20 June 2022 | Investments

Invitae: Who They Left Behind

By

Hey everyone!

Congratulations to Matthew Fitzpatrick on winning the US Open!

One of the best storylines from Matt’s win was that his caddy Billy Foster finally won his first major after 40 years in the business, carrying bags for some of the best golfers along the way.

Showtime! (Or I guess meme time!)

Billy’s reaction was amazing and inspired a meme that I feel is so good that I had to kick off the newsletter with it.

Want to get these in your inbox to never miss an edition? Subscribe to The Crossover today!

Meme of the Day

Invitae: A VC Play in the Private Markets?

Introduction

“Invitae is a venture capital play in the public markets.”

-Steven D. Soclof, CEO of Matrix Equities (my Dad)

If you asked me what stock I have learned the most from in my years as an investor, I would say Invitae.

I initially invested in the company @ ~$10/share in 2015. I was compelled by the company’s vision to bring comprehensive genetic information into mainstream medicine to improve healthcare for billions of people.

You do not have to be a rocket scientist to know that genetic information was the future of medicine, and Invitae’s early success both scientifically and commercially had me intrigued.

In November 2013, Invitae launched its first commercial offering, an assay of 216 genes covering 85 genetic disorders. The company’s original efforts were focused on hereditary cancers including breast, colon, and pancreatic cancers, charging $1,500 per test.

In the first 9 months of 2014 (data provided in S-1), the company had $729K in revenue and 1,189 tests completed. Fast forward to 2021 and the company had generated over $460.4M in revenue and completed over 1.1M billable tests. Remarkable.

In many ways, Invitae has successfully set themselves on the path to becoming “The Amazon of Genomics.” However, in the process, they left one thing behind: their shareholders.

Invitae

“For years I have detested the growth-at-all-costs business models followed by emerging growth companies. They work – until one day (or quarterly update) they don’t. All it takes is one disappointing revenue growth rate or downward revision in guidance for Wall Street analysts to issue sharply lower price targets. The little guy is usually the one that ends up getting hurt. That means you, dear reader.”

-Maxx Chatsko, The Street

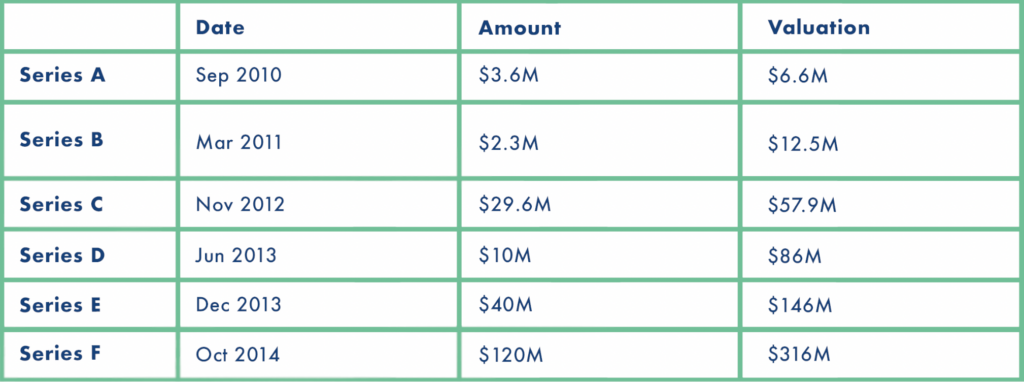

Invitae was founded in 2010 by an accomplished biotech/genomics executive named Dr. Randy Scott. The company’s vision and early scientific success enabled them to raise 6 rounds in the private markets, raising over $200M.

Invitae successfully IPO’d in February 2015 at a $492M post-money valuation. The company raised $101.6M and started trading @ $16/share.

In order to become the one-stop shop for genomics Invitae needed to:

- Drive down the cost of genetic testing

- Create infrastructure and a platform that could support millions of genetic tests a year

- Expand menu of tests to cover incredibly wide amount of healthcare sectors

All while not compromising the science, but actually driving it forward. This was an incredibly expensive task filled with acquisitions, breathtaking cash burn, and issuance of additional stock.

According to Pitchbook, since their IPO, Invitae has done 16 acquisitions totaling over $3B. These acquisitions have varied across every component of what Invitae is looking to build.

Here are just 3 examples of acquisitions the company did to build out their platform.

- Medical: ArcherDX (liquid biopsy)

- Platform: Citizen (help patients organize and share medical documents digitally)

- Data: One Codex (bioinformatics)

In order to fuel these acquisitions/growth, Invitae has seen serious cash burn over the past several years:

- 2015: -$80M

- 2016: -$100M

- 2017: -$123M

- 2018: -$129M

- 2019: -$242M

- 2020: -$602M

- 2021: -$379M

The company lost more money than they did revenue, in 7 out of the 8 past years totaling over $1.6B.

