Welcome to Hospitalogy, a newsletter breaking down healthcare finance, M&A, and strategy twice weekly. Join 23,700+ executives and investors from leading healthcare organizations including HCA, Optum, and Tenet, nonprofit health systems including Providence, Ascension, and Atrium, as well as leading digital health firms like Privia, Oak Street Health, and Aledade by subscribing here!

Welcome back to the annual Hospitalogy Soothsayer Special! Parth Desai and I have been brainstorming over the past several weeks on where healthcare is headed in the new year.

Based on discussions with industry folks, market signals buried in earnings and disclosures, and our often misguided internal dialogues, here are some of our predictions for healthcare in 2024.

Have questions or want to get in touch with Parth? E-mail [email protected]. Have any of your own predictions or thoughts for the piece? Shoot ‘em over to me at [email protected].

1) Hospitals Mine for Gold Outside of Their Core Business

The pandemic exacerbated the financial pressures that hospitals were already facing. While the drivers of these pressures are abating, the macro and existential threats providers face to their core business are not. To remain financially viable, hospitals need to quickly diversify their margin creation streams.

The obvious and traditional diversification playbook has included expansion into specialty pharmacy / 340B, ambulatory and outpatient services, clinical R&D commercialization, spin-outs / joint ventures of clinical or digital assets and even venture investing. However, in 2024, we expect providers to get even more creative, announcing bolder bets into non-traditional services that redefine what the system of the future looks like and maybe even helps them recover lost ground.

There are already some interesting early indicators out there on the types of bets providers could start making. Investing into dental care is interesting, given the medical-oral health connection, the fact that dental care sites often function as primary care access (and patient acquisition) points and the needed opportunity to enable value-based dental care delivery. Maybe more hospitals could also profitably expand into grocery and retail services. Makes sense given that the setting can function as a primary care access point and given the whole health implications of dietary decisions.

Some providers may also look to monetizing best-in-class clinical and non-clinical core competencies through global advisory and consulting services, or owning educational institutions that support workforce development. We’d be remiss not to call out the monumental clinical data and derivative product monetization opportunities that present a very compelling future financial opportunity for hospitals.

2) The Infusion Services Market Reaps the Bounty of a Specialty Therapy Boom

The FDA is expected to approve 51 specialty drugs by the end of this year, which would break the previous record of 40 approvals in 2021. It’s a continuation of a shifting trend in therapeutic pipelines and approvals from small molecules to more complex and higher-cost therapeutics (ie, cell and gene therapies, biosimilars) for targeted populations (ie, rare diseases). In fact, of the over 19,500 drugs in active development, nearly half are biologic products, whose method of administration is primarily infusion or injection (with some exceptions).

The curative promise of some of these therapies means that access to them is critical, especially for patients who have exhausted other clinical alternatives. That said, not only are many of these therapies complex to administer, but they come with a high price tag. And there is considerable debate around how the healthcare system will pay for the therapies, given differences in how different stakeholders assess their long-term clinical and financial value. CMS seems likely to begin covering some of the highest-cost therapies, like cell and gene therapies, through outcomes-based payment modalities where payment is tied to clinical progress over a longer period of time. And as is often the case, CMS policies are a bellwether for the industry.

No matter the form these contracts take, tracking and collecting clinical outcomes will require an infrastructure overhaul that supports a multitude of recurring care touchpoints, ongoing monitoring and real world data collection. With all that complexity, a very logical place for this infrastructure to coalesce around is the infusion site where treatment is delivered, patients are monitored, and a specialist can quarterback care.

In 2024, therefore, we expect to see more creative energy focused on innovating the infusion therapy services experience.

3) Dollars Dry Up for the AI Application Layer… But Stream into the AI Data Layer

2023 was the year of AI hype. As we predicted last year, AI funding activity surged as healthcare enterprises made new bets to attempt to tap into the productivity potential of this technology. Interestingly, funding levels cooled in the back half of the year as pragmatism was ushered in via an increased focus on governance and safety but also an appreciation for the limitations of the current state of technology.

A key limitation in broad scale adoption of these models is data quality, a contingency in effective model development. And despite generating 30% of the world’s data, usability is a significant challenge across the care delivery and payment universe. Addressing healthcare’s data quality challenge is multifaceted and complicated, but a foundational step in solving it is to modernize the data and infrastructure stack (particularly Infrastructure, Analytics, Data Science / MLOps). And for many reasons, we expect the healthcare industry to shift its focus to tackling this challenge in 2024.

