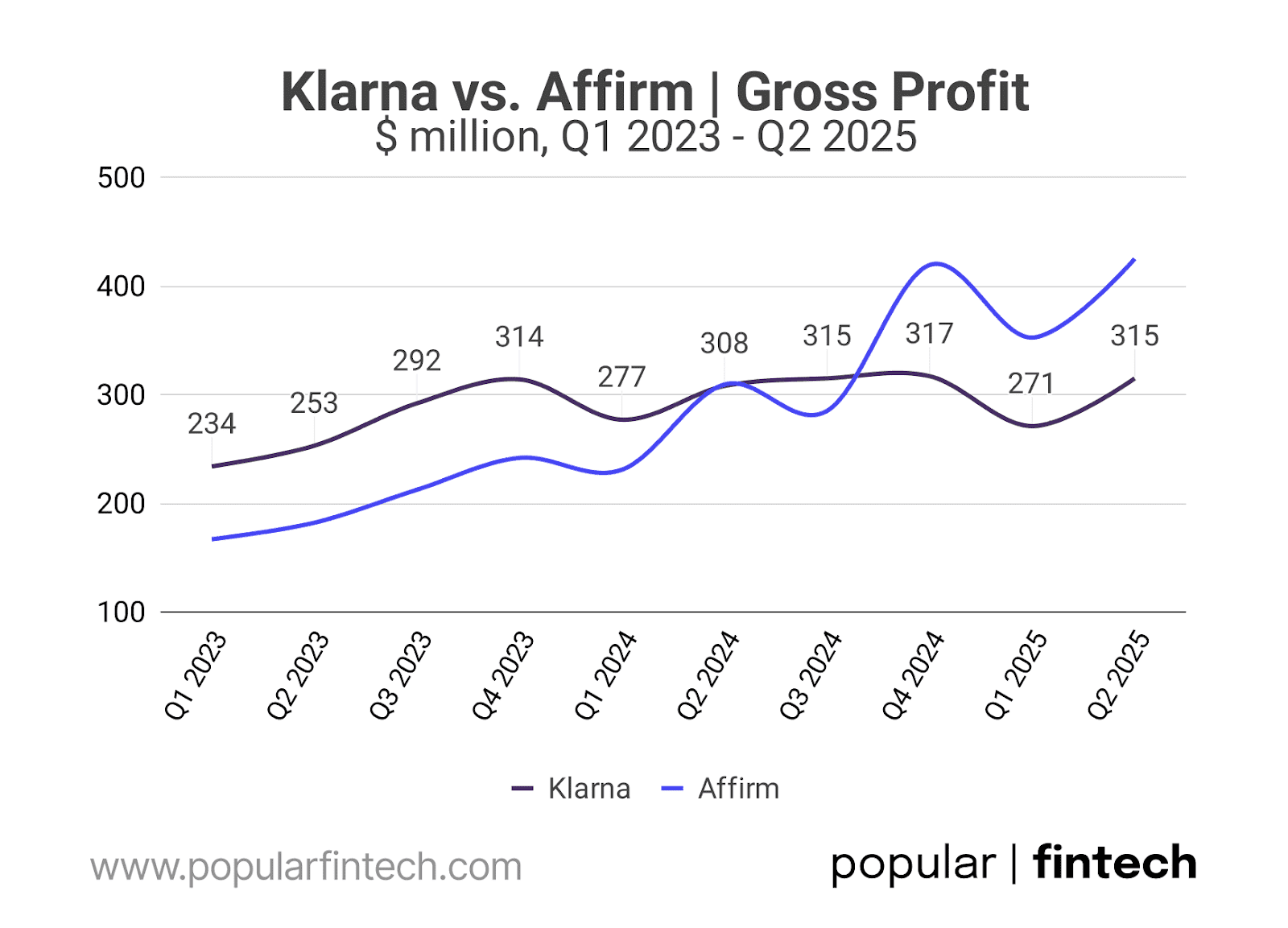

My fintech friend Jev Kazanins, author of the indispensable newsletter Popular Fintech, wrote a great piece on Klarna’s second attempt at going public. In it, he points out that Klarna has begun to lose ground to its biggest BNPL rivals:

