{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Monday, Fintech Laborers!

I hope you are putting down your shovels and pickaxes (or your laptops and noise-cancelling headphones) and taking a well-deserved break.

That’s what I’ll be doing (mostly) today, but here is a little fintech news to catch up on, whenever you have the time.

Ohh, and by the way, are you signed up? I assume you are signed up. If you’re not signed up, you should sign up. Exciting stuff is happening very soon for folks who are signed up.

- Alex |

Was this email forwarded to you? |

|

|

Engineering: driving wheels of a railway locomotive, and section of piston. Coloured lithograph, 1905, by Stanislas petit. |

|

|

#1: Firing On All Pistons |

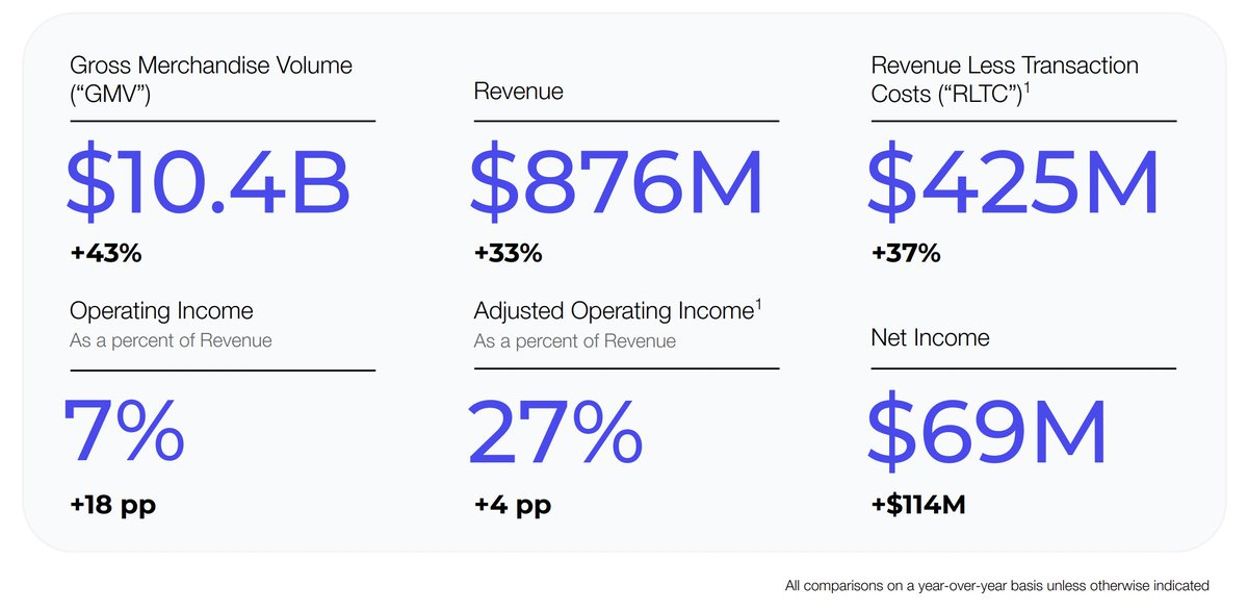

Affirm had a very good quarter:

Affirm stock popped 10% Friday after the buy now, pay later firm beat Wall Street’s expectations across the board in its fiscal fourth-quarter results.

CEO Max Levchin told CNBC on “Money Movers” Friday that the company is “firing on all pistons.” |

Profitability is the headline.

Net income of $69 million, up $114 million year-over-year. Honing in on operating income, Affirm reported its first-ever quarterly operating profit at $58 million. For the fiscal year, the company recorded a net income of $52 million, contrasting with a substantial net loss of $517 million in the prior fiscal year.

Driving this shift to profitability is growth in gross merchandise volume (GMV), which is the total value of the goods and services purchased through Affirm. GMV increased by 43% in this quarter, with a substantial portion of that growth attributed to 0% APR monthly installment loans. The use of these loans increased by 93%, with a vast majority (nearly 95%) being funded by the merchant, rather than Affirm. These loans are less profitable for Affirm (no interest revenue, obviously), but the company claims that they lead to stickier, more profitable customer relationships (featuring plenty of interest-bearing loans) over time.

