22 June 2023 | Climate Tech

Fair-weather insurers

By

Here’s the headline: This month, State Farm and Allstate announced they will no longer write new home insurance policies in California. They both did this relatively quietly, without citing climate change directly. Farmers Insurance also announced it will stop writing new policies in Florida.

Two weeks ago, New York City was enveloped in smoke from Canadian wildfires. Many words have been penned on the smoke. I won’t pen too many more. But I will borrow a few.

While the smoke definitely brought climate change to the fore as a conversation topic, it’s exceedingly difficult to accurately pin any single weather event, wildfire, or natural disaster on climate change. The Canadian wildfires could have happened even if global mean temperatures hadn’t risen 1.2°C over the past hundred-plus years. As Robinson Meyer wrote in Heatmap:

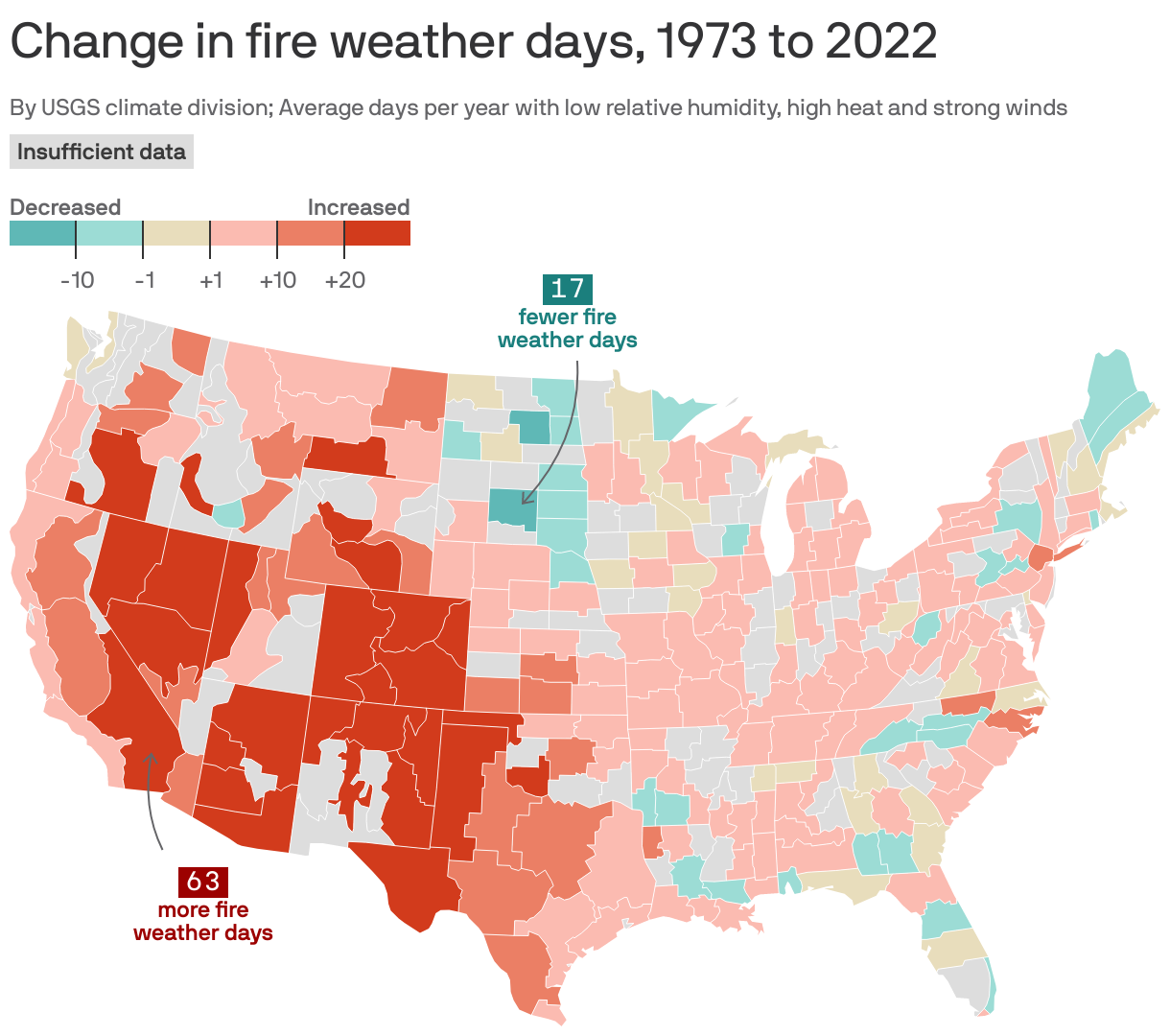

There’s no doubt, to be clear, that climate change will make wildfires worse across North America: The Intergovernmental Panel on Climate Change says that hot, dry ‘fire weather’ will increase throughout the 21st century. But, again, Quebec is not in drought. As for today, no climate-change signal has appeared in eastern Canadian wildfire data. Their connection to climate change is far less clear cut than it is in, say, California’s blazes.