Over the last four reported quarters (Q3 2024 - Q2 2025), Affirm’s “gross profit” came in at $1.48 billion, growing 49% YoY. Meanwhile, Klarna generated $1.22 billion in “gross profit,” with a much slower 9% growth rate. In short, Affirm is now bigger and growing much faster than its Swedish rival. |

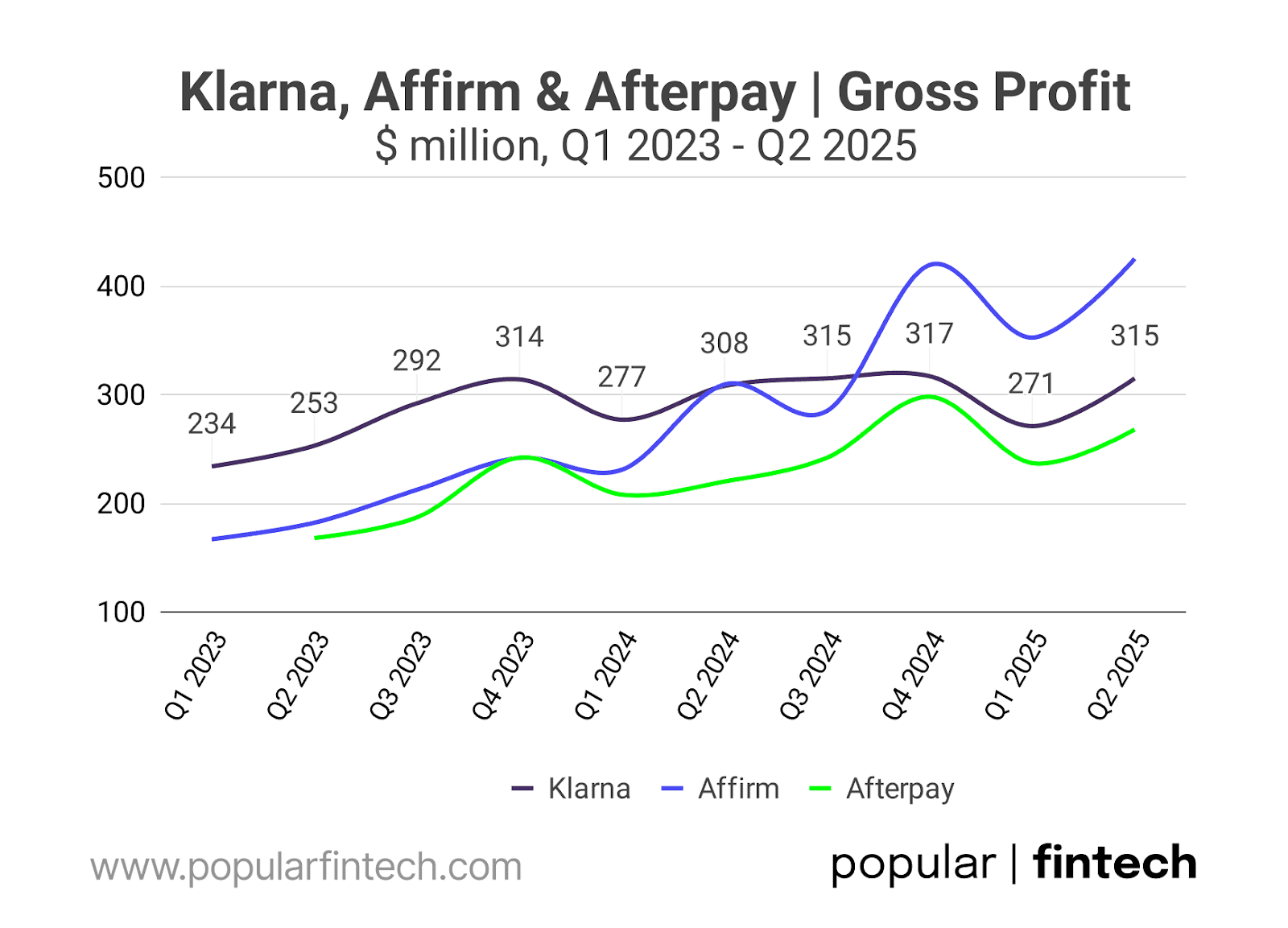

Even Block’s Afterpay is catching up with Klarna, posting $1.05 billion in “gross profit” and growing at a solid 22% YoY. Perhaps, Klarna was trying to prioritize profitability over growth as it prepared for the IPO, or maybe it was trying to lower its default rates to calm future investors. Whatever the reason, the outcome is clear: Klarna is falling behind in the most important aspect of a growth company, growth itself. |

Now, I think the company is in a tricky situation. It's turned into a laggard when it comes to growth, but it has yet to prove it can operate profitably. The company even seemed to pull back on its big thesis that AI could replace its support staff, returning to hiring instead. In the meantime, Affirm managed to become GAAP profitable without hurting its growth one bit. |

That last point from Jev is key: Affirm is finding an optimal balance between growth and profitability, whereas Klarna is (comparatively) struggling at both.