A few policy tailwinds emerged in 2023 that we believe will catalyze this shift in 2024. The first is the launch of TEFCA and the operationalization of the first QHINs in 2024, which over time should improve the availability and volume of high quality training data. Just last week, the federal government also mandated a push to ensure AI algorithm transparency, which will undoubtedly require model developers and their customers to ensure training data and outputs are more traceable, accurate and equitable. Lastly, as additional phases of the price transparency rule go into effect next year, penalties for non-compliance will also get steeper, requiring providers and payers to invest in the machine-readability of their data.

As all of these tailwinds converge, in 2024 we expect more of the dollars that were focused on the application layer to flow into innovation that modernizes the data technology stack

Join the thousands of healthcare professionals who read Hospitalogy

Subscribe to get expert analysis on healthcare M&A, strategy, finance, and markets.

No spam. Unsubscribe any time.

4) The VBC Toolkit Finally Arrives on Specialty Care’s Doorsteps

Value-based care strategies featured prominently in managed care earnings calls this year. Echoes of “value-based care is the centerpiece of our future growth strategy” rang loudly through numerous recent earnings calls. And that makes sense, as MCOs, emboldened by continued promising performance, are clearly signaling an accelerated push to increase the breadth and depth of risk-based arrangements in the years ahead.

While the industry has been focused on empowering primary care providers to take on risk, high-cost specialty care is the next frontier as it makes up more than 60% of total medical spend (and growing), despite wide variation in cost and quality relative to primary care. Some risk-bearing primary care groups estimate that the quality of their specialist referral networks can drive a 40% + swing in cost savings.

