Hello! Kiah here. Welcome to Fintech Takes Banking, a weekly newsletter focused on things that I think are interesting or important for bankers.

I promised you some nerdy bank content, and today we are diving headfirst. Millennials are staring in horror at all the 2000s trends that are reemerging, so it felt like a good time to highlight a financial product that was popular during that era, and also went south in a big, big way. Welcome back to low-rise jeans, all the teen stores at the mall and CRTs. Let’s see what’s new this time around. |

Was this email forwarded to you? |

|

|

Throwing it Back to a 2000-era Financial Instrument |

Let’s make a bet.

You work at a bank that has a $1 million portfolio of auto loans, which carry a risk-weighting of 100%. You think that portfolio carries a 1% risk of loss, or $10,000.

Your bank can pay a counterparty — like a hedge fund, insurance provider or me — to take $7,000 of that credit risk for a specific period of time. Let’s say I take the other side of this bet. In order for me to take this bet, I evaluate the likelihood of the risk and use it to determine a fee you need to pay me for my troubles. And now, after the Great Recession, I have to prefund the loss, so I deposit $7,000 in a special “credit default bet” account at your bank. The bet is now on.

That, folks, is a very basic explanation of a credit risk transfer, or CRT: a transaction that transfers all or some of the credit risk tied to an asset, or portfolio of assets, from one party to another. (CRTs are also sometimes called synthetic risk transfers; I will use CRT because "synthetic risk transfers” sounds needlessly complex and financialized.) The holder of these assets is buying protection from their risks; the counterparty is selling protection from this risk.

Of course, these transactions aren’t structured as simple bets. They’re more like notes or bonds, with the bank paying investors some compensation that reflects the risk the investors have acquired, based on how the underlying asset performs. If the loans default, that loss reduces the principal amount the bank owes to investors.

CRTs acquired a deservedly bad reputation during the 2007-09 financial crisis. In recent years, big banks have used them sporadically, but not much is known about current activity these days. But we’re still going to talk about them because right now, banks have a window of opportunity to use CRTs to manage capital ratios, credit risk or both. |

Everything Old (2000s) is New Again |

If all this sounds a little familiar, you’re not having déjà vu. We have been here before! Institutions have issued CRTs in the United States since the 1990s, wrote Warren Kornfeld, SVP of North America banks and finance companies at Moody's Ratings, in a May report. One type of CRT is a credit default swap, or CDS, which infamously caused $30 billion in losses at AIG during the 2007-09 financial crisis. After that, CRT activity “came to a standstill for many years,” Warren wrote.

There had likely been a thaw in the intervening years, but there wasn’t good data. CRT transactions are not public by default; instead, a public bank would disclose them if the transaction is “material” enough to be disclosed. But Warren said there were a couple of external events that likely had made these transactions more attractive to banks, leading to an increase in interest and activity around 2022.

The first external event was that the 2022 spike in interest rates meant banks now carried sizeable unrealized losses in their securities portfolios, some of which would erode certain risk-based capital ratios. The second was that in 2023, regulators proposed a capital regime called Basel III Endgame that could increase capital ratios at big banks. Impacted institutions might be interested in finding ways to increase the capital ratio without increasing the amount of actual capital.

Capital rules assign different risk-weightings to different portfolios of assets at banks. The risk weightings assigned to different assets can sometimes exceed the actual risk of the asset, based on historical performance.

