{if ftt_dorm_120 == true}

Quick favor: Our records indicate that you aren’t opening this email. But records can be wrong. Please click here if you’d like to remain subscribed to Fintech Takes. |

|

|

{/if}Happy Monday, Fintech Takers!

With Money20/20 roughly two months away, it is time (believe it or not) to start the invitation and RSVP process.

I have a lot of fun stuff planned for this year’s event, which I will announce in the newsletter over the next four to six weeks. However, I want to start with the big one.

The Fintech Takes 3x3 Basketball Tournament is happening, once again!

This will be our third year in a row hosting the event, and this year’s tournament (sponsored by SOLO) will be the best one yet. If you’d like to participate, please RSVP using the link at the bottom of this email!

- Alex |

Was this email forwarded to you? |

|

|

Fasciated snake by George Shaw (1751-1813). |

|

|

#1: Fighting Over Federal Preemption |

The banking lobby, state regulators, and the crypto industry continue to argue about stablecoins. The latest bone they are wrestling over is Section 16(d) of the GENIUS Act, which allows state-chartered, uninsured depository institutions that own permitted stablecoin issuers to conduct money transmission and custody activities across state lines without obtaining separate state licenses. A group of trade associations representing banks and state regulators wrote a letter that vehemently opposed Section 16(d):

Section 16(d) allows any state-chartered uninsured depository institution with a stablecoin subsidiary to perform traditional (i.e., not solely related to payment stablecoins) money transmission and custody activities nationwide through that subsidiary, thereby bypassing host state licensing and allowing substantially less state oversight. This unprecedented overriding of state law and supervision weakens vital consumer protections, creates opportunities for regulatory arbitrage, and undermines state sovereignty.

And, of course, the Blockchain Association and Crypto Council for Innovation wrote their own letter in response, arguing for Section 16(d):

We oppose repealing Section 16(d). This provision is a necessary safeguard to protect stablecoin holders and ensure timely redemption and execution of other permitted stablecoin issuer activities. As written, Sec. 16(d) allows subsidiaries of state-chartered institutions to conduct money transmission only in support of lawful stablecoin issuer activities across state lines. This allows a stablecoin issuer to redeem stablecoins for fiat with a holder in another state without first having to seek a license. Without it, states could effectively veto the stablecoin redemption rights of out-of-state holders, recreating the same fragmented, balkanized regulatory regime that stifles interstate commerce and denies Americans equal access to financial products based solely on geography. Reinstating state veto authority would undermine that principle and invite a patchwork of 50 conflicting regimes to dictate the future of U.S. payments.

|

This is one of those situations where there aren’t any good guys. Everyone is just trying to preserve or upend the status quo in a way that most benefits their interests. Let’s review.

Community banks fear the competitive threat posed by stablecoins. State banking regulators despise federal preemption because it eliminates the need for institutions to obtain licenses (and pay fees) in each state. So they jointly argue that Section 16(D) will allow uninsured depository institutions with stablecoin subsidiaries (e.g., institutions with national trust bank charters or state-level narrow bank charters like Wyoming’s Special Purpose Depository Institution charter) to run roughshod over the entire U.S. without adequate supervision or consumer protections in place (ignoring the fact that the GENIUS Act will ensure that the reserves backing all regulated payment stablecoins are fully-backed by highly stable and liquid assets like T-Bills).

Crypto companies want to take advantage of every possible shortcut to compete with banks and fintech companies, so their lobbyists argue that it’s patently absurd to require a stablecoin issuer to obtain money transmission and custody licenses in all 50 states (ignoring the fact that thousands of non-bank fintech companies do exactly that without bitching about it and ignoring the fact that section 16(d) is unnecessarily broad in its scope and ignoring the fact that even though GENIUS-regulated stablecoins are fully backed by stable and liquid assets, the GENIUS Act has some glaring flaws when it comes to insolvency and bankruptcy).

See what I mean? No good guys here. Also, interestingly, the Bank Policy Institute, which represents the largest banks in the U.S., did not join in the lobbying against Section 16(d). Why not?