In order to support all of these acquisitions and cash burn, Invitae’s issuance of additional stock was off the charts.

As of April 2022, the company had 229M shares outstanding.

How many did the company have at IPO? Just 30M shares outstanding. Yup. More than 7x increase in shares outstanding in just 7 years.

As an investor, it is very hard to make money when there is that much dilution occurring.

For a while, Invitae’s growth-at-all-costs business plan was working. Interest rates were low and stock issuances were being gobbled up. However, as inflation kicked in and fears of a recession began, Wall Street started valuing profitability—which Invitae is not known for, to say the least—sending the stock down 80% since the beginning of the year, down to ~$2.50.

Nasty.

Existential Crisis

Another reason why the stock is this low is likely due to the fact that from a liquidity perspective, the company is facing an existential crisis.

The company has $885M in cash remaining with a projected cash burn of $600-$650M for FY22. The company is aggressively looking to reduce this cash burn and a burn of $650M would already represent a ~$200M burn decrease year over year.

The company announced that they are confident in their ability to increase their runway to the end of 2023, however, this is still not something to be too proud of. Additionally, the low stock price makes it nearly impossible to issue additional stock, making this rate of cash burn a going concern.

It is important to note that the company also has a $400M shelf offering that could be used as a last resort. In my eyes, this likely could be keeping the stock down in the short run as well because, as investors know, if the stock were to return to the teens— or even the high single digits—the redemption of this shelf is a high possibility.

Regardless, with significant cash burn in a tough fundraising environment, there is a real possibility that Invitae has an existential threat on their hands.

Public or Private

As usual, my dad is right.

This is a venture capital play and venture capital is meant for the private markets not public. The public markets should be a place where investors can expect profitability, fiduciary responsibility, and a return of capital within a handful of years.

It appears that responsible capital allocation was never in the cards for Invitae.

At the same time, it’s important to recognize how close Invitae was to pulling this off. If the macro environment would have held stable, investment returns likely would have been there — just taking longer than investors would have liked.

At the end of the day, the macro environment was anything but stable, and that is the risk of a venture capital play on the public markets and the growth at all costs model that Maxx’s quote refers too.

There is serious precedent for a company like Invitae to have remained a private entity: Illumina and Grail.

Illumina, a $35B company that is one of the largest manufacturers for genetic machinery systems on the market, spun off a company called Grail in January of 2016 into the private markets.

The vision for Grail was to create a cutting-edge liquid biopsy platform that screened for cancer from a simple blood test by leveraging genetic data. The company raised a $100M Series A backed by Illumina, Arch Partners, and others.

Grail raised over $2B in the private markets to fuel this growth before being acquired by the company that originally spun them off, Illumina, for ~$8B.

This significant price was achieved even with Grail earning just $12M in 2021 revenue and $391M in annual losses. Yup, you read that right. Genomics, for now, is expensive.

Without getting too into the weeds, it is my understanding that what Grail has built is just a fraction of what Invitae’s platform is able to do. But one of these companies was acquired for $8B and the other is sitting at a few hundred million in the public markets.

There is something to be said about having a strong group of investors in the private markets and doing the dirty work in private; in many ways, that is why venture capital exists.

Additionally, there are serious benefits to not being a publicly traded company, including needing to deal with market scrutiny and hitting quarterly benchmarks set by the street — which can be a serious distraction.

In hindsight, which is always 20/20, it would have just made sense for Invitae to have stayed a private company.

Next Piece

This piece on Invitae was a little spicy. I think you would be a little spicy too if a company you have invested in and believed in was down ~70% after several years.

However, at these current price levels, I am actually incredibly intrigued by Invitae’s long term prospects.

In part two of this breakdown, dropping over the next few weeks, I will share why I am optimistic on Invitae’s future, why the stock at these levels is just too cheap, and the hidden gem in Invitae that not enough people are talking about!

In The News

Klarna’s Valuation Collapse

TL;DR: The FinTech giant Klarna is looking to raise new venture funds @ a $15B valuation, significantly down from the $46B valuation last year.

3 Key Points:

- Just last month, company was looking to raise $1B @ a ~$30B valuation

- Klarna’s Q1 losses quadrupled year over year reaching around $250M

- Last month the company also announced they would be cutting 10% of workforce

Key Quote:

“Klarna, Affirm and other buy-now-pay-later providers face increasing competition. Apple Inc. said this month it would launch a buy-now-pay-later offering in the U.S. later this year. Barclays PLC and PayPal Holdings Inc. have also launched their own services. The industry is also facing greater regulatory scrutiny. Last year, the U.K. government said it would start regulating buy-now-pay-later products to protect consumers.”

