26 August 2022 | FinTech

Potential Winners and Losers in a Rising Rate Environment

By Alex Johnson

This happened about a month ago:

The Federal Reserve continued a sprint to reverse its easy-money policies by approving another unusually large interest rate increase and signaling more rises were likely coming to combat inflation that is running at a 40-year high. Officials agreed unanimously Wednesday to lift their benchmark federal-funds rate to a range between 2.25% and 2.5%.

Fed officials are raising rates at the most aggressive pace since the 1980s. Until last month, the central bank hadn’t raised rates by 0.75 point since 1994.

And, somewhat hilariously, the stock market actually went up immediately after because the Chairman of the Federal Reserve vaguely hinted that they might slow (not stop) these rate increases at some indeterminate point in the future:

But markets rallied after the meeting because Fed Chairman Jerome Powell offered fewer specifics about the magnitude of upcoming rate rises and hinted at an eventual slowdown.

Stocks rallied after Mr. Powell’s news conference. The S&P 500 gained 2.6% to close at 4023.61. Yields on the benchmark 10-year Treasury note fell to 2.79%.

You know you’re in for a sustained period of rising rates when the mere glimmer of a chance at a slowdown in rate increases causes market analysts to weep with relief.

And if we look a little further beyond the Fed’s next meeting in September, I think it’s reasonable to expect rates to continue to rise as the Fed attempts to reset economic conditions to a place where they can more effectively balance growth and inflation:

Market expectations of rate cuts reflect a major misunderstanding about how the central bank is likely to react to slowing growth and rising unemployment with higher inflation, said Dan Morehead, chief executive and founder of hedge-fund firm Pantera Capital.

In recent years, low inflation has given the Fed more flexibility to quickly cut rates in reaction to growth slowdowns, but officials don’t have that luxury right now because inflation is high. They are worried about consumers and businesses anticipating inflation to stay high. Economists and central bankers believe those expectations can play a fundamental role in shaping actual inflation.

“There’s no working age American who has traded [bonds] in a rising inflation environment,” said Mr. Morehead. He thinks it is possible the Fed will raise the fed-funds rate to 5% or “some number that nobody can get their head around,” he said.

This probably means that being in the business of building, selling, or financing houses is going to be kind of a bummer for a while:

The housing market, as one of the most interest-rate sensitive corners of the economy, has been the epicenter of the Fed’s effort to stimulate growth last year and to slow it this year. Prices have surged amid strong demand, but sales are slumping now as rates rise sharply.

The Mortgage Bankers Association reported Wednesday that the average 30-year fixed mortgage rate stood at 5.74% last week, holding close to 14-year highs. The National Association of Realtors separately said Wednesday that an index measuring contracts signed to purchase existing homes fell 8.6% in June from May and was 20% below the level from a year earlier.

“Right now, we’ve kind of gone from order takers to financial therapists as home builders…The buyer is a little bit in shock,” Douglas Bauer, chief executive at Nevada-based home builder Tri Pointe Homes Inc., told analysts last week.

And it also means that the Fed might, in an attempt to curb inflation, drive the economy into a recession (if we’re not already in a recession?) … or not because the economy is super weird right now:

Mr. Powell, who goes by Jay, repeated his view Wednesday that he is more concerned about the risk of failing to stamp out high inflation than about the possibility of raising rates too high and pushing the economy into a recession.

Employers have been adding jobs at a brisk pace this year, and the unemployment rate has held at 3.6%—a historically very low level—between March and June.

Mr. Powell cited job growth in dismissing concerns that the economy is currently in a recession. “I do not think the U.S. is currently in a recession,” he said. “There are just too many areas of the economy that are performing too well.”

So, to sum up:

- Interest rates seem likely to keep going up, although perhaps at a slower pace than they have been.

- Rising rates are absolutely freezing the housing and mortgage market, despite surging demand for housing across the U.S.

- The Fed’s actions may drive the economy into a recession (if we’re not already there), thus depressing consumer spending and imperiling their ability to repay all of their credit obligations.

Given all of that, I thought it might be an interesting exercise to list out some potential winners and losers in financial services in this super-fun-and-not-at-all-confusing economic environment.

Winner: Banks that have sufficient deposits to lend with and are good at lending.

Our most obvious winner – most banks!

