Key Takeaways

I took a look at forward revenue (topline growth) and forward EBITDA (profitability metric) to see how the various healthcare services sectors were performing in 2023. I’m comparing company multiples on 1/1/2023 to multiples as of 9/28/23. All data was sourced from Koyfin, which licenses data from S&P Capital IQ. Recently acquired firms were excluded from the ongoing analysis

Main thoughts:

- Median EBITDA Multiples dropped in all sectors but dialysis and value-based senior clinics. If you include Cano Health’s precipitous dropoff, dialysis was the only sector that stood its ground.

- The most notable activity is happening in ‘advanced’ primary care. While there were numerous public players a year ago in this space, today there are just 2. And as we’re speaking, Cano Health is selling itself off for parts, leaving just CareMax as the lone senior value-based senior clinic player here in short order.

- For growing emerging players like enablement platforms, EV/Rev and EV/EBITDA are likely not the best metrics. Still, they are readily available, so I included them for the sake of comparability to the rest of healthcare. That being said, Agilon is a huge outlier on forward EBITDA expectations. Given the relative success of enablement firms in the public markets (Privia, Agilon, ApolloMed, Evolent), it is interesting to note that Agilon is the only player to see this level of multiple expansion. Or maybe the multiple forward estimates are jacked up. If anyone has any commentary as to the rationale, I’m all ears.

- Talkspace is quietly mounting a comeback.

- We’ve seen a number of services deals in the public markets lately, including buyouts of Amedisys, LHC Group, One Medical, Oak Street Health, Signify Health and most recently, parts of Cano Health. Of course, don’t forget about VillageMD-Summit, CareMax-Steward, and the significant amount of fundraising taking place throughout value-based care and enablement.

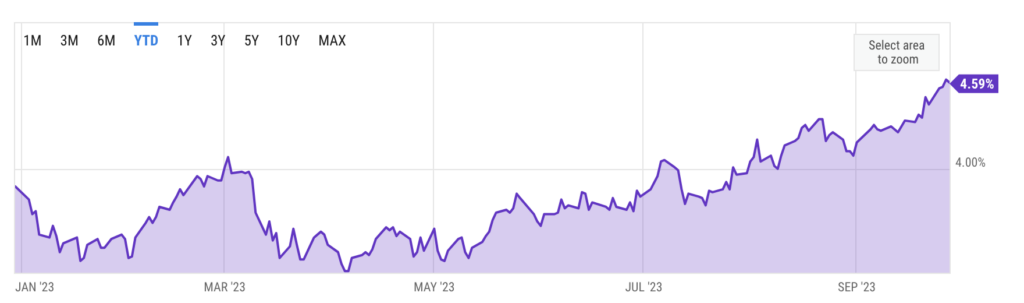

In my mind, the dropoff in forward multiples for traditional, steady healthcare services players are much more likely to be a function of macro economic activity rather than company-specific performance. Take, for instance, interest rates rising this year:

Where are there winners in the public markets, and who’s expected to see multiple expansion? Look no further than Parth’s commentary from July on this newsletter:

A handful of companies have seen meaningful multiple expansion over the last 6 months, irrespective of their fundamental profitability. Their relatively strong performance over the first half of this year appears to be correlated to commercial potential and market momentum around artificial intelligence, payment innovation / value-based care enablement and an improving care utilization outlook.

The final category of outperformance has been amongst a group of inpatient and outpatient care providers (ie, Surgery Partners, US Physical Therapy, Tenet, HCA). Combing through earnings reports suggests this is likely a function of improved operating margins, particularly driven by patients scheduling more elective procedures in outpatient settings post-pandemic.

While it appears that stabilizing labor expense growth and increasing inpatient volumes are easing overall margin pressures, its important to note that revenue growth from outpatient care is far outpacing revenue growth from inpatient care. Combined with rate adjustments, denials and redeterminations, it is still not clear whether the current outperformance is either universal, or durable.

Parth’s commentary still holds true a few months later.

SPONSORED BY WEAVER

The business of healthcare is complex, and things are constantly changing.

Luckily, Weaver’s articles and industry trends make unpacking the economics of health care a lot more manageable.

Weaver’s healthcare professionals are industry-specific experts and always on top of market transitions, providing timely analyses such as the impact of transaction volume declines on valuation and retrospectives like the 2022 Year in Review.