And Affirm is very focused on building long-term relationships directly with consumers, as Affirm's COO, Michael Linford, explained to me on a call last week.

That consumer-direct business — most prominently represented by the Affirm Card — did quite well in Q4. Active cardholder count nearly doubled to 2.3 million. Affirm Card GMV grew 132% to $1.2 billion, and GMV derived from in-store usage of the card grew 187%.

And still, the company sees significant room for improvement. As Michael told me, “If I’m being real honest with you, today we don’t do a good job building a product that is really compelling for the everyday spend, the pay now stuff, as we call it.”

He also emphasized the importance of Affirm’s B2B2C initiative, specifically around the Affirm Card, which brings 'pay later' functionality to other banks’ debit cards (an initiative being pursued through a partnership with FIS). When I asked Michael about this initiative, he said, “It’s as exciting to me as the card was three years ago because it’s such an incredible opportunity for us to take our honest lending products and embed them in consumer debit cards everywhere.” Affirm is still in the process of finding a few initial launch partners for this B2B2C initiative, but it appears to be a strategic priority.

A few other quick notes from my conversation with Mr. Linford: -

I obviously had to ask about Affirm’s decision earlier this year to furnish repayment data for its loans to Experian and TransUnion. According to Michael, the decision was made because “We want to make sure that positive repayment for the consumers on our platform is reflected in people’s credit files.” He also went out of his way to point out that Affirm doesn’t have any incentive for customers to pay late, saying, “Our business model does not, cannot, will never be better if somebody is late. That stands in stark contrast to the credit card industry, which famously has a huge portion of their profitability sitting in late fees. It certainly stands in contrast to a lot of other players in the [BNPL] space.” This was as close as he came in our conversation to referencing Klarna and Afterpay, both of which charge late fees and have stated that they will not be furnishing data anytime soon.

-

When I asked Michael about consumers’ overall financial health and how that is showing up in Affirm’s credit performance, he said, “It’s a mistake to look at our credit results and infer consumer health. It’s also a mistake to look at consumer health away from us and assume we can’t deliver results that are good.” He explained that Affirm’s approach to underwriting is significantly different from competitors, stating, “Our product is structurally different. We underwrite every transaction, and the short duration of our asset allows us to engineer different credit outcomes than what you might see with the credit card issuers.”

- I also asked Michael about the spat between JPMorgan Chase and Plaid, and it sounds like Affirm is keeping its head down on that topic. “It doesn’t really impact us at all. It’s a trivial cost to us. Double it, triple it, 10x it. It’s kinda moot. Cash flow underwriting is a tool. It’s a tool we don’t use all that often.” OK then!

|

#2: Will Fintech Become More Expensive? |

Speaking of JPMorgan Chase and Plaid, consumers may begin to pay higher prices for their fintech apps, according to Forbes:

The big new fees JPMorgan Chase is planning to charge some financial technology companies may well trickle down to consumers, several fintech CEOs tell Forbes.

[The] fees are set to take effect very soon, since Chase told aggregators they’d start charging them in 60 days. Chase spokesperson Drew Pusateri says the bank is still in active negotiations with aggregators. But after two months of back and forth, no agreements have been announced. The fintech CEOs we spoke with who run personal finance apps and pay for Plaid’s services expect Plaid to pass on the costs of Chase’s new fees to their own businesses. Now those CEOs are considering raising prices for consumers–or eliminating free features altogether–to offset the potential blow to their balance sheets. |

Nothing has changed significantly in the U.S. open banking landscape since I last wrote about it.