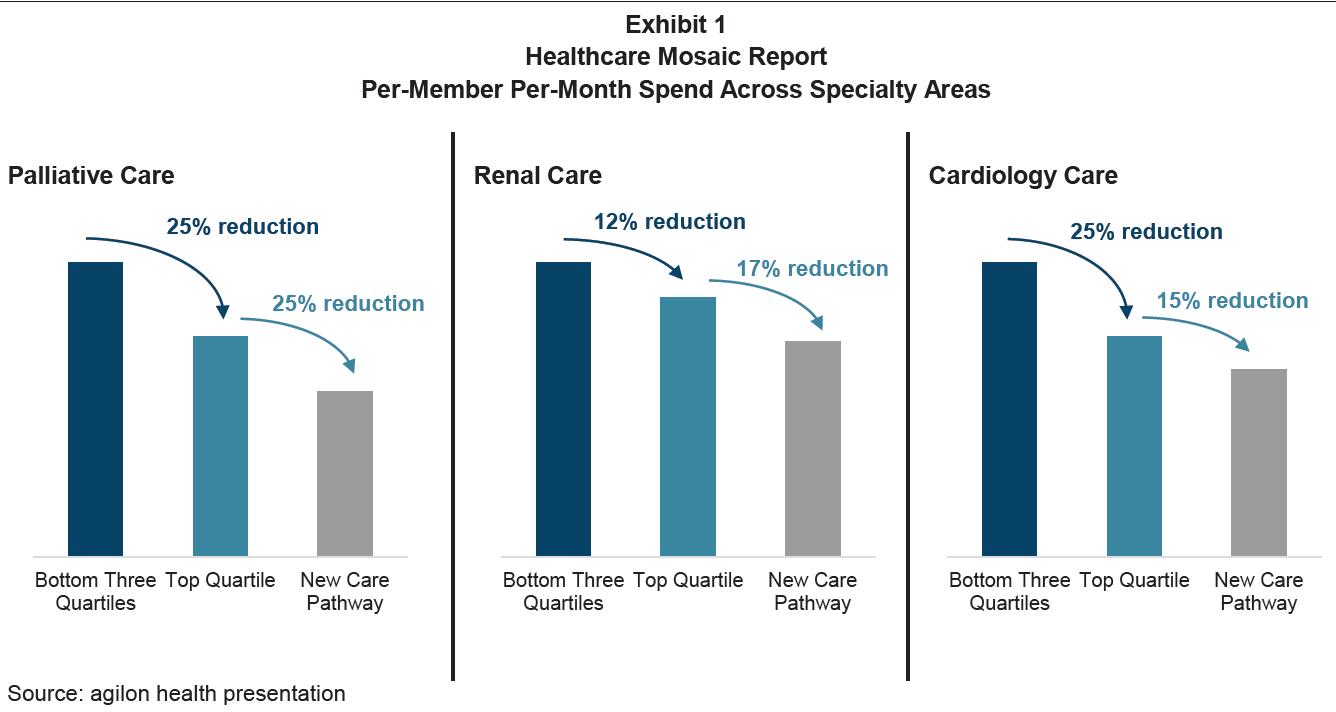

“In aggregate, agilon noted that within just three specialties: end-of-life (palliative) care, renal care, and cardiology care, it believes it can drive more than $300 million in savings—again simply by moving patients to the best referrals and care pathways.” Image Source: Advanced Specialty Care: The Next Wave of Growth in Value- Based Care – William Blair

A major problem is that the vast majority of primary care groups are unable to leverage the data they need to differentiate value amongst specialists, let alone differentiate value at the procedure level, which is critical to structuring bundles. And it’s no surprise that specialists are also hesitant to take on risk, without knowing whether they’re equipped to profitably manage a specific case.

One clear need that we expect will attract more investment next year is in the infrastructure and tooling to help risk-bearing primary care groups and specialists better collaborate in structuring high-performing specialty networks and, in particular, start off with bundles and case agreements.

5) Labor Turmoil Creates Permanent Side Effects

Care delivery organizations will continue to face labor challenges. Younger nurses are leaving the healthcare profession at a much higher rate compared to more experienced nurses, leading to a strained and understaffed workforce. This situation also puts pressure on hospitals, impacting their capacity and financial margins.

Health systems can’t even hire foreign nurses for support. Bloomberg estimates that there’s a backlog of 10,000 nurses trying to enter and work in the country but can’t due to visa issues, processing backlogged visas from 2+ years ago…

Beyond increased outpatient optionality for nursing & physician staff, there’s even competition for admin (IT, accounting) and entry-level positions (Amazon, McDonald’s, Walmart).

Through all the noise and challenges, nurses and physicians remain bastions of healthcare:

Already, we’ve seen health systems like Kaiser shell out for clinical talent, and the feeling / rhetoric from clinicians is that they’re being exploited for profits over patients while the C-suite makes bank. These resentments aren’t going away anytime soon, and the mistrust is an evergreen issue between admin and clinicians.

Unhappy with compensation, deteriorating care quality, and administrative burden, clinicians will want increased leverage against The Man. We’d expect to see this dynamic culminate in different ways, including talent leaving employment for external staffing platforms along with strikes & unionization even among physicians.

Expect winning healthcare organizations in the new labor normal to invest in supply pipelines of clinical talent through new partnerships with community-based organizations, colleges, and universities. They’ll also focus on internal retention programs, career advancement opportunities, mental health support, wellness, and improved internal communication in an attempt to ensure that physician and nurse voices are heard.

Thanks to Board Room’s Geoffrey Roche – Director of Workforce Development at Siemens Healthineers for his contribution on this prediction!

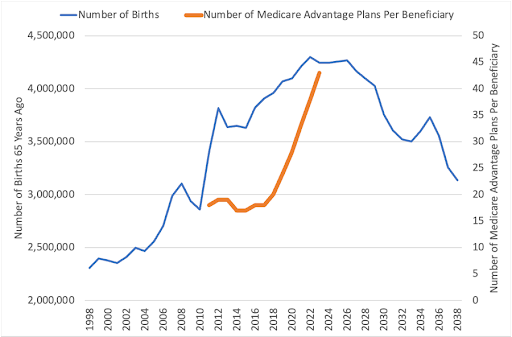

6) The Medicare Advantage Manna Dries Up

We’ve reached the growth apex in Medicare Advantage, and upcoming headwinds will result in an end to the ‘Manna from Heaven’ phase of the privatized entitlement program.

These headwinds include some of the following:

- The Baby Boomer demographic growth bump has reached its peak, meaning customer acquisition costs will rise as new seniors entering Medicare eligibility age shrinks. Insurers will have to convince Traditional Medicare participants to switch – a rarity.

