29 August 2022 | Investments

Klarna (Private) vs. Affirm (Public)

By

Happy Monday!

Over the weekend, we had a goodbye party for one of my good friends in Boston.

One issue.

We forgot to invite her to her own party! Thankfully, we tracked her down not too long after the party began, but man was that a wild situation.

Showtime!

Want to get these in your inbox to never miss an edition? Subscribe to The Crossover today!

Klarna vs. Affirm

Introduction

Today we have a FinTech focused crossover comparing two BNPL companies Klarna (Private) & Affirm (Public).

Special shoutout to my Workweek teammate Alex Johnson of FinTech Takes for the assistance prepping for this edition!

Klarna

There is no venture backed entity that has better reflected the vicissitudes of the venture environment over the past couple of years than Klarna. BTW – I did not know that vicissitudes was part of my vocabulary either.

Checkout Klarna’s funding rounds from January 2020 to July 2022:

Klarna’s valuation skyrocketed from $5.4B to over $45B in just a year and a half.

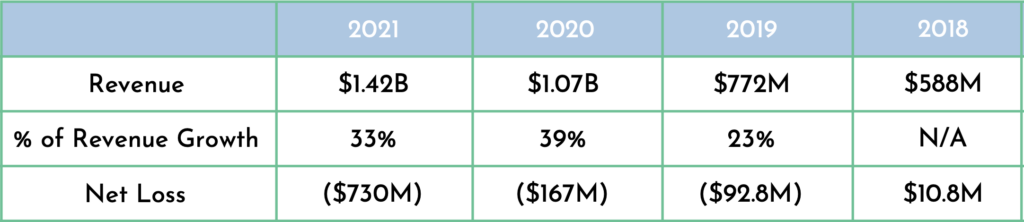

Interestingly, if you were to look at Klarna’s financials, there were no big developments that warranted such a sharp increase in valuation:

There was obviously rock solid growth for Klarna, however, nothing out of the ordinary that merited more than an 8x growth in valuation in such a small window of time.

That is why, it was no surprise to anyone when the valuations of high flying stocks and ventures started coming down, Klarna’s valuation did too.

Fast forward to July 12 and Klarna raised an $800M round @ a $6.7B valuation – a breathtaking 85% drop in valuation in the private markets.

Affirm

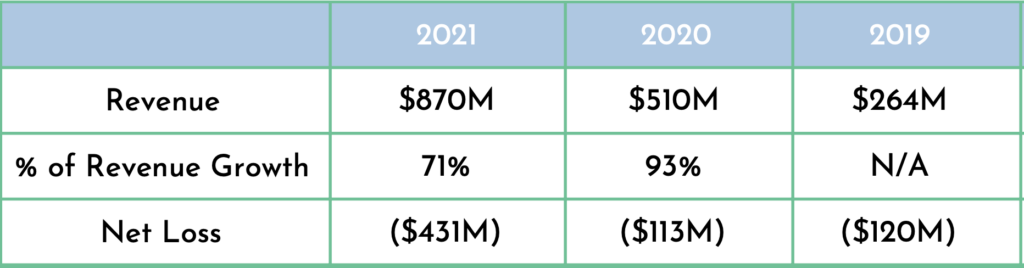

Now let’s take a closer look at Affirm & their financials:

As you can see, Klarna’s revenues are almost 2x the size of Klarna’s but growing @ half the speed.

What would you think Affirm valuation should be after seeing this chart and knowing Klarna financial from above?

Before I share the answer, check out these two numbers too:

Affirm: 7.1M active consumers & $8.3B

Klarna: 147M active customers & $80B in GMV

You would have to think that Klarna’s massive consumer base & GMV would require some sort of premium right? Well, not according to Mr. Market.

As of mid August, Affirm was valued @ around $10B, 66% more than Klarna. At the surface level, you would think that Affirm valuation should be closer to Klarna, but there are some key differences to why the public markets are arguing differently.

Alan’s Angle

There are two key differences between Affirm & Klarna that account for this discrepancy:

- Makeup of customers

- Partnerships

First, regarding the makeup of customers, socioeconomic status really matters. The fact that Klarna only makes $1.2B on nearly 150M global customers shows not only that their clients are more low/middle income, but also that the BNPL product they sell is more challenging to monetize.