Perhaps because the big banks are busy arguing for their own expanded federal preemption from state laws:

U.S. banks are petitioning the Office of the Comptroller of the Currency to seek national standards for providing banking services that would override state-imposed rules

Large banks, in particular, are lobbying for uniform U.S. regulations outlining how they can make loans, issue bonds or provide investment banking services, or assess anti-money laundering risks while curbing state powers over their operations |

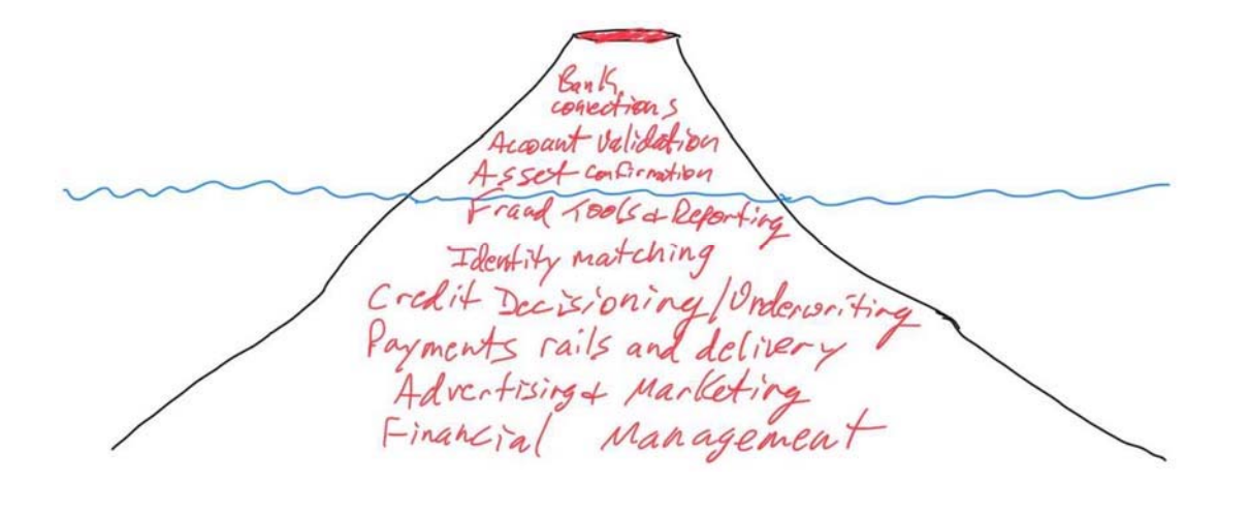

#2: Visa Walks Away From The Volcano |

Visa is shuttering its open banking business in the U.S.

Visa Inc. shut its open-banking business in the US amid regulatory uncertainty about consumer-data rights and the prospect of higher fees for customer information, according to people familiar with the matter.

In response to a request for comment about the move, a spokesperson for Visa said the company is focusing its open-banking strategy “in high-potential markets like Europe and Latin America.” On an earnings call in July, Visa Chief Executive Officer Ryan McInerney said those markets have the “greatest potential” for open banking.

Visa’s decision was made independently of JPMorgan’s change in strategy, one of the people familiar with the matter said. |

After attempting to acquire Plaid for $5 billion in 2020, settling for Tink in 2022, building a respectable open banking business in Europe (working with companies like Adyen and Revolut), and expanding to the U.S. last year, Visa is now retreating.

How embarrassing. And the stated reason is bullshit. You don’t pull out of a market as lucrative as the U.S. because of a little regulatory uncertainty. Visa lives, perpetually, with regulatory uncertainty. Visa thrives on regulatory uncertainty. It knows that the CFPB will not allow the banks to kill open banking (and pay by bank, specifically) in the U.S. Visa is walking away from the opportunity that inspired this infamous graphic: |

Because JPMorgan Chase — likely Visa’s single largest customer — is mad. |

#3: The Ouroboros of Credit Building |

Kikoff announced a new feature:

Kikoff … today announces the launch of AI Credit Disputes, a proprietary feature that helps users identify and correct errors on their credit reports today.

The tool simplifies a traditionally confusing and costly process by using AI to generate personalized, FCRA-compliant dispute letters tailored to each user’s specific situation. Instead of relying on generic templates, users can now use personalized language that reflects their reason for the dispute, to increase chances of approval and making the process more effective and approachable. |

Kikoff should send Tomo a fruit basket.

By being so blatantly bad at scamming consumers who are desperate to improve their credit scores, Tomo has taken a lot of the heat off of other, less obviously bad credit-building services. Despite my obsession with credit builder products (which was doctor has told me I need to stop analyzing in order to preserve my physical and mental health), I haven’t spent much time looking at Kikoff. Well, that ends today (sorry, Doc!) Kikoff is … not great. The primary offering is a credit-building service (the Kikoff Tradeline), which, if I understand it correctly, is a credit line designed to be used exclusively to finance itself. I know. Confusing. Allow me to explain using an example. The basic plan costs $5 per month. For that $5, you get a $750 credit line. That credit line is only used to finance the monthly $5 fee, which is then repaid to Kikoff via a linked debit card (which Kikoff strongly encourages you to set on auto-pay).