JPMC introduced pricing. The fintech companies and data aggregators complained (loudly). The CFPB initiated the official process to revise the open banking rule (read my initial takeaways from the ANPR in this essay). And yet, I found many of the details in this Forbes article to be pretty interesting. Here are a few (with my color commentary attached): -

JPMC and the data aggregators are still negotiating over the bank’s proposed pricing, but have not yet reached any agreements. (I would imagine that the tenor of those negotiations changed significantly when the CFPB reversed course and asked the court to pause the BPI lawsuit. If you’re Plaid, right now, why would you give an inch in those negotiations?)

-

Plaid isn’t saying whether it will pass along any fees to its customers if new pricing does go into effect, but its fintech customers expect that it will. (IMHO, Plaid absolutely will pass on the fees to its customers if the fees do end up being implemented.)

-

The fintech companies that Forbes spoke with are split on whether they would pass along fees to their end customers. (PFM providers like Rocket Money and Monarch are the ones that will be significantly impacted by the fees, if they stick. Those are the companies that would need to make hard decisions. To other fintechs like Chime, PayPal, and Affirm, fees would be a minor inconvenience.)

-

JPMC’s proposed fees are significantly higher than what it would need to charge simply to recoup its costs. (We’ve known this was true since the news broke, but Forbes does a good job putting concrete numbers to it. As I have written before, JPMC’s pricing was intentionally designed to curb secondary data use and make pay by bank less commercially viable. It was never just about cost recovery.)

- Fintech companies might be open to paying fees if they were solely to help banks recoup their costs. (This is good because there is a real chance that capped cost-recovery fees will end up in the revised rule.)

-

Fintech companies and/or data aggregators may sue JPMC if they are unable to negotiate acceptable agreements with the bank. (I don’t think we’ll get to this point. I think there is a reasonable chance that JPMC doesn’t move forward with its fee gambit, as that would put it in a challenging position with the CFPB. My best guess is that everything goes into wait-and-see mode until the CFPB proposes a revised rule.)

|

#3: Growing a Vertical SaaS Platform |

A vertical SaaS platform focused on the home services space raised a seed round:

Sequifi, a Lehi, UT-based provider of a real-time pay and forecasting engine designed for home services companies, raised $6.7M in Seed funding.

Led by CEO Roshan Kumar, Sequifi leverages a real-time pay and forecasting engine designed for home services companies, which empowers workers with same-day payments and transparent earnings while giving business owners the systems infrastructure needed to scale and retain top talent. |

I’ve been studying the vertical SaaS space quite intently for the last couple of months (pay attention to the Fintech Takes podcast feed in September 👀), and one thing that I’ve found is that every platform, in the early days, needs a wedge that is well-suited to its chosen vertical.

In the case of Sequifi, that wedge is payroll and commission management for industries with large, decentralized teams and employees with complex pay plans (tiered commissions, overrides, role-specific incentives, etc.)

From what I can tell, Sequifi started by focusing specifically on the mortgage industry (where complex pay plans for loan officers and brokers are very common) before broadening out to focus on home services (solar, pest control, HVAC, etc.) It also appears to be positioning itself as a more generalized HR platform (including employee onboarding, training, and performance management). The question is, where does Sequifi go from here?

In vertical SaaS, you either want to broaden your functionality while keeping your vertical focus tight, or you want to broaden your vertical focus while keeping your functionality tight.

Does Sequifi attempt to transition from HR for all of these different home services business segments to more of an all-in-one operating system for one of those segments (e.g., Slice outflanking Toast specifically for pizza restaurants)?

Will it pivot to become more of an infrastructure provider (payroll and commission management for industries with complex pay plans) that partners with vertical SaaS companies for distribution (e.g., Pipe getting out of the direct lending and into lending-as-a-service)?

The next steps here will be fascinating to watch! |

|

|

What happens when borrowers want to pay, but the economy says nope (again and again)?

In TruStage’sTM new article, they unpack why 70% of consumers are sweating repayment, and why lenders need more than traditional credit scores to manage rising risk. Spoiler: Default risk isn’t just a data problem, it’s a design one.

The fix? Smarter tools — like digital lending insurance, which gives borrowers a safety net (job loss, injury, unexpected chaos) and lenders fewer charge-offs to stress about.