I think the reason for this is simple. Affirm is a lending business. Klarna is a payments business.

Roughly 85% of Affirm’s lending volume comes from monthly installment loans (primarily interest-bearing, but with a growing number of 0% loans). Only 15% come from short-term 0% interest pay-in-x loans (pay-in-4 is the most common structure). And even Affirm’s direct-to-consumer debit card is driving lending volume for the company. Roughly 80% of Affirm card gross merchandise volume (GMV) in this latest quarter was interest-bearing.

By contrast, while Klarna has actually seen more GMV volume shift from pay now (i.e., debit) to pay later (i.e., lending) over the last couple of years, the vast majority of that lending volume comes from short-term, 0% interest pay-in-x products, rather than monthly installment loans. While pay-in-x BNPL products are legally considered loans, they are much more similar, from a unit economics perspective, to payments. A comparatively lucrative form of payments, but payments nonetheless. And as Jev points out, the growth opportunity for both companies is to extend the reach of their integrated lending capabilities by growing their respective debit card franchises: Affirm has surpassed 2.3 million cardholders with the Affirm Card, all with hardly any marketing.

Klarna serves five times the number of consumers and does three times the GMV that Affirm does, making it more of a payments company than a pure lender. Given that, cross-selling the Klarna Card should be a no-brainer at its scale. At this point, it feels like this is Klarna’s opportunity to lose. Indeed, but even if Klarna wins that opportunity and accelerates revenue growth through its new debit card, the profitability waiting on the other side of that growth isn’t nearly as attractive as the profitability awaiting Affirm. |

A couple of interesting bits of news from OpenBankingLand.

First, Stripe wasted no time in forcefully pushing back against JPMorgan Chase:

Allowing JPMorgan Chase & Co. to charge fees while the CFPB considers whether to allow the bank and others in the industry to do so “will cause significant damage to the marketplace and consumers,” Stripe said in comments filed with the agency Friday and made public Tuesday.

The comments by Stripe, a payments-focused firm, come as the CFPB attempts to revamp its rule governing the sharing of personal financial data. The company acknowledged that it’s commenting at an “early juncture,” but said that allowing banks to levy charges while the regulatory landscape is unclear would mean that “thousands of businesses and millions of consumers will suffer irreparable harm before the CFPB can finalize a rule that prohibits or limits such fees.”

And second, JPMC officially selected Nova Credit to help power its efforts in cash flow underwriting:

Nova Credit … today announced that Chase has selected Cash Atlas™ to power its cash flow underwriting capabilities. Chase will also use Nova Credit’s Credit Passport® to access and decision with international credit data. These solutions will enable Chase to serve more customers across the U.S. who have limited credit history or are underserved by traditional credit models. |

Let’s take these in order. The purpose of the Stripe comment letter is very specific: To stop JPMC from implementing its aggressive new open banking fees until the CFPB’s revamped rule is finalized.

That’s why Stripe rushed to get this comment submitted. The pricing will start going into effect this month (Editor’s Note — My understanding is that no contracts have been signed yet, but talks continue), unless Chase is persuaded not to push forward with its original plan. Stripe has a few different ideas for how the CFPB can be persuasive on this issue, if it wants to be: |

-

Deter data access fee demands by maintaining existing compliance deadlines for the largest data providers.

-

Issue guidance clarifying that assessing fees for data access may violate the law if doing so would unduly impede consumers’ rights under Section 1033 to access their account information, and announcing that the CFPB stands ready to enforce the law today and/or enforce the rule once the compliance deadlines pass.

-

Monitor market developments and refer any instances of possible anti-competitive conduct to the Federal Trade Commission and/or Department of Justice.