Image credit: Mario Schlosser

- As the U.S. contends with Medicare insolvency, softening rate increases will impact insurers’ bottom lines

- Upcoming risk scoring changes will cause headaches for many

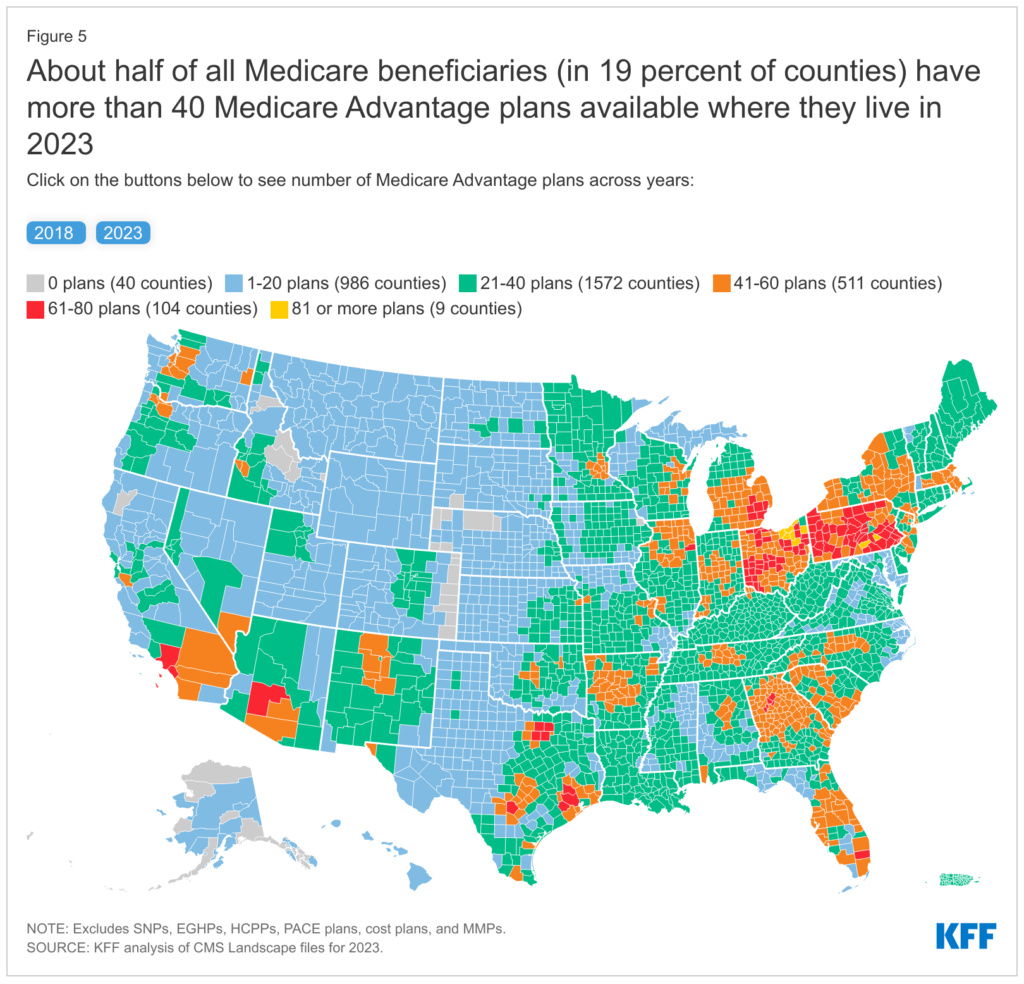

- There are an abundance of Medicare Advantage plans available – the average beneficiary could choose from 43 plans and 9+ firms in 2023. This dynamic seems unsustainable as the above factors play out, and would expect some consolidation from this point.

- Finally, take the recently canceled Humana <> Cigna merger as a market signal that Humana might want to diversify away from pure-play MA despite investing significant resources into the program over the past decade.