The BNPL space is becoming more & more competitive. Based off of increased competition & Klarna’s serious losses, I still think a $15B valuation is generous. I look forward to breaking this down further in the coming weeks.

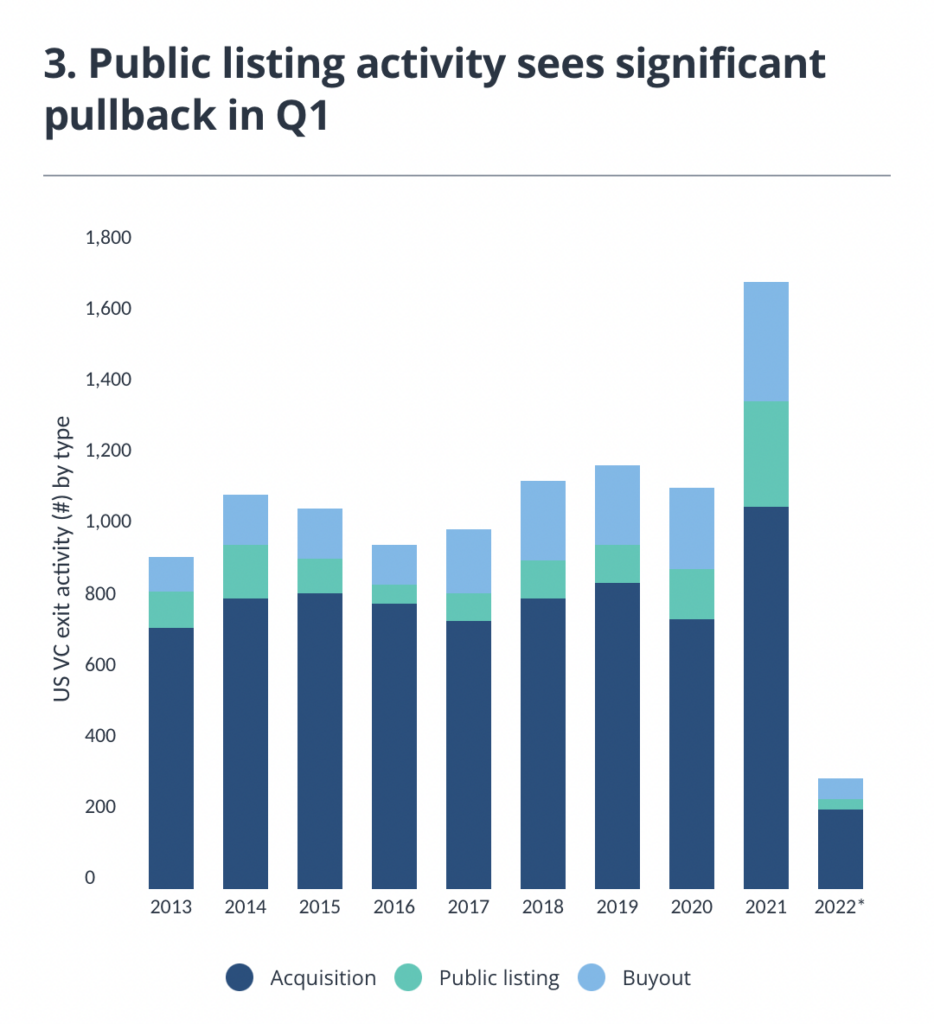

A Quiet Quarter

- In Q1 ’22 there were only 224 acquisitions, 28 public listings, and 58 buyouts representing a significant decrease from Q1 ’21 where there were 1,074 acquisitions, 296 public listings, and 339 buyouts.

- The significant decrease is likely due to the uncertainty surrounding inflation & interest rates as well as the collapse/lack of consensus surrounding valuations

Golden Nuggets

- I can’t get over this video of Deuce Tatum, Jayson Tatum’s son, celebrating his dad’s performance during The NBA Finals.

- Interesting little story here that Elon Musk is being sued for his connection with Dogecoin

- Okay. This looks sweet. I cannot wait until traffic is a thing of the past

- Robinhood has raised $7.5B in equity funding but its current market cap is $6.1B. Wow.

- I really enjoyed Bill Simmons’ appearance on Peter Kafka’s pod

Thanks for the read! Let me know what you thought by replying back to this email. See you in your inbox every Monday and Thursday.

— Alan

Disclaimer: This analysis is for educational and entertainment purposes solely and is not professional investment advice. The author of this piece and/or members of Workweek media could be invested in companies discussed.