In 1995, Jim Barksdale was pitching Netscape to a room full of investment bankers.

The company was in the final stages of going public, and Barksdale, Netscape’s CEO, was wrapping up an exhausting multi-country roadshow, trying to drum up investor interest in his company’s web browser. The last question he was asked, just before leaving the meeting to run to the airport, was, “How do you know that Microsoft isn’t just going to bundle a browser into their product?”

Barksdale’s off-the-cuff answer became the quote that he is now best known for:

“Gentlemen, there’s only two ways I know of to make money: bundling and unbundling.”

Nearly 30 years later, this statement is widely seen as being axiomatically true. However, like any axiom, the truth behind this one is often oversimplified. I think when people read, “The only ways to make money are bundling and unbundling,” what they hear is, “Bundling and unbundling are equally good ways to make money.”

This is wrong. Understandable, but wrong.

So, for today’s newsletter, I thought it would be fun to dig a bit deeper into the concepts of bundling and unbundling and seek to answer the following question – in a time of disruption, like the one that we’ve been enjoying in financial services for the last few decades, how should market incumbents respond to the threat of unbundling?

But first, let’s agree on some definitions.

Bundling and Unbundling

I define bundling as the development, packaging, and pricing of a product (or set of products) in order to optimize profit-to-value for a specific segment of customers within a static distribution environment.

That’s a bit of a mouthful, so let’s break it down.

First, the basics – a bundle is a combination of products or a single product designed to appeal to a specific set of customers. Multi-product bundles are what most people picture when they think of a bundle. A Happy Meal at McDonald’s, with the burger, fries, drink, and toy, is a good example. But the concept of bundling can be applied at the individual product level as well. Think of health insurance. The bundle isn’t the product. It’s the carefully-calibrated pool of healthy and not-so-healthy customers who use the product.

Now the second part – optimize profit-to-value. A common belief about bundles is that they are a ripoff for customers. Why, the conventional thinking goes, should a customer have to pay for 300 TV channels when all they really want to watch is HGTV?

There’s actually a very good reason for them to do so, as Shishir Mehrotra (a former executive at YouTube) explains:

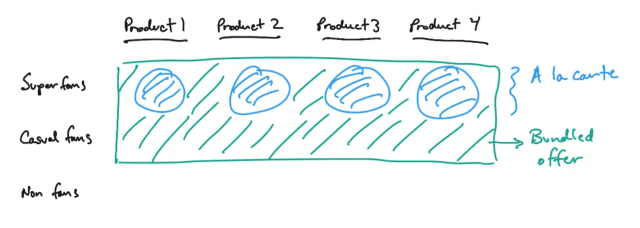

Imagine there are four products each delivered as a monthly subscription. We have a choice to deliver them each a-la-carte, or to produce a bundle across all of them. Now let’s divide the population for each good into 3 parts. Imagine that for each good, each prospective customer is one of these 3:

SuperFan: This is someone who fits two criteria:

They would pay the a-la-carte price for the channel. This means that they are fairly far along the price elasticity curve for the good (perhaps to the inelastic point)

They have the activation energy to seek out the good and purchase it.

CasualFan: Someone who would value the good if they had access to it, but lack one of the two SuperFan criteria ー either they aren’t willing to pay the a-la-carte price for the good, or don’t have the activation energy to seek it out, or both.

NonFan: Someone who will ascribe zero (or perhaps negative) value to having access to the good.

Here’s a quick visual:

Join Fintech Takes, Your One-Stop-Shop for Navigating the Fintech Universe.

Over 36,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

If we offered these goods a-la-carte, then:

The providers would only provide service (and collect revenue) from their SuperFans (the blue highlights), and

Consumers would only have access to goods for which they are a SuperFan

The a-la-carte model clearly doesn’t maximize value, as consumers are getting access to fewer goods than they might be interested in, and providers are only addressing part of their potential market.