There’s no question that climate change makes temperatures hotter on average, wildfires more fierce, and droughts more prolonged.

Perhaps more important is that it makes the entirety of the Earth’s climate and weather systems less predictable. Look no further than this winter in California, where it rained far more than anywhere on the East Coast (and far more than it had in decades).

Fair-weather insurers

Unpredictability is an albatross for many industries. For the insurance industry, the unexpected means business. Their business is insuring you against the unexpected.

But the unexpected becomes a problem for insurance companies when it turns into the unpredictable, when it turns into something that can’t be modeled sufficiently well anymore, or when things are changing so rapidly that forward forecasting becomes foolhardy.

State Farm and Allstate both made their exits from California rather quietly. You could have missed it in the regular barrage of the news cycle.

Still, wildfire risk likely has a lot to do with State Farm and Allstate’s decisions. The fire season in California has intensified significantly over the past fifty years. Average areas burned by wildfires in California over the past fifty years have quintupled (some of that may have to do with fire management practices and other factors.)

It isn’t just insurance companies that are forced to respond to growing wildfire risks (and costs). Utilities are increasingly trying to recoup costs by passing them through to customers, which would set a precedent for much more of the same when future wildfires inevitably burn.

Nor is this newsletter all about wildfire risk. Last week, Farmers Insurance also announced it will stop writing new policies in Florida. That’s a hurricane story, and perhaps a rising sea-level one.

Some climate change naysayers often argue that hurricanes haven’t gotten measurably worse over the past decades. While there’s plenty of data to dispute this from NOAA and NASA, in the future, I’ll ask them why they think Farmers abandoned its Floridian business instead.

While less directly related to insurers bowing out of real estate markets, extreme heat is another major factor that will weigh on home prices in the future. Texas is feeling the heat this week. What happens to a real estate market when the heat is unbearable three months out of the year?

I’m not just talking about whether you or someone you love likes living in Austin, Houston, or the DFW area. What happens if it’s too hot to work outside for even a dozen days of the year? That wreaks havoc on construction and countless other critical economic industries.

Climate tech to the rescue?

The thing is, this trend has been snowballing for some time. As noted by Mark Friedlander, a spokesperson for the Insurance Information Institute:

Over the past 18 months in Florida, we’ve had 15 companies decide to stop writing new business…

Similarly, concerns over pricing and availability of homeowner insurance are already ripe in other markets, like the Gulf Coast, which has witnessed a multi-decadal intensification of hurricanes.

Still, the fact that three major insurers have backed out of the country’s first and third most populous states in a matter of weeks is stark. These are insurance companies whose ads you’re used to getting bombarded by on TV.

Other major insurers still ‘in the room’ must be deciphering the writing on the wall. What happens if more rush towards the exits? What happens when you, as a prospective home buyer, can’t get insurance? Does the government step in as the insurer of the last resort? Do we all move to Minnesota? I don’t know.

Plenty of climate tech companies and institutes are stepping up to help. Most focus on providing would-be insurers with better data and modeling or prediction tools.

- Tomorrow.io, based out of Boston and Tel Aviv, Israel, raised $87M in Series E funding to collect better weather information, monitor weather systems, and mitigate risk (via satellites).

- Companies like Reask are developing AI tooling to better assess the risks posed by specific events (in their case, tropical cyclones). Reask raised a $6.55M seed round that it announced last week.

- NOAA and the National Science Foundation recently launched two new research centers explicitly to help insurance companies better understand climate risk.

The list goes on. Other established players like Floodbase are working to offer deeper data and better modeling to mitigate flood risk. Their goal is to enable parametric flood insurance coverage, which focuses coverage on more binary factors, insuring policyholders based on the occurrence of a specific event rather than the extent of damage. I spoke with the CTO of Floodbase, Subit Chakrabarti, a while back in a wide-reaching convo you can find here.

These are important (and likely) lucrative niches for climate tech companies to fill in coming years. But are they enough to convince insurers to continue to offer policies in environments with increasingly unpredictable and significant climate risk? Can ‘insure-tech’ innovation, or entirely new types of insurance, like parametric insurance to help women in India recover lost wages due to extreme heat, keep up with climate change? Again, I don’t know.

My hunch is that even significant innovation and progress in climate data management, parametric insurance, modeling, and other related areas will be a helpful palliative rather than a comprehensive solution. To be sure, some of these climate tech companies will make lots of money. But home insurance will get extremely complicated (or simply sparse) in many markets.

The net-net

All of this goes beyond climate’s impact on real estate, insurance, and new tech companies.