If you’re in digital lending and not thinking about built-in protection, you’re already behind.

But there's one way to catch up. |

1 TruStage 2025 Consumer Lending Preferences Research, March 2025 PGI-8309693.1-0825-0927 |

|

|

2 READING RECOMMENDATIONS |

Jason doesn’t editorialize much in his newsletter, but he made an exception yesterday, and I’m glad he did.

TomoCredit is an obvious scam. It’s been obvious for many years. And yet it persists, without any intervention from state or federal regulators. I have no idea how that’s possible, but it shouldn’t make anyone feel good about the government's ability to keep consumers safe over the coming years, which feels increasingly likely to be a golden age for scammers. Give this one a read. |

I’ve found the mainstream coverage of the Lisa Cook news very frustrating because, for the most part, it treats the accusations against her seriously and, by extension, vests Bill Pulte (Director of the FHFA and originator of the accusations against Cook) with a level of credibility that he does not deserve.

Adam’s analysis of the news (which he has followed up on here and here) does not fall into that trap.

|

1 PERSON WHO HELPS BRING FINTECH TAKES TO LIFE |

In lieu of our usual question to ponder today and in honor of Labor Day, I am featuring an interview with one of my colleagues. Fintech Takes is a team. Except for myself, most of our team operates (mostly) behind the scenes. They don’t get public recognition despite being absolutely essential to the insane productivity and excellence of Fintech Takes.

That needs to change. So, I will periodically publish brief interviews with my teammates, starting with Al “Sandy” Dubois. What do you do?

Al: I am the A/V producer for the podcasts Fintech Takes and The Marketing Millennials. How did you get to Workweek?

Al: I found Workweek by searching online for media companies in and around the Austin area. I'm quite happy I landed here.

Take us inside your job. What’s a small, specific, nerdy thing that you know or do in your role that our audience likely doesn’t understand?

Al: Sometimes during a recording, a guest’s phone will ring or vibrate, and the mic picks it up beneath their voice. Using a special program that displays the audio as a heat map, I can pinpoint the exact frequency of that sound and remove it without touching their words. The audience never knows it was there. (Editor’s Note — As this example illustrates, Al is a warlock. He makes me sound much less dumb and inarticulate than I actually am, and he makes all Fintech Takes podcast guests feel at home. I’m very grateful to get to work with him!) What’s one thing that you’ve done for Fintech Takes that you’re proud of?

Al: I worked closely with our production team to revamp the Fintech Takes branding. The colors, photos, and overall vibe look the way they do because I had a hand in shaping them, and I’m really proud of how it turned out.

Please give us one non-fintech content recommendation. Can be a movie, TV show, book, article, or podcast. What content are you LOVING right now?

Al: Since returning from some travels this summer, I’ve been leaning more into movies rather than television. As a Western lover, that led me to rewatch No Country for Old Men, the Coen Brothers classic. That then brought me to see Honey Don’t! — the new dark comedy from Ethan Coen — and although it’s received mixed reviews, I’d still kindly recommend it.

|

|

|

🏀 FINTECH TAKES THE COURT 🏀 |

Yep, it’s happening again!

I am DELIGHTED to officially announce the third annual “Fintech Takes The Court” 3x3 basketball tournament, which will take place in the morning on Sunday, October 26th, in Las Vegas.

This year’s tournament is being sponsored by SOLO, and it’s going to be the best one yet. If you’ll be attending Money20/20 (or just in Las Vegas that week) and are interested in getting off the Strip for a few hours and getting some exercise (or just coming to cheer the teams on!), fill out this form. Space is limited, so don’t wait 🙂

|

| |

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if profile.vars.rh_reflink_11}  | Share with Fintech Takes, get cool stuff! | Have friends who'd love Fintech Takes too? Click the link below to share with your friends and get awesome rewards when they subscribe! | |

|

PS: You have referred {{profile.vars.rh_totref_11}} people so far | | Share Fintech Takes! | |

|

{/if} |

|

|

Get your brand in front of 56,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|