On the other hand, the bundled offer expands the universe and not only matches SuperFans with the products they are SuperFans of, but also allows for those consumers to get access to products of which they may be CasualFans. From a providers perspective, it gives access to consumers much beyond their natural SuperFan base. This is the heart of how bundles create value ー it’s not about addressing the SuperFan, it’s about allowing the CasualFan to participate.

In other words, bundles make all the other channels that our HGTV SuperFan casually enjoys – your History channel and Disney channel and CNN – cheaper and more easily accessible for them than they otherwise would be.

Bundles, when done well, optimize profit-to-value for providers and their customers.

And now the third part – within a static distribution environment. As Marc Andreessen (Jim Barksdale’s old Netscape colleague) explains, the exact nature of a bundle is usually a function of the technology used to distribute it:

the newspaper bundle, the idea of this slug of news and sports scores and classifieds and stock quotes that arrives once a day was a consequence of the printing plant. Of the metro area printing plant, of the distribution network for newspapers using trucks and newsstands and newspaper vending machines and the famous newspaper delivery boy. That newspaper bundle was based on the distribution technology of a time and place.

And when new technology emerges, the opportunity to unbundle presents itself.

I define unbundling as the creation of a narrow product for a specific sub-segment of customers, which prioritizes value over profit and is enabled by new distribution technology.

Obviously, when we talk about new distribution technology that facilitates unbundling, we are talking (at least in a modern context) about the internet, which precipitated the breakup of many of the great bundles of the 20th century – music, news, and television, among many others.

And the specific sub-segment of customers? Those are the SuperFans. And the pitch to them is straightforward – let us give you just the thing you really love, cheaper and more convenient than you are getting it today.

That pitch is particularly well-suited to come from new market entrants, which are trying to take market share away from incumbents. Startups (particularly when they’re operating in a low-interest-rate environment) don’t care about profitability. They don’t have the incentive to defend the integrity of established bundles and to remind those SuperFans that they are also CasualFans. All they want to do is design the most narrowly attractive product proposition and use it as a wedge to drive growth.

This is why I would argue that while, yes, the only two ways to make money are bundling and unbundling, it is important to understand Barksdale’s axiom within the appropriate context – bundling is about profitability, and unbundling is about growth.

Unbundling the Business

An underappreciated consequence of unbundling is that it doesn’t just lead to the disassembly of the product (music albums → individual songs) but also of the business behind the product.

This isn’t always a bad thing.

I said earlier that bundles, when done well, optimize profit-to-value for providers and their customers. The problem is that, over time, most companies tend to wreck their own bundles by over-optimizing for profit at the expense of customer value. This sometimes manifests itself in simple ways, like cable companies mindlessly passing on rising carriage fees from content producers rather than aggressively negotiating on behalf of their customers. And sometimes it manifests in more nefarious ways, like when the big five record companies conspired to raise the price of CDs in the 90s. These companies probably deserved to be unbundled!

Having said that, unbundling does have consequences that can be harmful to the broader ecosystem in ways that are often difficult to appreciate in the moment.

One of the challenges with bundles is that they obscure costs. It becomes difficult, from the outside, to tell how much of the price of a bundle is going to cover the company’s costs and how much is going to their bottom line. And as we just covered, customers have good reason not to fully trust companies’ justifications for the changing prices of their bundles.

This lack of transparency makes it easy for startups to sell customers on the idea that the price of their new, unbundled product reflects the true cost of building and delivering that offering, minus all the operational inefficiencies and profiteering of their legacy competitors.

But that’s not entirely true.

Some of the costs that disruptive companies like Spotify have stripped out are, indeed, unnecessary. Digital distribution is very cheap!

However, there are also some costs that are inherent to the creation of the products themselves, and those critical input costs now can’t be fully covered by the low, unbundled prices that customers have become accustomed to paying. Just ask musicians how they feel about Spotify!

Should You Unbundle Yourself?

The classic, Steve-Jobsian answer is yes; cannibalize yourself before someone else does.