-

Potentially leverage its emergency rulemaking powers under 5 U.S.C. § 553(b)(4)(B) to immediately halt any fees that would cause irrevocable harm to the marketplace and consumer data access rights under the law.

|

You’ll note that there is some ambiguity as to whether the current open banking rule, which was finalized under the Biden Administration, restricts data providers from charging fees right now, or if that prohibition goes into effect with the rules rolling compliance deadlines, which begin (for the largest data providers like JPMC) on April 1, 2026. Either way, Stripe argues that the CFPB needs to make it clear to Chase (and other banks interested in following its lead) that its proposed fees are unacceptable.

I’ll also point out that the last option that Stripe suggests — invoking the “good cause” exception to the Administrative Procedure Act to forego notice and comment rulemaking — is a really dangerous idea to suggest to this CFPB, especially given the Trump administration’s inherent lack of enthusiasm for proper administrative procedure. Invoking the “good cause” exception is the very definition of a double-edged sword. Regarding the Nova Credit news, it strikes me as a very positive development that JPMC is investing in cash flow underwriting.

Obviously, Chase has long been a participant in the regulatory discussions surrounding cash flow underwriting (dating back to the OCC’s Project REACh), and it likely already uses cash flow underwriting, to a degree, to assess its existing customers for loans. This news suggests that the bank is ramping things up, which will be a boon for consumers with thin, damaged, or absent credit histories. (Editor’s Note — The inclusion of Nova Credit’s OG Credit Passport product is also good to see. The capability to assess prospective borrowers from other countries needs to become table stakes in our industry.)

It’s also, obviously, ironic timing, given everything that’s happening on the regulatory front. However, it’s important to note that cash flow underwriting would be one of the least-impacted use cases in open banking under an API-access-for-a-fee model (there is generally plenty of margin available to cover the cost), and JPMC, for its part, has copious “on-us” data to use without needing to pay any fees at all (yet another benefit of being the biggest bank in the country).

|

Stripe and Paradigm officially announced their new Layer-1 blockchain, Tempo:

As stablecoins go mainstream, there’s a growing need for optimized infrastructure. Much of today’s crypto stack either explicitly or implicitly caters to trading (a highly valuable use case in its own right) but is comparatively underoptimized for payments.

Tempo is purpose-built for stablecoins and real-world payments, born from Stripe’s experience in global payments and Paradigm’s expertise in crypto tech. We are building the chain with design input from global leaders in AI, e-commerce, and financial services: Anthropic, Coupang, Deutsche Bank, DoorDash, Lead Bank, Mercury, Nubank, OpenAI, Revolut, Shopify, Standard Chartered, Visa, and more. We are excited to further crypto’s ability to tackle real-world use cases including global payments and payroll, remittances, tokenized deposits for 24/7 settlement, embedded financial accounts, microtransactions, agentic payments, and more.

|

The Whiplash quote seems appropriate for this story, given that the last time a large tech company attempted to launch a high-performance, payments-centric blockchain and stablecoin, things got … a bit tense. Back then, the tension was between Facebook and the regulators and incumbent banks.

Today, the potential for tension seems to be between Stripe and Paradigm, which are saying all the right things about creating an unbiased and decentralized network, and lots of folks in the crypto/stablecoin ecosystem, who seem concerned about the temptation Stripe will feel, at some point down the road, to tilt the rules of the network in its favor.

The best articulation of those concerns that I have seen is this Twitter thread from Christian Catalini, who worked on Libra/Diem and is now the co-founder and Chief Strategy Officer at Lightspark. Allow me to quote from a few of the tweets in his thread:

The problem with corporate chains like Tempo isn't a matter of code—it's a matter of incentives. We already know the script. A tech player builds a network and promises fairness to get everyone on board.

But once they have a captive market, the temptation to tilt the playing field becomes irresistible. Would a sane competitor bet its future on Stripe's promise not to eventually favor its own products?