Specifically, Klarna’s BNPL product requires 25% upfront and 25% payments for two weeks (for the next 6 weeks) until the payment is paid off. They are all short term loans with no interest.

Affirm comes from a very different angle as they are focused on more of an affluent clientele and offer a variety of different BNPL packages.

Additionally, many of Affirm’s BNPL loan structures charge interest, hence, the significantly greater monetization of GMV – even from a base that is a 10th of the size.

Finally, it is important to point out that Klarna is much more vulnerable to a global recession/significant economic downturn due to the financial circumstances of many of their customers.

The second difference is in partnerships.

There is no BNPL company with the sheer size of partnerships that Klarna has throughout the world with over 400K retailers including Lululemon, Converse, Bed Bath and Beyond, Macy’s and (obviously) many more.

However, what really allows Affirm to stand apart in my eyes is their ability to create exclusive deals with some of the biggest partners in the world and customize offerings for them.

By biggest partners, I mean the two biggest partners: Amazon & Shopify.

In November of ‘21, Amazon announced that they were expanding their partnership with Affirm to be the exclusive BNPL provider for the e-commerce giant.

Interestingly, this deal expires in Jan ‘23 so will be something to watch, but the fact that Amazon made Affirm their exclusive partner for years is quite the endorsement.

In May, Shopify announced that they would be extending their current exclusive BNPL partnership with Affirm in a multi-year-deal.

Affirm also is the integrated partner with Target & Walmart.

All together, Affirm’s partners handle more than 60% of ecommerce sales in the US.

Getting deals done with the greatest gatekeepers in commerce are deals that generational companies get done.

Wrapping It Up

Over the past couple of years, the rise & fall of Klarna has been a closely followed one for VCs. However, for us crossover investors, we get the extra angle of analyzing how Klarna’s valuation compares to Affirm’s.

As of now, it appears that the financial markets are valuing Affirm’s partnerships & ability to monetize their customer base ahead of Klarna’s more “taylor to the masses” approach.

Additionally, the fact that Klarna’s customer base is likely at higher risk to default on BNPL payments in a recessionary environment is a key differentiating factor.

I personally agree with this view of the BNPL space.

At the same time, if Affirm is unable to continue to grow into these deals or lose Amazon as a partner, and recessionary fears are overdone, maybe just maybe Klarna will come roaring back!

-Alan

Note: Affirm announced earnings on August 25th below Wall St. expectations sending the stock down 20% to a ~$7B valuation. I still believe Affirm deserves a premium to Klarna & might even warrant a look in The Crossover Portfolio!

The Crossover Portfolio

In The News: A Name Change for Callaway

The Rundown: Portfolio Pick Callaway Golf announced that they are changing their name to “TopGolf Callaway Brands Corp and ticker symbol to $MODG (Modern Golf)

3 Key Points:

- Callaway Golf owns a plethora of strong and growing brands including TopGolf, TravisMatthew, Jack Wolfskin, Ogio, and others

- In the past quarter alone, 60% of sales were from outside of golf equipment. TopGolf alone made up 36% of revenue!

- The corporate name change is expected to take place on Sep 6th and ticker symbol change on Sep 7th

Alan’s Angle:

I really like this move by Callaway. TopGolf is a rocket ship from both a business and a consumer perspective, and it is great that Callaway will be so strongly affiliated with TopGolf.

Also, this is the third portfolio pick that has seen their name change this past year:

- ViacomCBS – Paramount Global

- Penn National Gaming – Penn Entertainment

- Callaway Golf – TopGolf Callaway Brands

We here @ The Crossover feel that all of these companies have under appreciated assets and these name changes show us that the company’s believe this too!

Golden Nuggets

- The Savannah Bananas do it again!

- With so much of my recent focus being on the newsletter, I haven’t been able to prep for fantasy football as I normally do. So happy to have Josh Larky’s rankings!

- The Atlanta Braves’ mascot needs to chill out a little

- The first episode of House of the Dragon was incredible. HBO does it again.

Meme of the Day

Thanks for the read! Let me know what you thought by replying back to this email. See you in your inbox every Monday and Thursday.

— Alan

Disclaimer: This analysis is for educational and entertainment purposes solely and is not professional investment advice. The author of this piece and/or members of Workweek media could be invested in companies discussed.