Net interest margin (NIM) – the difference between rates paid out by banks for deposits and rates charged by banks for loans – tends to increase in a rising rate environment. NIM is the lifeblood for many banks and it has been getting squeezed relentlessly for the last few years. A rising rate environment should benefit most banks, assuming a few things:

- The bank is able to maintain sufficient deposits to fund its lending without raising interest rates too high on the deposit side. If competition heats up too fast in deposits, NIM will decrease.

- The bank isn’t overly dependent on mortgage lending or commercial real estate, which aren’t gonna do great in a rising rate environment. Community banks and credit unions do a lot of this type of lending, so they may benefit less than the bigger banks.

- The bank is able to crank up its lending while maintaining adequate loss reserves and not causing too big a spike in delinquencies. Lending is an art and the banks that are the most artful will benefit the most.

Winner: Fintech companies that are lending money and have bank charters.

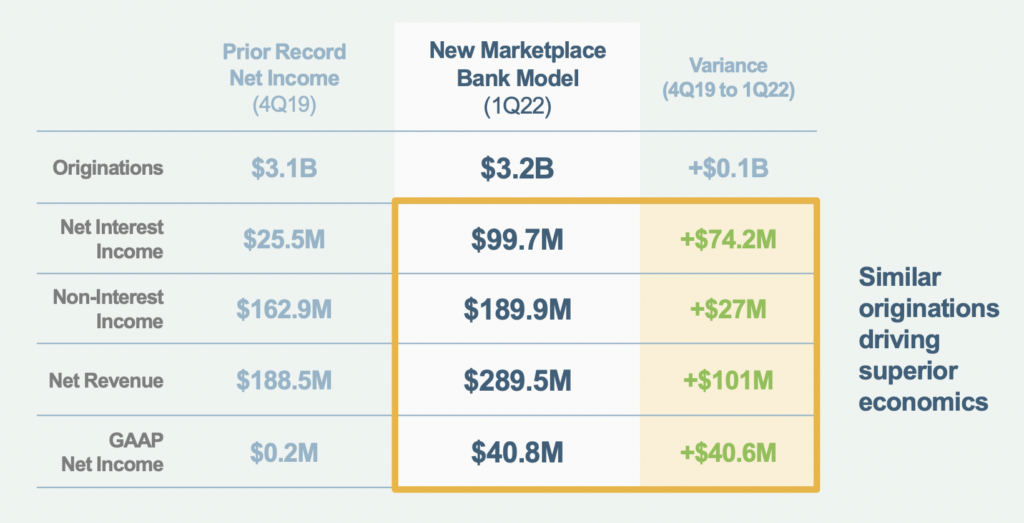

This slide from LendingClub’s Q1 2022 earnings presentation continues to blow my mind:

LendingClub’s best quarter for generating net income, prior to acquiring and fully integrating Radius Bank, was Q4 of 2019. That quarter, LendingClub originated $3.1 billion in loans and earned $200,000 in GAAP net income. In Q1 of 2022, with Radius Bank incorporated, LendingClub originated a slightly better $3.2 billion and generated a vastly better $40.8 million in GAAP net income. And if you look closely, you’ll see that the big contributor isn’t non-interest income (fees) but net interest income (NIM!).

This is why you get a bank charter.

Of course, LendingClub is subject to the same cautions I listed above for banks in this environment. I am particularly interested in how the company will innovate on the deposits side (beyond what it acquired from Radius) to maintain an ample supply of low-cost funding for its lending business. That said, the company seems well positioned to thrive over the next couple of years.

And it isn’t alone! There are other fintech companies that have managed to both acquire a bank charter and spin up a lending business.

SoFi is one to watch. The company got approval from regulators at the beginning of this year to become a chartered national bank (through the acquisition of Golden Pacific Bancorp) and, according to its Q2 2022 earnings release, that addition is already making a positive difference:

Our bank charter is enabling new flexibility that has proven even more valuable in light of the current macro environment, and the economic benefits are already starting to materialize and positively impact our operating and financial results. Deposits grew 135% during the quarter to $2.7 billion at quarter-end and have accelerated since we raised the maximum APY to 1.80% in July from 1.50% in June. As a result of this growth in high quality deposits, we have benefited from a lower cost of funding for our loans. Our deposit funding also increases our flexibility to capture additional net interest margin (NIM) and optimize returns, a critical advantage in light of notable macro uncertainty.