This model has two benefits. First, it’s inexpensive and low risk, which makes it highly likely that consumers will make on-time payments. Secondly, it helps lower consumers’ overall credit utilization ratio by providing a credit line that they can access only a fraction of ($745 of the $750 line is never used). It’s the ouroboros of credit building; the revolving credit line that eats its own tail.

It should go without saying, but the data furnished to the credit bureaus by this Kikoff Tradeline is garbage. The purpose of using credit utilization ratio as a proxy for creditworthiness is that it helps lenders assess a consumer’s discipline and restraint. Do you have access to credit that you don’t need or that you choose not to use? By eliminating the ability for customers to use the Kikoff Tradeline for anything other than paying their monthly Kikoff subscription, Kikoff has rendered this measurement of responsibility meaningless.

The company’s remaining features and premium offerings are similarly problematic: -

Rent reporting only works with Equifax, and Kikoff doesn’t furnish missed rent payments.

- Bill payment reporting only works with TransUnion, and Kikoff doesn’t furnish late payments.

-

The credit bureaus’ dispute processes are not great, by any means, and I’m not here to defend them … but I’m not sure that inundating the bureaus with unverified, AI-generated dispute letters is the way to fix it.

Even canceling your Kikoff subscription comes with this warning:

If you’ve already made a payment to Kikoff, closing your account could negatively affect the average account age of your overall credit profile. Keeping your account open and continuing to make your monthly plan payments helps you continue to build credit over time.

Very cool. And not manipulative at all. And then there are the customer reviews.

On the surface, they appear to be somewhere between okay (3.7 stars out of 5 on the Better Business Bureau) and reasonably good (4.6 stars out of 5 on Trustpilot). However, if you look at the most recent reviews, you see a lot of unhappiness. Here are some quotes:

STAY AWAY!!!!! Waste of time If you’re trying to build credit, look for safer, more reliable options.

The 5 star ratings are fake. These people are preying on poor people with low credit and it's disgusting. I really hope they get shut down and sued!!

In support of that last comment, Trustpilot (where Kikoff has more than 2,000 reviews, including an awful lot of 5-star reviews) has added this disclosure to Kikoff’s page: |

|

|

2 READING RECOMMENDATIONS |

This is a rather wild story about the capabilities and (self-imposed?) limitations of AI chatbots and large language models.

I appreciate Kiah Haslett (author of the upcoming Fintech Takes Banking newsletter) for bringing this to my attention.

|

No one is better suited to write this piece on the future of content and community in the age of AI than Ben Thompson. |

There are a TON of interesting questions being asked in the Fintech Takes Network. I’ll share one question, sourced from the Network, each week. However, if you’d like to join the conversation, please apply to join the Fintech Takes Network.

How do we create accountability around the use of LLMs in financial services? Is it as simple as keeping a human in the loop? Do we need new liability frameworks? How important is explainability to accountability?

If you have any thoughts on this question, reply to this email or DM me in the Fintech Takes Network! |

|

|

🏀 FINTECH TAKES THE COURT 🏀 |

Yep, it’s happening again!

I am DELIGHTED to officially announce the third annual “Fintech Takes The Court” 3x3 basketball tournament, which will take place in the morning on Sunday, October 26th, in Las Vegas.

This year’s tournament is being sponsored by SOLO, and it’s going to be the best one yet. If you’ll be attending Money20/20 (or just in Las Vegas that week) and are interested in getting off the Strip for a few hours and getting some exercise (or just coming to cheer the teams on!), fill out this form. Space is limited, so don’t wait 🙂

|

|

|

Thanks for the read! Let me know what you thought by replying back to this email.

— Alex |

|

|

{if profile.vars.rh_reflink_11}  | Share with Fintech Takes, get cool stuff! | Have friends who'd love Fintech Takes too? Click the link below to share with your friends and get awesome rewards when they subscribe! | |

|

PS: You have referred {{profile.vars.rh_totref_11}} people so far | | Share Fintech Takes! | |

|

{/if} |

|

|

Get your brand in front of 55,000+ fintech and banking executives. |

Workweek Media Inc.

1023 Springdale Road, STE 9E

Austin, TX 78721

Want to ruin my day? Unsubscribe. |

|

|

|

_2.png)