Dive into Health Care Valuation Trends

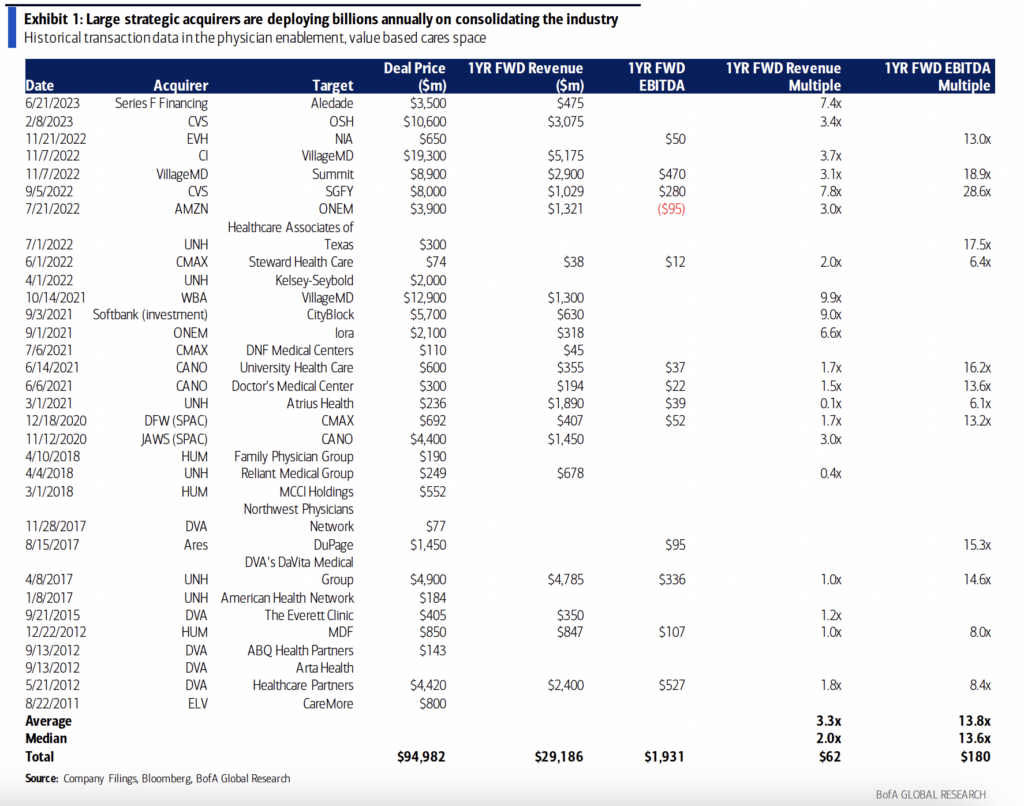

Finally, as I’ve touched on, the most notable activity in general is in advanced primary care. Bank of America updated the recent transactions in a great note after the Walmart-ChenMed rumors.

Billions of billions of dollars are exchanging hands in this space, and valuations are driven by downstream synergies and associated profitability with owning advanced primary care assets (supplemental MA benefits, pharmacy, PBM market share, MLR gamesmanship, etc). Expect to see continued activity in this arena:

Source: BofA Global Research: ‘Another Day, Another Billion-Dollar Primary Care Deal’

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

Healthcare 2023 Forward EBITDA and Revenue Multiples by Sector:

Acute Care Hospitals:

Ambulatory Services:

Enablement:

VBC Senior Clinics:

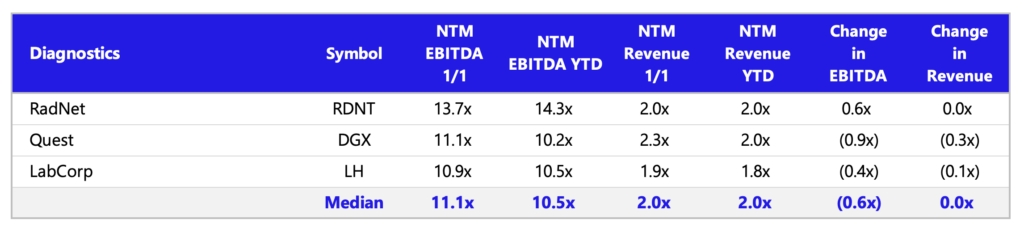

Diagnostics:

Dialysis:

Behavioral Health:

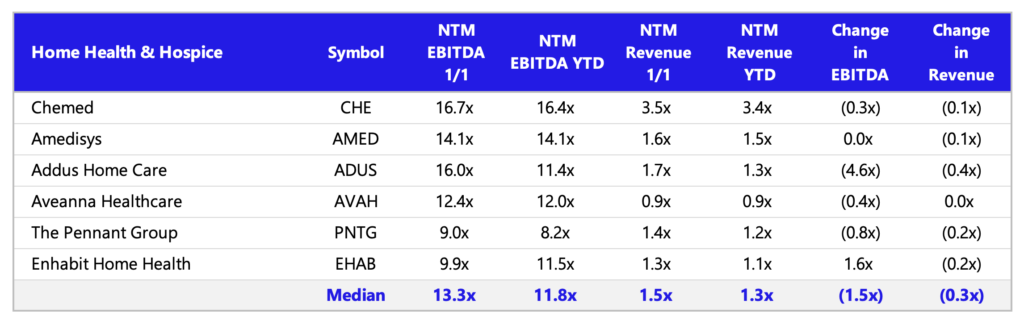

Home Health & Hospice:

Post-Acute Care:

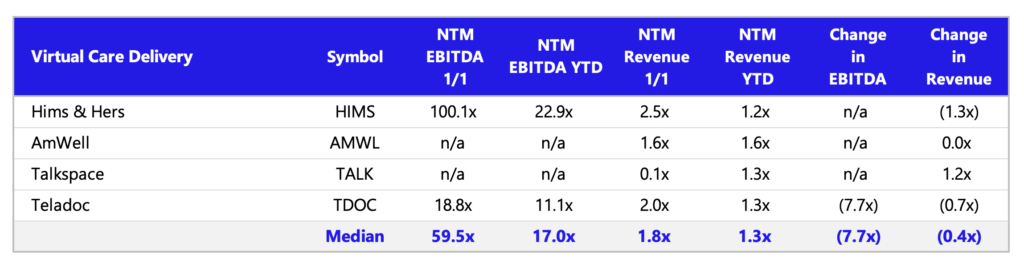

Virtual Care Delivery:

If you enjoyed this, consider subscribing to Hospitalogy, my newsletter breaking down the finance, strategy, innovation, and M&A of healthcare. Join 20,000+ healthcare executives and professionals from leading organizations who read Hospitalogy! (Subscribe Here)