And finally, we have Cash App, which has, for the last couple of years, been quietly testing out a small dollar lending product – Cash App Borrow – and has recently scaled it up, seeing more than one million users borrowing funds through the app in June of 2022. These loans are not yet being originated through Square Financial Services (the ILC bank owned by Block), but that would seem like a logical next step, as would funding the loans out of the deposits being gathered by Square Financial Services.

Loser: Fintech companies that have bank charters but aren’t doing much lending.

The flip side to the LendingClub/SoFi/Cash App story is Varo.

Varo has a bank charter. It reportedly spent $100 million and three years to acquire it. It has not, however, been able to capitalize on the opportunity its charter affords it – lending off its own balance sheet – according to analysis from Jason Mikula at Fintech Business Weekly:

Varo has struggled to build a meaningful loan book by lending to its customers. In its Q1 2022 call report, it indicated about $9.4 million in credit card balances — but Varo’s card offering is secured and does not generate interest income nor significant fee income, apart from interchange.

Varo did report about $3.6 million in “other revolving” loans to customers, which, presumably, is its Varo Advance small dollar unsecured lending product — an average of less than $1 outstanding per deposit account.

Despite the small amount of lending Varo does to its own customers, it still saw about $500,000 in charge offs against these amounts in Q1 2022; its charge offs for the quarter including “all other loans” (eg, apart from those to its own customers) totaled nearly $2.2 million.

And turning this situation around is going to be extremely challenging. Here’s Jason again:

Boosting its interest income would require Varo to engage in more lending — either directly, to its own customers, or by deploying its balance sheet to purchase loans or debt securities from other issuers.

The former is difficult, as the typical Varo customer has just $83 in their account, and, presumably, skews subprime or thin/no file.

Regarding the latter, it’s likely Varo has chosen not to purchase assets originated by others, as it allows the bank to maintain a low risk capital/assets ratio — a necessity, as it remains unprofitable.

Loser: Most fintech lenders without a bank charter.

If you are a fintech lender operating without a bank charter, you need a few things to be true:

- Investment banks are willing to loan you large amounts of money at relatively low interest rates, which you will use to fund your loans.

- Partly due to the competitive rates provided by those investment banks, you are able to offer low interest rates to your customers, thus allowing you to outcompete other fintech companies and traditional banks.

- Your lending portfolio will perform about as well as you expect, and that, combined with investors’ frantic search for yield, makes it easy for you to package and sell your loans on the secondary market. The revenue generated from these sales will also go towards funding more loans.

Unfortunately, when interest rates rise, a lot of these things stop being true:

Finance companies such as Upstart Holdings Inc. and Mosaic lend money to people for purchases such as cars, solar panels and home electronics. But they have to borrow the money they lend out to consumers—and that is becoming increasingly expensive as the Federal Reserve continues to raise interest rates aggressively.

The lenders’ use of artificial intelligence to find and approve large numbers of borrowers quickly made them popular among stock and bond buyers when markets soared last year. Now they are falling out of favor.

Investors have been selling out of asset-backed bonds issued by the finance companies, and some banks and credit unions have stopped buying the loans they make. That has pushed funding costs even higher.

I should note that not every non-bank fintech lender will be impacted by rising rates with equal severity. Those that focus on mortgage lending, mortgage refinance, and large dollar unsecured installment lending (which is used chiefly for refi) will be especially challenged as rising rates make their products less appealing to consumers (in addition to the funding challenges outlined above).

I’m cautiously optimistic that the big BNPL providers might do OK in this environment. Thanks to the fees they generate from their merchant partners, BNPL providers aren’t dependent on net interest income (in fact, most BNPL loans don’t charge any interest). Additionally, the potential for massive loan losses is comparatively smaller in BNPL than for other lending categories because the loans themselves are primarily low-dollar and short-term.

Slight Winner: Fintech infrastructure companies that help lenders collect on delinquent debt.

The irony of the collections business, which companies like TrueAccord understand very well, is that lenders typically don’t invest in loan servicing and collections technology when credit conditions are good, and lenders are thriving. That investment often doesn’t happen until the credit cycle starts to turn and lenders realize they’re about to be swamped with delinquencies, which is, of course, too late for that investment to make a difference in the short term.

Looking at the data, it’s a bit unclear to me how likely we are to see a major uptick in loan delinquencies in the next few quarters (which would spur more investments in collections). Consumers aren’t saving. Spending on credit cards is up. Lenders are increasing loss reserves, but they’re also significantly ramping up their customer acquisition efforts. And consumers’ capacity for handling increased debt seems like it might still be pretty good, given the low level of unemployment?