Folks working in business strategy, particularly within the tech industry, romanticize this answer. This is what smart market incumbents are supposed to do. You either take the threat of disruption seriously (remember Jamie Dimon’s famous “Silicon Valley is coming” line?) and invest in proactively disrupting yourself, or you become a dinosaur.

While I agree with this mindset generally, I think when it comes to unbundling specifically, some caution is warranted.

There are two quick examples I want to talk about.

The first is TV.

The cable TV bundle is perhaps the most successful consumer product bundle in history. At its peak in 2011, 85% of households in the U.S. paid for TV.

Then came Netflix.

(Editor’s note – Netflix was founded in 1997 and launched its streaming service in 2007, but it wasn’t until 2011 that Netflix, as we know it today, really took off. In May of 2011, Netflix accounted for 30% of all internet streaming traffic in North America.)

As Ben Thompson points out, legacy media companies made a huge strategic shift in trying to respond to the emergence of Netflix and other streaming competitors:

Netflix is not some new phenomenon, of course. For the first half of the decade a Netflix subscription was something you obtained on top of your pay-TV subscription, and while pay-TV did start to lose a small number of subscribers — in part because Netflix was a willing buyer of all of those expensive TV shows from the Peak TV era — the decline was very gradual.

What changed over the last five years is that nearly every media company decided to compete with Netflix, instead of accommodate it. Competing with Netflix, though, meant attracting customers to sign up for a new service, instead of simply harvesting revenue from people who hooked up cable whenever they moved house, without a second thought. The former is a lot more difficult than the latter, which meant the media companies had to leverage their best stuff to attract customers: their most interesting new shows, and sometimes even their sports rights.

The results of this shift have not been pretty.

Since the Fed started raising interest rates, Wall Street has stopped rewarding media companies for growing their streaming subscriber numbers and has started pushing on the companies to cut costs and focus on profitability. And that’s exactly what the companies have been doing:

Two big names, Comcast and Disney, have said that losses in the streaming business are at a peak or reaching one this year. And Paramount Global says investment in its streaming service Paramount+ is at a high — meaning that investors can expect it will spend less in the future.

All of that could bode well for profitability, which is increasingly a focus for investors. The stock market wiped a whopping $500 billion-plus in market capitalization from the world’s biggest media, cable, and entertainment giants in 2022.

But the long-term damage has already been done.

The number of pay TV households in the U.S. is projected to drop to less than 50 million by 2027, down from 100 million in 2013. And the evisceration of the cable bundle has had a dramatic negative impact on one of the primary inputs into scripted TV:

The union representing 11,500 writers of film, television and other entertainment forms are now on strike. It’s the first writers’ strike — and the first Hollywood strike of any kind — in 15 years. Here’s a look at the storylines the fight has spawned.

Streaming and its ripple effects are at the center of the dispute. The guild says that even as series budgets have increased, writers’ share of that money has consistently shrunk.

Streaming services’ use of smaller staffs — known in the industry as “mini rooms” — for shorter stints has made sustained income harder to come by, the guild says. And the number of writers working at guild minimums has gone from about a third to about half in the past decade.

Everything became big tech — the Amazon model of ‘We don’t actually have to make money; we just have to show shareholder growth.’ Everyone said, ‘Great. That seems like the thing to do.’ Which essentially was like, ‘Let’s all commit ritual suicide. Let’s take one of the truly successful money-printing inventions in the history of the modern world — which was the carriage system with cable television — and let’s just end it and reinvent ourselves as tech companies, where we pour billions down the drain in pursuit of a return that is completely speculative, still, this many years into it.’

The contrasting example that I want to talk about is BNPL.

As I wrote about recently, credit cards are one the most ingenious product bundles in the history of the financial industry:

Credit cards work because the different groups of consumers that use them act as cross-subsidizers and risk hedges for each other. To oversimplify a bit – ‘transactors’ (those who pay their full bill every month) generate predictable, but relatively low revenue streams at a low risk. They are generally using credit cards as a combination of a debit card and a 0% interest lending facility for larger purchases. By contrast, ‘revolvers’ (those who carry a balance month-to-month) generate higher revenue streams (interchange + interest and the occasional late fee), but it is less predictable and has higher risk. They are using credit cards as rolling loans. Every credit card issuer has a slightly different strategy, in terms of the mix of customers that they target and the product levers they use to attract and incentivize behavior, but it’s all built on this mix of transactors and revolvers.