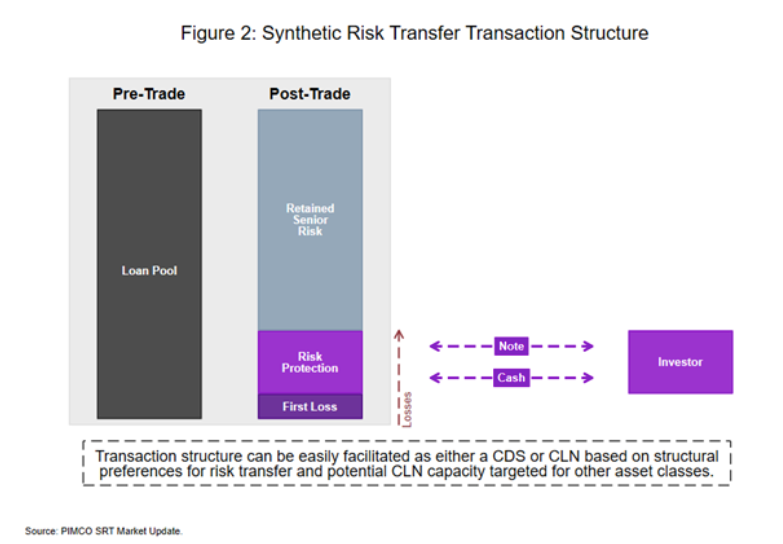

“[The] disconnect between required capital and actual risk creates an incentive for banks to either reduce their lending or find ways to better align their capital with the true risks,” wrote two researchers at the Bank Policy Institute, a big bank advocacy group, in 2024. A CRT that’s been structured correctly allows banks to reduce the risk-weighting assigned on a set of assets, say, from 100% to 30% after the CRT. Warren says this change serves to “reduce the denominator” figure in the capital ratio calculations. |

Source: BPI’s 2024 blogpost, itself citing a PIMCO market update. In the caption, CDS is a credit default swap and CLN is a credit-linked note. |

Moody’s recently surveyed 69 US banks it has rated, asking them about their issuance of these instruments, and published the results this May. Warren and his team found that only 15 of those banks, or 22%, had issued a CRT. The total outstanding CRT balances for these banks exceed $15 billion and reference more than $150 billion in assets at these institutions. Most of the CRT transactions involved high-quality assets that were performing well as of the May report. The capital benefit was about 25 basis points, which Warren said is pretty “modest.” A bank with an 11% CET1 ratio might raise that figure to 11.25% by using CRTs.

The report also found waning interest from banks as their outlook on the environment has changed. In September 2024, the Federal Reserve said it would repropose the Basel capital rules, and there will likely be different capital ratios as a result. (You can still buy these sick shirts though.)

Additionally, banks may have been able to weather the unrealized losses in their securities portfolios better by increasing their liquidity or hedging or restructuring the portfolios, removing some pressure on the risk-based capital ratios. |

While big banks seem to have used CRTs, they’re not only for big banks. There’s another reason why banks of all sizes might want to think about adding CRTs to their risk management toolbox: They help manage credit risk. Like, it’s in the name, right? Banks could use them to cover asset portfolios that have uneven credit performance, or to trim exposure to a concentration. Warren said risk and credit management concerns are likely driving most interest in CRTs right now, rather than capital treatments.

Merchants Bancorp used credit-linked notes and credit default swaps — two different types of CRTs — in 2023 and 2024, and upsized an existing CDS in June 2025. These CRTs “totaled $3.7 billion in loans to reduce risk of losses, with incremental coverage ranging from 13-14% of the unpaid principal balances for each arrangement,” the $19.1 billion bank said in its second-quarter earnings. The balance of these covered loans was $2.8 billion at the end of the quarter. The bank recorded a credit risk transfer premium expense — the fee it pays — of $4.8 million in the second quarter, which was up 23% from the quarter prior and 108% from the prior year.

The Carmel, Indiana-based bank didn’t return my request for comment (If you’re wondering who calls banks these days, the answer is me. Without a media contact at the bottom of the press releases, I had to call the bank’s “Contact Us” line, navigating the recorded messages to try to talk to an employee without having an account and asking whoever answered to be transferred to the marketing department before leaving a message. If you work at Merchants and are reading this, HMU).

Merchants Bancorp also operates a mortgage banking firm called Merchants Capital, which provides financing for multifamily housing. Merchants Capital has a capital markets platform, which has completed four CRT transactions totalling $3.5 billion in assets between 2022 and July 2025.

In October 2024, it securitized $630 million of healthcare commercial real estate bridge loans that were originated by its joint venture partner and underwritten and closed on Merchants Bank’s balance sheet. The loans supported the properties as they sought permanent financing through the U.S. Department of Housing and Urban Development. (Based on my reading of the timing of the bank’s press releases, this transaction seems to be different from the March and December 2024 CRTs that Merchants Bancorp recorded in its earnings, but I could be wrong.)