Ultimately, Stripe's Tempo is a referendum on the ghost of Libra. If that ghost was merely a product of bad timing, then Tempo is poised for a historic victory, and the crypto world's original dreamers may finally have to accept a more pragmatic, centralized reality. But if Libra’s ghost is a warning about a fundamental truth—that any system with a single architect is built on a fatal flaw—then Stripe is not writing a new story. It is merely staging an entertaining, and very expensive, sequel. I doubt that we end up in the same place we did last time, with Maxine Waters screaming, “Are you a rusher, or are you a dragger or are you gonna be ON MY FUCKING TIME?” at Mark Zuckerberg. The regulatory environment, regarding stablecoins and blockchain-based payments, is entirely different today. However, as impressive as the team Stripe has assembled for this project is, I think it will be more challenging to get the ecosystem on board with Tempo than they may believe. |

|

|

2 READING RECOMMENDATIONS |

I’m still not sure what I think about agentic commerce, to be honest. I’m spending a lot of time talking to folks this week to learn more.

In preparing for those conversations, I found this thoughtfully written piece by Justine and Alex to be a valuable resource. |

If comparison is indeed the thief of joy, then banks and fintech companies should know who Becca Bloom is, because she is likely robbing their customers of some serious happiness.

And, as I wrote a few years ago, banks and fintech companies need to solve for happiness.

|

1 PERSON WHO HELPS BRING FINTECH TAKES TO LIFE |

We’re continuing our series of interviews with the humans behind Fintech Takes. This week’s human? Lindsey Quinn! What do you do?

Lindsey: I lead content strategy at Workweek. I help our creators build newsletters, podcasts, and events that reflect their values and truly connect with their audiences. My job is part strategy, part creative coaching, and part making sure the stuff we create actually feels human. How did you get to Workweek?

Lindsey: I started out in newsletters back in 2016 as one of the first writer hires at a daily business/tech email called The Hustle in San Francisco. We were seven people working out of the third floor of a house in the Sunset, and they had just hired their head of sales... a charismatic Missourian named Adam Ryan. I eventually headed the content team there and convinced Adam to hire an ops shark named Becca Sherman. Fast-forward nine years, and Adam and Becca had the hairbrained idea to co-found Workweek and brought me on as a creator coach and strategist. Life works in mysterious ways, I’ll tell ya.

Take us inside your job. What’s a small, specific, nerdy thing that you know or do in your role that our audience likely doesn’t understand?

Lindsey: At its core, my job is being the go-between for the business and the creative talent that drives it. I’ve seen firsthand how a deadline-driven content business can suck the joy out of creating. The best part of my job is finding ways to protect and kindle creators' creative spirit and helping them build the skills to evolve with their brands as they grow.

(Editor’s Note — Speaking from personal experience, creating content on a rigid weekly schedule is indeed a grind, and I am very thankful to have LQ on the team to continually help me breathe joy and life and creativity into the content. She is a delight to work with!) What’s one thing that you’ve done for Fintech Takes that you’re proud of?

Lindsey: Call it recency bias, but helping launch the Fintech Takes Banking vertical with Kiah takes the cake. Collaborating with Alex and Kiah to build the content strategy from the ground up, and working with Kiah to hone her voice in a new medium, has been incredibly rewarding. Please give us one non-fintech content recommendation. Can be a movie, TV show, book, article, or podcast. What content are you LOVING right now?

Lindsey: A Manual for Cleaning Women by Lucia Berlin. It’s a collection of semi-autobiographical short stories spanning the 60s, 70s, and 80s, inspired by Berlin’s childhood in Western mining towns, glamorous teenage years in Chile, three failed marriages, a lifelong struggle with alcoholism, and the various jobs she held to support her writing and four sons. It’s fantastic, funny, visceral, and the kind of book that makes good company.

|

|

|

🏀 FINTECH TAKES THE COURT 🏀 |

Yep, it’s happening again! I am DELIGHTED to officially announce the third annual “Fintech Takes The Court” 3x3 basketball tournament, which will take place in the morning on Sunday, October 26th, in Las Vegas.

This year’s tournament is being sponsored by SOLO, and it’s going to be the best one yet. If you’ll be attending Money20/20 (or just in Las Vegas that week) and are interested in getting off the Strip for a few hours and getting some exercise (or just coming to cheer the teams on!), fill out this form. Space is limited, so don’t wait 🙂

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if profile.vars.rh_reflink_11}  | Share with Fintech Takes, get cool stuff! | Have friends who'd love Fintech Takes too? Click the link below to share with your friends and get awesome rewards when they subscribe! | |

|

PS: You have referred {{profile.vars.rh_totref_11}} people so far | | Share Fintech Takes! | |

|

{/if} |

|

|

Get your brand in front of 56,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|