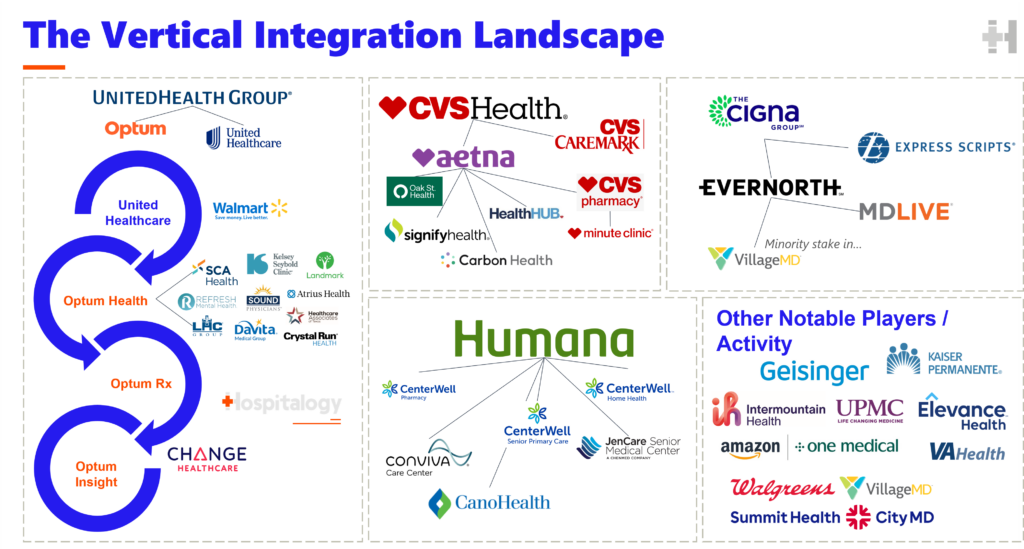

Now obviously these trends will play out over a decade-plus. But the prediction here is that looking back in hindsight, MA growth for insurers as a whole will have peaked in 2024. And the downstream ramifications of that growth peak (coinciding with a sustained rise in utilization from an aging population) include more intense narrow network formation, hospitals pulling out of many MA plan networks, and continued pursuit by payors of owning care delivery assets (vertical integration).

In recent weeks, we’ve seen Cigna announce, along with an $11.3B share buyback, Evernorth bolt-on acquisitions, CVS is touting its recently acquired PBM market preservation strategy integrated care delivery model lowering CAC, and of course, the 800-pound UnitedHealth Group / Optum leading the way, with over 130k combined physicians & APPs.

7) Provider M&A Gets a lot Harder; Digital Health Consolidates

The FTC has made it clear: they’re NOT a fan of megamergers. Just ask Adobe and Figma, which shut down its $20B merger today based on a beleaguered antitrust review.

Healthcare will receive more scrutiny than ever before in 2024. We’ve already seen a not-so-subtle attempt at taking down private equity, and proposed guidelines at the federal and state level will require more disclosure and have to clear more hurdles. Not to mention mergers – especially involving large corporations or in-market consolidation – are nigh on impossible.

For instance, HCA failed to acquire 5 same-market Utah hospitals in 2022 while this year, the hospital giant is getting sued for its Mission Health takeover debacle. Most recently, Tenet had its deal with John Muir called off. The hospital M&A environment is skin-tight, and we should expect that dynamic to continue while more creative structures (Risant health, cross-market megamergers) should proliferate.

The consensus on digital health is an expected wave of consolidation. Point solutions or startups with promising products but inability to raise additional funds will fold into larger organizations, or engage in mergers of equals (like the Commure-Athelas deal). This isn’t a bad thing. CIOs are inundated with point solutions, and having a broader suite of solutions for needed use cases should drive more successful commercialization given the enhanced focus on profitability.

Finally, from a private equity perspective, the high interest rate environment will continue in 2024 – which will affect debt-saddled players with liquidity issues, but that same dynamic will benefit those with freshly raised capital. Assuming interest rates get cut as forecasted, we may see banks ease up on loan pressure and lending requirements, leading to an uptick in provider deals in the back half of the year.

8) Political Healthcare Rhetoric Spikes after Texas Supreme Court Ruling on mifepristone

Since 2020, we’ve seen a stay-the-course approach to federal healthcare policy from Democrats, building on years of healthcare talking points like expanded subsidies for the ACA and passage of the Inflation Reduction Act to enact drug price controls on major spend categories.

Couple that dynamic with the fact that Republicans have been…silent on healthcare (apart from yelling about the politically popular ACA) and we’re shaping up for an election year where healthcare takes a back seat to the economy, foreign policy, and other more “pressing” matters.

Until the abortion case dropped, that is.

This post isn’t meant to be a political commentary, but generally speaking abortion is an electric, unifying topic among Democrats. To that end, we should expect to see major rallying cries to codify Roe especially among younger generations with voter turnout.