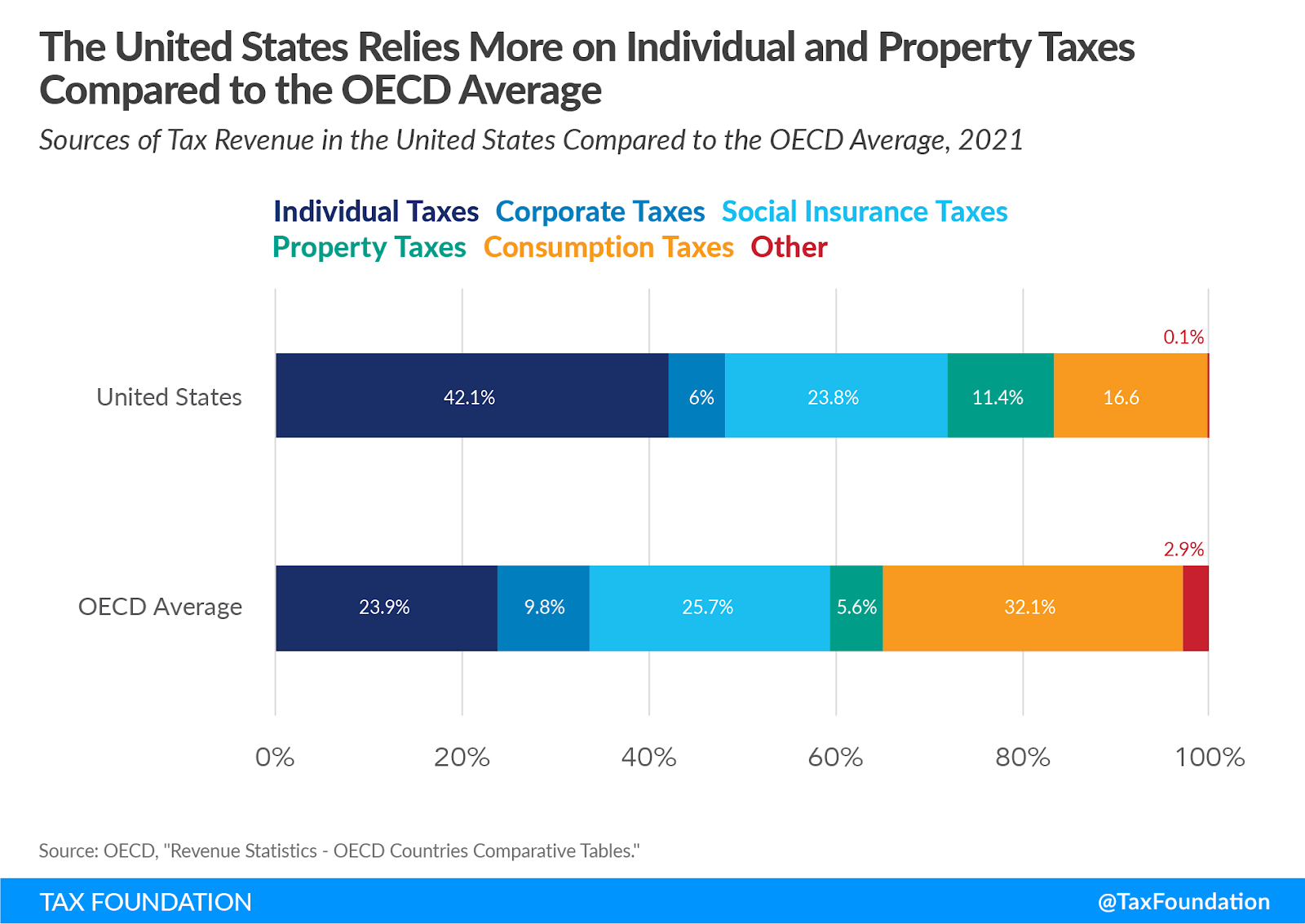

The real estate market has been the most reliable wealth-creation mechanism for the American middle class. It is vital to our national self-image and the American economy that home prices are stable (and, ideally, continue to appreciate). “Home wealth,” as it were, represents about half of all national household wealth. What happens when some of the states with the most valuable homes and the most wealth tied up in real estate become uninsurable? Even by the most basic measure (property taxes), the U.S. relies twice as heavily on household-wealth-driven tax income than other OECD countries:

Biden has yet to pull one big lever in the climate fight. It’s one that many of the most engaged environmental activists wanted him to pull years ago. The name of the game is declaring a national climate change emergency.

Beyond sending a strong signal, doing so would open avenues of executive action and federal funding that outstrip even the IRA. The Biden Admin could, for instance, use the Defense Production Act to accelerate clean energy tech manufacturing if it declared a climate change emergency.

Here’s my hot take for a hot week. I doubt wildfires that inevitably rip through California again or other public health concerns from wildfire smoke will convince America to treat climate change like a serious national security threat. I doubt a drought in the Southwest will do the convincing. I doubt another hurricane on the Gulf Coast does the trick. I doubt even weeks or months of extreme heat waves that kill many people would do it.

But home prices? That could.