I don’t know. The economy is weird right now.

Slight Loser: BaaS platforms.

BaaS platforms exist to balance out supply and demand. They bring fintech partners to banks that are looking to make money by loaning out their charters and they bring banks to fintech companies that are looking to offer financial products.

I’m not overly worried about a rising rate environment impacting the demand for partner banks. Despite a recent deceleration in funding, fintech companies that need bank partners will keep being founded and any slowdown on the fintech side will likely be balanced out by increasing demand for bank partners by non-finance brands interested in embedded finance.

However, I think it’s possible that this rising rate environment, combined with a recent increase in regulatory scrutiny, might cause community banks to cool a bit on BaaS, which would impact the supply of bank partners available to BaaS platforms. I don’t know that this would cause any immediate problems for the BaaS platforms, which all already have multiple bank partners signed up, but it bears watching.

Slight Winner: Banks already doing BaaS.

The inverse of the BaaS platform concern – might a slowdown in community bank enthusiasm for BaaS give banks that are already doing BaaS a little more breathing room, competitively speaking?

Toss-Up: LaaS and CCaaS platforms.

I can make the case both ways on this one.

I think that lending-as-a-service and credit-card-as-a-service platforms will become significantly more popular as neobanks move from checking accounts and debit cards to credit cards and installment loans. The pressure to achieve profitability (or, at least, positive unit economics) will help drive this shift, and these platforms stand to benefit.

On the other hand, lending is riskier and less profitable than it was a year ago. And LaaS and CCaaS platforms can’t do much to solve the funding challenge that all non-bank lenders are now facing.

This one is a toss-up.

Slight Winner: High-yield savings accounts.

Are high-yield savings accounts about to make a comeback? Will they once again become a wedge product for fintech startups? Will traditional banks try to box fintech companies out of the deposits space by pouring a little bit of that net interest income back into more aggressive pricing?

It seems distinctly possible to me!

My only caution would be that savings products are usually much more attractive to consumers during a recession or economic downturn. In that type of environment, you typically see a ‘flight to safety’ wherein consumers shift a lot of their money out of riskier investments and into savings (we saw this at the start of the pandemic).

But if this weird economy of ours doesn’t break all the way bad, we may not see that flight to safety.

Slight Loser: Investing platforms.

The inverse of the high-yield savings argument – if a worsening economy does cause a flight to safety among consumers, investing platforms, particularly the high-risk/high-reward active trading platforms like Robinhood, will see an increased outflow of assets and reduced trading activity.

Given the trajectory that Robinhood is already on, this would be very bad news.

Slight Winner: More creative fintech lending products.

Fintech has pushed lending in some very interesting directions.

We have income share agreements (ISAs), which tie loan payments to income, allowing consumers to reduce or even eliminate their payments if their income decreases or they lose their job. These loans are often, but not exclusively, made to help finance the costs of higher education.

We have home equity investment products, which allow consumers to sell a portion of the equity in their home in exchange for cash without having to take out a loan or pay interest at all.

And we even have a credit card for subprime consumers that is secured by the equity those consumers have in their cars.

I have plenty of concerns about these products, which I will elaborate on in a future newsletter. However, I do think these products have the potential to be more competitive in a rising rate environment because of the creative ways in which they reduce borrowing costs for consumers.

They will still face the same loan funding struggles that other non-bank fintech lenders face, so I am only ranking them as a slight winner here.

Winner: Corporate card and expense management providers.

Corporate credit cards aren’t an obvious winner in a rising rate environment, as the same funding and credit risk concerns apply to this product category.

However, most providers in this space have built out expense management software to complement their core card and banking products. This software aims to help businesses get a much better handle on their expenses, which is a value proposition that seems to be resonating in the current market.

Ramp is a good case study:

Despite a cooling market, corporate spend management startup Ramp reports that it has more than doubled its revenue run rate since the start of the year.

“We believe that Ramp’s ability to help its customers spend 3.5% less is uniquely appealing and valuable to businesses in this macroeconomic climate,” [Eric] Glyman [CEO of Ramp] said.

“Our biggest hope is to go to work for more companies that are looking to cut costs, become efficient and do it in ways that improve the quality of the business, while preserving the ability to make investments and support people and staff,” he told TechCrunch in an interview.