While much of healthcare needs help, we’d expect most other healthcare issues like…pending Medicare insolvency, PBM reform, price transparency, and everything in between to take a back seat to this topic.

If Biden wins re-election, expect the following:

- Continuing to build on ACA – Medicaid redetermination & enrollment, subsidies for ACA plans expiring in 2025

- Attempting to crack down on market power, M&A

In the event of a Republican win, expect:

- A lot of smoke around anti-ACA rhetoric – ‘Repeal and Replace’ (with who knows what)

- Support for Medicaid block grants

- A push for more healthcare programs at state rather than federal level

In general, a divided government is good for the healthcare status quo, as put succinctly by Centene during its investor day:

- “…important to take away is the high probability of divided government. And therefore, the idea that if there is reform, it’s probably incremental around the edges as opposed to systemic. And so our view actually is that the growth that the marketplace is seeing is far and away the best moat. By the time we get to 2025, we could be talking about somewhere north of around 20 million members that you’d be taking coverage away for that — from, that’s not a great thing to do regardless of what side of the aisle you sit on.”

Conclusion

We are excited to see where healthcare grows after a challenging 2023. Our take is that growing pains will turn into innovative new digital health solutions, higher satisfaction among clinicians, and ultimately better patient care – driven by the healthcare delivery models of 2024 and beyond.

Resources

Other predictions pieces worth reading:

- Sachin Jain’s predictions https://www.forbes.com/sites/sachinjain/2023/11/28/top-10-healthcare-industry-predictions-for-2024/

- Dr. Raihan Faroqui’s predictions https://www.linkedin.com/pulse/my-healthtech-2024-predictions-raihan-faroqui-md-ojjbf%3FtrackingId=SiR1tnEkRAW9lErD6RN25g%253D%253D/

- Nikhil Krishnan’s predictions https://www.outofpocket.health/p/2024-healthcare-predictions-out-of-pocket-style

- Dr. Benjamin Schwartz’s predictions https://dembones.substack.com/p/looking-toward-2024

- Where AI will impact healthcare in 2024 – Mobihealthnews https://www.mobihealthnews.com/news/where-ai-will-impact-healthcare-2024

- Venturing in Senior Care: Observations and Predictions for 2024 and Beyond – by Daniel Kaplan https://medium.com/@daniel.kaplan19/venturing-in-senior-care-predictions-and-observations-for-2024-and-beyond-a34ea0764cc7

- Anti-predictions from Seth Joseph https://www.forbes.com/sites/sethjoseph/2023/12/14/overhyped-digital-health-executive-anti-predictions-for-healthcare-in-2024/?sh=72929a29522f

- Spotlight on Consumer-Directed Technologies: 7wireVentures 2024 Digital Health Predictions https://www.7wireventures.com/perspectives/spotlight-on-consumer-directed-technologies-7wireventures-2024-digital-health-predictions/

Bonus: Way-too-specific predictions

- Mark Cuban Cost Plus Drugs takes over the entire drug industrial complex and we fix healthcare completely

- Walmart tries to acquire Humana (again) and/or makes a material acquisition in Medicare Advantage

- Amazon divests Iora Health

- GLP-1s reach a frenzied state as manic, cash hungry influencers advertise shady direct-to-GLP-1 telehealth firms. Ozempic-as-a-platform leads to rampant fraud, waste, and abuse

- Walgreens gets desperate; deepens its ties with Cigna or another large payor – e.g., Walgreens spins off VillageMD into a public entity or sells a larger portion to Evernorth / private equity sometime in late 2024 to raise cash

- Facebook enters healthcare & AI-driven solutions in some real material capacity

- Blues respond to mounting competition from payors, health systems by attempting to consolidate

- 2-3 high profile digital health firms that raised in peak ZIRP 2021 will fail

- 2-3 profitable and/or cash flow positive health tech firms go public in summer 2024

- Best-performing healthcare stock in 2024: Oscar Health (cashflow buoyed by interest income while leaned up; ACA exchange growth thesis plays out) honorable mention: Talkspace

- Google acquires some healthcare software solutions to bolster its enterprise healthcare cloud offering

- Affordability of healthcare issues causes more self insured employers to pursue narrow networks, direct care deals

- Large health systems rebound financially in 2024 amid a rise in utilization