Over the last five years, driven by an incentive to grow market share at all costs, fintech companies attempted to unbundle the credit card by offering an incredibly appealing product for the credit-dependent, shopping-loving customer sub-segment – pay-in-4 BNPL:

Pay-in-4 BNPL loans have, over the last couple of years, been the closest thing in the market to free money for consumers. No interest rate. No fees (for the most part). No need for a prime or near-prime credit score. No need to worry about your credit score getting dinged up if you’re late for a payment. No need to worry about being declined because you’ve stacked up a dozen different loans from other BNPL providers.

And it has been great for merchants too! Pay-in-4 has helped them move a massive amount of merchandise ($100 billion in 2021, according to Cornerstone Advisors), much of that incremental to what they would have ordinarily sold (Shopify, which partnered with Affirm to offer BNPL, claims that merchants see a 50% increase in average order value). This is the unrealized spending that that merchants have always wanted to unlock with their customers, they just didn’t have lending partners willing to underwrite the risk … until pay-in-4 BNPL came along.

Now here’s the really interesting part – instead of reacting aggressively to the rapid growth and obvious appeal of pay-in-4 BNPL, credit card issuers mostly just stood pat.

A few of the larger issuers introduced BNPL as a feature within their credit card products, which allowed cardholders to convert transactions over a certain size, post-purchase, into fixed installment loans.

Beyond that, though? They mostly did nothing.

This was controversial! Smartass analysts like me were making fun of these banks on Twitter. Slightly-less-snarky analysts were pressuring the CEOs of these banks on earnings calls about why they weren’t taking the threat of BNPL more seriously.

Here’s how American Express’ CEO Stephen Squeri explained his company’s restrained response to BNPL:

Buy now, pay later is not really a competitive threat to us. It’s targeted at debit card issuers. As a customer acquisition vehicle it’s not the game we’re playing.

On a tactical level, that’s not really correct. As a product, BNPL is a competitive threat to credit cards, including AmEx cards. It’s free money! Delivered in an extremely convenient fashion! BNPL has almost certainly taken at least a little market share away from American Express over the last couple of years. That’s why stock market analysts were concerned.

However, on a more strategic level, Mr. Squeri’s response is exactly right. BNPL isn’t a long-term competitive threat to credit cards because, as a business, BNPL just doesn’t make a lot of sense. Its growth has been fueled by high-risk borrowers and funded by abnormally low interest rates and excessively exuberant VC investment. There is ample reason to believe that, as a standalone business, pay-in-4 BNPL will burn itself out within the next few years.

Credit card issuers can continue to just ride it out.

And you know what? Their customers won’t be mad. Customers like credit cards! According to J.D. Power, in 2022, credit card issuers saw big gains in customer satisfaction, trust, and net promoter scores. The bundle is doing just fine!

“It’s not the game we’re playing”

I hope that 30 years from now, this quote from Stephen Squeri is as well-remembered as Jim Barksdale’s quote.

What banks got right in responding to BNPL (and what media companies got wrong in responding to streaming) is recognizing that sometimes the only way to win is to not play.

Created By

Alex Johnson

Join Fintech Takes, Your One-Stop-Shop for Navigating the Fintech Universe.

Over 36,000 professionals get free emails every Monday & Thursday with highly-informed, easy-to-read analysis & insights.

No spam. Unsubscribe any time.

Events

Staying up-to-date with the fast-paced, dynamic changes in the fintech industry can be challenging! Join Alex as he demystifies our industry’s most pressing news and answers your burning questions.

Fintech moves fast. But here at Fintech Takes, Alex Johnson and his rotating panel of guests move faster so that you can stay on top of the latest and greatest news in the industry without breaking a sweat.