In the October transaction, Merchants Capital partnered with a “large investment manager specialized in alternative assets” that purchased the junior securities, which was 15% of the total transaction. The junior securities are the credit risk bits: “As part of its purchase, the investor retained the first loss Risk Retention certificates as a third-party purchaser.” In the release, Merchants Capital’s Capital Markets EVP Evan Gibson said these transactions have “helped to provide capital relief, reduce credit risk, and allow Merchants to continue as one of the top multifamily and healthcare bridge lenders in the country." |

CRTs operate within a golden window of opportunity — one that the industry might currently be in. CRTs require one party to sell credit risk and another party to buy it, and so interest and pricing is best in “benign” credit environments, Warren said. The cost of a CRT for a bank rises with the credit risk of the covered asset pool, and credit risk is pretty low right now. Quarterly net charge-offs for the second quarter totalled 60 basis points, according to the Federal Deposit Insurance Corp.’s quarterly banking profile.

“If we switch to a volatile and uncertain credit market, those investors are either going to not want to invest, or the rate they are going to charge is going to increase,” Warren said. He also said newly issued CRTs should work without blowing up. Remember the bet framework I explained earlier? I mentioned that in taking the other side of the bet, I would have to prefund the loss amount. That prefunding basically guarantees that the counterparty can cover the loss, should it be incurred.

“I don't think there's a question as to whether they will work,” he said. “They're all prefunded.”

One potential area of concern that Moody’s flagged is a concentration among CRT counterparties and investors. The survey found that around 40% of total CRT exposure is held by the largest investor, and the top three investors hold 80% of total exposure. These investors include specialized credit funds, such as private debt and hedge funds, which Moody’s said could raise risk in periods of market stress.

Banks should also be aware that using CRTs could send a signal. They could indicate a bank is a prudent and sophisticated credit risk manager, but Warren says a capital ratio benefit of more than 1% could indicate a “reliance” on these transactions to maintain risk-based capital ratios. He said at that point, a ratings firm like Moody’s would view CRTs as a “credit negative” and likely prefer that the bank increase equity capital, which is permanent capital that can cover credit losses.

And of course, a bank that does a CRT should know what it’s doing. I presented an absurdly simple scenario, but CRTs are complex instruments with specific scenarios that need to be outlined and priced accordingly. Warren suggested that bank executives interested in these instruments make sure they have an appropriate level of sophistication, including robust risk management and modeling capabilities. “Without strong risk-management capabilities,” Moody’s wrote, “a bank's capacity to fully understand the CRT’s implications and its risk exposure is limited.” |

|

|

What I’ve been reading, watching and listening to this week: |

🍿Grabbing my popcorn: to watch the next round of federal preemption fights. Reuters reported that large banks are lobbying the Office of the Comptroller of the Currency “for uniform U.S. regulations outlining how they can make loans, issue bonds or provide investment banking services, or assess anti-money laundering risks while curbing state powers over their operations.” State banking agencies are sure to have some thoughts about this.

|

🏃🏻♀️Inspired by: Emma Maria Mazzenga, a 95-year-old elite masters sprinter whose performance and physiology are being studied by scientists interested in how bodies change over time. Her 200-meter (half a track length) time is 54.47 seconds — what’s yours? |

😍Obsessed with: my laptop cover that looks like an old-school composition notebook. Yes, I wrote my name on it, and yes, I’m covering it with stickers. |

Warren at Moody’s wanted me to be clear that the “bet” framework at the opening of this newsletter is my characterization, not his! Thanks to Moody’s for the report and interview.

Reminder to put a press contact at the bottom of your press releases so I don’t have to call your bank’s main line and confuse someone in the call center.

And finally, what other banking trends or products are having a comeback and give you a sense of déjà vu? Until next week, thanks so much for reading! – Kiah |

|

|

Get your brand in front of 55,000+ financial services execs. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|